Bunge Global (BG)

We’re cautious of Bunge Global. Its plummeting sales and returns on capital show its profits are shrinking as demand fizzles out.― StockStory Analyst Team

1. News

2. Summary

Why We Think Bunge Global Will Underperform

With origins dating back to 1818 and operations spanning both hemispheres to balance seasonal harvests, Bunge Global (NYSE:BG) is an agribusiness and food company that processes oilseeds, grains, and other agricultural commodities into vegetable oils, protein meals, flours, and specialty ingredients.

- Annual sales declines of 3.7% for the past three years show its products struggled to connect with the market

- Easily substituted products (and therefore stiff competition) result in an inferior gross margin of 6.1% that must be offset through higher volumes

- Limited cash reserves may force the company to seek unfavorable financing terms that could dilute shareholders

Bunge Global’s quality is inadequate. More profitable opportunities exist elsewhere.

Why There Are Better Opportunities Than Bunge Global

Bunge Global is trading at $116.89 per share, or 14.4x forward P/E. This multiple is cheaper than most consumer staples peers, but we think this is justified.

Cheap stocks can look like great bargains at first glance, but you often get what you pay for. These mediocre businesses often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. Bunge Global (BG) Research Report: Q4 CY2025 Update

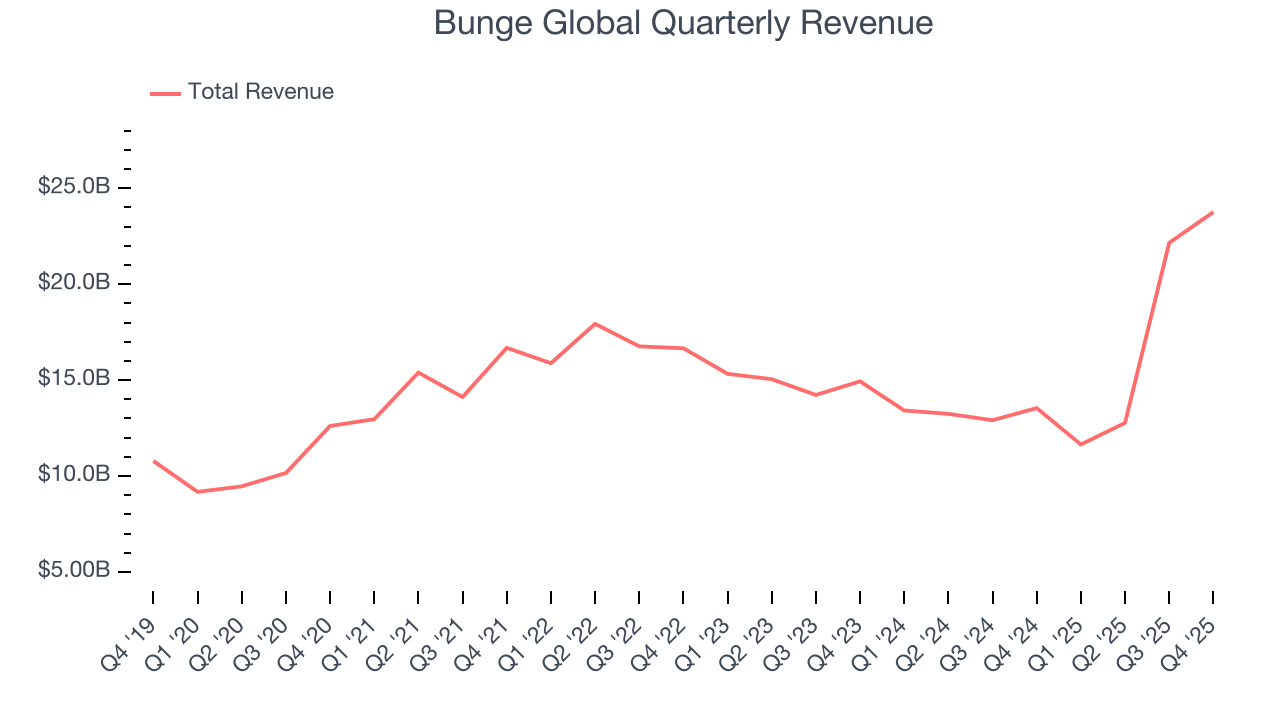

Global agribusiness company Bunge Global (NYSE:BG) announced better-than-expected revenue in Q4 CY2025, with sales up 75.5% year on year to $23.76 billion. Its non-GAAP profit of $1.99 per share was 9.6% above analysts’ consensus estimates.

Bunge Global (BG) Q4 CY2025 Highlights:

- Revenue: $23.76 billion vs analyst estimates of $22.39 billion (75.5% year-on-year growth, 6.1% beat)

- Adjusted EPS: $1.99 vs analyst estimates of $1.82 (9.6% beat)

- Adjusted EBITDA: $563 million vs analyst estimates of $846.4 million (2.4% margin, 33.5% miss)

- Adjusted EPS guidance for the upcoming financial year 2026 is $7.75 at the midpoint, missing analyst estimates by 13.3%

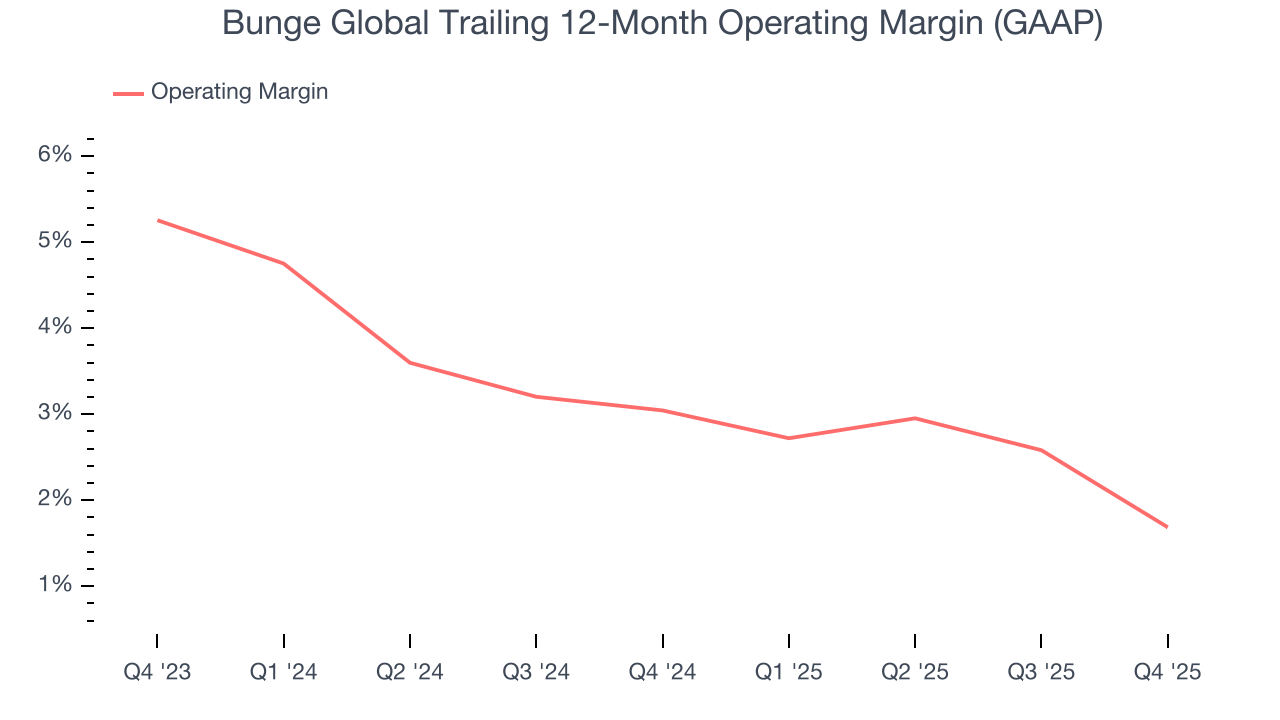

- Operating Margin: 1.1%, down from 4.7% in the same quarter last year

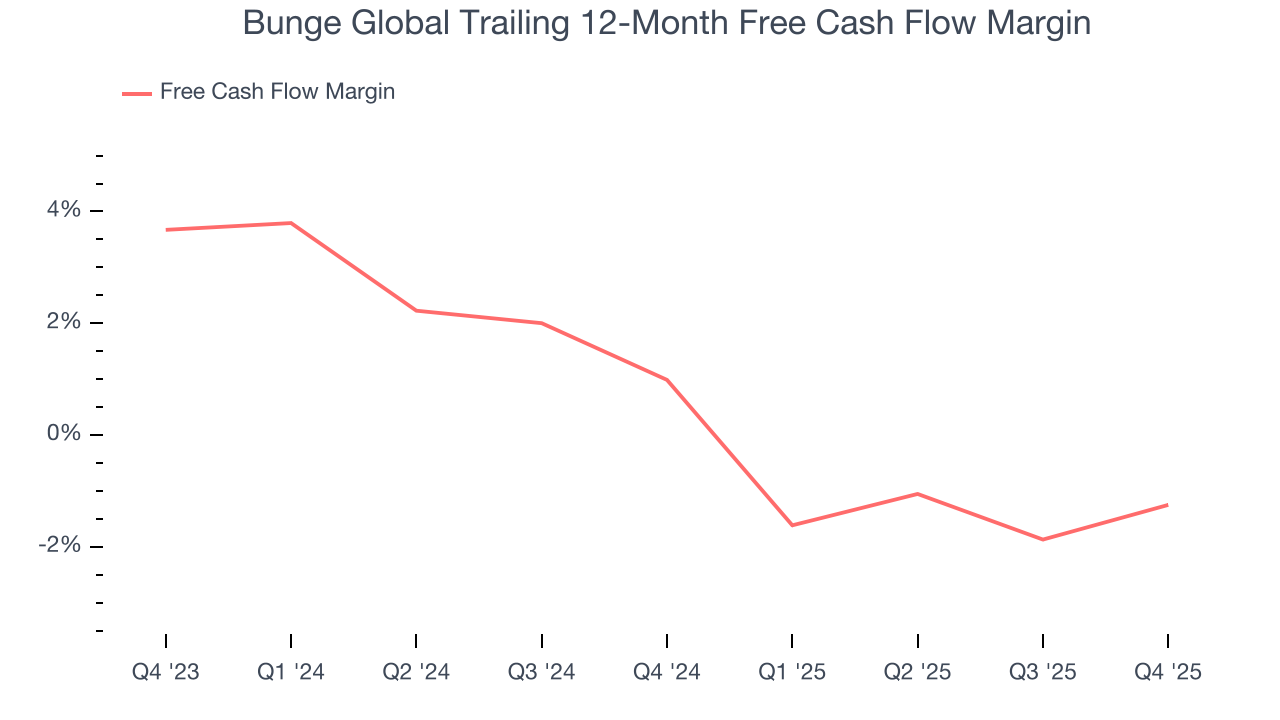

- Free Cash Flow Margin: 3.4%, similar to the same quarter last year

- Market Capitalization: $22.61 billion

Company Overview

With origins dating back to 1818 and operations spanning both hemispheres to balance seasonal harvests, Bunge Global (NYSE:BG) is an agribusiness and food company that processes oilseeds, grains, and other agricultural commodities into vegetable oils, protein meals, flours, and specialty ingredients.

Bunge's operations are organized into core segments: Agribusiness, Refined and Specialty Oils, and Milling. In its Agribusiness segment, the company purchases, stores, processes, and sells agricultural commodities worldwide, with processing facilities strategically distributed across North America, South America, Europe, and Asia-Pacific. This global footprint allows Bunge to manage supply chain risks and take advantage of different growing seasons.

The Refined and Specialty Oils segment produces both consumer-packaged products and bulk oils used by food manufacturers and renewable diesel producers. Bunge owns notable consumer brands including Soya in Brazil and Venusz, Kujawski, and Dalda in various international markets. The company's specialty oils and fats are ingredients in countless food products, from baked goods to confectionery.

In its Milling segment, Bunge produces wheat flours and bakery mixes in Brazil under brands like Suprema and Soberana, and corn-based products in North America. These products serve food processors, bakeries, and food service companies.

Bunge's integrated business model creates synergies across segments through shared raw material procurement, logistics, risk management, and co-located facilities. The company also offers financial services including trade structured finance and risk management to agricultural producers and end users, helping secure commodity supplies while managing price volatility.

4. Ingredients, Flavors & Fragrances

Ingredients, flavors, and fragrances companies supply essential components to food, beverage, personal care, and household product manufacturers. These firms develop proprietary formulations that enhance taste, scent, and texture, creating customer stickiness through specialized expertise and regulatory-approved ingredient portfolios. Tailwinds include growing consumer demand for natural and clean-label products, expansion in emerging markets, and innovation in plant-based and functional ingredients. However, headwinds persist from volatile raw material costs, particularly for agricultural and petrochemical inputs. Regulatory scrutiny over synthetic additives and fragrance allergens poses compliance challenges, while consolidation among major customers increases pricing pressure and negotiating leverage against suppliers.

Bunge Global's primary competitors include Archer Daniels Midland (NYSE:ADM), Cargill Incorporated (privately held), Louis Dreyfus Company (privately held), Wilmar International (SGX:F34), and COFCO International (part of state-owned COFCO Group).

5. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

With $70.33 billion in revenue over the past 12 months, Bunge Global is one of the most widely recognized consumer staples companies. Its influence over consumers gives it negotiating leverage with distributors, enabling it to pick and choose where it sells its products (a luxury many don’t have). However, its scale is a double-edged sword because there are only so many big store chains to sell into, making it harder to find incremental growth. To accelerate sales, Bunge Global likely needs to optimize its pricing or lean into new products and international expansion.

As you can see below, Bunge Global’s sales grew at a sluggish 1.5% compounded annual growth rate over the last three years. This shows it failed to generate demand in any major way and is a rough starting point for our analysis.

This quarter, Bunge Global reported magnificent year-on-year revenue growth of 75.5%, and its $23.76 billion of revenue beat Wall Street’s estimates by 6.1%.

Looking ahead, sell-side analysts expect revenue to grow 33.6% over the next 12 months, an acceleration versus the last three years. This projection is eye-popping for a company of its scale and implies its newer products will spur better top-line performance.

6. Gross Margin & Pricing Power

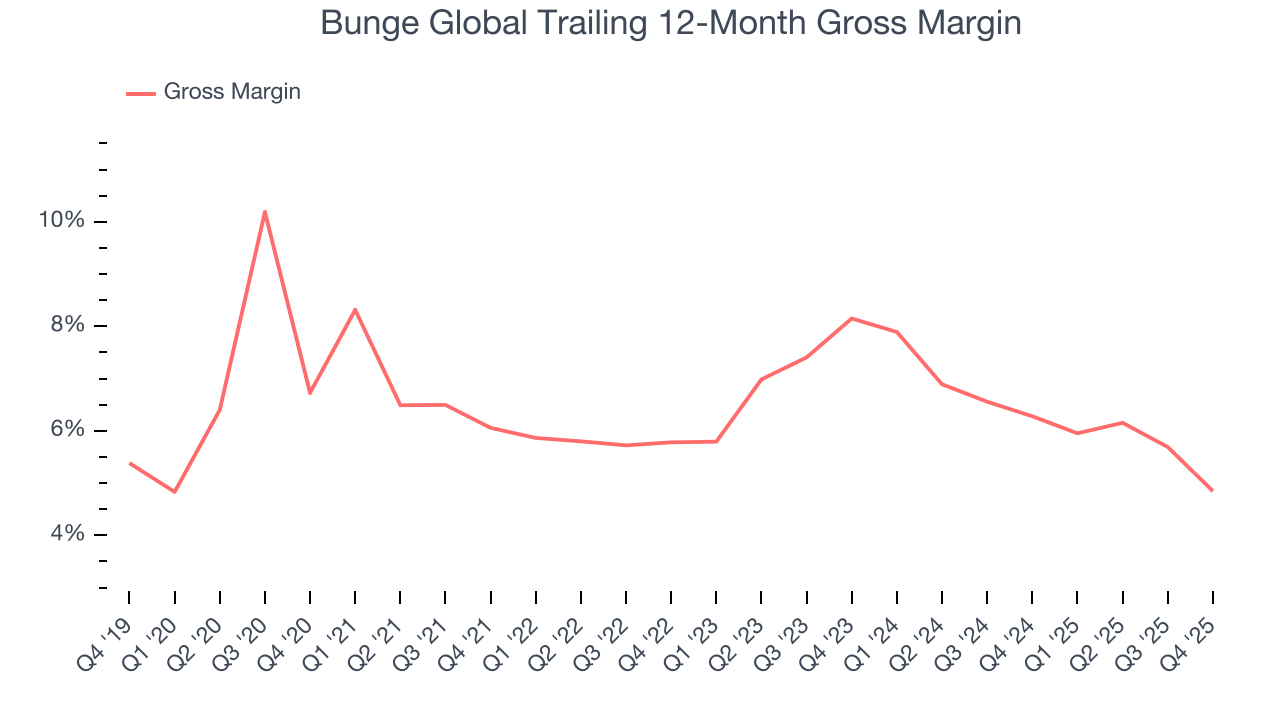

Bunge Global has bad unit economics for a consumer staples company, signaling it operates in a competitive market and lacks pricing power because its products can be substituted. As you can see below, it averaged a 5.5% gross margin over the last two years. Said differently, for every $100 in revenue, a chunky $94.54 went towards paying for raw materials, production of goods, transportation, and distribution.

In Q4, Bunge Global produced a 4.3% gross profit margin, marking a 3.3 percentage point decrease from 7.6% in the same quarter last year. Bunge Global’s full-year margin has also been trending down over the past 12 months, decreasing by 1.4 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to lower prices and higher input costs (such as raw materials and manufacturing expenses).

7. Operating Margin

Operating margin is a key profitability metric because it accounts for all expenses enabling a business to operate smoothly, including marketing and advertising, IT systems, wages, and other administrative costs.

Bunge Global was profitable over the last two years but held back by its large cost base. Its average operating margin of 2.3% was weak for a consumer staples business. This result isn’t too surprising given its low gross margin as a starting point.

Looking at the trend in its profitability, Bunge Global’s operating margin decreased by 1.4 percentage points over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Bunge Global’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, Bunge Global generated an operating margin profit margin of 1.1%, down 3.5 percentage points year on year. Since Bunge Global’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, and administrative overhead increased.

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

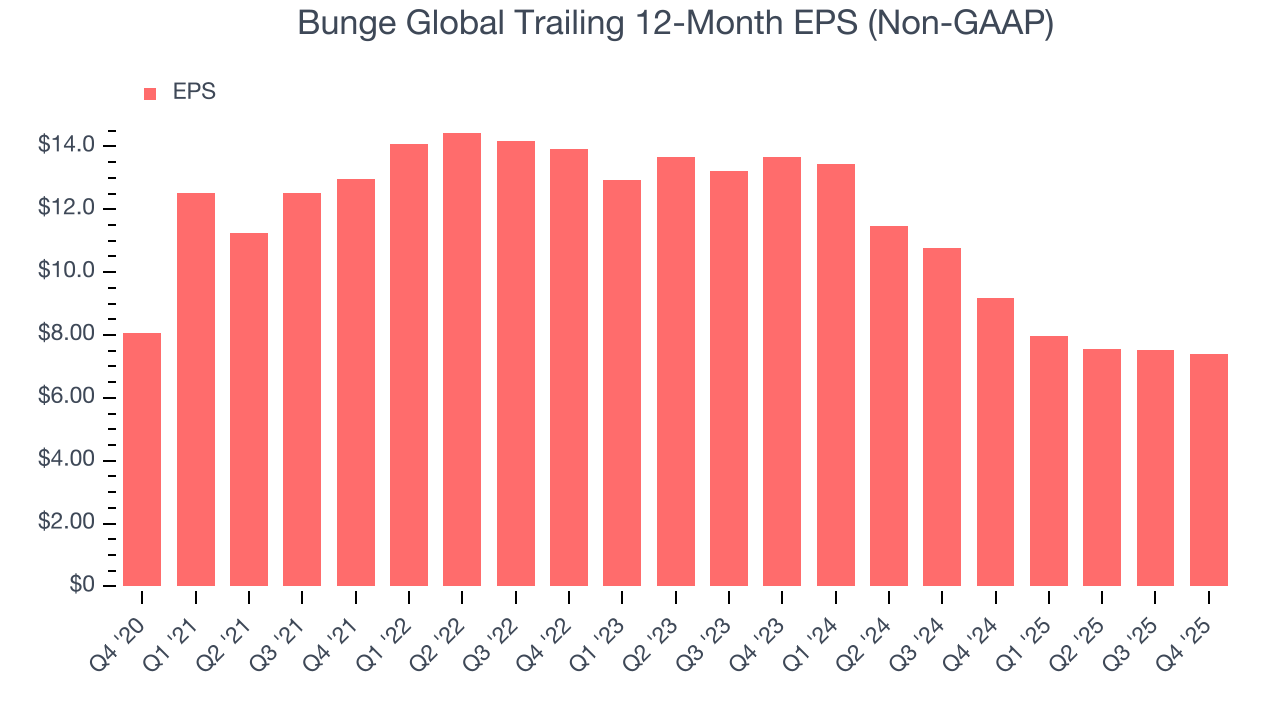

Sadly for Bunge Global, its EPS declined by 19.1% annually over the last three years while its revenue grew by 1.5%. This tells us the company became less profitable on a per-share basis as it expanded.

In Q4, Bunge Global reported adjusted EPS of $1.99, down from $2.13 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 9.6%. Over the next 12 months, Wall Street expects Bunge Global’s full-year EPS of $7.38 to grow 20.1%.

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Bunge Global broke even from a free cash flow perspective over the last two years, giving the company limited opportunities to return capital to shareholders.

Taking a step back, we can see that Bunge Global’s margin dropped by 2.2 percentage points over the last year. Almost any movement in the wrong direction is undesirable because of its already low cash conversion. If the trend continues, it could signal it’s in the middle of an investment cycle.

Bunge Global’s free cash flow clocked in at $809 million in Q4, equivalent to a 3.4% margin. This cash profitability was in line with the comparable period last year and above its two-year average.

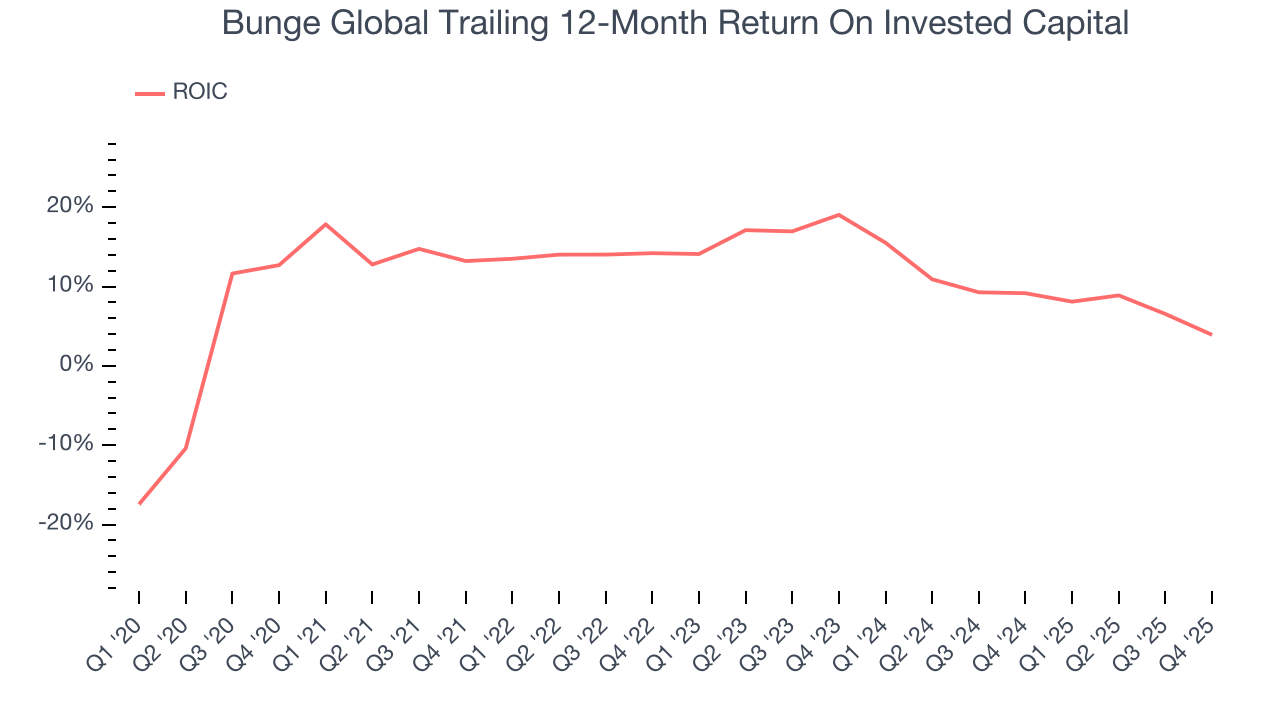

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Bunge Global’s management team makes decent investment decisions and generates value for shareholders. Its five-year average ROIC was 11.9%, slightly better than typical consumer staples business.

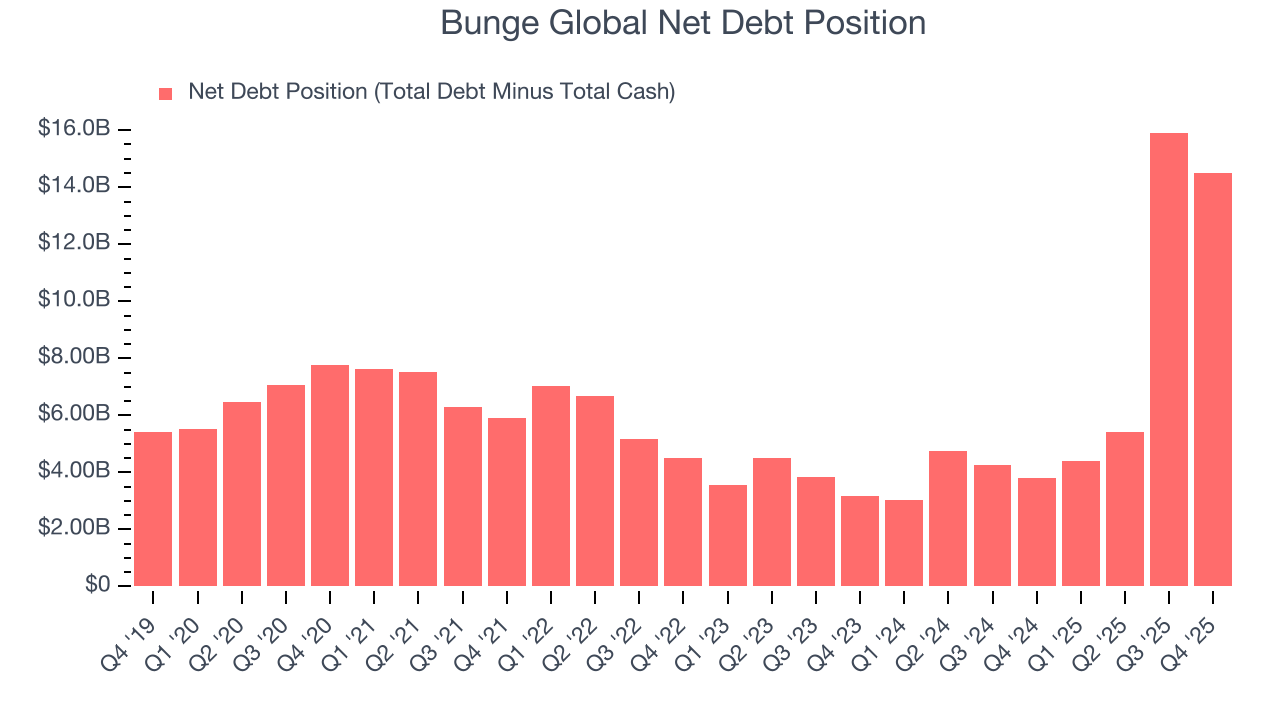

11. Balance Sheet Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

Bunge Global burned through $879 million of cash over the last year, and its $15.65 billion of debt exceeds the $1.14 billion of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

Unless the Bunge Global’s fundamentals change quickly, it might find itself in a position where it must raise capital from investors to continue operating. Whether that would be favorable is unclear because dilution is a headwind for shareholder returns.

We remain cautious of Bunge Global until it generates consistent free cash flow or any of its announced financing plans materialize on its balance sheet.

12. Key Takeaways from Bunge Global’s Q4 Results

We were impressed by how significantly Bunge Global blew past analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its full-year EPS guidance missed and its EBITDA fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 4.3% to $111.87 immediately after reporting.

13. Is Now The Time To Buy Bunge Global?

Updated: February 4, 2026 at 6:23 AM EST

Before making an investment decision, investors should account for Bunge Global’s business fundamentals and valuation in addition to what happened in the latest quarter.

Bunge Global isn’t a terrible business, but it doesn’t pass our quality test. For starters, its revenue growth was weak over the last three years. And while its unparalleled brand awareness makes it a household name consumers consistently turn to, the downside is its declining EPS over the last three years makes it a less attractive asset to the public markets. On top of that, its gross margins make it more challenging to reach positive operating profits compared to other consumer staples businesses.

Bunge Global’s P/E ratio based on the next 12 months is 13.2x. While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're fairly confident there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $110.90 on the company (compared to the current share price of $111.87).