Estée Lauder (EL)

Estée Lauder doesn’t excite us. Its low returns on capital and plummeting sales suggest it struggles to generate demand and profits, a red flag.― StockStory Analyst Team

1. News

2. Summary

Why We Think Estée Lauder Will Underperform

Named after its founder, who was an entrepreneurial woman from New York with a passion for skincare, Estée Lauder (NYSE:EL) is a one-stop beauty shop with products in skincare, fragrance, makeup, sun protection, and men’s grooming.

- Products have few die-hard fans as sales have declined by 5.8% annually over the last three years

- Sales were less profitable over the last three years as its earnings per share fell by 36.9% annually, worse than its revenue declines

- A silver lining is that its differentiated product offerings are difficult to replicate at scale and result in a best-in-class gross margin of 73.2%

Estée Lauder doesn’t check our boxes. There are better opportunities in the market.

Why There Are Better Opportunities Than Estée Lauder

Estée Lauder is trading at $120.42 per share, or 49.5x forward P/E. The current multiple is quite expensive, especially for the tepid revenue growth.

There are stocks out there similarly priced with better business quality. We prefer owning these.

3. Estée Lauder (EL) Research Report: Q4 CY2025 Update

Beauty products company Estée Lauder (NYSE:EL) met Wall Street’s revenue expectations in Q4 CY2025, with sales up 5.6% year on year to $4.23 billion. Its non-GAAP profit of $0.89 per share was 6.6% above analysts’ consensus estimates.

Estée Lauder (EL) Q4 CY2025 Highlights:

- Revenue: $4.23 billion vs analyst estimates of $4.22 billion (5.6% year-on-year growth, in line)

- Adjusted EPS: $0.89 vs analyst estimates of $0.83 (6.6% beat)

- Management raised its full-year Adjusted EPS guidance to $2.15 at the midpoint, a 7.5% increase

- Operating Margin: 9.5%, up from -14.5% in the same quarter last year

- Free Cash Flow Margin: 24%, similar to the same quarter last year

- Organic Revenue rose 4% year on year (beat)

- Market Capitalization: $43.1 billion

Company Overview

Named after its founder, who was an entrepreneurial woman from New York with a passion for skincare, Estée Lauder (NYSE:EL) is a one-stop beauty shop with products in skincare, fragrance, makeup, sun protection, and men’s grooming.

In addition to its namesake brand, the company also goes to market with the Clinique, MAC, Bobbi Brown, and La Mer brands. While there are differences between the brands, the unifying theme is quality and elegance.

Estée Lauder caters to a broad spectrum of beauty enthusiasts, but their core customer is a more affluent adult woman. This woman isn’t afraid to pay a premium for trusted brands and wants beauty products that are effective. To meet her needs, the company maintains an air of exclusivity through a combination of aspirational marketing, thoughtful distribution, and product innovation.

Estée Lauder's products are most commonly found in upscale department stores like Nordstrom (NYSE:JWN) and Bloomingdale's as well as specialty beauty retailers such as Ulta Beauty (NASDAQ:ULTA) and Sephora. The company also strategically places its products in luxury boutiques and upscale spas to maintain its premium image. On the other hand, Estée Lauder will generally not be found in drugstores, lower-tier department stores, or discount chains.

4. Personal Care

While personal care products products may seem more discretionary than food, consumers tend to maintain or even boost their spending on the category during tough times. This phenomenon is known as "the lipstick effect" by economists, which states that consumers still want some semblance of affordable luxuries like beauty and wellness when the economy is sputtering. Consumer tastes are constantly changing, and personal care companies are currently responding to the public’s increased desire for ethically produced goods by featuring natural ingredients in their products.

Competitors that offer a wide range of beauty and cosmetics products include L’Oreal (ENXTPA:OR), Coty (NYSE:COTY), Proctor & Gamble (NYSE:PG), and private company Revlon.

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

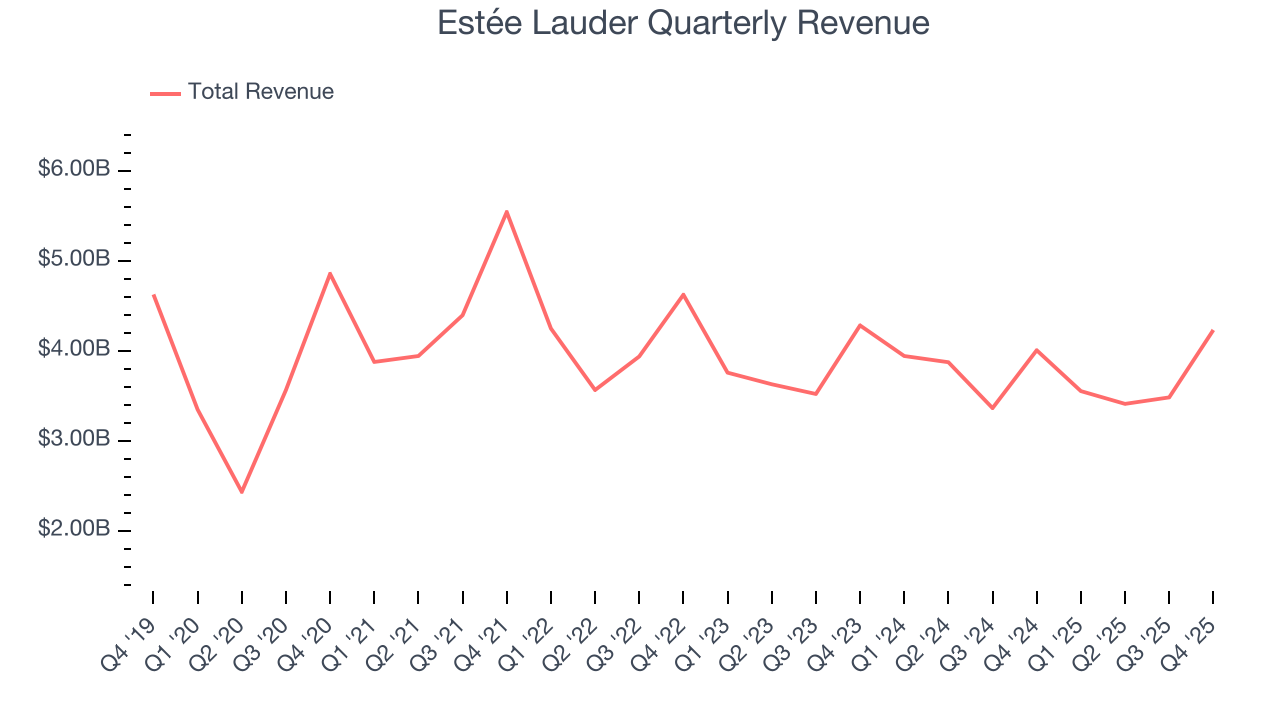

With $14.67 billion in revenue over the past 12 months, Estée Lauder is one of the larger consumer staples companies and benefits from a well-known brand that influences purchasing decisions. However, its scale is a double-edged sword because there are only a finite number of major retail partners, placing a ceiling on its growth. To accelerate sales, Estée Lauder likely needs to optimize its pricing or lean into new products and international expansion.

As you can see below, Estée Lauder struggled to generate demand over the last three years. Its sales dropped by 3.6% annually, a rough starting point for our analysis.

This quarter, Estée Lauder grew its revenue by 5.6% year on year, and its $4.23 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 4.2% over the next 12 months. Although this projection suggests its newer products will spur better top-line performance, it is still below the sector average.

6. Organic Revenue Growth

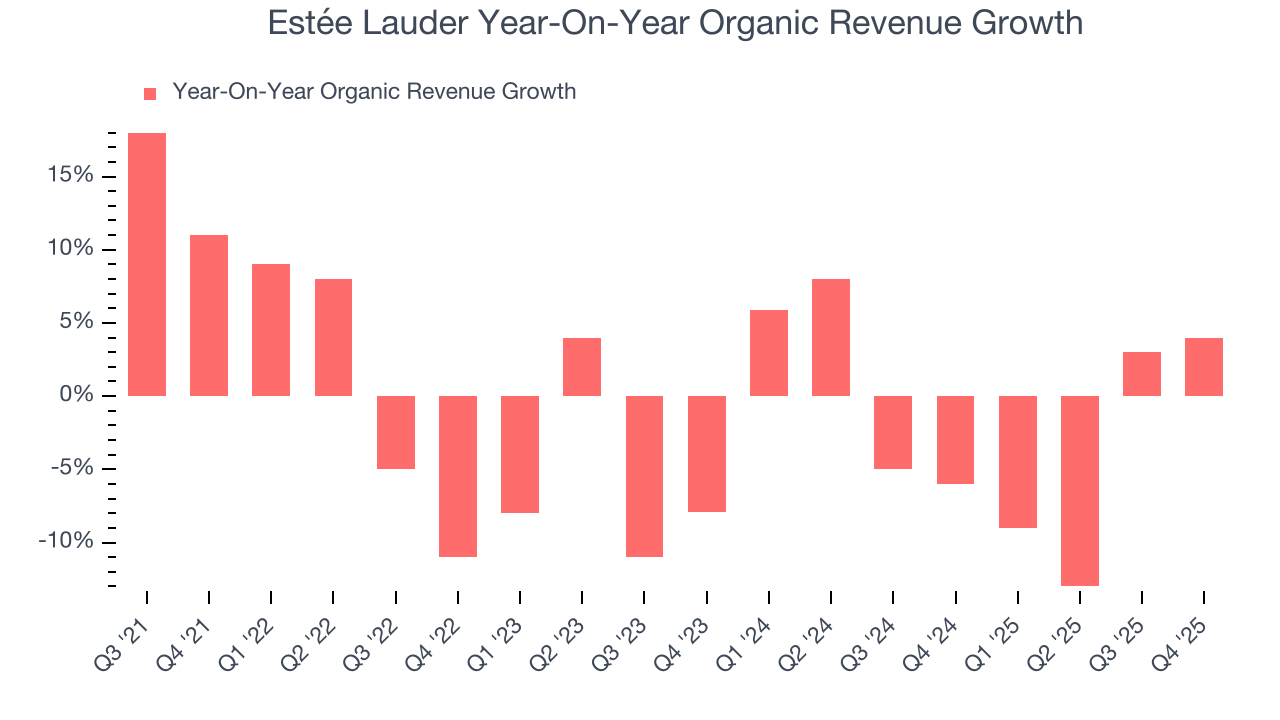

When analyzing revenue growth, we care most about organic revenue growth. This metric captures a business’s performance excluding one-time events such as mergers, acquisitions, and divestitures as well as foreign currency fluctuations.

Estée Lauder’s demand has been falling over the last eight quarters, and on average, its organic sales have declined by 1.5% year on year.

In the latest quarter, Estée Lauder’s organic sales rose by 4% year on year. This growth was a well-appreciated turnaround from its historical levels, showing the business is regaining momentum.

7. Gross Margin & Pricing Power

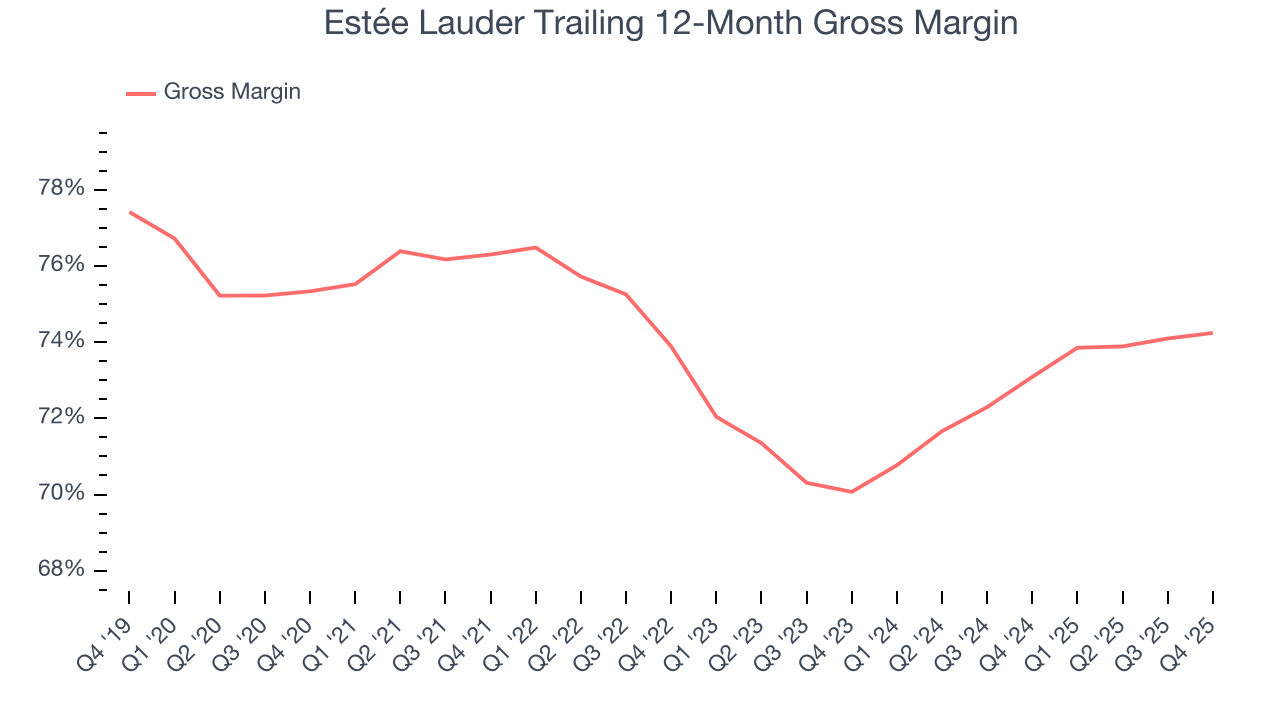

Estée Lauder has best-in-class unit economics for a consumer staples company, enabling it to invest in areas such as marketing and talent to grow its brand. As you can see below, it averaged an elite 73.7% gross margin over the last two years. That means for every $100 in revenue, only $26.34 went towards paying for raw materials, production of goods, transportation, and distribution.

In Q4, Estée Lauder produced a 76.5% gross profit margin, in line with the same quarter last year. On a wider time horizon, Estée Lauder’s full-year margin has been trending up over the past 12 months, increasing by 1.2 percentage points. If this move continues, it could suggest better unit economics due to more leverage from its growing sales on the fixed portion of its cost of goods sold (such as manufacturing expenses).

8. Operating Margin

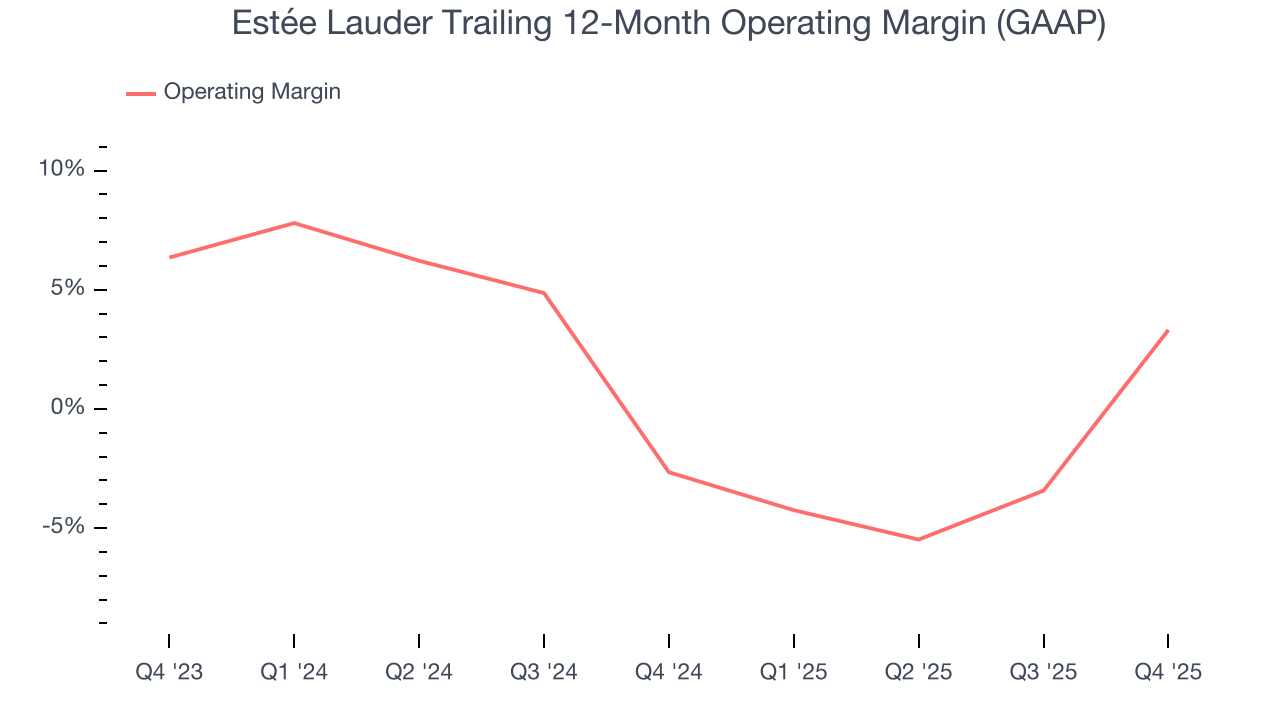

Estée Lauder was roughly breakeven when averaging the last two years of quarterly operating profits, lousy for a consumer staples business. This result is surprising given its high gross margin as a starting point.

On the plus side, Estée Lauder’s operating margin rose by 6 percentage points over the last year.

This quarter, Estée Lauder generated an operating margin profit margin of 9.5%, up 24 percentage points year on year. The increase was solid, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, and administrative overhead.

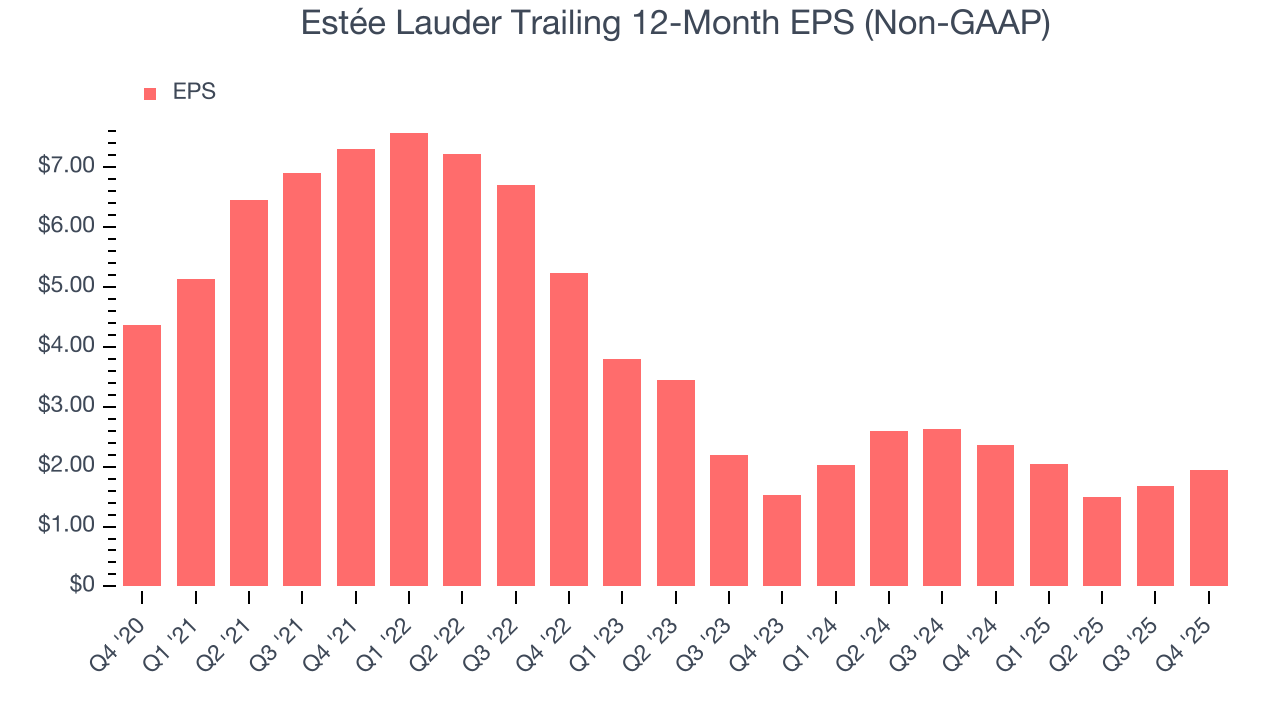

9. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Estée Lauder, its EPS declined by 28% annually over the last three years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

In Q4, Estée Lauder reported adjusted EPS of $0.89, up from $0.62 in the same quarter last year. This print beat analysts’ estimates by 6.6%. Over the next 12 months, Wall Street expects Estée Lauder’s full-year EPS of $1.95 to grow 31.5%.

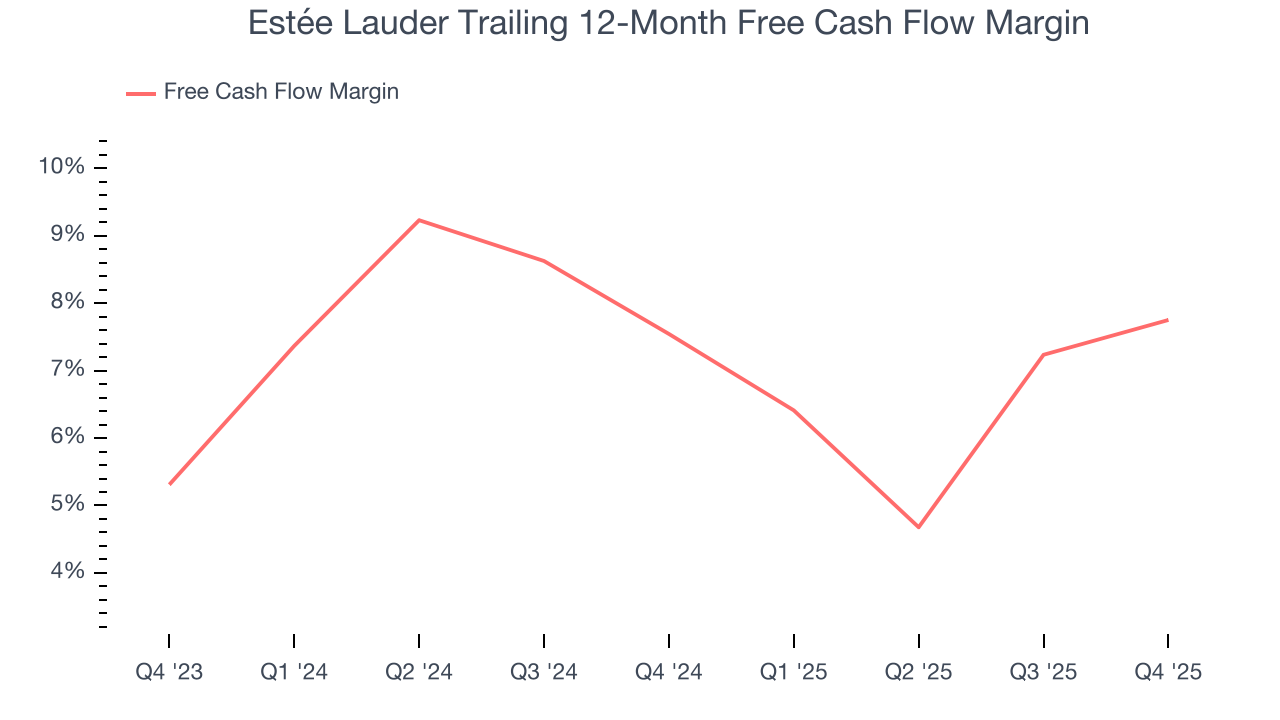

10. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Estée Lauder has shown impressive cash profitability, driven by its attractive business model that gives it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 7.6% over the last two years, better than the broader consumer staples sector. The divergence from its underwhelming operating margin stems from the add-back of non-cash charges like depreciation and stock-based compensation. GAAP operating profit expenses these line items, but free cash flow does not.

Estée Lauder’s free cash flow clocked in at $1.02 billion in Q4, equivalent to a 24% margin. This cash profitability was in line with the comparable period last year and above its two-year average.

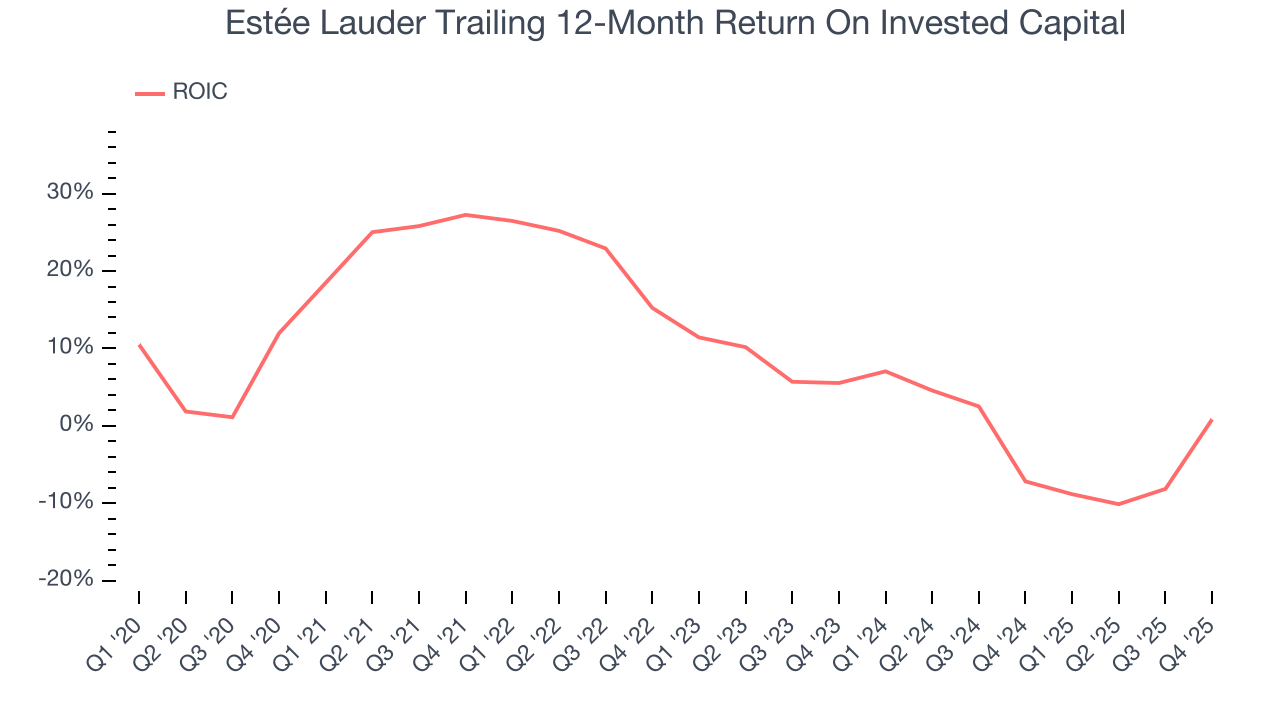

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Estée Lauder historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 8.3%, somewhat low compared to the best consumer staples companies that consistently pump out 20%+.

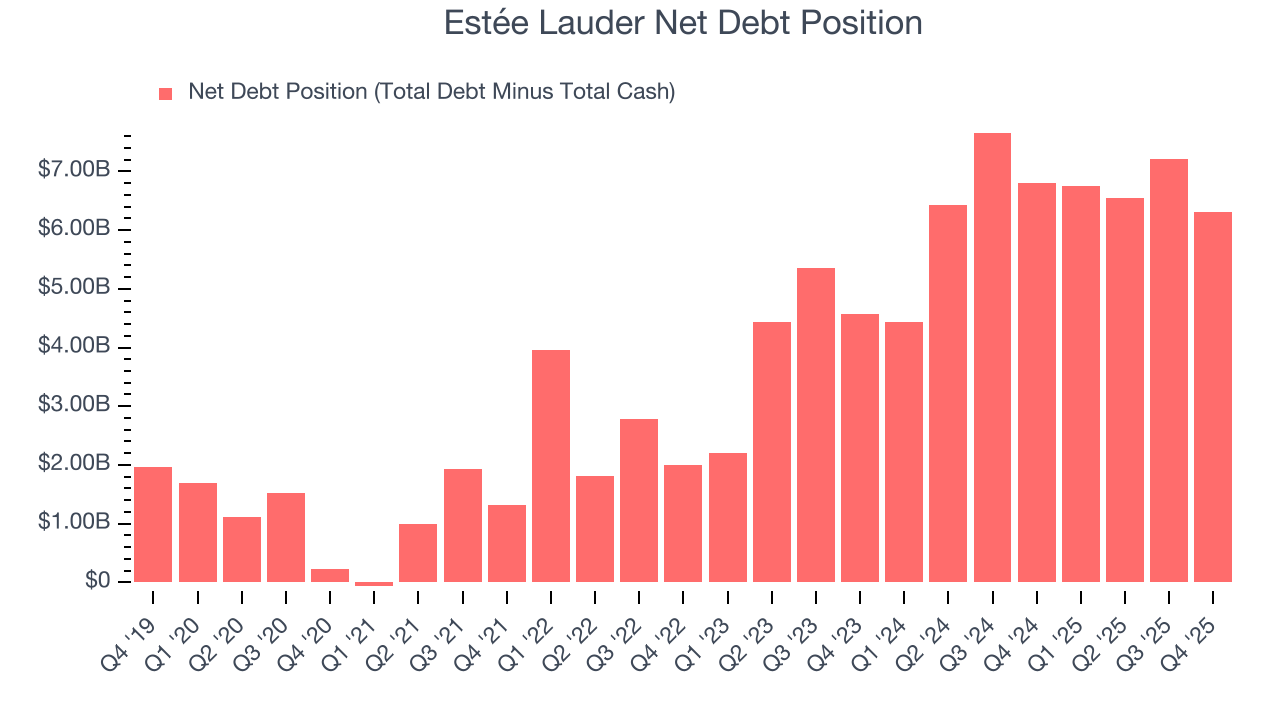

12. Balance Sheet Assessment

Estée Lauder reported $3.08 billion of cash and $9.39 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $1.92 billion of EBITDA over the last 12 months, we view Estée Lauder’s 3.3× net-debt-to-EBITDA ratio as safe. We also see its $111 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

13. Key Takeaways from Estée Lauder’s Q4 Results

It was good to see Estée Lauder narrowly top analysts’ organic revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its full-year EPS guidance fell slightly short of Wall Street’s estimates. This guide is weighing on shares. The stock traded down 7.9% to $110.18 immediately after reporting.

14. Is Now The Time To Buy Estée Lauder?

Updated: February 5, 2026 at 6:26 AM EST

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Estée Lauder.

Estée Lauder isn’t a terrible business, but it isn’t one of our picks. To kick things off, its revenue has declined over the last three years. And while its admirable gross margins are a wonderful starting point for the overall profitability of the business, the downside is its declining EPS over the last three years makes it a less attractive asset to the public markets. On top of that, its operating margins reveal poor profitability compared to other consumer staples companies.

Estée Lauder’s P/E ratio based on the next 12 months is 46.6x. At this valuation, there’s a lot of good news priced in - you can find more timely opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $109.75 on the company (compared to the current share price of $110.18).