Core & Main (CNM)

We love companies like Core & Main. Its superior revenue growth and returns on capital show it can achieve fast and profitable expansion.― StockStory Analyst Team

1. News

2. Summary

Why We Like Core & Main

Formerly a division of industrial distributor HD Supply, Core & Main (NYSE:CNM) is a provider of water, wastewater, and fire protection products and services.

- Impressive 17% annual revenue growth over the last five years indicates it’s winning market share this cycle

- Additional sales over the last two years increased its profitability as the 19.1% annual growth in its earnings per share outpaced its revenue

- Industry-leading 15.1% return on capital demonstrates management’s skill in finding high-return investments

We see a bright future for Core & Main. The valuation looks reasonable when considering its quality, so this could be a good time to buy some shares.

Why Is Now The Time To Buy Core & Main?

At $48.71 per share, Core & Main trades at 18.9x forward P/E. This multiple is lower than most industrials companies, and we think the stock is a deal when considering its quality characteristics.

Entry price matters far less than business fundamentals if you’re investing for a multi-year period. But if you can get a bargain price it’s certainly icing on the cake.

3. Core & Main (CNM) Research Report: Q4 CY2025 Update

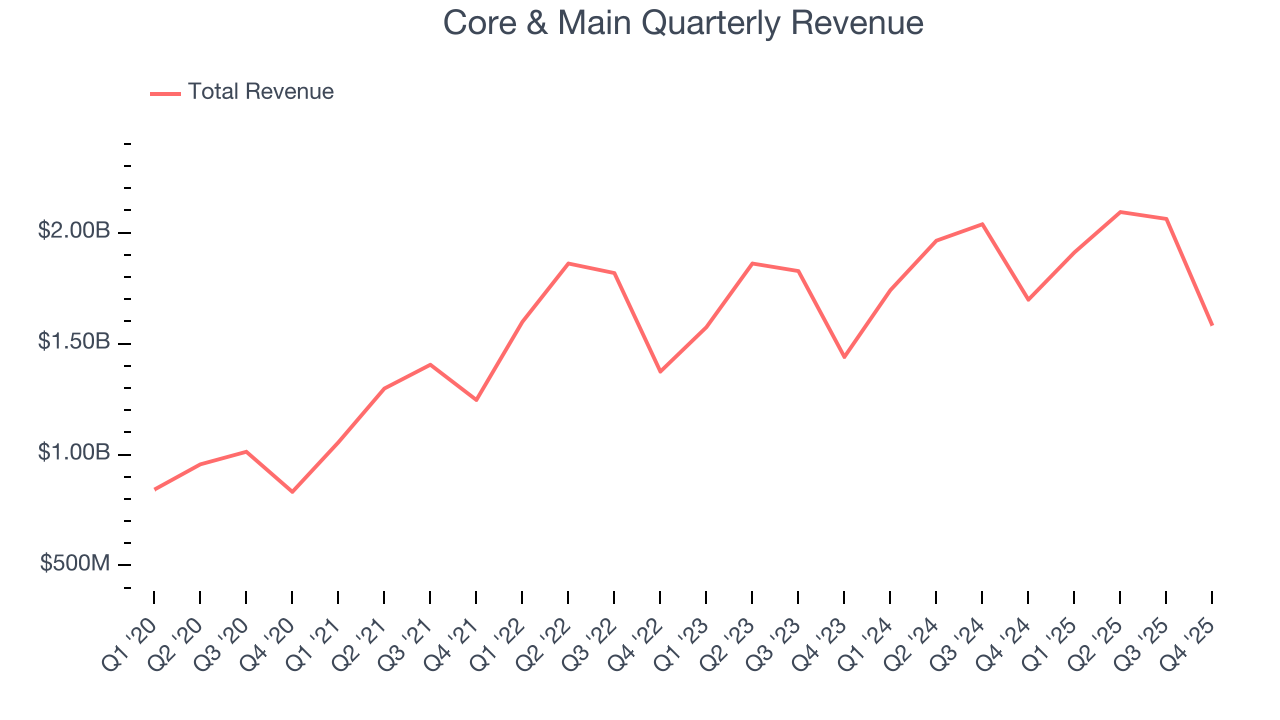

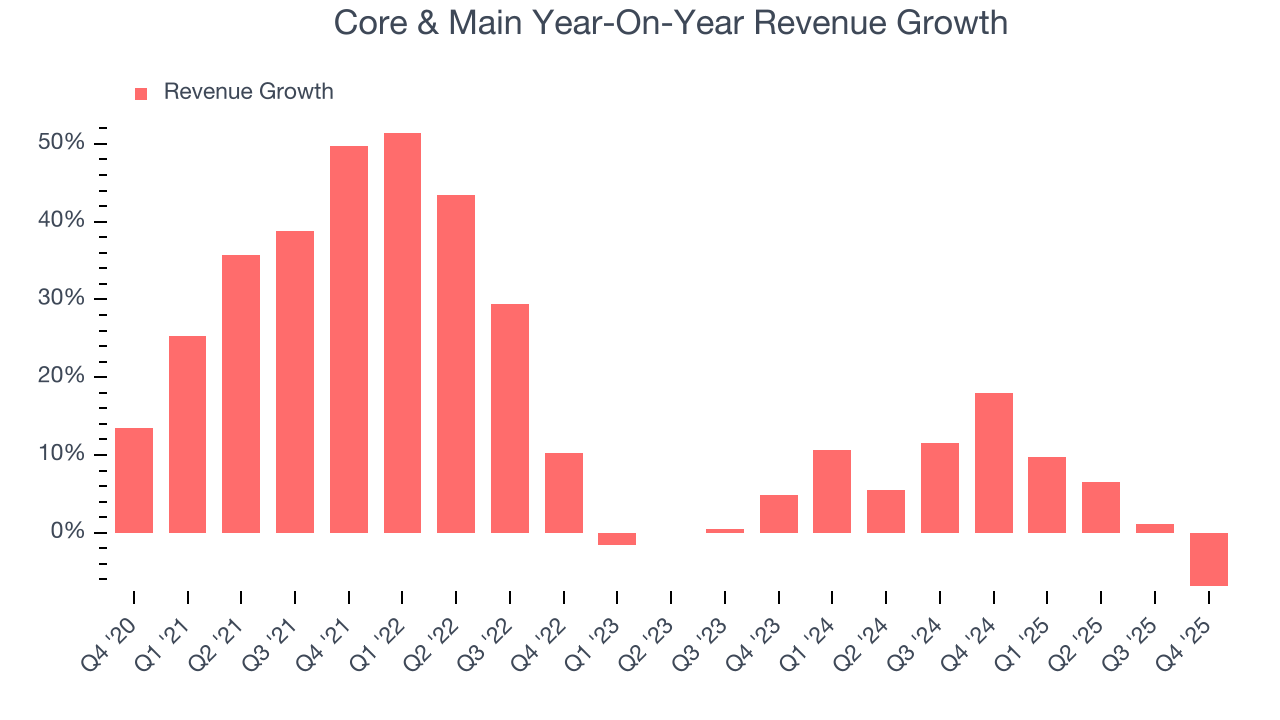

Water and fire protection solutions company Core & Main (NYSE:CNM) missed Wall Street’s revenue expectations in Q4 CY2025, with sales falling 6.9% year on year to $1.58 billion. The company’s full-year revenue guidance of $7.85 billion at the midpoint came in 1% below analysts’ estimates. Its non-GAAP profit of $0.52 per share was 57.8% above analysts’ consensus estimates.

Core & Main (CNM) Q4 CY2025 Highlights:

- Revenue: $1.58 billion vs analyst estimates of $1.59 billion (6.9% year-on-year decline, 0.7% miss)

- Adjusted EPS: $0.52 vs analyst estimates of $0.33 (57.8% beat)

- Adjusted EBITDA: $167 million vs analyst estimates of $165.2 million (10.6% margin, 1.1% beat)

- EBITDA guidance for the upcoming financial year 2026 is $965 million at the midpoint, below analyst estimates of $987.4 million

- Operating Margin: 7.5%, in line with the same quarter last year

- Free Cash Flow Margin: 16%, up from 13.2% in the same quarter last year

- Market Capitalization: $9.14 billion

Company Overview

Formerly a division of industrial distributor HD Supply, Core & Main (NYSE:CNM) is a provider of water, wastewater, and fire protection products and services.

Core & Main offers a range of solutions designed to support the construction and maintenance of critical infrastructure. Specifically, the company supplies municipalities with essential waterworks products, assists industrial clients with wastewater management solutions, and supports residential developers with fire protection equipment. These products range from the simple such as pipes and pipe sealants to the complex such as advanced meters that reads flow data with high precision.

The primary revenue sources for Core & Main come from the sale of its products and the provision of services such as maintenance and installation. Recurring revenue is generated through long-term contracts and ongoing maintenance services. The company's go-to-market strategy encompasses a direct sales force and robust distribution network to build enduring customer relationships.

4. Infrastructure Distributors

Focusing on narrow product categories that can lead to economies of scale, infrastructure distributors sell essential goods that often enjoy more predictable revenue streams. For example, the ongoing inspection, maintenance, and replacement of pipes and water pumps are critical to a functioning society, rendering them non-discretionary. Lately, innovation to address trends like water conservation has driven incremental sales. But like the broader industrials sector, infrastructure distributors are also at the whim of economic cycles as external factors like interest rates can greatly impact commercial and residential construction projects that drive demand for infrastructure products.

Competitors in the water and fire protection industry include Ferguson (NYSE:FERG), Mueller Water Products (NYSE:MWA), and Essential Utilities (NYSE:WTRG).

5. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Thankfully, Core & Main’s 16% annualized revenue growth over the last five years was incredible. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Core & Main’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 6.8% over the last two years was well below its five-year trend.

This quarter, Core & Main missed Wall Street’s estimates and reported a rather uninspiring 6.9% year-on-year revenue decline, generating $1.58 billion of revenue.

Looking ahead, sell-side analysts expect revenue to grow 4% over the next 12 months, a slight deceleration versus the last two years. This projection is underwhelming and indicates its products and services will see some demand headwinds. At least the company is tracking well in other measures of financial health.

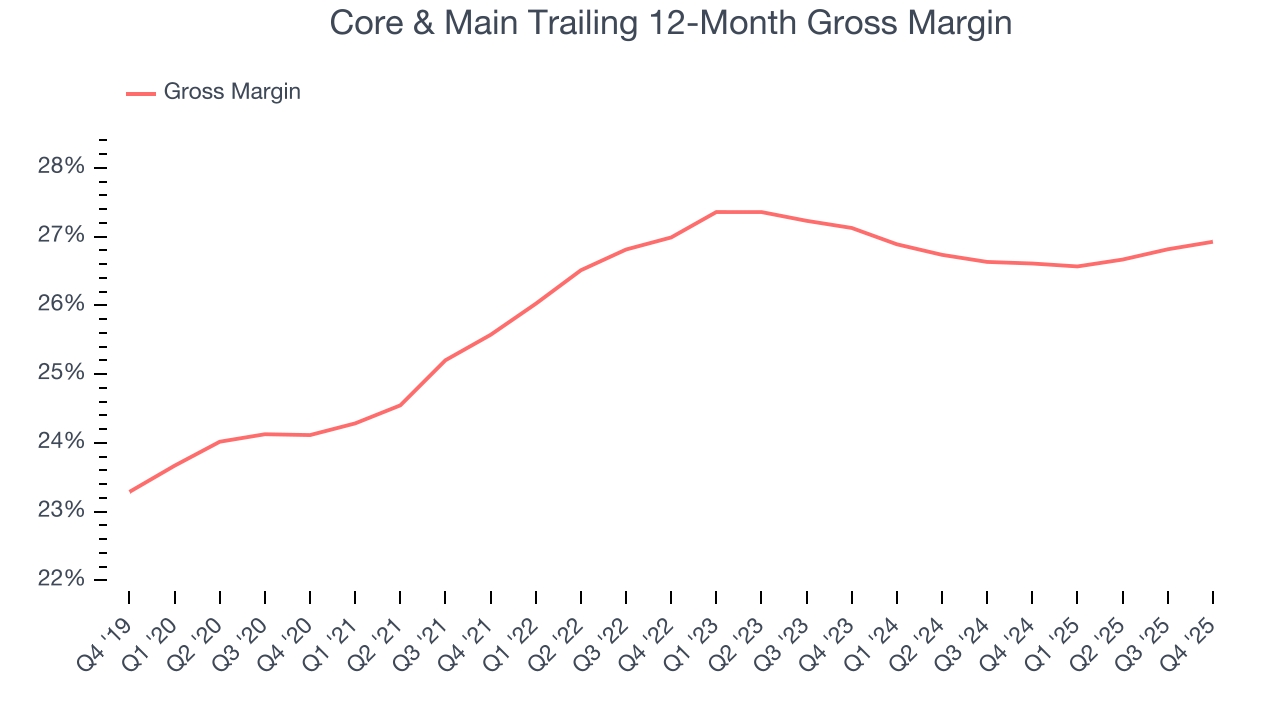

6. Gross Margin & Pricing Power

Core & Main has bad unit economics for an industrials company, giving it less room to reinvest and develop new offerings. As you can see below, it averaged a 26.7% gross margin over the last five years. That means Core & Main paid its suppliers a lot of money ($73.29 for every $100 in revenue) to run its business.

In Q4, Core & Main produced a 27.1% gross profit margin, in line with the same quarter last year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

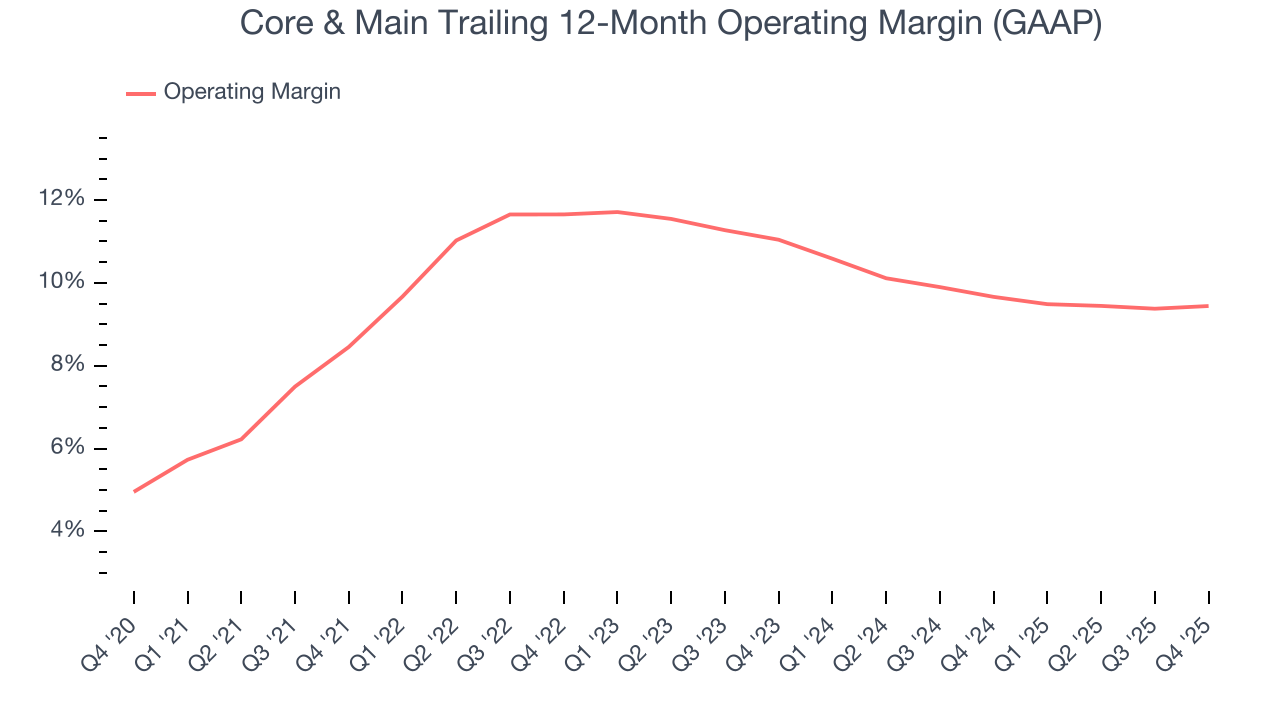

7. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Core & Main’s operating margin has generally stayed the same over the last 12 months, averaging 10.1% over the last five years. This profitability was solid for an industrials business and shows it’s an efficient company that manages its expenses well. This was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Looking at the trend in its profitability, Core & Main’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. We like to see margin expansion, but Core & Main’s performance still shows it’s one of the better Infrastructure Distributors companies as most peers saw their margins plummet.

This quarter, Core & Main generated an operating margin profit margin of 7.5%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

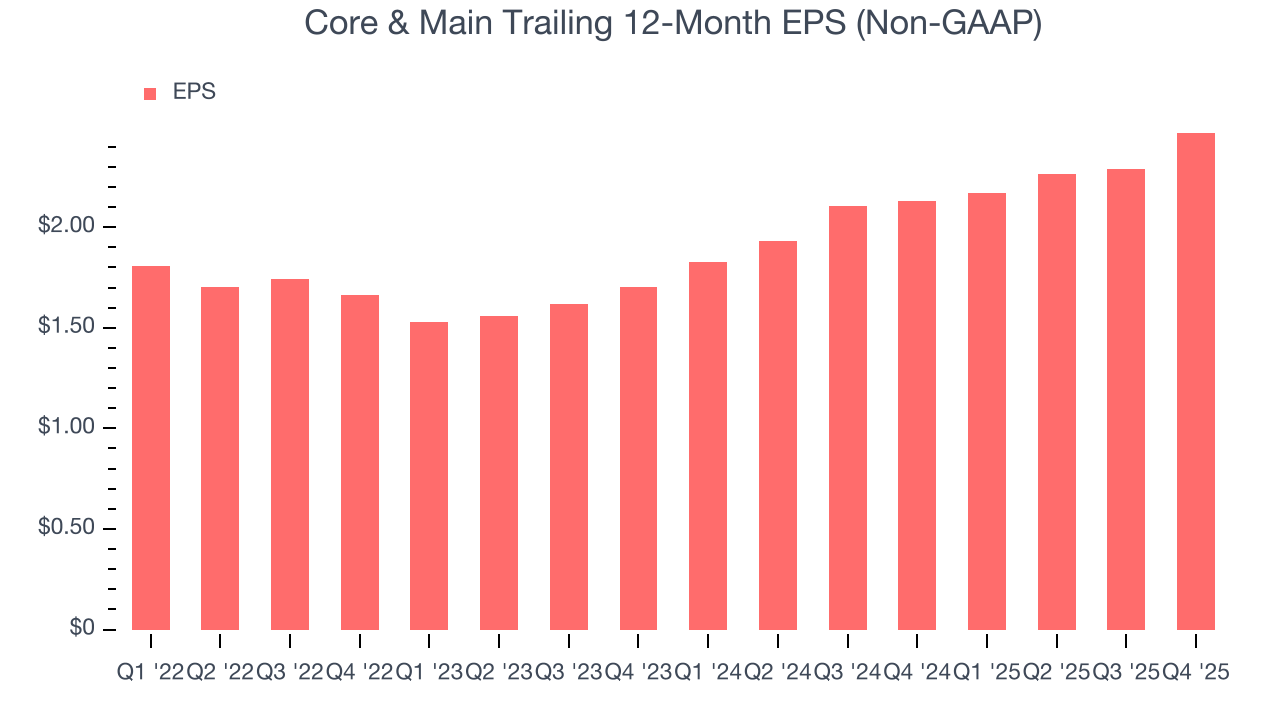

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Core & Main’s full-year EPS grew at a solid 10.4% compounded annual growth rate over the last four years, better than the broader industrials sector.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

Core & Main’s EPS grew at an astounding 20.4% compounded annual growth rate over the last two years, higher than its 6.8% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

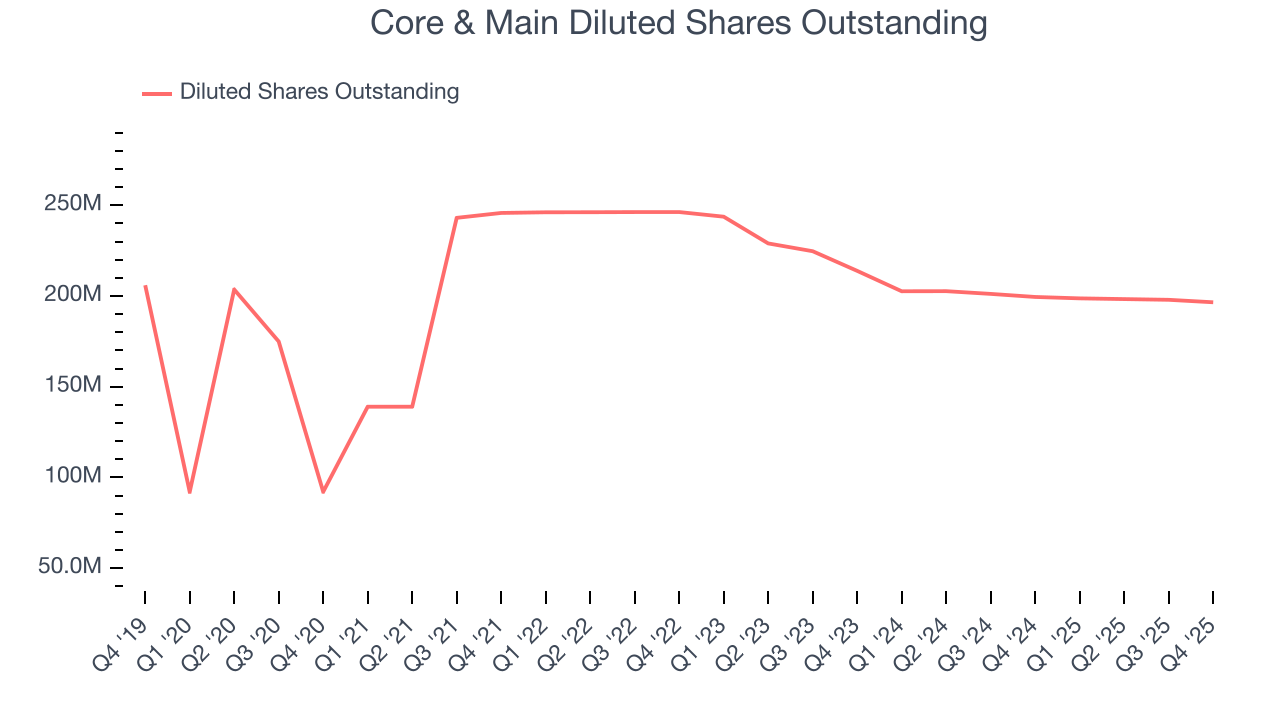

We can take a deeper look into Core & Main’s earnings to better understand the drivers of its performance. A two-year view shows that Core & Main has repurchased its stock, shrinking its share count by 8.1%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q4, Core & Main reported adjusted EPS of $0.52, up from $0.34 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Core & Main’s full-year EPS of $2.47 to grow 4.3%.

9. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

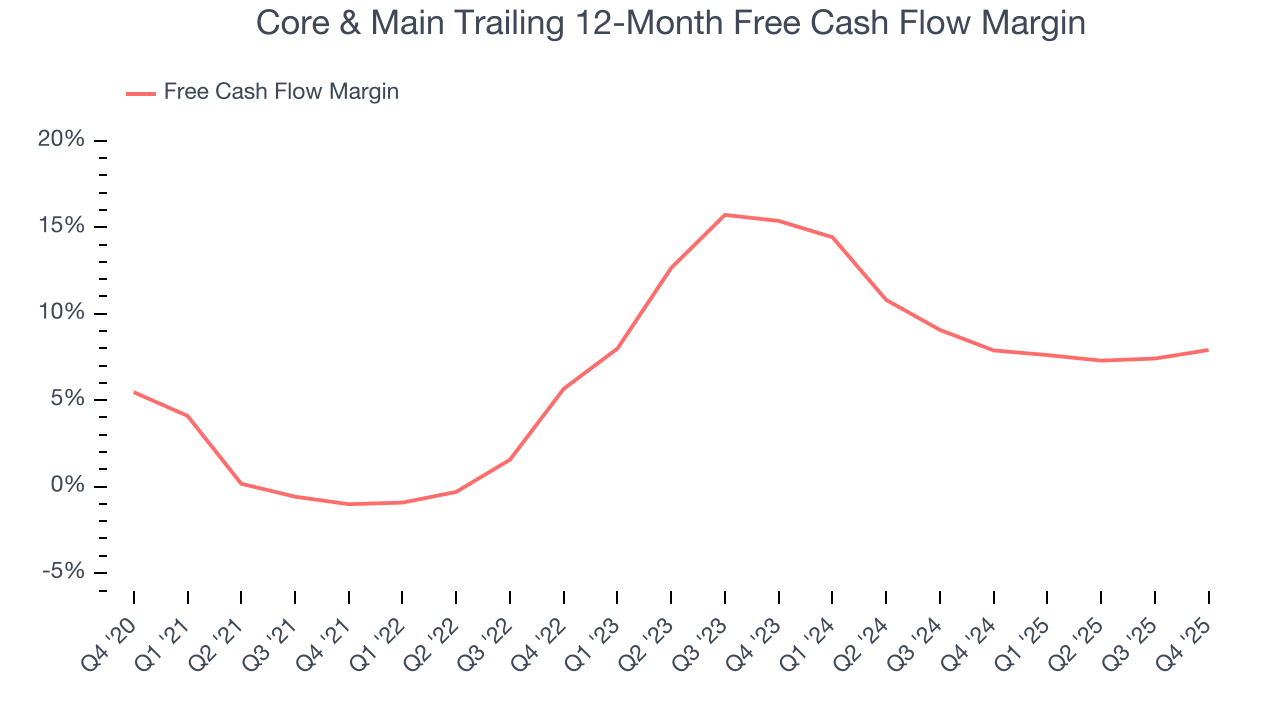

Core & Main has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 7.6% over the last five years, slightly better than the broader industrials sector.

Taking a step back, we can see that Core & Main’s margin expanded by 8.9 percentage points during that time. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability was flat.

Core & Main’s free cash flow clocked in at $253 million in Q4, equivalent to a 16% margin. This result was good as its margin was 2.8 percentage points higher than in the same quarter last year, building on its favorable historical trend.

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

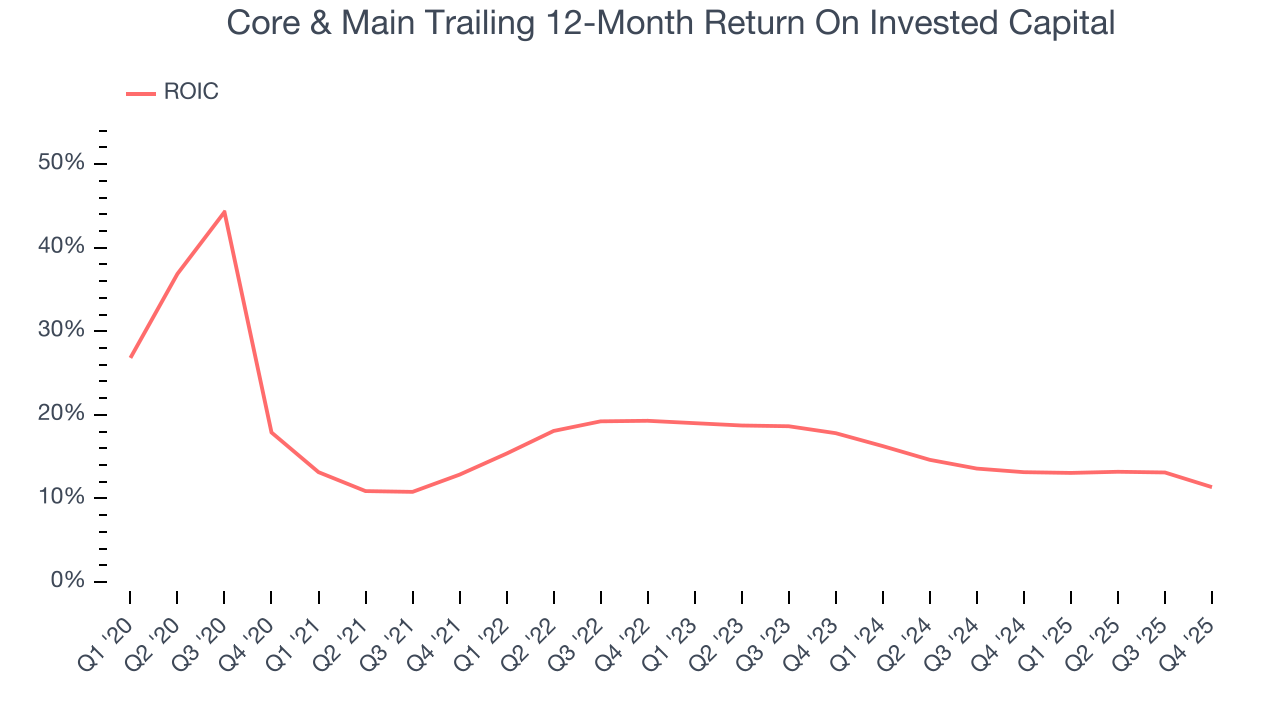

Core & Main’s five-year average ROIC was 14.9%, beating other industrials companies by a wide margin. This illustrates its management team’s ability to invest in attractive growth opportunities and produce tangible results for shareholders.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. On average, Core & Main’s ROIC decreased by 3.8 percentage points annually each year over the last few years. Only time will tell if its new bets can bear fruit and potentially reverse the trend.

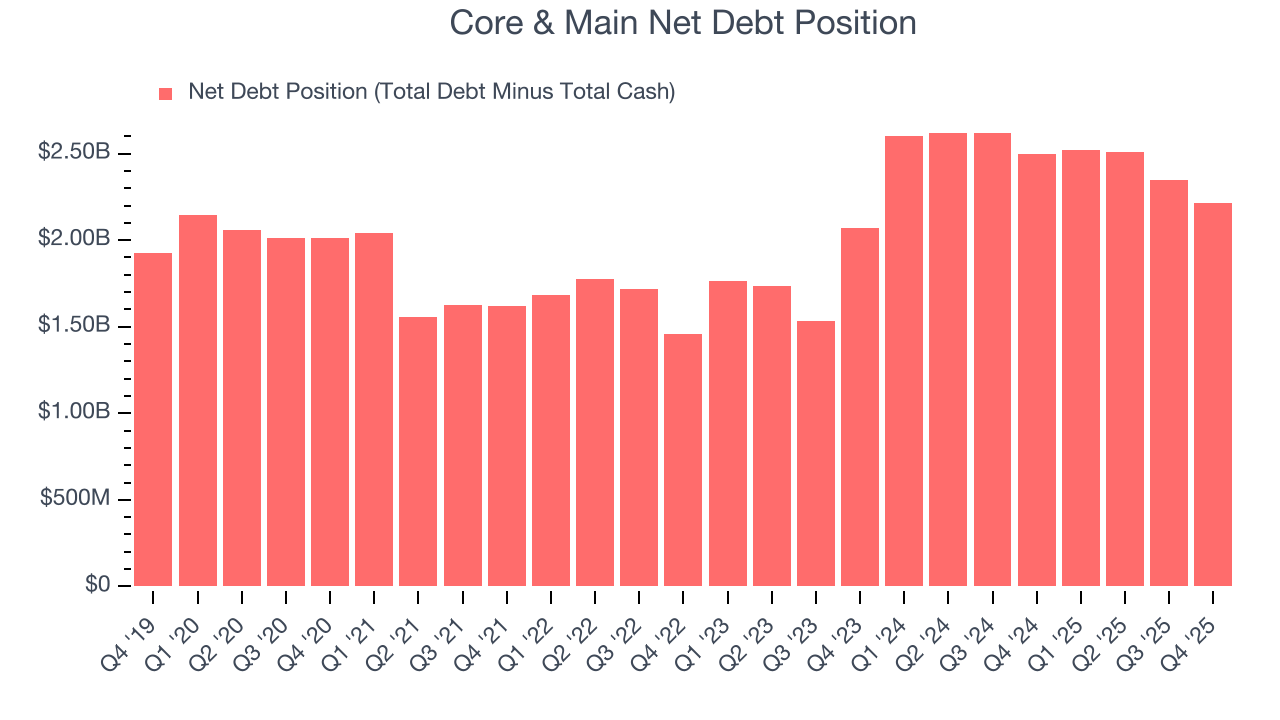

11. Balance Sheet Assessment

Core & Main reported $220 million of cash and $2.44 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $931 million of EBITDA over the last 12 months, we view Core & Main’s 2.4× net-debt-to-EBITDA ratio as safe. We also see its $62 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Core & Main’s Q4 Results

It was good to see Core & Main beat analysts’ EPS expectations this quarter. We were also happy its EBITDA narrowly outperformed Wall Street’s estimates. On the other hand, its full-year EBITDA guidance missed and its revenue fell slightly short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 6.3% to $45.37 immediately after reporting.

13. Is Now The Time To Buy Core & Main?

Updated: March 24, 2026 at 7:40 AM EDT

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own Core & Main, you should also grasp the company’s longer-term business quality and valuation.

Core & Main is a fine business. To kick things off, its revenue growth was exceptional over the last five years. And while its diminishing returns show management's recent bets still have yet to bear fruit, its rising cash profitability gives it more optionality. On top of that, its solid ROIC suggests it has grown profitably in the past.

Core & Main’s P/E ratio based on the next 12 months is 18.8x. Looking across the spectrum of industrials companies today, Core & Main’s fundamentals shine bright. We like the stock at this price.

Wall Street analysts have a consensus one-year price target of $60.94 on the company (compared to the current share price of $45.37), implying they see 34.3% upside in buying Core & Main in the short term.