Brinker International (EAT)

We aren’t fans of Brinker International. Its sales and earnings are expected to be muted over the next 12 months, implying a dearth of catalysts.― StockStory Analyst Team

1. News

2. Summary

Why Brinker International Is Not Exciting

Founded by Norman Brinker in Dallas, Brinker International (NYSE:EAT) is a casual restaurant chain that operates the Chili’s, Maggiano’s Little Italy, and It’s Just Wings banners.

- Lacking pricing power results in an inferior gross margin of 17% that must be offset by turning more tables

- Estimated sales growth of 3.7% for the next 12 months implies demand will slow from its six-year trend

- On the bright side, its average same-store sales growth of 15% over the past two years indicates its restaurants are resonating with diners

Brinker International doesn’t live up to our standards. There are more rewarding stocks elsewhere.

Why There Are Better Opportunities Than Brinker International

At $161.75 per share, Brinker International trades at 15.2x forward P/E. This multiple is lower than most restaurant companies, but for good reason.

Cheap stocks can look like great bargains at first glance, but you often get what you pay for. These mediocre businesses often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. Brinker International (EAT) Research Report: Q3 CY2025 Update

Casual restaurant chain Brinker International (NYSE:EAT) reported revenue ahead of Wall Streets expectations in Q3 CY2025, with sales up 18.5% year on year to $1.35 billion. On the other hand, the company’s full-year revenue guidance of $5.65 billion at the midpoint came in 1.2% below analysts’ estimates. Its non-GAAP profit of $1.93 per share was 8.8% above analysts’ consensus estimates.

Brinker International (EAT) Q3 CY2025 Highlights:

- Revenue: $1.35 billion vs analyst estimates of $1.33 billion (18.5% year-on-year growth, 1.3% beat)

- Adjusted EPS: $1.93 vs analyst estimates of $1.77 (8.8% beat)

- Adjusted EBITDA: $172.4 million vs analyst estimates of $167.3 million (12.8% margin, 3% beat)

- The company reconfirmed its revenue guidance for the full year of $5.65 billion at the midpoint

- Management reiterated its full-year Adjusted EPS guidance of $10.20 at the midpoint

- Operating Margin: 8.7%, up from 5% in the same quarter last year

- Free Cash Flow Margin: 4.6%, up from 0.6% in the same quarter last year

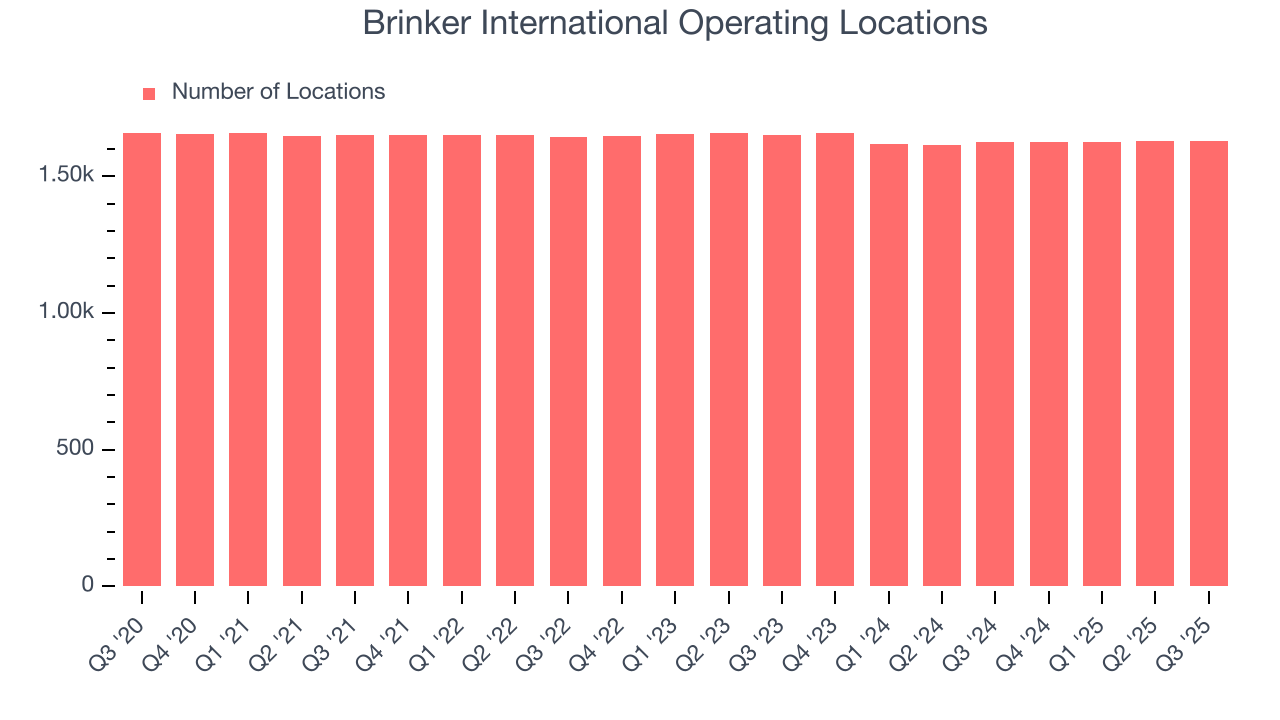

- Locations: 1,630 at quarter end, up from 1,625 in the same quarter last year

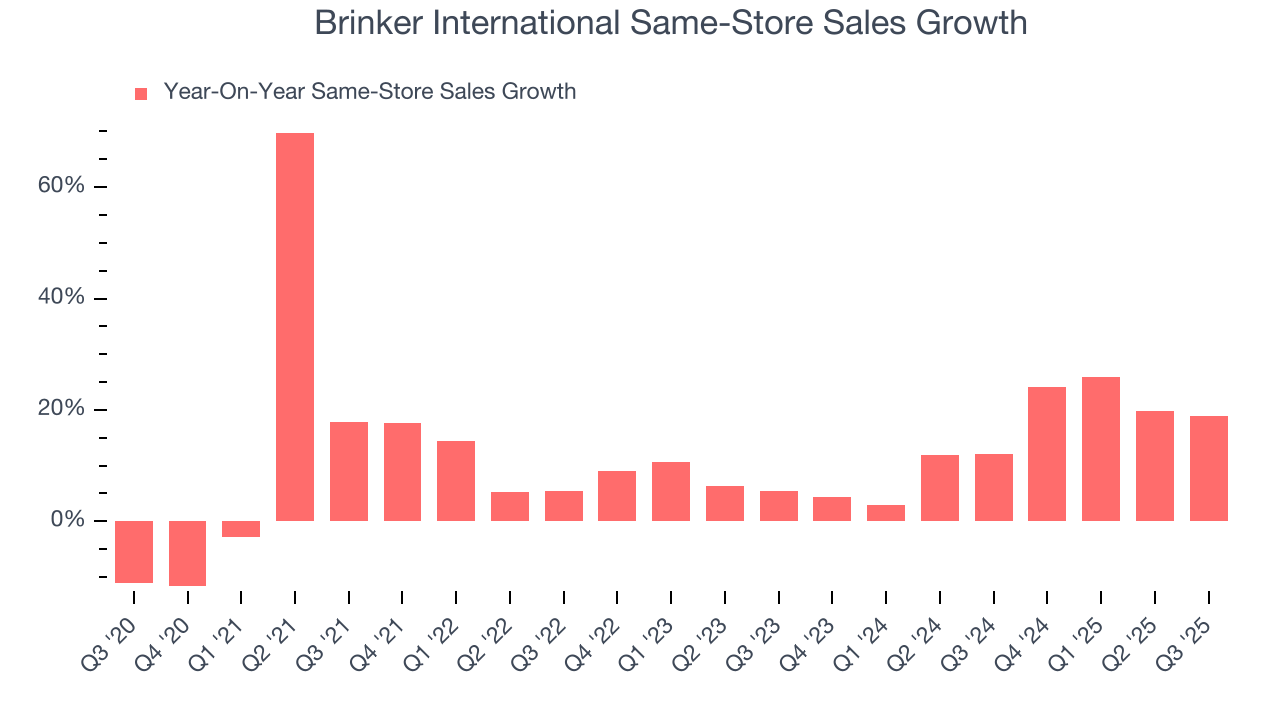

- Same-Store Sales rose 18.9% year on year (12% in the same quarter last year)

- Market Capitalization: $5.52 billion

Company Overview

Founded by Norman Brinker in Dallas, Brinker International (NYSE:EAT) is a casual restaurant chain that operates the Chili’s, Maggiano’s Little Italy, and It’s Just Wings banners.

The company’s history starts with its 1983 acquisition of Chili’s, which at the time was a Dallas burger joint. Chili’s became the cornerstone of Brinker’s portfolio, and the parent company expanded the Chili’s menu and experience to feature Southwestern American casual fare. Today, Chili’s most famous dish is its Baby Back Ribs.

From that initial acquisition, Brinker has added to its portfolio. The focus was familiar, comfort food served in an inviting family atmosphere. Maggiano’s Little Italy offers big plates of pasta and classic dishes like Chicken Parmasean for the table to share. Just Wings is exactly what the name describes, and it is actually a virtual restaurant. Customers order through an app and have the product delivered, which means there is no physical store to visit and dine in.

For Chili’s and Maggiano’s, the core customer is a middle-income family looking for a nice, full service dinner out. They don’t want to break the bank or visit a restaurant that is too stuffy and serious, though. The Just Wings customer is more tech savvy since the concept is a virtual one. This customer also values the convenience of home delivery.

4. Sit-Down Dining

Sit-down restaurants offer a complete dining experience with table service. These establishments span various cuisines and are renowned for their warm hospitality and welcoming ambiance, making them perfect for family gatherings, special occasions, or simply unwinding. Their extensive menus range from appetizers to indulgent desserts and wines and cocktails. This space is extremely fragmented and competition includes everything from publicly-traded companies owning multiple chains to single-location mom-and-pop restaurants.

Multi-brand full-service restaurant competitors include Darden (NYSE:DRI), Bloomin’ Brands (NASDAQ:BLMN), Dine Brands (NYSE:DIN), and The Cheesecake Factory (NASDAQ:CAKE).

5. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $5.59 billion in revenue over the past 12 months, Brinker International is one of the larger restaurant chains in the industry and benefits from a well-known brand that influences consumer purchasing decisions.

As you can see below, Brinker International’s sales grew at a decent 9.5% compounded annual growth rate over the last six years (we compare to 2019 to normalize for COVID-19 impacts) despite not opening many new restaurants, implying that growth was driven by higher sales at existing, established dining locations.

This quarter, Brinker International reported year-on-year revenue growth of 18.5%, and its $1.35 billion of revenue exceeded Wall Street’s estimates by 1.3%.

Looking ahead, sell-side analysts expect revenue to grow 3.2% over the next 12 months, a deceleration versus the last six years. This projection is underwhelming and implies its menu offerings will see some demand headwinds. At least the company is tracking well in other measures of financial health.

6. Restaurant Performance

Number of Restaurants

A restaurant chain’s total number of dining locations often determines how much revenue it can generate.

Brinker International operated 1,630 locations in the latest quarter, and over the last two years, has kept its restaurant count flat while other restaurant businesses have opted for growth.

When a chain doesn’t open many new restaurants, it usually means there’s stable demand for its meals and it’s focused on improving operational efficiency to increase profitability.

Same-Store Sales

The change in a company's restaurant base only tells one side of the story. The other is the performance of its existing locations, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales gives us insight into this topic because it measures organic growth at restaurants open for at least a year.

Brinker International has been one of the most successful restaurant chains over the last two years thanks to skyrocketing demand within its existing dining locations. On average, the company has posted exceptional year-on-year same-store sales growth of 15%. Given its flat restaurant base over the same period, this performance stems from a mixture of higher prices and increased foot traffic at existing locations.

In the latest quarter, Brinker International’s same-store sales rose 18.9% year on year. This growth was an acceleration from its historical levels, which is always an encouraging sign.

7. Gross Margin & Pricing Power

Gross profit margins tell us how much money a restaurant gets to keep after paying for the direct costs of the meals it sells, like ingredients, and indicate its level of pricing power.

Brinker International has bad unit economics for a restaurant company, signaling it operates in a competitive market and has little room for error if demand unexpectedly falls. As you can see below, it averaged a 17% gross margin over the last two years. Said differently, Brinker International had to pay a chunky $82.99 to its suppliers for every $100 in revenue.

This quarter, Brinker International’s gross profit margin was 17%, up 2.7 percentage points year on year. Brinker International’s full-year margin has also been trending up over the past 12 months, increasing by 3.9 percentage points. If this move continues, it could suggest better unit economics due to more leverage from its growing sales on the fixed portion of its cost of goods sold

8. Operating Margin

Brinker International has done a decent job managing its cost base over the last two years. The company has produced an average operating margin of 8.2%, higher than the broader restaurant sector.

Analyzing the trend in its profitability, Brinker International’s operating margin rose by 4.5 percentage points over the last year, as its sales growth gave it immense operating leverage.

This quarter, Brinker International generated an operating margin profit margin of 8.7%, up 3.8 percentage points year on year. The increase was encouraging, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, and administrative overhead.

9. Earnings Per Share

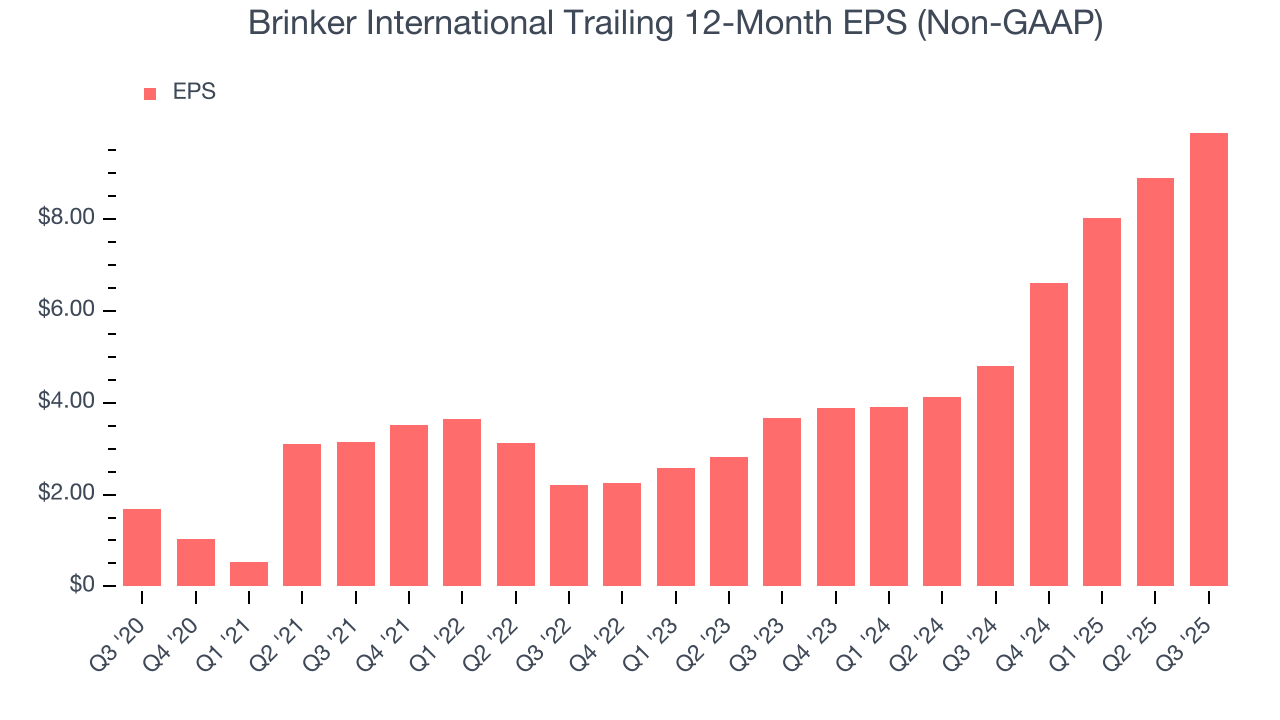

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Brinker International’s EPS grew at a decent 16.7% compounded annual growth rate over the last six years, higher than its 9.5% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

In Q3, Brinker International reported adjusted EPS of $1.93, up from $0.95 in the same quarter last year. This print beat analysts’ estimates by 8.8%. Over the next 12 months, Wall Street expects Brinker International’s full-year EPS of $9.88 to grow 8.1%.

10. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Brinker International has shown impressive cash profitability, giving it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 6.8% over the last two years, better than the broader restaurant sector.

Taking a step back, we can see that Brinker International’s margin expanded by 3.6 percentage points over the last year. This is encouraging because it gives the company more optionality.

Brinker International’s free cash flow clocked in at $62.2 million in Q3, equivalent to a 4.6% margin. This result was good as its margin was 4.1 percentage points higher than in the same quarter last year, building on its favorable historical trend.

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Brinker International’s five-year average ROIC was 13.6%, beating other restaurant companies by a wide margin. This illustrates its management team’s ability to invest in attractive growth opportunities and produce tangible results for shareholders.

12. Balance Sheet Assessment

Brinker International reported $33.6 million of cash and $1.68 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $821.2 million of EBITDA over the last 12 months, we view Brinker International’s 2.0× net-debt-to-EBITDA ratio as safe. We also see its $28.3 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

13. Key Takeaways from Brinker International’s Q3 Results

We were impressed by how significantly Brinker International beat analysts’ same-store sales expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. On the other hand, its full-year revenue guidance slightly missed and its full-year EPS guidance fell short of Wall Street’s estimates. This forward outlook is weighing on shares, and the stock traded down 6.6% to $116 immediately after reporting.

14. Is Now The Time To Buy Brinker International?

Updated: January 24, 2026 at 9:39 PM EST

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Brinker International.

Brinker International has some positive attributes, but it isn’t one of our picks. First off, its revenue growth was solid over the last six years. And while Brinker International’s gross margins make it more challenging to reach positive operating profits compared to other restaurant businesses, its marvelous same-store sales growth is on another level.

Brinker International’s P/E ratio based on the next 12 months is 15.2x. This valuation multiple is fair, but we don’t have much faith in the company. We're fairly confident there are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $179.05 on the company (compared to the current share price of $161.75).