e.l.f. Beauty (ELF)

e.l.f. Beauty is interesting. Its rare blend of fast revenue growth, attractive unit economics, and a strong outlook gives it upside.― StockStory Analyst Team

1. News

2. Summary

Why e.l.f. Beauty Is Interesting

Short for "eyes, lips, face", e.l.f. Beauty (NYSE:ELF) is a developer of high-quality beauty products at accessible price points.

- Annual revenue growth of 45.2% over the last three years was superb and indicates its market share is rising

- Notable projected revenue growth of 20.9% for the next 12 months hints at market share gains

- One risk is its smaller revenue base of $1.52 billion means it hasn’t achieved the economies of scale that some industry juggernauts enjoy (but also enables it to grow faster if it executes properly)

e.l.f. Beauty shows some potential. If you like the story, the valuation looks fair.

Why Is Now The Time To Buy e.l.f. Beauty?

e.l.f. Beauty is trading at $61.16 per share, or 20.3x forward P/E. While this multiple is higher than most consumer staples companies, we think the valuation is deserved for the revenue growth you get.

It could be a good time to invest if you see something the market doesn’t.

3. e.l.f. Beauty (ELF) Research Report: Q4 CY2025 Update

Cosmetics company e.l.f. Beauty (NYSE:ELF) announced better-than-expected revenue in Q4 CY2025, with sales up 37.8% year on year to $489.5 million. The company’s full-year revenue guidance of $1.61 billion at the midpoint came in 2.3% above analysts’ estimates. Its non-GAAP profit of $1.24 per share was 71.4% above analysts’ consensus estimates.

e.l.f. Beauty (ELF) Q4 CY2025 Highlights:

- Revenue: $489.5 million vs analyst estimates of $460.1 million (37.8% year-on-year growth, 6.4% beat)

- Adjusted EPS: $1.24 vs analyst estimates of $0.72 (71.4% beat)

- Adjusted EBITDA: $123 million vs analyst estimates of $82.65 million (25.1% margin, 48.9% beat)

- The company lifted its revenue guidance for the full year to $1.61 billion at the midpoint from $1.56 billion, a 2.9% increase

- Management raised its full-year Adjusted EPS guidance to $3.08 at the midpoint, a 8.8% increase

- EBITDA guidance for the full year is $324.5 million at the midpoint, above analyst estimates of $306.9 million

- Operating Margin: 13.8%, up from 9.9% in the same quarter last year

- Free Cash Flow was $52.79 million, up from -$19.76 million in the same quarter last year

- Market Capitalization: $5.06 billion

Company Overview

Short for "eyes, lips, face", e.l.f. Beauty (NYSE:ELF) is a developer of high-quality beauty products at accessible price points.

The company was founded in 2004 on a simple but “crazy” idea: sell premium cosmetics over the internet for $1. Today, e.l.f. has expanded its price points and distribution channels. Specifically, e.l.f. offers a wide range of makeup, skincare, and beauty tools such as mascara, face washes, and makeup brushes under its namesake brand.

e.l.f. targets the budget-conscious beauty enthusiast who is likely young and trend-conscious. Since these individuals are more likely to experiment with different looks and buy cosmetics with more frequency and breadth, the company’s affordable prices and trendy products are attractive. e.l.f. prides itself on selling its products at everyday low prices rather than running occasional promotions and sales.

e.l.f. products can be found in various types of retailers and businesses, making them easily accessible. Mass retailers such as Walmart (NYSE:WMT), national drug store chains such as CVS (NYSE:CVS), and beauty specialty stores such as Ulta (NASDAQ:ULTA) all carry e.l.f. Products. Additionally, e.l.f. allows consumers to buy directly from the company and access exclusive deals, beauty tutorials, and product recommendations.

4. Personal Care

While personal care products products may seem more discretionary than food, consumers tend to maintain or even boost their spending on the category during tough times. This phenomenon is known as "the lipstick effect" by economists, which states that consumers still want some semblance of affordable luxuries like beauty and wellness when the economy is sputtering. Consumer tastes are constantly changing, and personal care companies are currently responding to the public’s increased desire for ethically produced goods by featuring natural ingredients in their products.

Competitors that offer beauty or cosmetics products include Coty (NYSE:COTY), Estee Lauder (NYSE:EL), and L’Oreal (ENXTPA:OR).

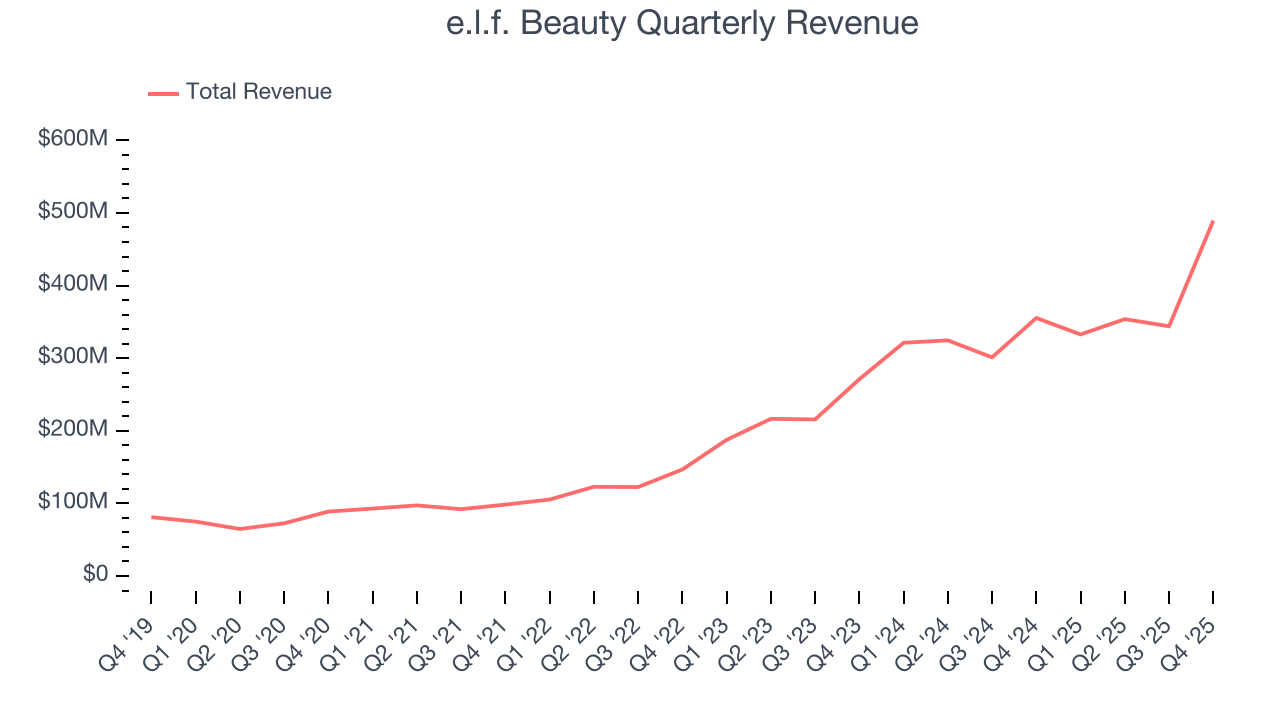

5. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $1.52 billion in revenue over the past 12 months, e.l.f. Beauty is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers. On the bright side, it can grow faster because it has a longer list of untapped store chains to sell into.

As you can see below, e.l.f. Beauty’s sales grew at an incredible 45.2% compounded annual growth rate over the last three years. This is an encouraging starting point for our analysis because it shows e.l.f. Beauty’s demand was higher than many consumer staples companies.

This quarter, e.l.f. Beauty reported wonderful year-on-year revenue growth of 37.8%, and its $489.5 million of revenue exceeded Wall Street’s estimates by 6.4%.

Looking ahead, sell-side analysts expect revenue to grow 17.6% over the next 12 months, a deceleration versus the last three years. Still, this projection is admirable and indicates the market is baking in success for its products.

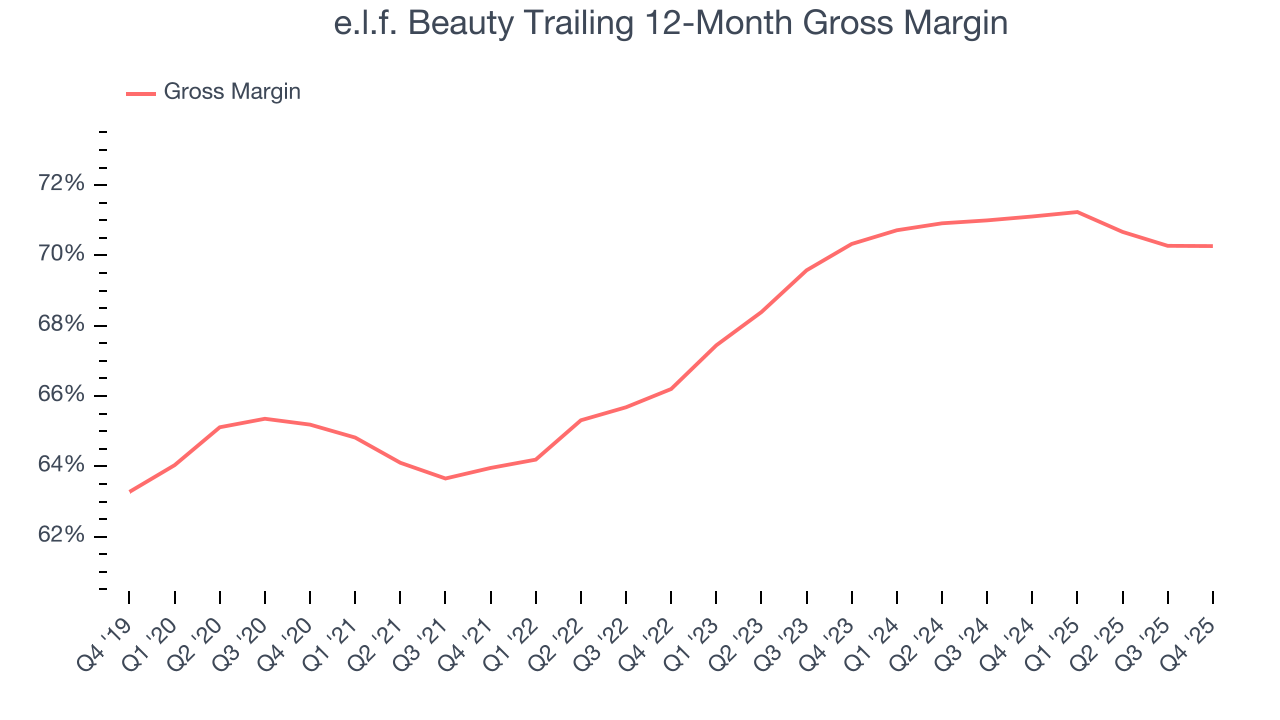

6. Gross Margin & Pricing Power

e.l.f. Beauty has best-in-class unit economics for a consumer staples company, enabling it to invest in areas such as marketing and talent to grow its brand. As you can see below, it averaged an elite 70.7% gross margin over the last two years. That means for every $100 in revenue, only $29.34 went towards paying for raw materials, production of goods, transportation, and distribution.

e.l.f. Beauty produced a 71% gross profit margin in Q4, in line with the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

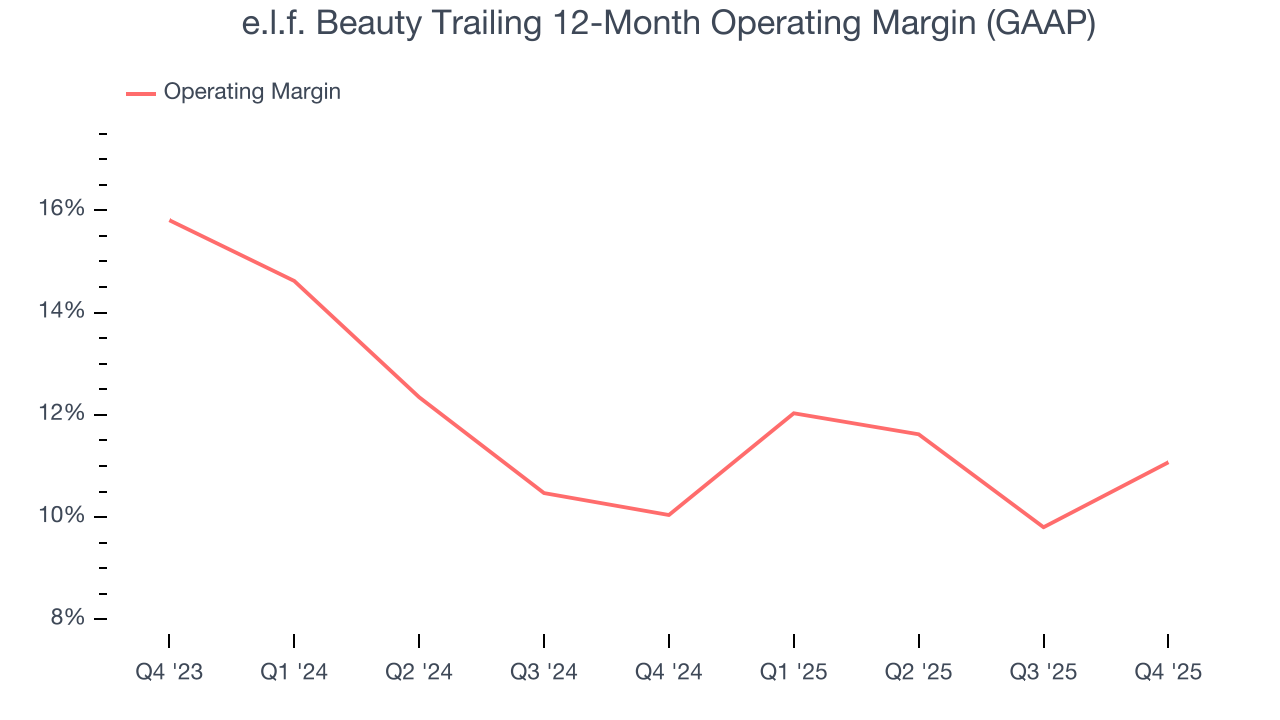

7. Operating Margin

e.l.f. Beauty has done a decent job managing its cost base over the last two years. The company has produced an average operating margin of 10.6%, higher than the broader consumer staples sector.

Looking at the trend in its profitability, e.l.f. Beauty’s operating margin rose by 1 percentage points over the last year, as its sales growth gave it operating leverage.

This quarter, e.l.f. Beauty generated an operating margin profit margin of 13.8%, up 3.9 percentage points year on year. The increase was encouraging, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, and administrative overhead.

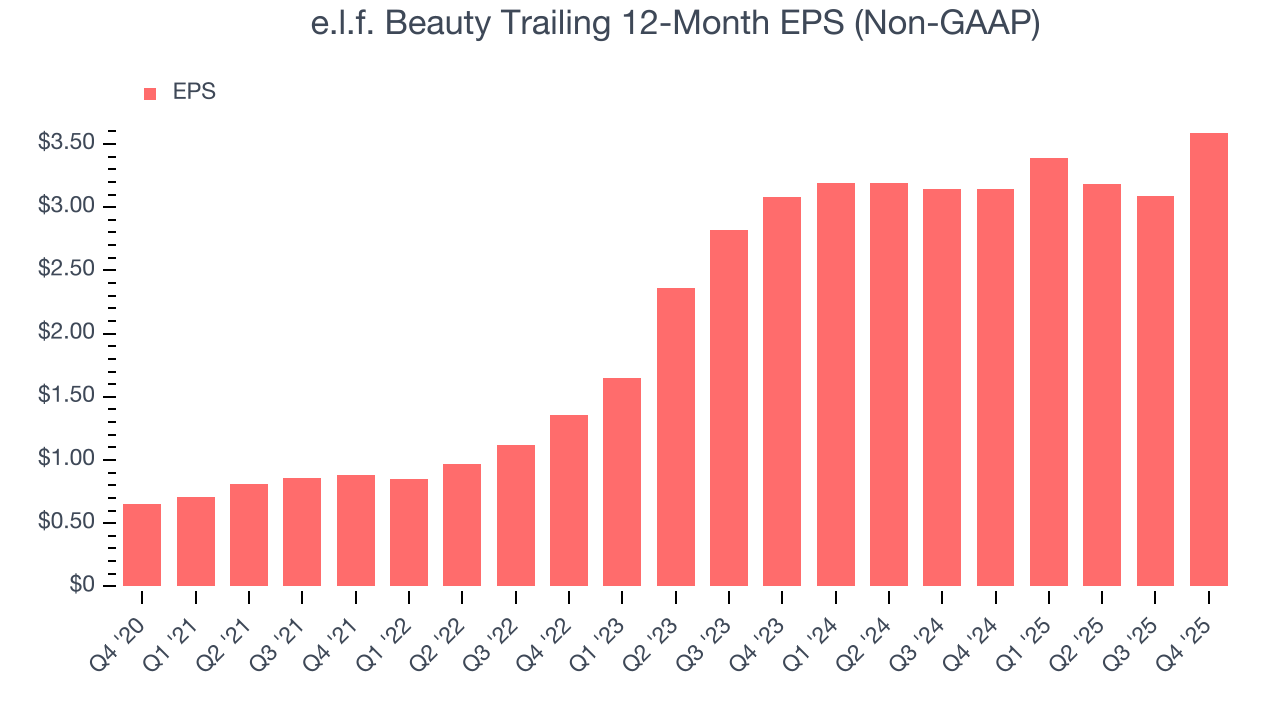

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

e.l.f. Beauty’s EPS grew at an astounding 38.2% compounded annual growth rate over the last three years. However, this performance was lower than its 45.2% annualized revenue growth, telling us the company became less profitable on a per-share basis as it expanded.

In Q4, e.l.f. Beauty reported adjusted EPS of $1.24, up from $0.74 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects e.l.f. Beauty’s full-year EPS of $3.59 to shrink by 10%.

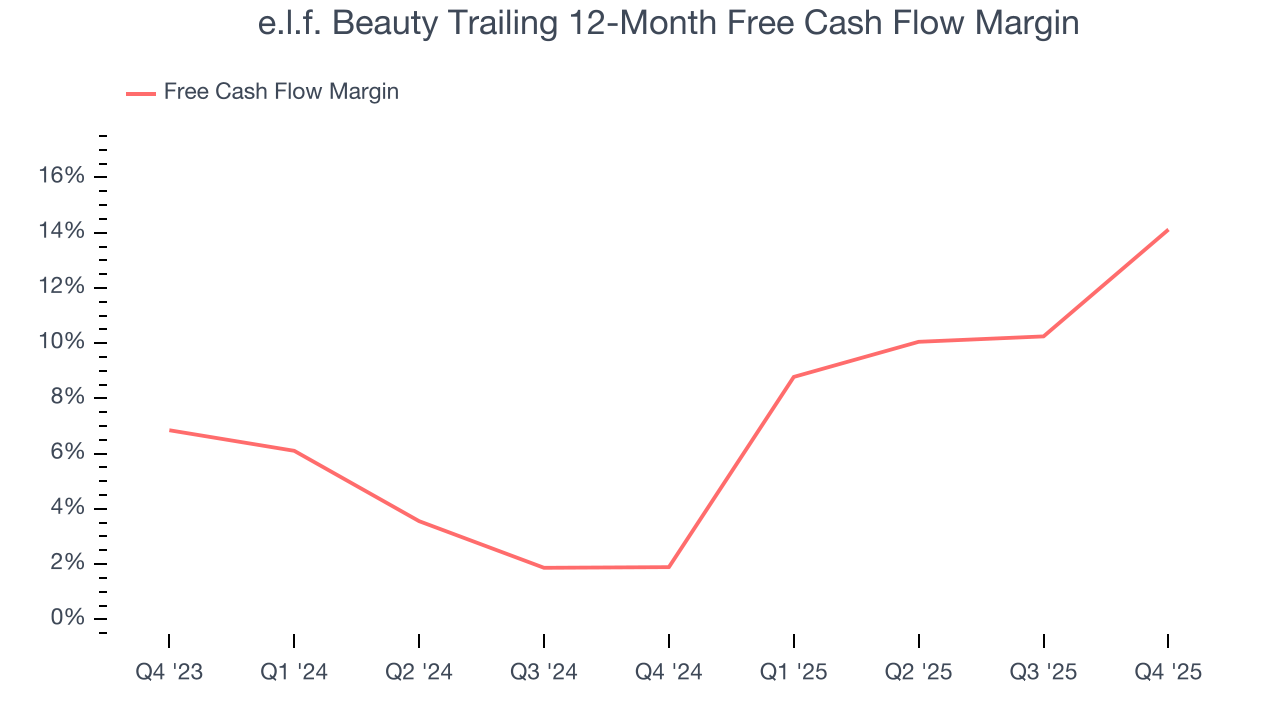

9. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

e.l.f. Beauty has shown impressive cash profitability, driven by its attractive business model that gives it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 8.5% over the last two years, better than the broader consumer staples sector.

Taking a step back, we can see that e.l.f. Beauty’s margin expanded by 12.2 percentage points over the last year. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

e.l.f. Beauty’s free cash flow clocked in at $52.79 million in Q4, equivalent to a 10.8% margin. Its cash flow turned positive after being negative in the same quarter last year, building on its favorable historical trend.

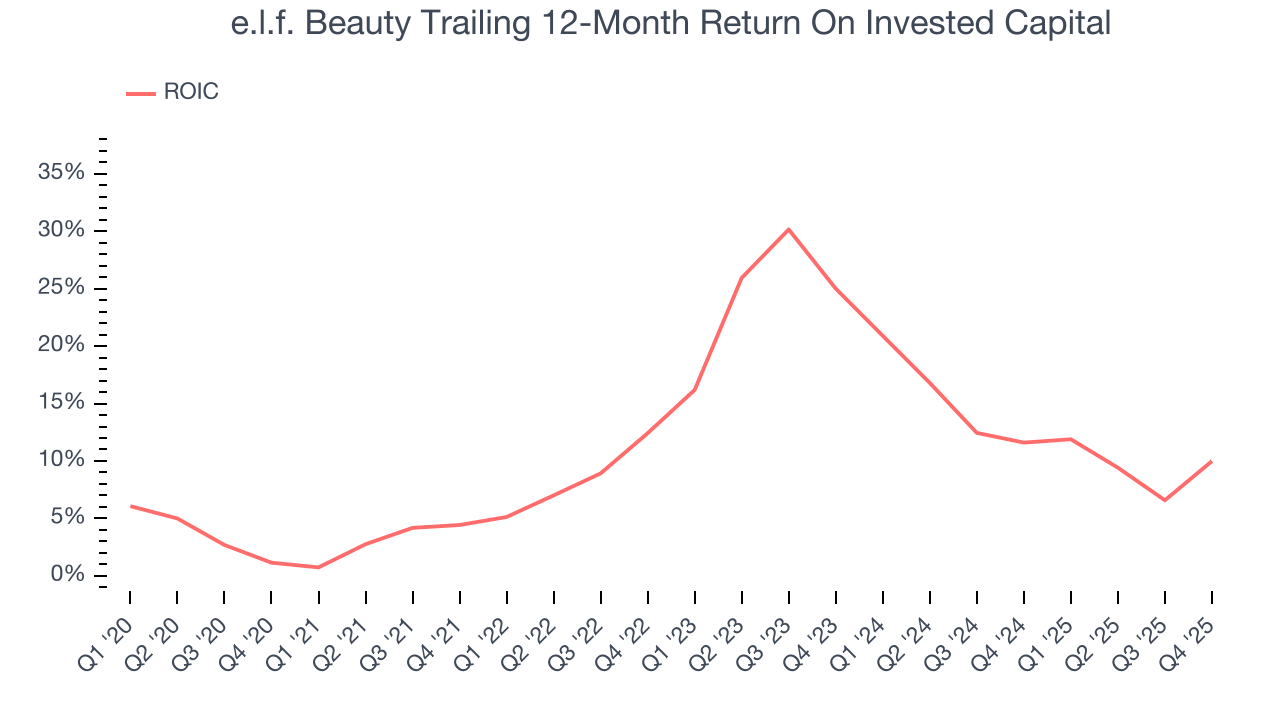

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

e.l.f. Beauty’s management team makes decent investment decisions and generates value for shareholders. Its five-year average ROIC was 12.7%, slightly better than typical consumer staples business.

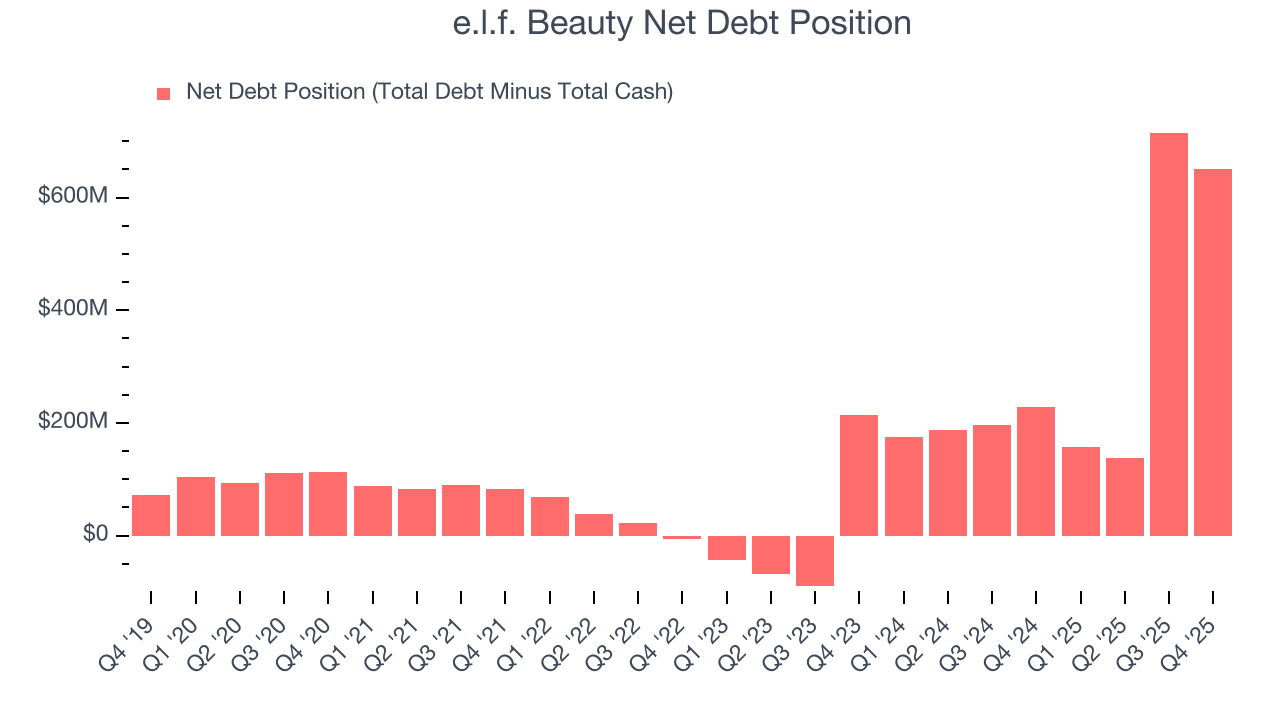

11. Balance Sheet Assessment

e.l.f. Beauty reported $196.8 million of cash and $846.7 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $357.7 million of EBITDA over the last 12 months, we view e.l.f. Beauty’s 1.8× net-debt-to-EBITDA ratio as safe. We also see its $27 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from e.l.f. Beauty’s Q4 Results

It was good to see e.l.f. Beauty beat analysts’ revenue and EPS expectations convincingly this quarter. We were also excited that the company raised full-year guidance for those two metrics. Zooming out, we think this quarter featured some important positives. The stock traded up 2.1% to $86.97 immediately after reporting.

13. Is Now The Time To Buy e.l.f. Beauty?

Updated: March 28, 2026 at 10:44 PM EDT

Before investing in or passing on e.l.f. Beauty, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

e.l.f. Beauty is a fine business. To kick things off, its revenue growth was exceptional over the last three years. And while its projected EPS for the next year is lacking, its admirable gross margins are a wonderful starting point for the overall profitability of the business. On top of that, its EPS growth over the last three years has been fantastic.

e.l.f. Beauty’s P/E ratio based on the next 12 months is 20.3x. Looking at the consumer staples landscape right now, e.l.f. Beauty trades at a pretty interesting price. If you’re a fan of the business and management team, now is a good time to scoop up some shares.

Wall Street analysts have a consensus one-year price target of $111.71 on the company (compared to the current share price of $61.16), implying they see 82.7% upside in buying e.l.f. Beauty in the short term.