Bausch + Lomb (BLCO)

We aren’t fans of Bausch + Lomb. Its poor returns on capital indicate it barely generated any profits, a must for high-quality companies.― StockStory Analyst Team

1. News

2. Summary

Why We Think Bausch + Lomb Will Underperform

With a nearly 170-year history dedicated to vision care and eye health innovation, Bausch + Lomb (NYSE:BLCO) develops and manufactures a comprehensive range of eye health products including contact lenses, pharmaceuticals, surgical devices, and consumer eye care solutions.

- Falling earnings per share over the last three years has some investors worried as stock prices ultimately follow EPS over the long term

- Low returns on capital reflect management’s struggle to allocate funds effectively

- High net-debt-to-EBITDA ratio of 5× could force the company to raise capital at unfavorable terms if market conditions deteriorate

Bausch + Lomb’s quality doesn’t meet our expectations. We see more favorable opportunities in the market.

Why There Are Better Opportunities Than Bausch + Lomb

Bausch + Lomb’s stock price of $15.37 implies a valuation ratio of 20.5x forward P/E. This multiple is quite expensive for the quality you get.

It’s better to pay up for high-quality businesses with strong long-term earnings potential rather than to buy lower-quality companies with open questions and big downside risks.

3. Bausch + Lomb (BLCO) Research Report: Q4 CY2025 Update

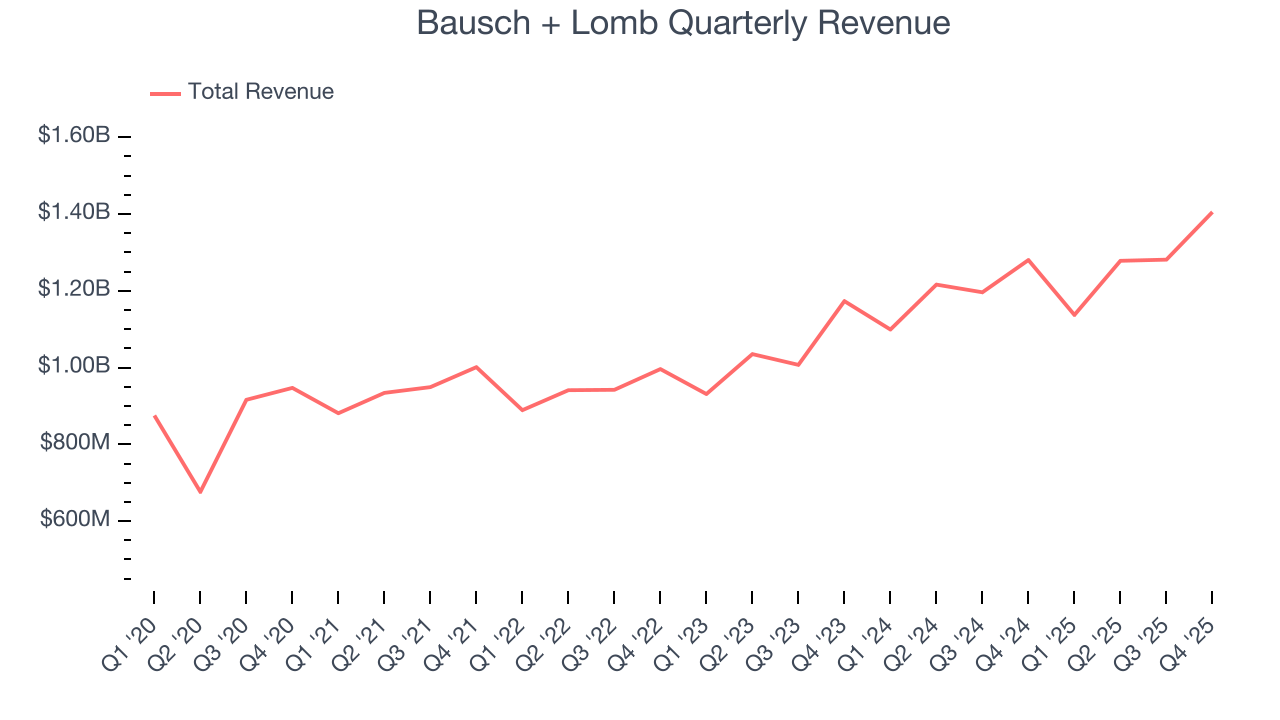

Eyecare company Bausch + Lomb (NYSE:BLCO) announced better-than-expected revenue in Q4 CY2025, with sales up 9.8% year on year to $1.41 billion. The company’s full-year revenue guidance of $5.43 billion at the midpoint came in 0.7% above analysts’ estimates. Its non-GAAP profit of $0.32 per share was 10.3% below analysts’ consensus estimates.

Bausch + Lomb (BLCO) Q4 CY2025 Highlights:

- Revenue: $1.41 billion vs analyst estimates of $1.38 billion (9.8% year-on-year growth, 1.5% beat)

- Adjusted EPS: $0.32 vs analyst expectations of $0.36 (10.3% miss)

- Adjusted EBITDA: $330 million vs analyst estimates of $320.7 million (23.5% margin, 2.9% beat)

- EBITDA guidance for the upcoming financial year 2026 is $1.03 billion at the midpoint, above analyst estimates of $1.01 billion

- Operating Margin: 8%, up from 6.8% in the same quarter last year

- Free Cash Flow was $60 million, up from -$70 million in the same quarter last year

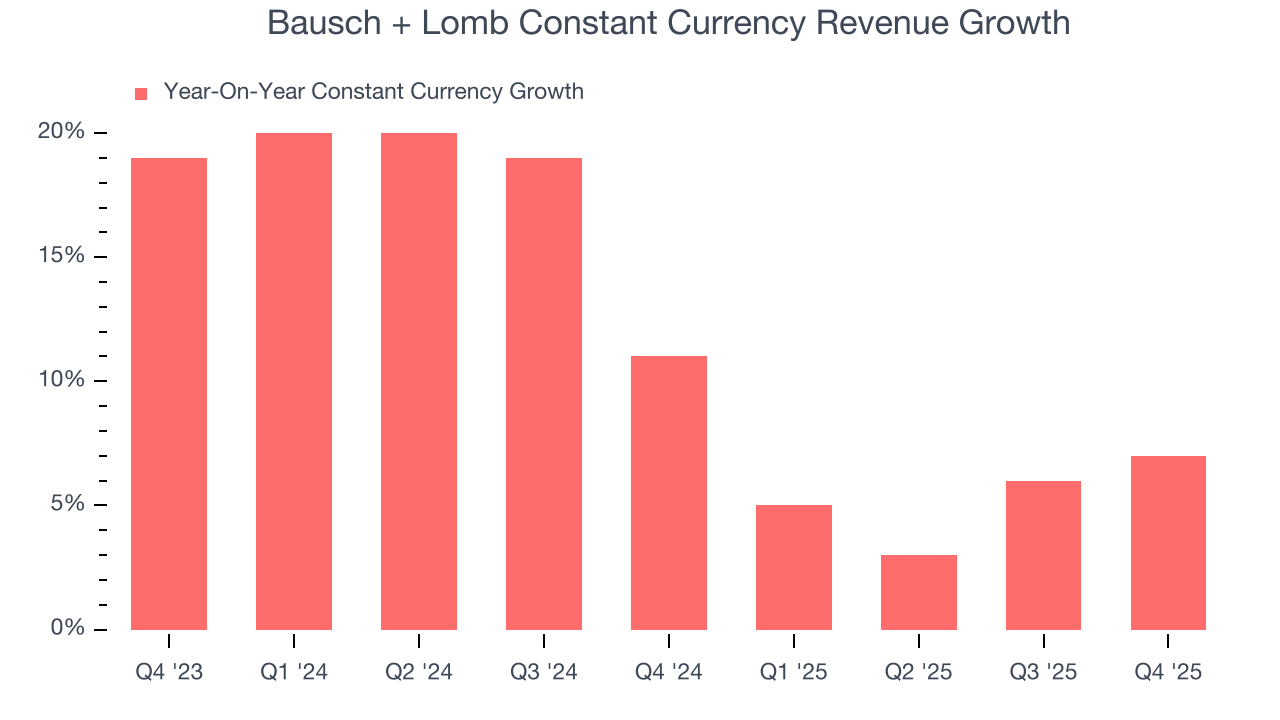

- Constant Currency Revenue rose 7% year on year (11% in the same quarter last year)

- Market Capitalization: $6.53 billion

Company Overview

With a nearly 170-year history dedicated to vision care and eye health innovation, Bausch + Lomb (NYSE:BLCO) develops and manufactures a comprehensive range of eye health products including contact lenses, pharmaceuticals, surgical devices, and consumer eye care solutions.

Bausch + Lomb operates through three distinct business segments: Vision Care, Ophthalmic Pharmaceuticals, and Surgical. The Vision Care segment includes both consumer eye care products and contact lenses. Consumer products range from vitamin supplements like PreserVision AREDS 2 for age-related macular degeneration to lens care solutions such as Biotrue and Renu, as well as over-the-counter eye drops like LUMIFY for redness relief. The contact lens portfolio features daily disposables like Bausch + Lomb INFUSE and monthly options like Bausch + Lomb ULTRA with specialized designs for conditions such as astigmatism and presbyopia.

The Ophthalmic Pharmaceuticals segment provides prescription medications for various eye conditions. XIPERE treats macular edema associated with uveitis, while Vyzulta reduces intraocular pressure in glaucoma patients. Other key products include Lotemax for post-operative inflammation and Besivance for bacterial conjunctivitis.

In the Surgical segment, Bausch + Lomb offers equipment, implantables, and consumables for eye surgeries. The Stellaris Elite system provides a platform for both cataract and vitreoretinal procedures. The VICTUS femtosecond laser assists in cataract and corneal refractive surgeries. The company also manufactures intraocular lenses (IOLs) that replace the eye's natural lens during cataract surgery, including brands like enVista and Crystalens.

Bausch + Lomb generates revenue through direct sales to eye care professionals, hospitals, and surgical centers, as well as through retail channels and distributors. The company maintains a global presence with products marketed in approximately 100 countries, supported by a network of sales representatives and distribution partners. Its business model combines selling high-volume consumer products through retail channels while also providing specialized medical devices and pharmaceuticals to healthcare providers.

The company invests in research and development to expand its product portfolio and address unmet needs in eye health. Bausch + Lomb holds hundreds of patents covering its technologies, though it operates in a competitive landscape where continuous innovation is essential to maintain market position.

4. Medical Devices & Supplies - Specialty

The medical devices industry operates a business model that balances steady demand with significant investments in innovation and regulatory compliance. The industry benefits from recurring revenue streams tied to consumables, maintenance services, and incremental upgrades to the latest technologies, although specialty devices are more niche. The capital-intensive nature of product development, coupled with lengthy regulatory pathways and the need for clinical validation, can weigh on profitability and timelines. In addition, there are constant pricing pressures from healthcare systems and insurers maximizing cost efficiency. Over the next several years, one tailwind is demographic–aging populations means rising chronic disease rates that drive greater demand for medical interventions and monitoring solutions. Advances in digital health, such as remote patient monitoring and smart devices, are also expected to unlock new demand by shortening upgrade cycles. On the other hand, the industry faces headwinds from pricing and reimbursement pressures as healthcare providers increasingly adopt value-based care models. Additionally, the integration of cybersecurity for connected devices adds further risk and complexity for device manufacturers.

Bausch + Lomb competes with several major eye health companies including Johnson & Johnson Vision (NYSE:JNJ), Alcon (NYSE:ALC), and Cooper Companies (NYSE:COO) in the contact lens and surgical markets. In pharmaceuticals, it faces competition from Novartis (NYSE:NVS), Regeneron (NASDAQ:REGN), and AbbVie's Allergan (NYSE:ABBV). The consumer eye care segment competes with Prestige Consumer Healthcare (NASDAQ:PBH) and private label brands.

5. Economies of Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With $5.1 billion in revenue over the past 12 months, Bausch + Lomb has decent scale. This is important as it gives the company more leverage in a heavily regulated, competitive environment that is complex and resource-intensive.

6. Revenue Growth

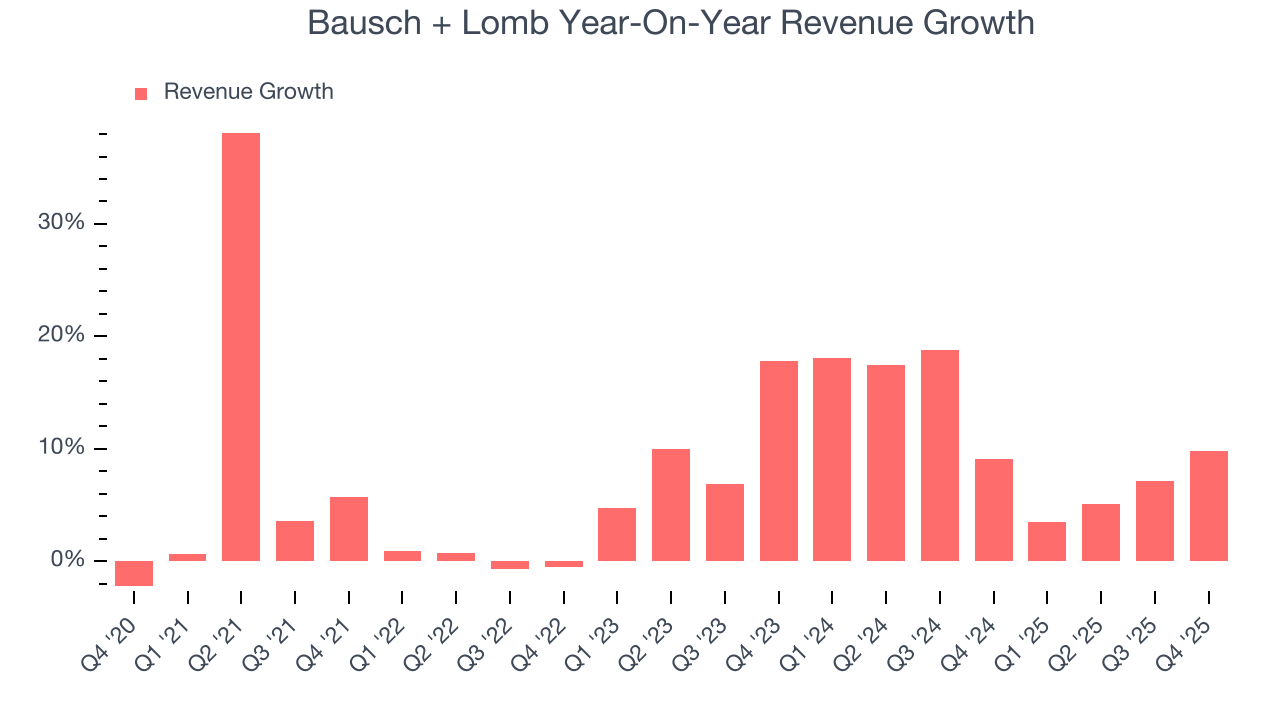

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, Bausch + Lomb’s 8.4% annualized revenue growth over the last five years was decent. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Bausch + Lomb’s annualized revenue growth of 10.9% over the last two years is above its five-year trend, suggesting some bright spots.

We can dig further into the company’s sales dynamics by analyzing its constant currency revenue, which excludes currency movements that are outside their control and not indicative of demand. Over the last two years, its constant currency sales averaged 11.4% year-on-year growth. Because this number aligns with its normal revenue growth, we can see that Bausch + Lomb has properly hedged its foreign currency exposure.

This quarter, Bausch + Lomb reported year-on-year revenue growth of 9.8%, and its $1.41 billion of revenue exceeded Wall Street’s estimates by 1.5%.

Looking ahead, sell-side analysts expect revenue to grow 6.5% over the next 12 months, a deceleration versus the last two years. Despite the slowdown, this projection is above the sector average and indicates the market is forecasting some success for its newer products and services.

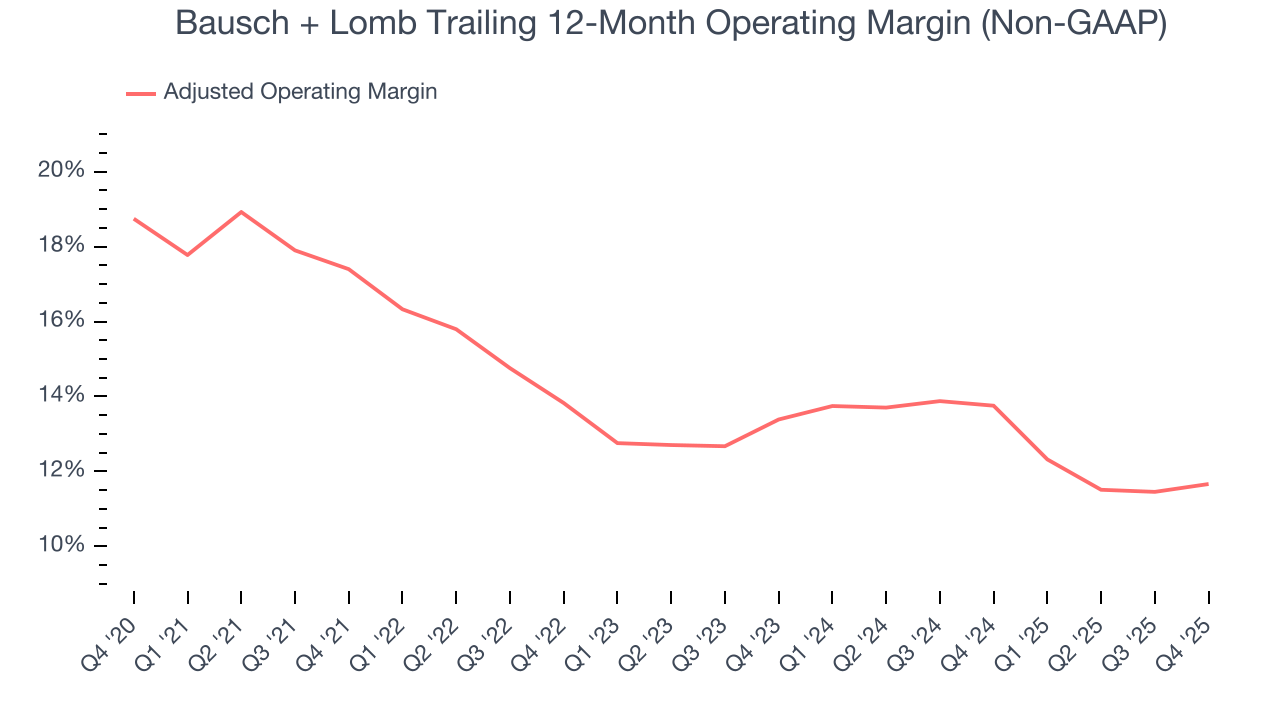

7. Adjusted Operating Margin

Bausch + Lomb has done a decent job managing its cost base over the last five years. The company has produced an average adjusted operating margin of 13.8%, higher than the broader healthcare sector.

Analyzing the trend in its profitability, Bausch + Lomb’s adjusted operating margin decreased by 5.7 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 1.7 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

In Q4, Bausch + Lomb generated an adjusted operating margin profit margin of 15.9%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

8. Earnings Per Share

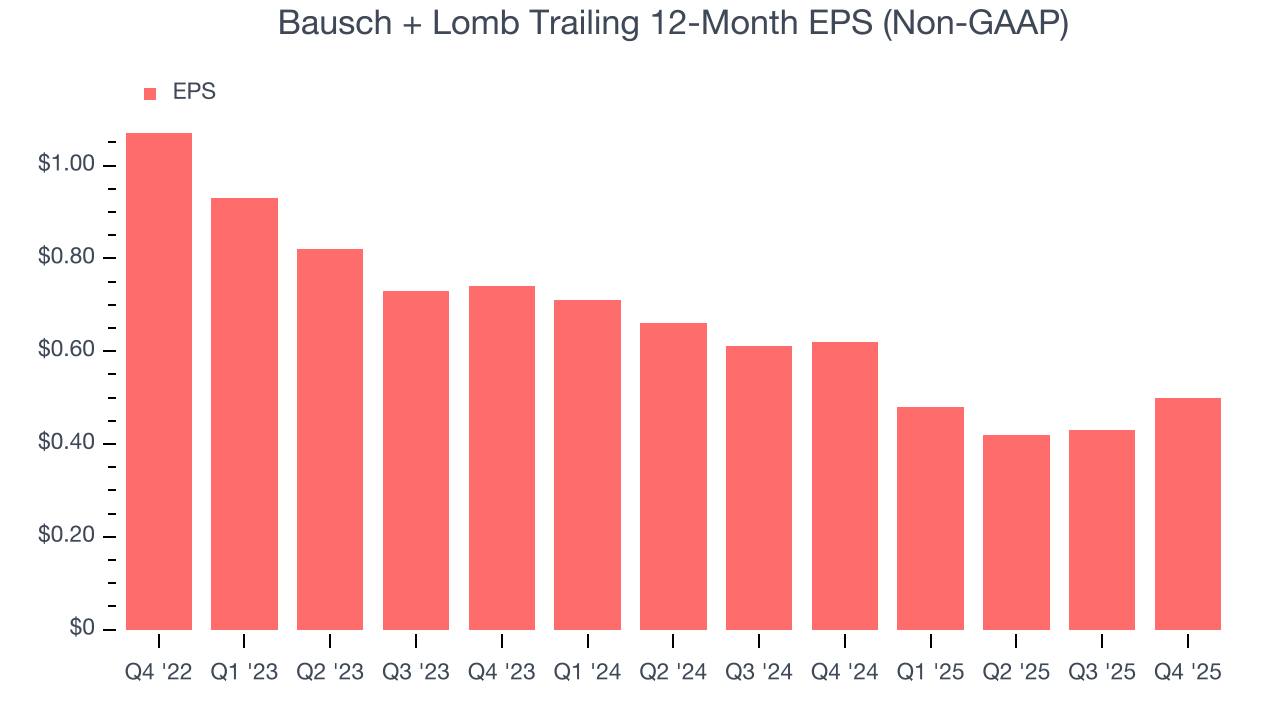

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Bausch + Lomb’s full-year EPS dropped significantly over the last three years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Bausch + Lomb’s low margin of safety could leave its stock price susceptible to large downswings.

In Q4, Bausch + Lomb reported adjusted EPS of $0.32, up from $0.25 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates. Over the next 12 months, Wall Street expects Bausch + Lomb’s full-year EPS of $0.50 to grow 53.4%.

9. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

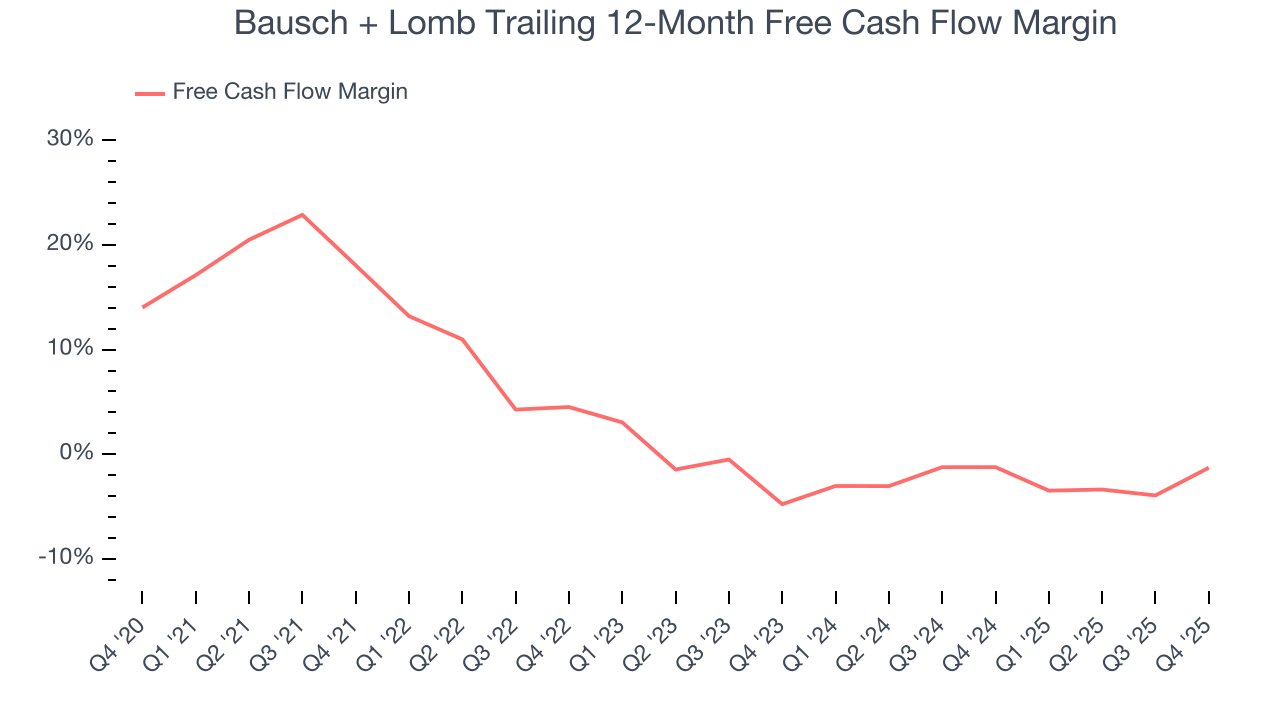

Bausch + Lomb has shown mediocre cash profitability over the last five years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 2.4%, subpar for a healthcare business.

Taking a step back, we can see that Bausch + Lomb’s margin dropped by 19.4 percentage points during that time. Almost any movement in the wrong direction is undesirable because of its already low cash conversion. If the trend continues, it could signal it’s becoming a more capital-intensive business.

Bausch + Lomb’s free cash flow clocked in at $60 million in Q4, equivalent to a 4.3% margin. Its cash flow turned positive after being negative in the same quarter last year, but we wouldn’t put too much weight on the short term because investment needs can be seasonal, causing temporary swings. Long-term trends are more important.

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

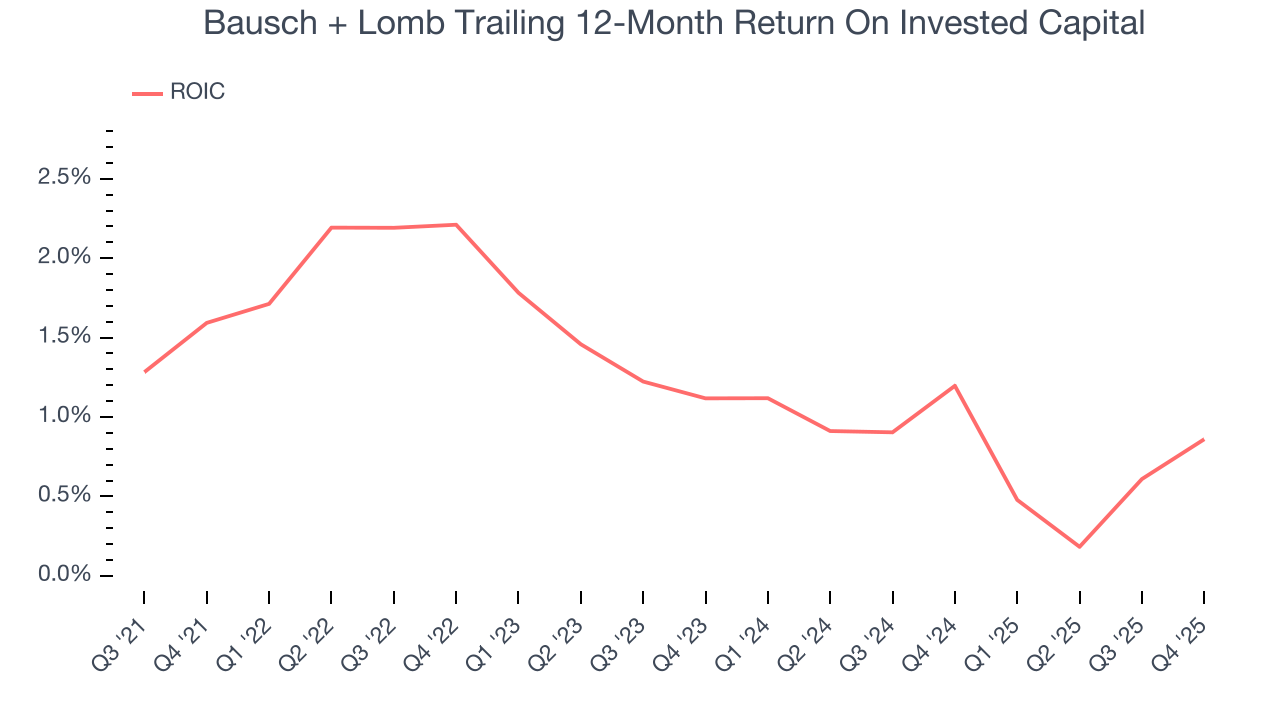

Bausch + Lomb historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 1.4%, lower than the typical cost of capital (how much it costs to raise money) for healthcare companies.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Bausch + Lomb’s ROIC has stayed the same over the last few years. If the company wants to become an investable business, it must improve its returns by generating more profitable growth.

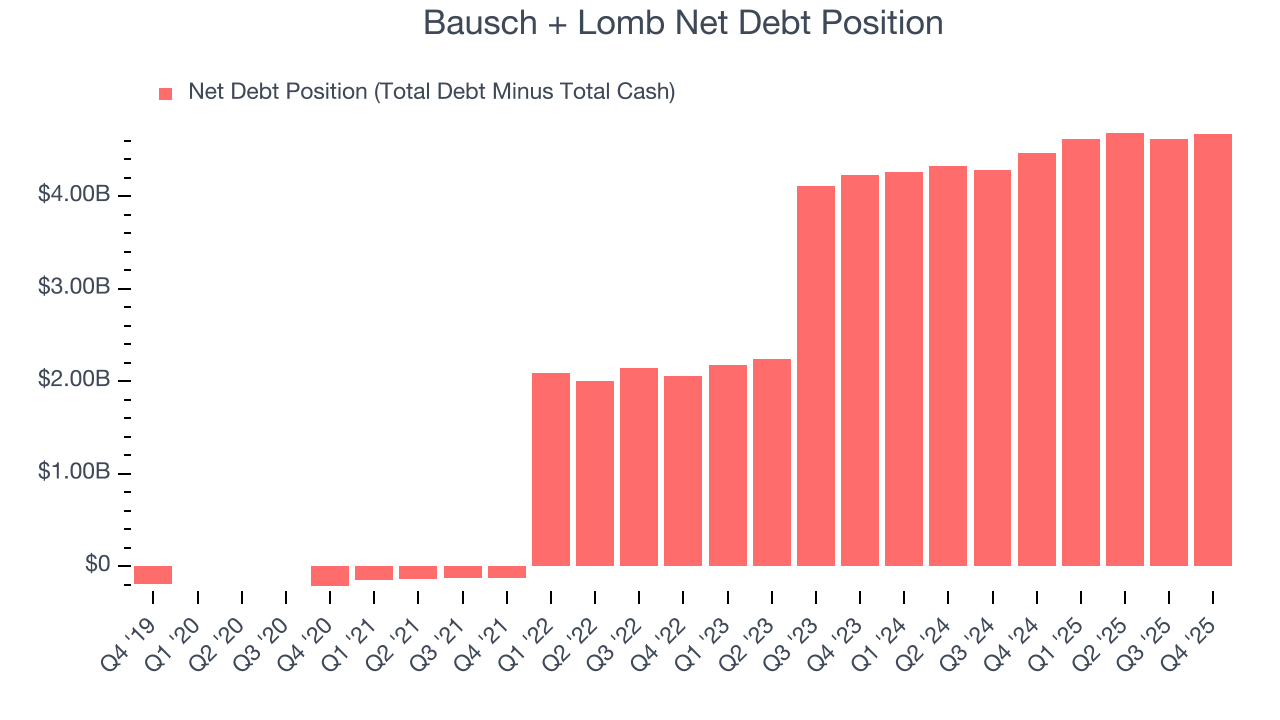

11. Balance Sheet Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

Bausch + Lomb’s $5.07 billion of debt exceeds the $397 million of cash on its balance sheet. Furthermore, its 5× net-debt-to-EBITDA ratio (based on its EBITDA of $891 million over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. Bausch + Lomb could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope Bausch + Lomb can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

12. Key Takeaways from Bausch + Lomb’s Q4 Results

It was good to see Bausch + Lomb narrowly top analysts’ revenue expectations this quarter. We were also glad its full-year revenue guidance slightly exceeded Wall Street’s estimates. On the other hand, its EPS missed. Overall, this was a weaker quarter. The stock remained flat at $18.44 immediately following the results.

13. Is Now The Time To Buy Bausch + Lomb?

Updated: March 29, 2026 at 11:49 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Bausch + Lomb.

Bausch + Lomb isn’t a terrible business, but it isn’t one of our picks. Although its revenue growth was decent over the last five years, it’s expected to deteriorate over the next 12 months and its declining EPS over the last three years makes it a less attractive asset to the public markets. And while the company’s constant currency growth has been splendid, the downside is its cash profitability fell over the last five years.

Bausch + Lomb’s P/E ratio based on the next 12 months is 20.5x. Investors with a higher risk tolerance might like the company, but we don’t really see a big opportunity at the moment. We're pretty confident there are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $18.46 on the company (compared to the current share price of $15.37).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.