Corebridge Financial (CRBG)

Corebridge Financial keeps us up at night. Its revenue growth has been weak and its profitability has caved, showing it’s struggling to adapt.― StockStory Analyst Team

1. News

2. Summary

Why We Think Corebridge Financial Will Underperform

Spun off from insurance giant AIG in 2022 to focus on the growing retirement market, Corebridge Financial (NYSE:CRBG) provides retirement solutions, annuities, life insurance, and institutional risk management products in the United States.

- Products and services are facing significant end-market challenges during this cycle as sales have declined by 1.8% annually over the last two years

- Insurance policy sales contracted this cycle as net premiums earned decreased by 2.2% annually over the last four years

- Net premiums earned contracted by 12.9% annually over the last two years, showing unfavorable market dynamics this cycle

Corebridge Financial falls short of our quality standards. There are more rewarding stocks elsewhere.

Why There Are Better Opportunities Than Corebridge Financial

Corebridge Financial’s stock price of $31.44 implies a valuation ratio of 1.1x forward P/B. This multiple is lower than most insurance companies, but for good reason.

It’s better to pay up for high-quality businesses with higher long-term earnings potential rather than to buy lower-quality stocks because they appear cheap. These challenged businesses often don’t re-rate, a phenomenon known as a “value trap”.

3. Corebridge Financial (CRBG) Research Report: Q4 CY2025 Update

Retirement solutions provider Corebridge Financial (NYSE:CRBG) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 35.7% year on year to $6.34 billion. Its non-GAAP profit of $1.22 per share was 9.7% above analysts’ consensus estimates.

Corebridge Financial (CRBG) Q4 CY2025 Highlights:

- Net Premiums Earned: $2.60 billion (38.7% year-on-year growth)

- Revenue: $6.34 billion vs analyst estimates of $4.31 billion (35.7% year-on-year growth, 47.3% beat)

- Pre-tax Profit: $760 million (12% margin)

- Adjusted EPS: $1.22 vs analyst estimates of $1.11 (9.7% beat)

- Book Value per Share: $25.60 (25.4% year-on-year growth)

- Market Capitalization: $16.22 billion

Company Overview

Spun off from insurance giant AIG in 2022 to focus on the growing retirement market, Corebridge Financial (NYSE:CRBG) provides retirement solutions, annuities, life insurance, and institutional risk management products in the United States.

Corebridge operates through four main business segments that serve different markets and customer needs. The Individual Retirement segment offers various annuity products including fixed, fixed index, registered index linked, and variable annuities that provide guaranteed income, death benefits, and investment growth potential. These products are distributed through a network of approximately 490 third-party firms including banks, broker-dealers, and independent agents.

The Group Retirement segment serves employees of tax-exempt and public sector organizations such as K-12 schools, higher education institutions, healthcare providers, and government employers. It provides both in-plan products like recordkeeping platforms and group annuities, as well as out-of-plan solutions including IRAs and advisory services. The company's employee financial advisors work directly with individuals to provide retirement planning guidance and comprehensive financial planning.

The Life Insurance segment focuses on term life, index universal life, and whole life insurance products. Corebridge has strategically shifted away from interest rate sensitive products like guaranteed universal life insurance toward products with better margins. It distributes these products through independent channels and its direct-to-consumer platform, targeting demographics from middle market to high net worth individuals.

The Institutional Markets segment offers sophisticated risk management solutions to large institutional clients, including pension risk transfer services, guaranteed investment contracts, structured settlement annuities, and stable value wrap contracts. These specialized products help corporations manage pension obligations, provide long-term payment streams for legal settlements, and offer stable returns for retirement funds.

Corebridge benefits from its strategic partnership with Blackstone, which helps the company source attractive fixed-income assets. The company's investment management capabilities are integral to its business model, as it manages general and separate account assets across various markets to produce consistent returns while minimizing earnings volatility.

4. Life Insurance

Life insurance companies collect premiums from policyholders in exchange for providing a future death benefit or retirement income stream. Interest rates matter for the sector (and make it cyclical), with higher rates allowing insurers to reinvest their fixed-income portfolios at more attractive yields and vice versa. Additionally, favorable demographic shifts, such as an aging population, are driving strong demand for retirement products while AI and data analytics offer significant opportunities to improve underwriting accuracy and operational efficiency. Conversely, the industry faces headwinds from persistent competition from agile insurtechs that threaten traditional distribution models.

Corebridge Financial competes with major retirement and insurance providers including Prudential Financial (NYSE:PRU), Lincoln National (NYSE:LNC), Equitable Holdings (NYSE:EQH), and Brighthouse Financial (NASDAQ:BHF). In the institutional markets segment, it also faces competition from MetLife (NYSE:MET) and Principal Financial Group (NASDAQ:PFG).

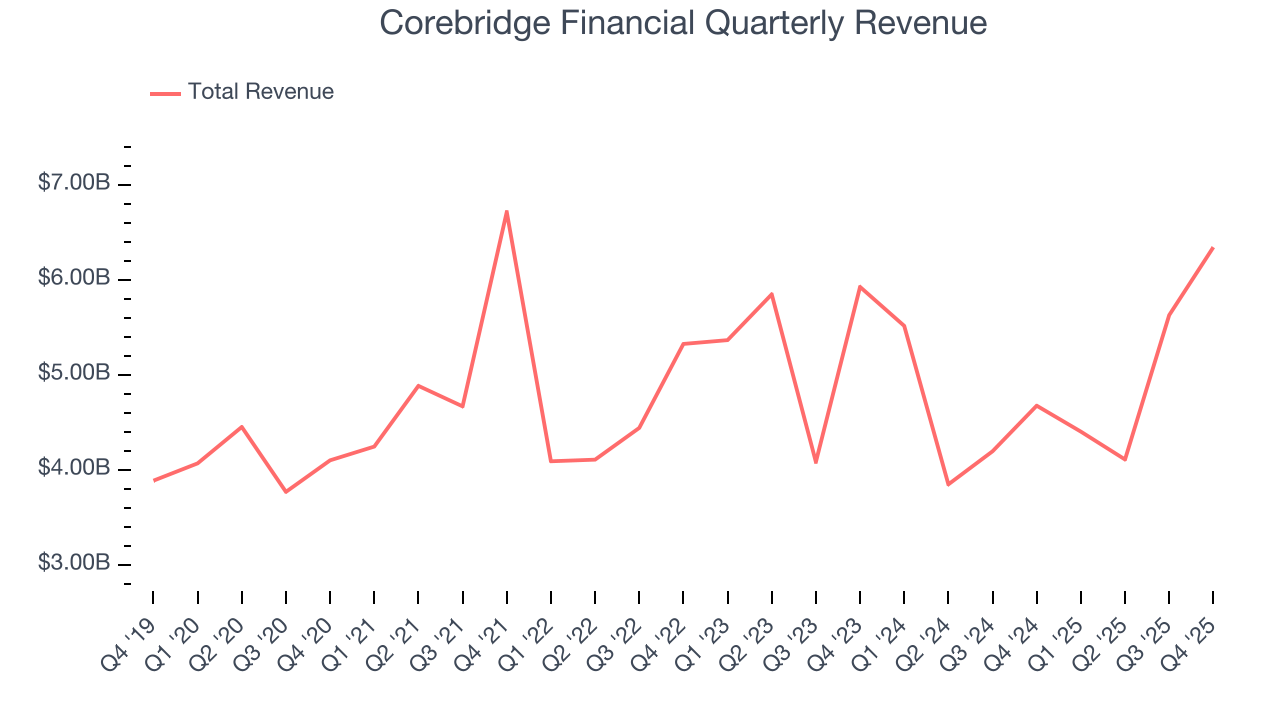

5. Revenue Growth

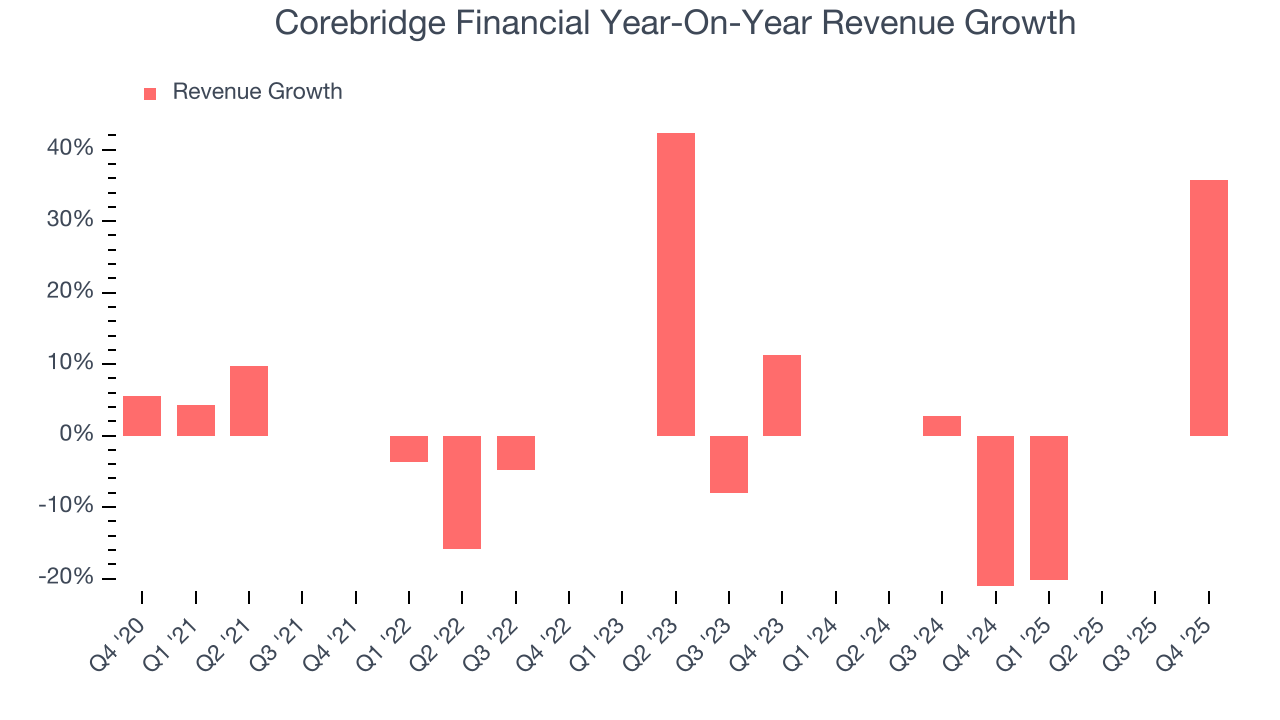

Insurance companies generate revenue three ways. The first is the core insurance business itself, represented in the income statement as premiums earned. The second source is investment income from investing the “float” (premiums collected but not yet paid out as claims) in assets such as fixed-income assets and equities. The third is fees from policy administration, annuities, and other value-added services. Unfortunately, Corebridge Financial’s 4.6% annualized revenue growth over the last five years was tepid. This fell short of our benchmark for the insurance sector and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Corebridge Financial’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 1.8% annually.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Corebridge Financial reported wonderful year-on-year revenue growth of 35.7%, and its $6.34 billion of revenue exceeded Wall Street’s estimates by 47.3%.

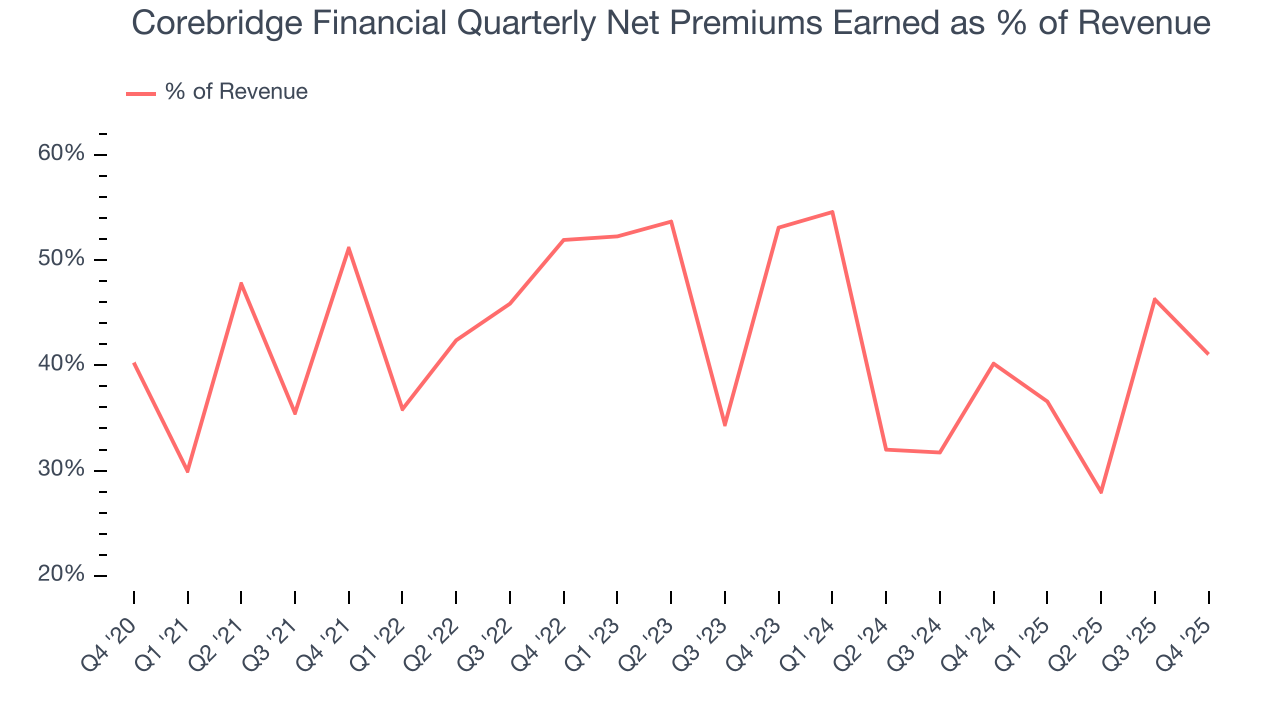

Net premiums earned made up 43.3% of the company’s total revenue during the last five years, meaning Corebridge Financial’s growth drivers strike a balance between insurance and non-insurance activities.

Markets consistently prioritize net premiums earned growth over investment and fee income, recognizing its superior quality as a core indicator of the company’s underwriting success and market penetration.

6. Net Premiums Earned

Net premiums earned are net of what’s paid to reinsurers (insurance for insurance companies), which are used by insurers to protect themselves from large losses.

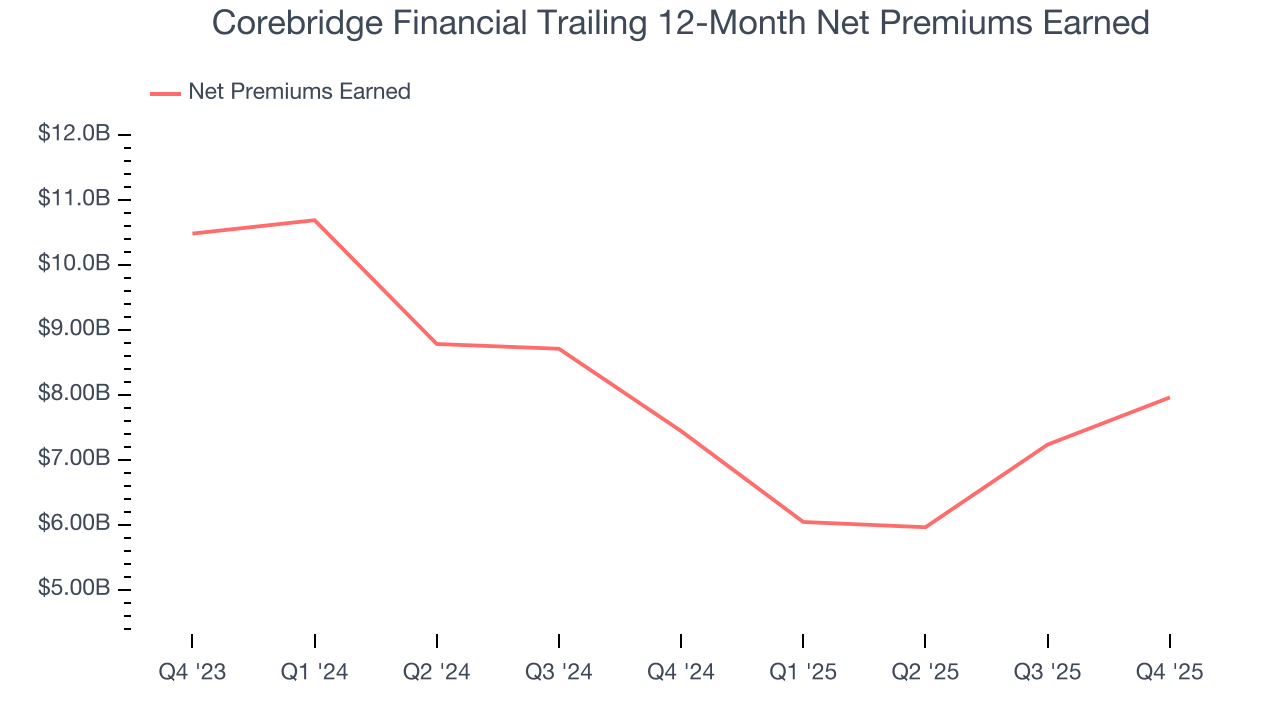

Corebridge Financial’s net premiums earned has declined by 2.2% annually over the last four years, much worse than the broader insurance industry.

When analyzing Corebridge Financial’s net premiums earned over the last two years, we can see its woes have continued as income dropped by 12.9% annually. Since two-year net premiums earned underperformed total revenue over this period, it’s implied that insurance policies were a detractor of consolidated growth.

Corebridge Financial’s net premiums earned came in at $2.60 billion this quarter, up a hearty 38.7% year on year.

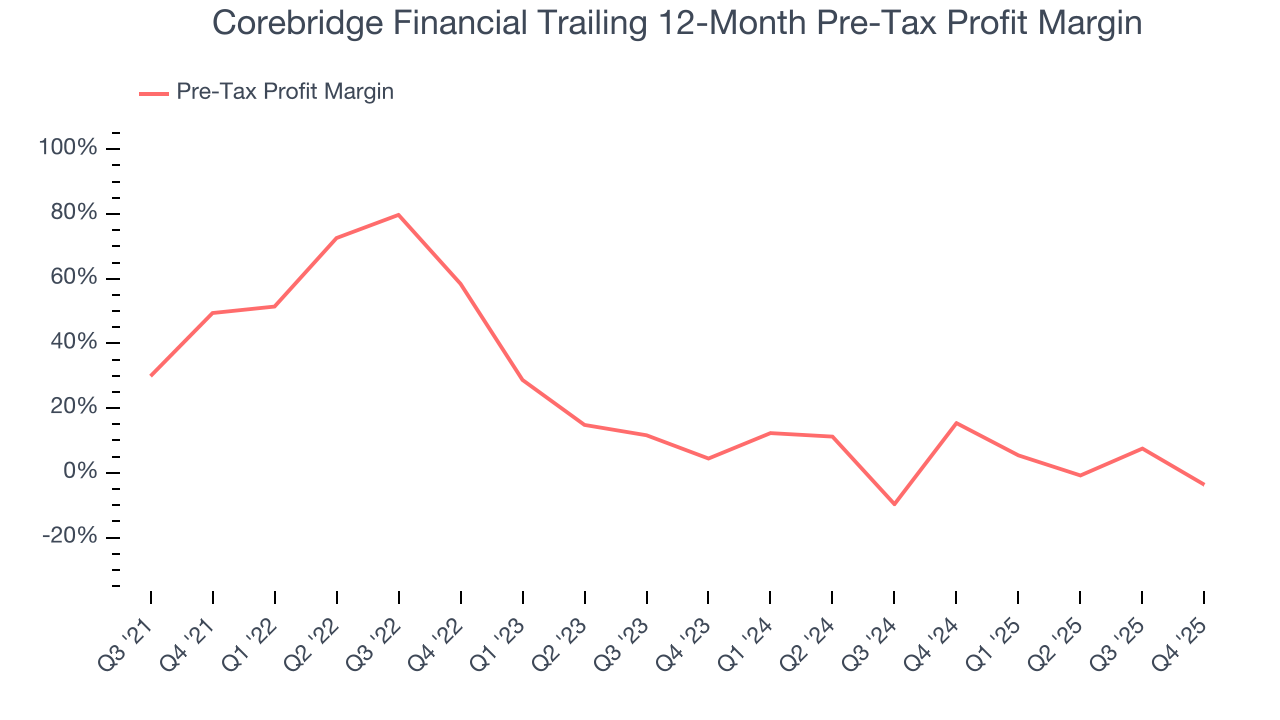

7. Pre-Tax Profit Margin

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For insurance companies, we look at pre-tax profit rather than the operating margin that defines sectors such as consumer, tech, and industrials.

Insurance companies are balance sheet businesses, where assets and liabilities define the economics. Interest income and expense should therefore be factored into the definition of profit but taxes - which are largely out of a company’s control - should not. This is pre-tax profit by definition.

Over the last four years, Corebridge Financial’s pre-tax profit margin has risen by 53.1 percentage points, going from 49.4% to negative 3.7%. It has also declined by 8.1 percentage points on a two-year basis, showing its expenses have consistently increased at a faster rate than revenue. This usually raises questions unless the company is in high-growth mode and reinvesting its profits into attractive ventures.

Corebridge Financial’s pre-tax profit margin came in at 12% this quarter. This result was 50.6 percentage points worse than the same quarter last year.

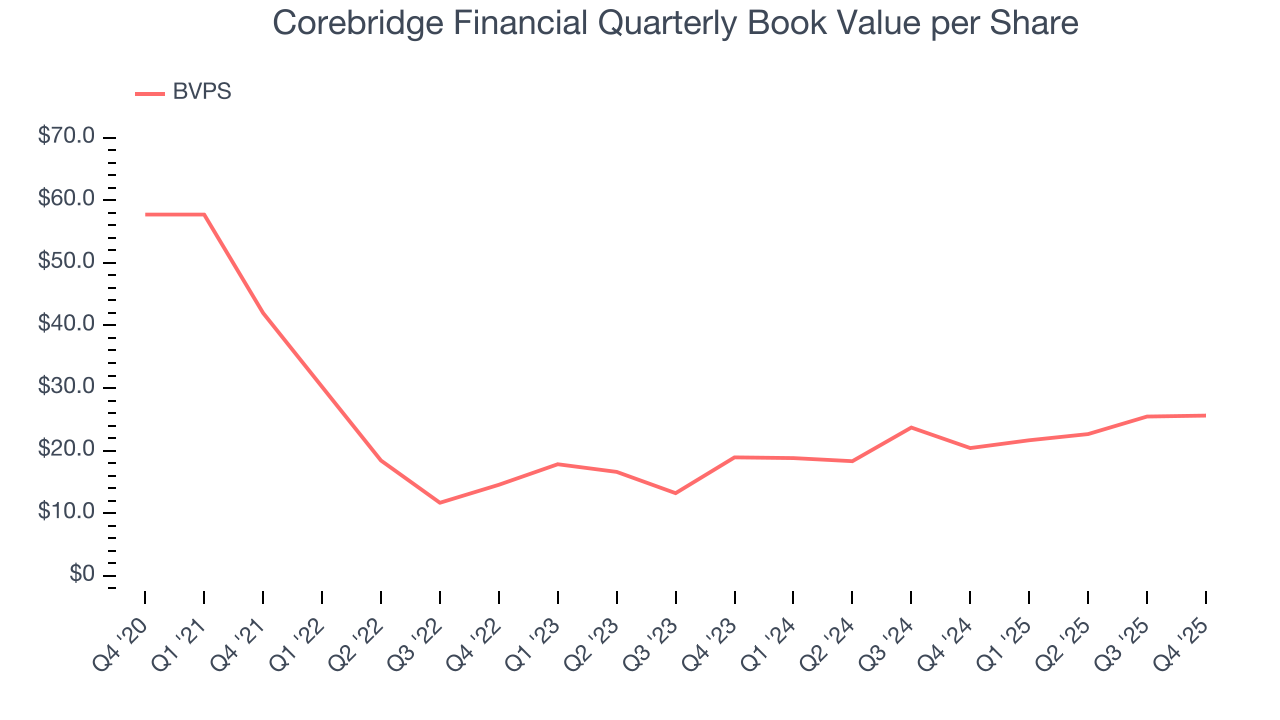

8. Book Value Per Share (BVPS)

Insurance companies are balance sheet businesses, collecting premiums upfront and paying out claims over time. The float–premiums collected but not yet paid out–are invested, creating an asset base supported by a liability structure. Book value per share (BVPS) captures this dynamic by measuring these assets (investment portfolio, cash, reinsurance recoverables) less liabilities (claim reserves, debt, future policy benefits). BVPS is essentially the residual value for shareholders.

We therefore consider BVPS very important to track for insurers and a metric that sheds light on business quality because it reflects long-term capital growth and is harder to manipulate than more commonly-used metrics like EPS.

Corebridge Financial’s BVPS declined at a 15% annual clip over the last five years. However, BVPS growth has accelerated recently, growing by 16.3% annually over the last two years from $18.93 to $25.60 per share.

9. Balance Sheet Assessment

The debt-to-equity ratio is a widely used measure to assess a company's balance sheet health. A higher ratio means that a business aggressively financed its growth with debt. This can result in higher earnings (if the borrowed funds are invested profitably) but also increases risk.

If debt levels are too high, there could be difficulties in meeting obligations, especially during economic downturns or periods of rising interest rates if the debt has variable-rate payments.

Corebridge Financial has no debt, so leverage is not an issue here.

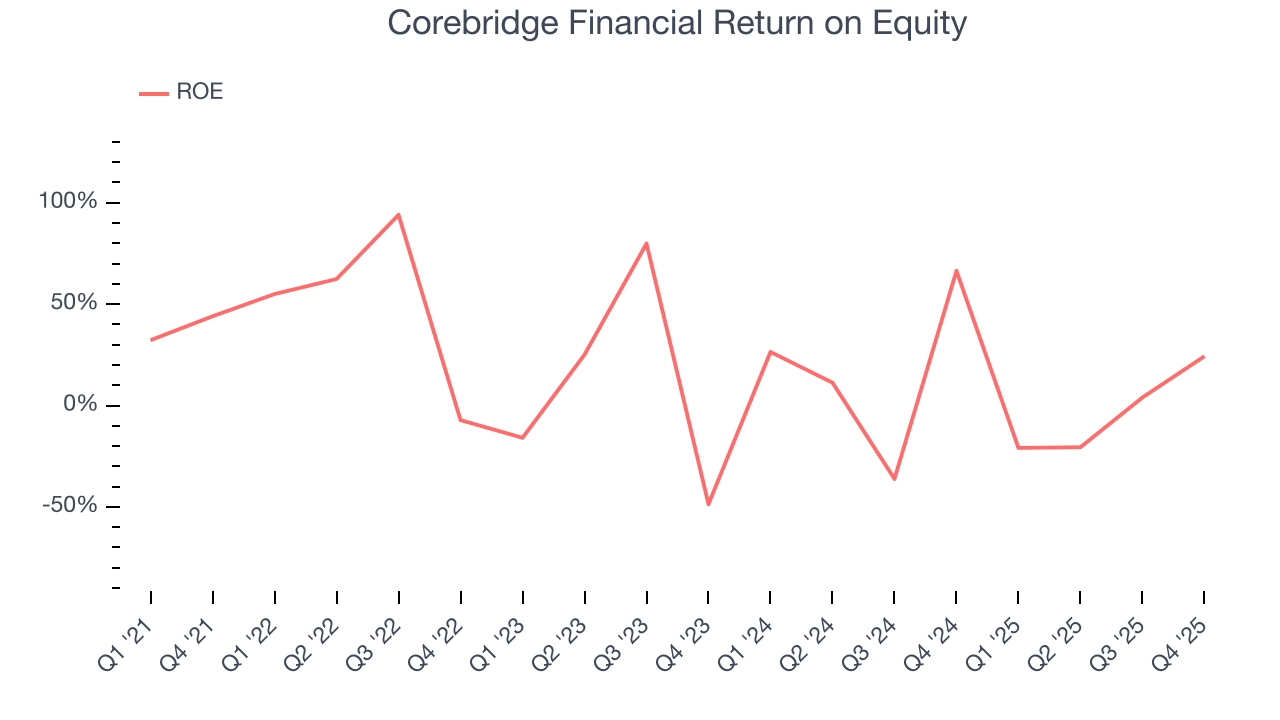

10. Return on Equity

Return on equity (ROE) serves as a comprehensive measure of an insurer's performance, showing how efficiently it converts shareholder capital into profits. Strong ROE performance typically translates to better returns for investors through a combination of earnings retention, share repurchases, and dividend distributions.

Over the last five years, Corebridge Financial has averaged an ROE of 20.9%, exceptional for a company operating in a sector where the average shakes out around 12.5% and those putting up 20%+ are greatly admired. This is a bright spot for Corebridge Financial.

11. Key Takeaways from Corebridge Financial’s Q4 Results

We were impressed by how significantly Corebridge Financial blew past analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Zooming out, we think this was a solid print. The stock remained flat at $31.38 immediately following the results.

12. Is Now The Time To Buy Corebridge Financial?

Updated: February 10, 2026 at 11:29 PM EST

Before investing in or passing on Corebridge Financial, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

Corebridge Financial doesn’t pass our quality test. To kick things off, its revenue growth was uninspiring over the last five years, and analysts expect its demand to deteriorate over the next 12 months. And while its stellar ROE suggests it has been a well-run company historically, the downside is its BVPS has declined over the last five years. On top of that, its declining pre-tax profit margin shows the business has become less efficient.

Corebridge Financial’s P/B ratio based on the next 12 months is 1.1x. While this valuation is fair, the upside isn’t great compared to the potential downside. There are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $37.23 on the company (compared to the current share price of $31.44).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.