BellRing Brands (BRBR)

BellRing Brands is a sound business. Its impressive sales growth and high returns on capital tee it up for fast and profitable expansion.― StockStory Analyst Team

1. News

2. Summary

Why BellRing Brands Is Interesting

Spun out of Post Holdings in 2019, Bellring Brands (NYSE:BRBR) offers protein shakes, nutrition bars, and other products under the PowerBar, Premier Protein, and Dymatize brands.

- Market-beating returns on capital illustrate that management has a knack for investing in profitable ventures, and its returns are growing as it capitalizes on even better market opportunities

- Products are flying off the shelves as its unit sales averaged 17.8% growth over the past two years

- On the flip side, its smaller revenue base of $2.32 billion means it hasn’t achieved the economies of scale that some industry juggernauts enjoy (but also enables it to grow faster if it executes properly)

BellRing Brands has the potential to be a high-quality business. If you like the story, the price looks fair.

Why Is Now The Time To Buy BellRing Brands?

BellRing Brands is trading at $16.74 per share, or 8.7x forward P/E. This valuation is quite compelling when considering the revenue growth you get.

If you think the market is undervaluing the company, now could be a good time to build a position.

3. BellRing Brands (BRBR) Research Report: Q4 CY2025 Update

Nutrition products company Bellring Brands (NYSE:BRBR) reported Q4 CY2025 results topping the market’s revenue expectations, but sales were flat year on year at $537.3 million. The company’s full-year revenue guidance of $2.44 billion at the midpoint came in 0.9% above analysts’ estimates. Its non-GAAP profit of $0.37 per share was 16.7% above analysts’ consensus estimates.

BellRing Brands (BRBR) Q4 CY2025 Highlights:

- Revenue: $537.3 million vs analyst estimates of $503.7 million (flat year on year, 6.7% beat)

- Adjusted EPS: $0.37 vs analyst estimates of $0.32 (16.7% beat)

- Adjusted EBITDA: $90.3 million vs analyst estimates of $80.97 million (16.8% margin, 11.5% beat)

- The company dropped its revenue guidance for the full year to $2.44 billion at the midpoint from $2.45 billion, a 0.6% decrease

- EBITDA guidance for the full year is $432.5 million at the midpoint, in line with analyst expectations

- Operating Margin: 14.6%, down from 21.6% in the same quarter last year

- Organic Revenue was flat year on year (beat)

- Sales Volumes were flat year on year (20.8% in the same quarter last year)

- Market Capitalization: $2.89 billion

Company Overview

Spun out of Post Holdings in 2019, Bellring Brands (NYSE:BRBR) offers protein shakes, nutrition bars, and other products under the PowerBar, Premier Protein, and Dymatize brands.

These products emphasize protein and low-carb or low-sugar content for weight loss and weight management. The Bellring Brands core customer is therefore a health-conscious individual who prioritizes nutritious eating or someone who wants to become that health-conscious person. Some customer archetypes include fitness enthusiasts or people on low-carb or keto diets looking to lose weight.

Bellring Brands’s products are available in general retailers such as grocery stores and club warehouse stores as well as in specialty retailers that cater to fitness and nutrition enthusiasts. Additionally, gyms and fitness centers sometimes carry the company’s products. Lastly, each of the company’s brands has a dedicated website where consumers can browse products, access exclusive deals, and access information on health and fitness.

4. Shelf-Stable Food

As America industrialized and moved away from an agricultural economy, people faced more demands on their time. Packaged foods emerged as a solution offering convenience to the evolving American family, whether it be canned goods or snacks. Today, Americans seek brands that are high in quality, reliable, and reasonably priced. Furthermore, there's a growing emphasis on health-conscious and sustainable food options. Packaged food stocks are considered resilient investments. People always need to eat, so these companies can enjoy consistent demand as long as they stay on top of changing consumer preferences. The industry spans from multinational corporations to smaller specialized firms and is subject to food safety and labeling regulations.

Competitors offering health and wellness supplements and products include The Simply Good Foods Company (NASDAQ:SMPL), Herbalife (NYSE:HLF), and Usana Health Sciences (NYSE:USNA) .

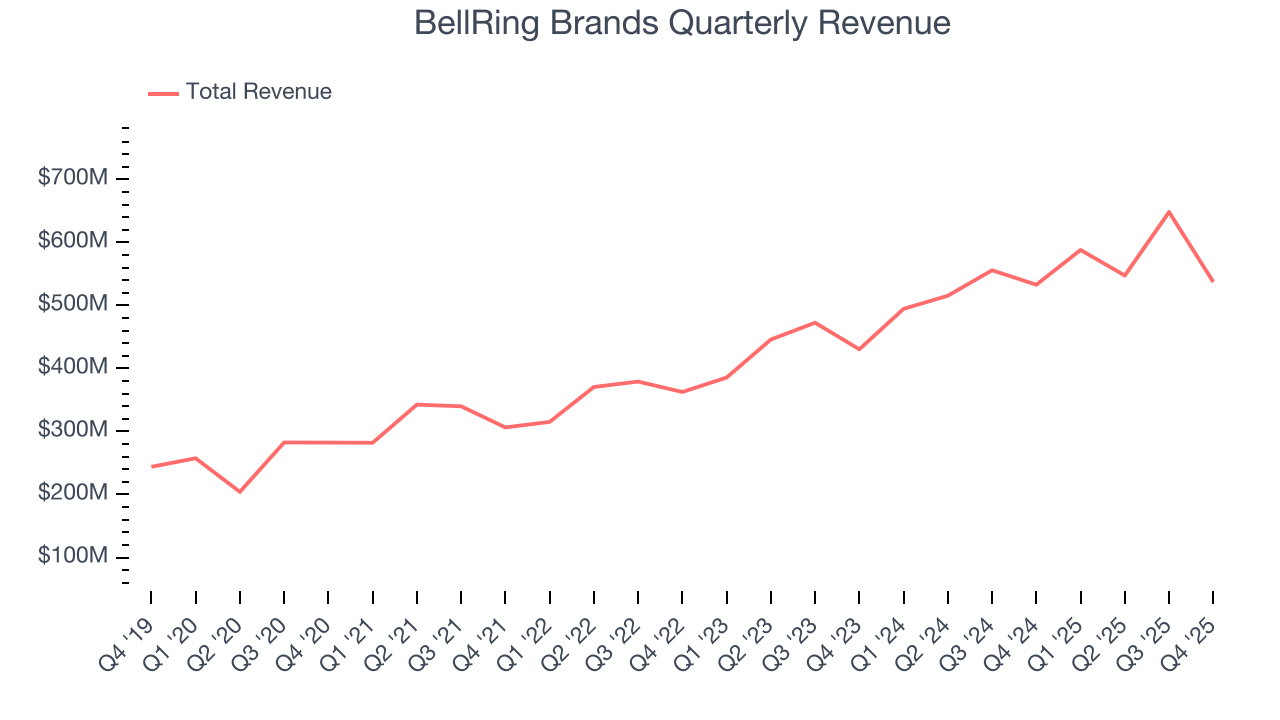

5. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $2.32 billion in revenue over the past 12 months, BellRing Brands is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers. On the bright side, it can grow faster because it has a longer list of untapped store chains to sell into.

As you can see below, BellRing Brands’s 17.6% annualized revenue growth over the last three years was impressive as consumers bought more of its products.

This quarter, BellRing Brands’s $537.3 million of revenue was flat year on year but beat Wall Street’s estimates by 6.7%.

Looking ahead, sell-side analysts expect revenue to grow 5.2% over the next 12 months, a deceleration versus the last three years. Still, this projection is above average for the sector and implies the market sees some success for its newer products.

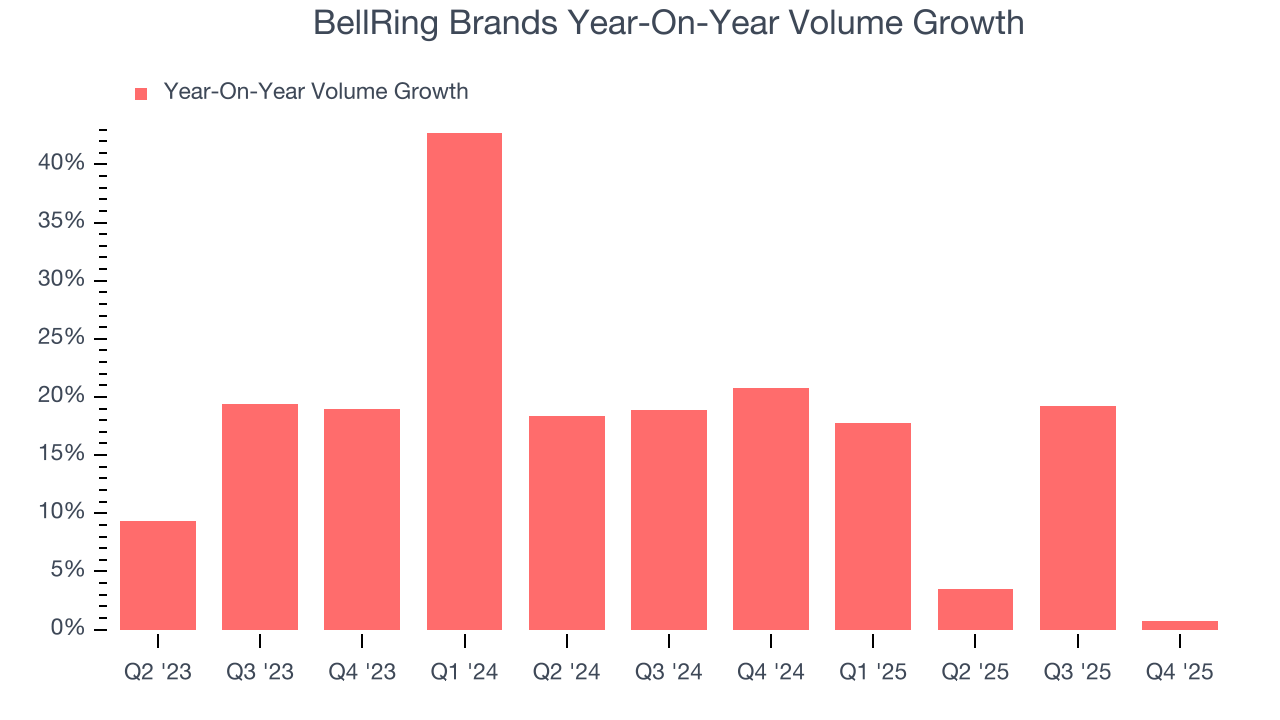

6. Volume Growth

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

To analyze whether BellRing Brands generated its growth from changes in price or volume, we can compare its volume growth to its organic revenue growth, which excludes non-fundamental impacts on company financials like mergers and currency fluctuations.

Over the last two years, BellRing Brands’s average quarterly volume growth of 17.8% has outpaced the competition by a long shot. In the context of its 16.3% average organic revenue growth, we can see that most of the company’s gains have come from more customers purchasing its products.

In BellRing Brands’s Q4 2026, year on year sales volumes were flat. This result was a meaningful deceleration from its historical levels. We’ll be watching closely to see if BellRing Brands can reaccelerate demand for its products.

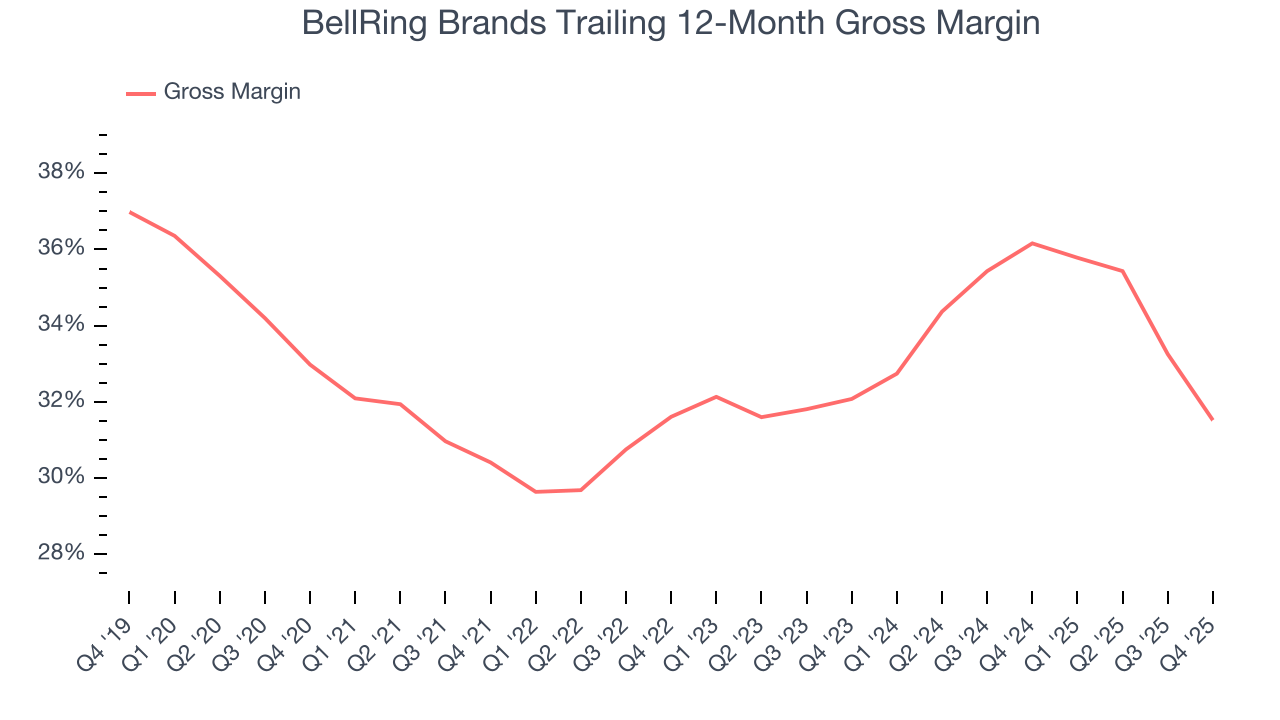

7. Gross Margin & Pricing Power

At StockStory, we prefer high gross margin businesses because they indicate pricing power or differentiated products, giving the company a chance to generate higher operating profits.

BellRing Brands’s unit economics are higher than the typical consumer staples company, giving it the flexibility to invest in areas such as marketing and talent to reach more consumers. As you can see below, it averaged a decent 33.7% gross margin over the last two years. Said differently, BellRing Brands paid its suppliers $66.28 for every $100 in revenue.

This quarter, BellRing Brands’s gross profit margin was 29.9%, marking a 7.5 percentage point decrease from 37.5% in the same quarter last year. BellRing Brands’s full-year margin has also been trending down over the past 12 months, decreasing by 4.6 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to lower prices and higher input costs (such as raw materials and manufacturing expenses).

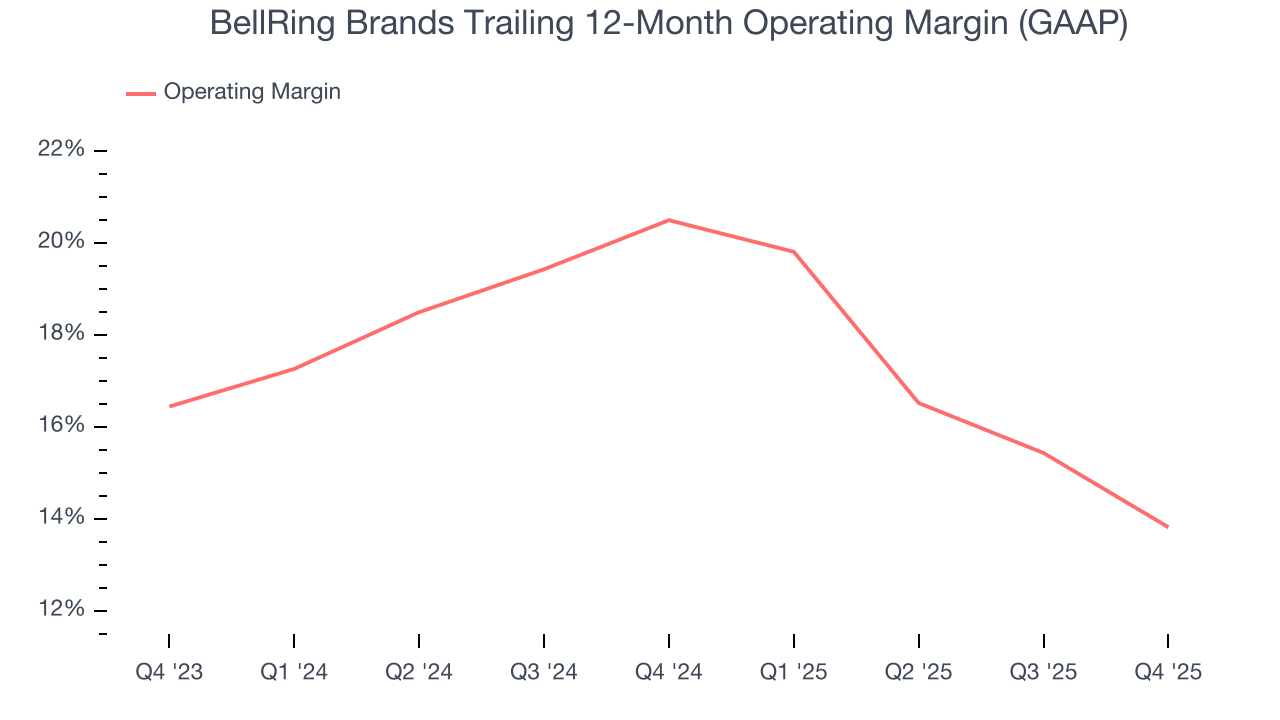

8. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

BellRing Brands has been an efficient company over the last two years. It was one of the more profitable businesses in the consumer staples sector, boasting an average operating margin of 17%.

Looking at the trend in its profitability, BellRing Brands’s operating margin decreased by 6.7 percentage points over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q4, BellRing Brands generated an operating margin profit margin of 14.6%, down 7 percentage points year on year. Since BellRing Brands’s gross margin decreased more than its operating margin, we can assume its recent inefficiencies were driven more by weaker leverage on its cost of sales rather than increased marketing, and administrative overhead expenses.

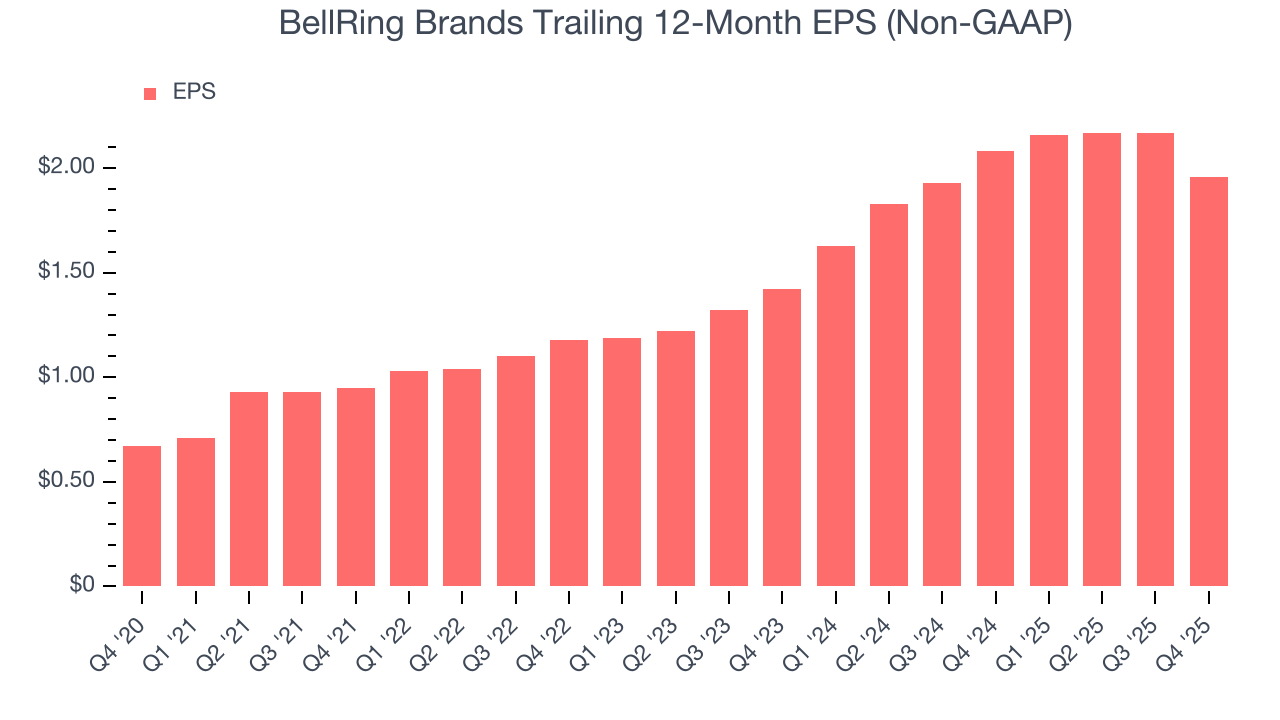

9. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

BellRing Brands’s remarkable 18.4% annual EPS growth over the last three years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

In Q4, BellRing Brands reported adjusted EPS of $0.37, down from $0.58 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects BellRing Brands’s full-year EPS of $1.96 to grow 1.4%.

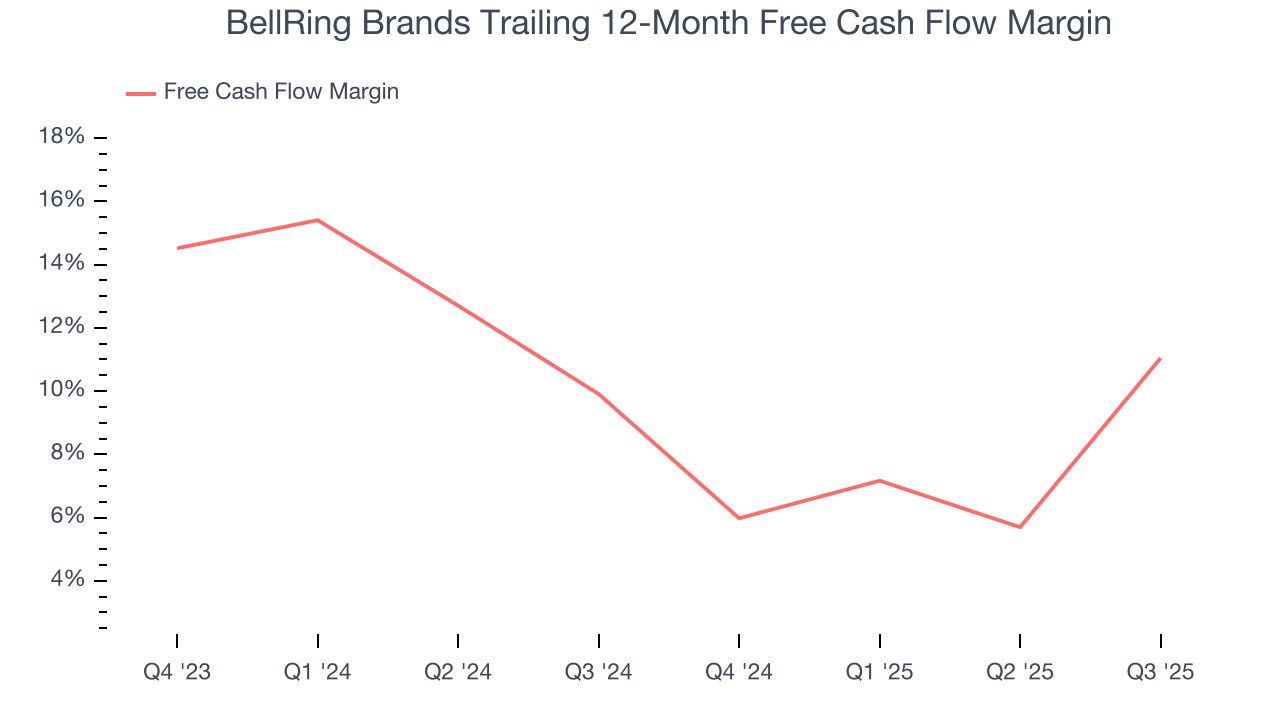

10. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

BellRing Brands has shown robust cash profitability, giving it an edge over its competitors and the ability to reinvest or return capital to investors. The company’s free cash flow margin averaged 9.8% over the last two years, quite impressive for a consumer staples business.

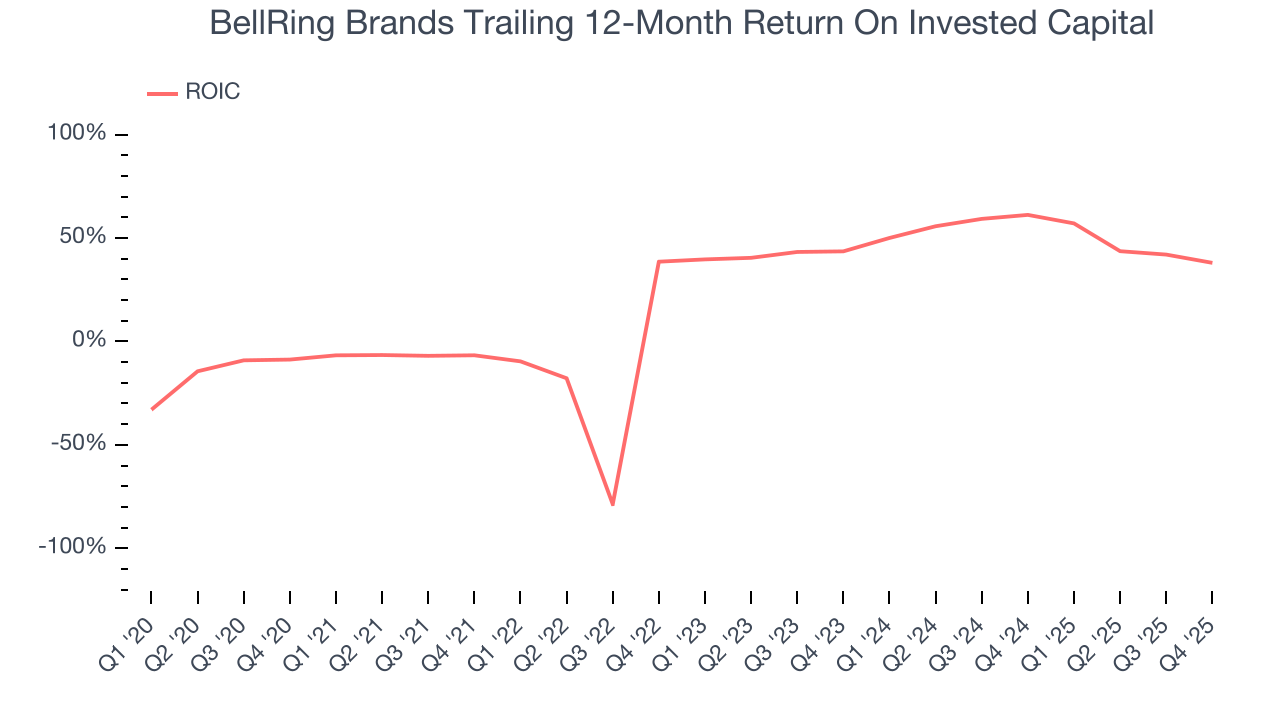

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Although BellRing Brands hasn’t been the highest-quality company lately, it found a few growth initiatives in the past that worked out wonderfully. Its four-year average ROIC was 45.3%, splendid for a consumer staples business.

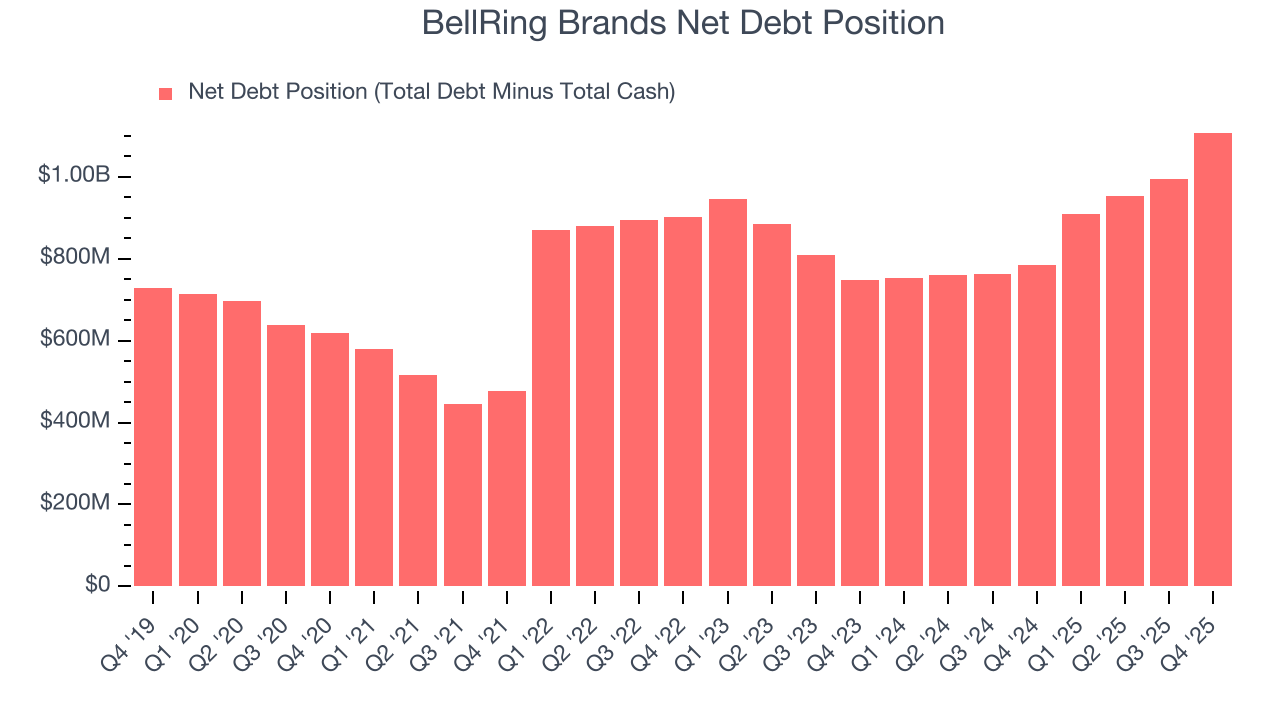

12. Balance Sheet Assessment

BellRing Brands reported $77 million of cash and $1.18 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $446.6 million of EBITDA over the last 12 months, we view BellRing Brands’s 2.5× net-debt-to-EBITDA ratio as safe. We also see its $34 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

13. Key Takeaways from BellRing Brands’s Q4 Results

We were impressed by how significantly BellRing Brands blew past analysts’ EBITDA expectations this quarter. We were also excited its organic revenue outperformed Wall Street’s estimates by a wide margin. On the other hand, its gross margin missed and full year revenue guidance was slightly reduced. Zooming out, we think this quarter was mixed. The stock remained flat at $24.39 immediately following the results.

14. Is Now The Time To Buy BellRing Brands?

Updated: March 23, 2026 at 10:42 PM EDT

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

In our opinion, BellRing Brands is a solid company. First off, its revenue growth was good over the last three years. And while its declining operating margin shows the business has become less efficient, its volume growth has been in a league of its own. On top of that, its stellar ROIC suggests it has been a well-run company historically.

BellRing Brands’s P/E ratio based on the next 12 months is 8.7x. Looking at the consumer staples space right now, BellRing Brands trades at a compelling valuation. If you believe in the company and its growth potential, now is an opportune time to buy shares.

Wall Street analysts have a consensus one-year price target of $30.07 on the company (compared to the current share price of $16.74), implying they see 79.7% upside in buying BellRing Brands in the short term.