Enova (ENVA)

Enova piques our interest, but the state of its balance sheet makes us slightly uncomfortable.― StockStory Analyst Team

1. News

2. Summary

Why Enova Is Not Exciting

Pioneering online lending since 2004 with a massive database of over 65 terabytes of customer behavior data, Enova International (NYSE:ENVA) provides online financial services including installment loans and lines of credit to non-prime consumers and small businesses in the United States and Brazil.

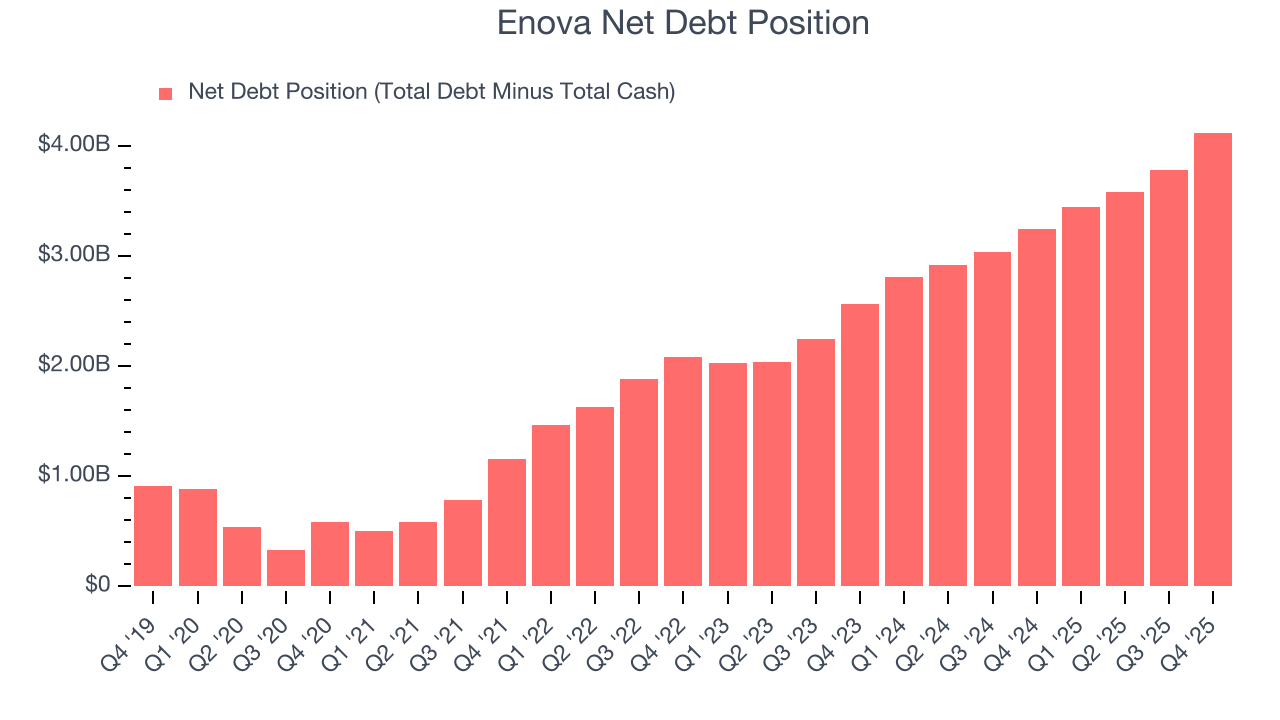

- High net-debt-to-EBITDA ratio of 5× increases the risk of forced asset sales or dilutive financing if operational performance weakens

Enova has some respectable qualities, but we’d hold off on buying the stock until its EBITDA can comfortably support its debt.

Why There Are Better Opportunities Than Enova

At $165.26 per share, Enova trades at 10.6x forward P/E. Yes, this valuation multiple is lower than that of other financials peers, but we’ll remind you that you often get what you pay for.

Our advice is to pay up for elite businesses whose advantages are tailwinds to earnings growth. Don’t get sucked into lower-quality businesses just because they seem like bargains. These mediocre businesses often never achieve a higher multiple as hoped, a phenomenon known as a “value trap”.

3. Enova (ENVA) Research Report: Q4 CY2025 Update

Financial technology company Enova International (NYSE:ENVA) met Wall Streets revenue expectations in Q4 CY2025, with sales up 15.1% year on year to $839.4 million. Its non-GAAP profit of $3.46 per share was 9.1% above analysts’ consensus estimates.

Correction Note:

The previous version of this report incorrectly stated that revenues were $501.9 million. This version has been updated to reflect the correct revenue figure of $839.4 million

Enova (ENVA) Q4 CY2025 Highlights:

- Revenue: $839.4 million vs analyst estimates of $838.1 million (15.1% year-on-year growth, in line)

- Pre-tax Profit: $98.78 million (11.8% margin)

- Adjusted EPS: $3.46 vs analyst estimates of $3.17 (9.1% beat)

- Book Value per Share: $54.08 (16.6% year-on-year growth)

- Market Capitalization: $4.08 billion

Company Overview

Pioneering online lending since 2004 with a massive database of over 65 terabytes of customer behavior data, Enova International (NYSE:ENVA) provides online financial services including installment loans and lines of credit to non-prime consumers and small businesses in the United States and Brazil.

Enova uses proprietary technology platforms and advanced analytics to quickly evaluate loan applications and make credit decisions. The company's machine learning-enabled models analyze data from over 65 terabytes of customer behavior information collected throughout its history, allowing it to assess risk more effectively than traditional credit scoring alone. This technology enables Enova to approve loans and provide funds to customers rapidly, often within the same day of application.

The company serves two distinct customer segments. Its consumer lending business targets individuals with an average annual household income of $38,000, typically with FICO scores between 500 and 680. For small businesses, Enova serves companies with median annual sales of approximately $594,000, with business owners generally having FICO scores between 650 and 780. Both customer groups often have bank accounts but limited access to traditional credit sources.

Enova offers several financial products across its markets. For consumers, these include installment loans ranging from $300 to $10,000 with terms between 3 and 60 months, and line of credit accounts with limits between $100 and $7,000. Small business products include installment loans between $5,000 and $250,000 with terms of 3 to 24 months, and lines of credit between $5,000 and $100,000. A customer seeking working capital might apply for a $15,000 small business loan through Enova's OnDeck platform, receive approval within hours, and use the funds to purchase inventory or equipment.

The company generates revenue primarily through interest and fees on its financial products. Enova operates in 37 states for consumer lending and 49 states for small business financing in the U.S., as well as in Brazil for consumer loans. It markets its products under several brands including CashNetUSA, NetCredit, OnDeck, Headway Capital, and Pangea, which provides international money transfer services.

4. Personal Loan

Personal loan providers offer unsecured credit for various consumer needs. The sector benefits from digital application processes, increasing consumer comfort with online financial services, and opportunities in underserved credit segments. Headwinds include credit risk management in unsecured lending, regulatory oversight of lending practices, and intense competition affecting margins from both traditional and fintech lenders.

Enova's competitors include traditional storefront lenders like Ace Cash Express, Check Into Cash, and One Main Financial in the consumer lending space. In the small business financing market, Enova competes with traditional banks, financial technology companies like Square Capital (Block, Inc.), PayPal Working Capital (PayPal Holdings, Inc.), and Kabbage (American Express).

5. Revenue Growth

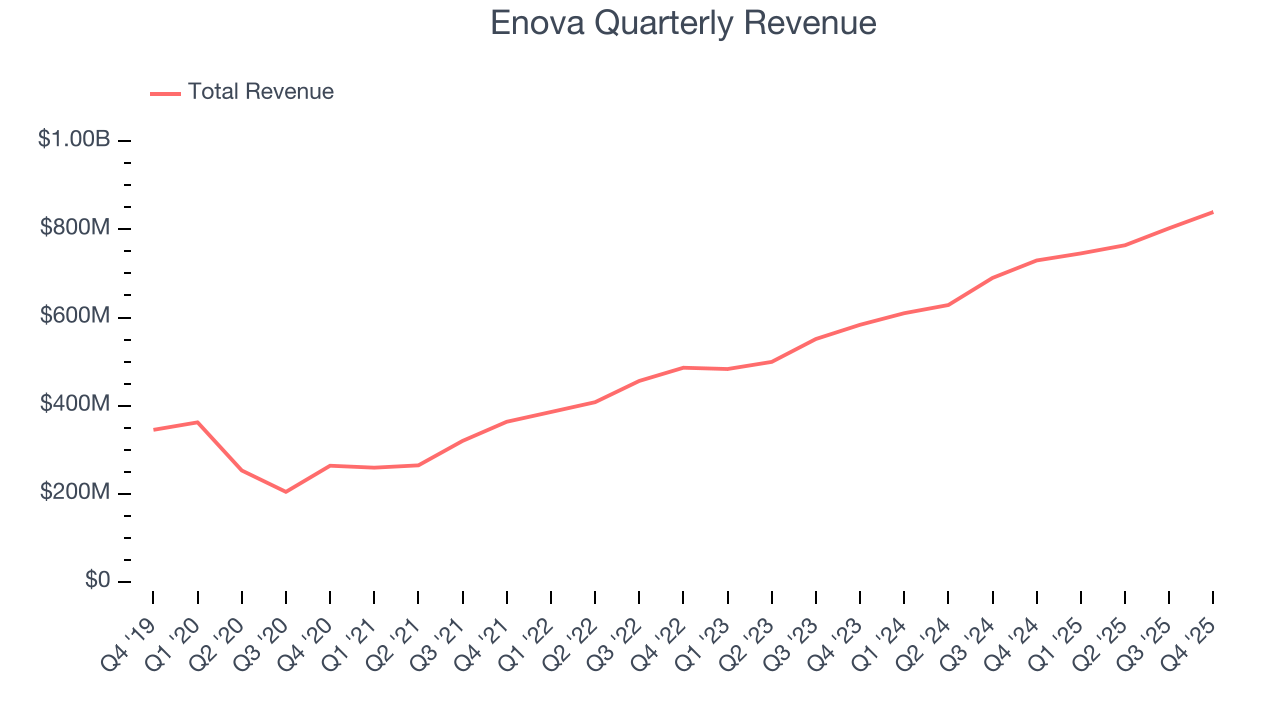

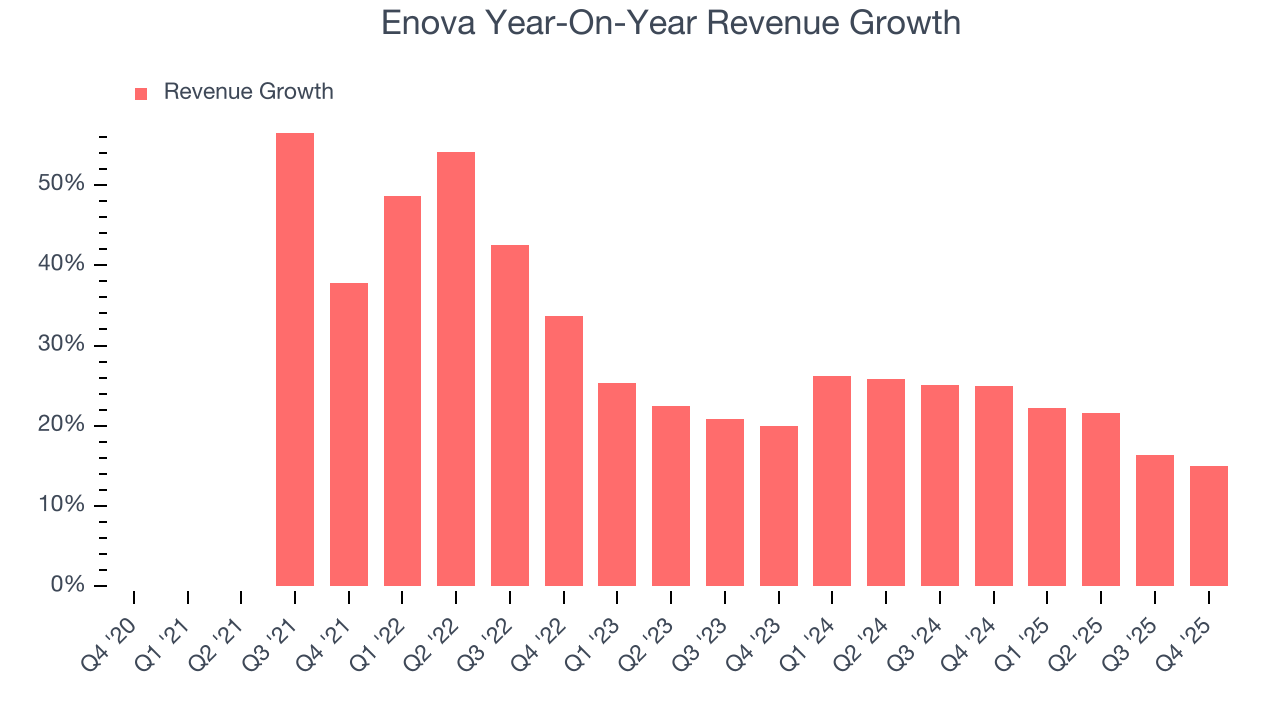

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Thankfully, Enova’s 23.8% annualized revenue growth over the last five years was exceptional. Its growth beat the average financials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Enova’s annualized revenue growth of 22% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Enova’s year-on-year revenue growth was 15.1%, and its $839.4 million of revenue was in line with Wall Street’s estimates.

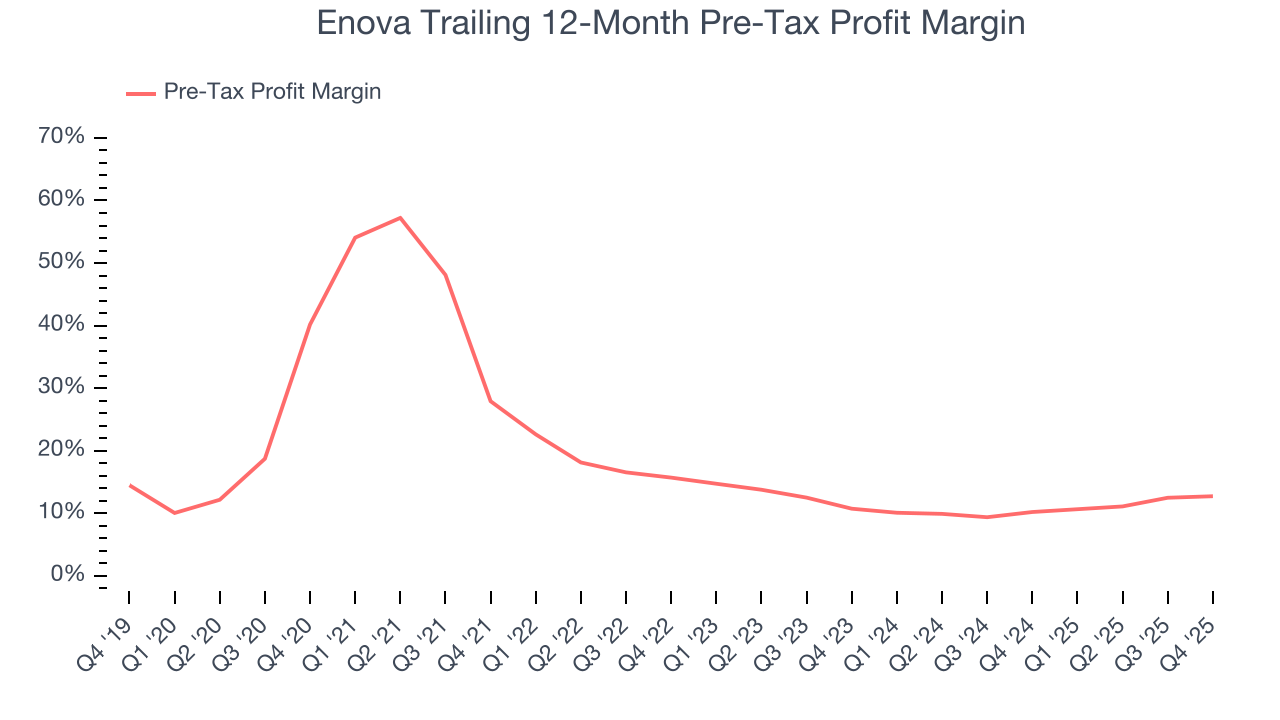

6. Pre-Tax Profit Margin

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For Personal Loan companies, we look at pre-tax profit rather than the operating margin that defines sectors such as consumer, tech, and industrials.

Financials companies manage interest-bearing assets and liabilities, making the interest income and expenses included in pre-tax profit essential to their profit calculation. Taxes, being external factors beyond management control, are appropriately excluded from this alternative margin measure.

Over the last five years, Enova’s pre-tax profit margin has risen by 27.5 percentage points, going from 27.9% to 12.7%. Luckily, it seems the company has recently taken steps to address its expense base as its pre-tax profit margin expanded by 2 percentage points on a two-year basis.

Enova’s pre-tax profit margin came in at 11.8% this quarter. This result was 1.2 percentage points better than the same quarter last year.

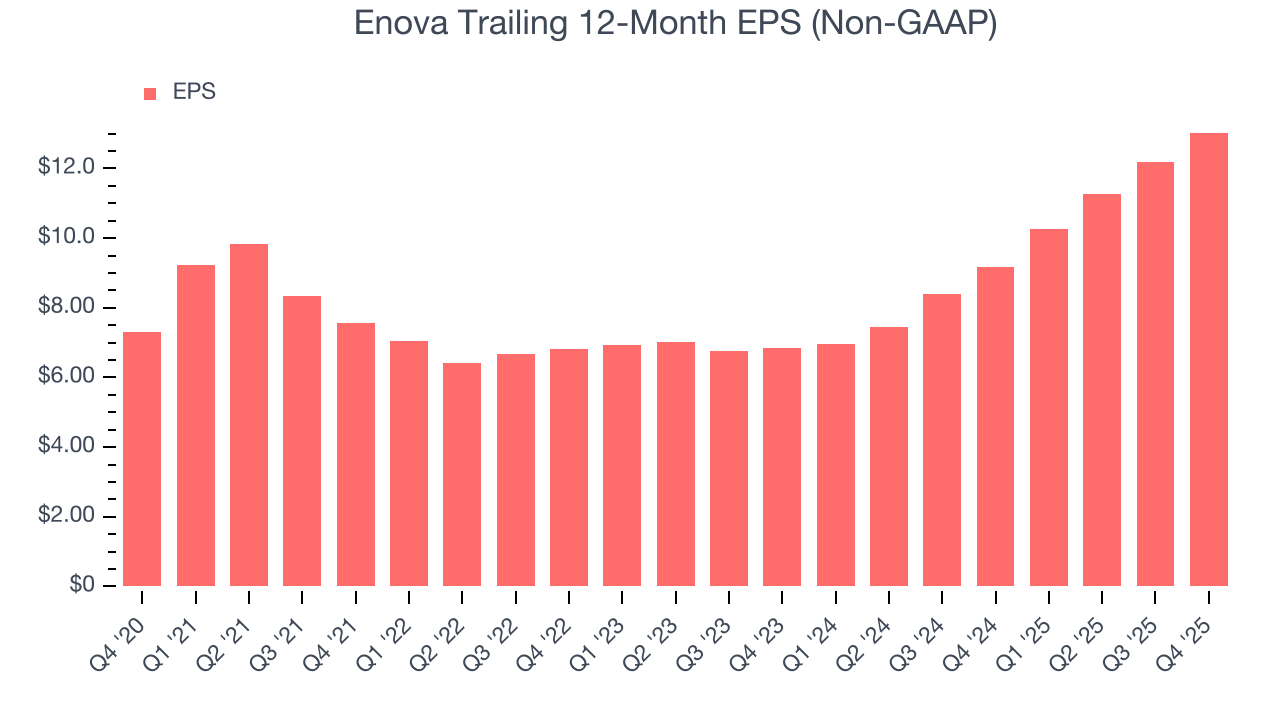

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Enova’s EPS grew at a decent 12.3% compounded annual growth rate over the last five years. However, this performance was lower than its 23.8% annualized revenue growth, telling us the company became less profitable on a per-share basis as it expanded due to factors such as interest expenses and taxes.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Enova, its two-year annual EPS growth of 38% was higher than its five-year trend. This acceleration made it one of the faster-growing financials companies in recent history.

In Q4, Enova reported adjusted EPS of $3.46, up from $2.61 in the same quarter last year. This print beat analysts’ estimates by 9.1%. Over the next 12 months, Wall Street expects Enova’s full-year EPS of $13.03 to grow 19.7%.

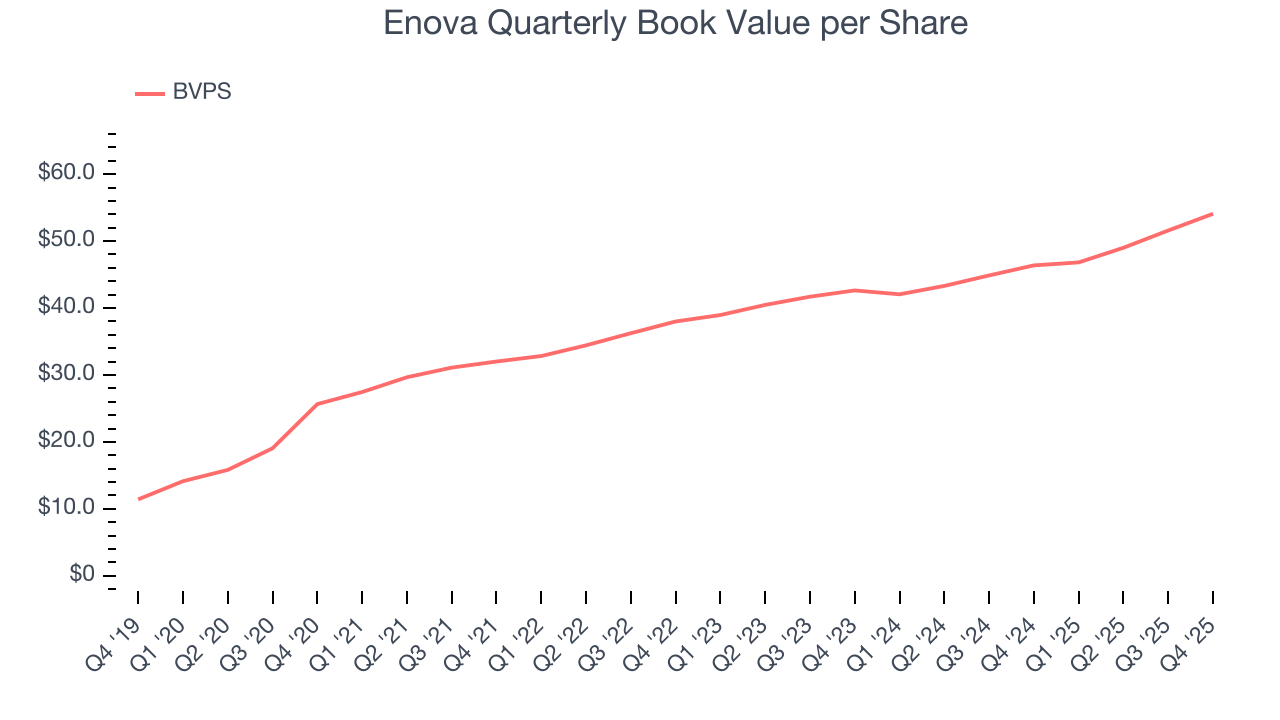

8. Book Value Per Share (BVPS)

Financial institutions with multiple business lines manage complex balance sheets that span various financial activities. Market valuations reflect this operational complexity, prioritizing balance sheet strength and sustainable book value growth across all business segments.

This is why we consider book value per share (BVPS) an important metric for the sector. BVPS represents the real net worth per share across all business segments, providing a clear measure of shareholder equity regardless of the complexity of operations. On the other hand, EPS is often distorted by the diverse nature of operations, mergers, and various accounting treatments across different business units. Book value provides clearer performance insights.

Enova’s BVPS grew at an excellent 16.1% annual clip over the last five years. BVPS growth has recently decelerated to 12.6% annual growth over the last two years (from $42.63 to $54.08 per share).

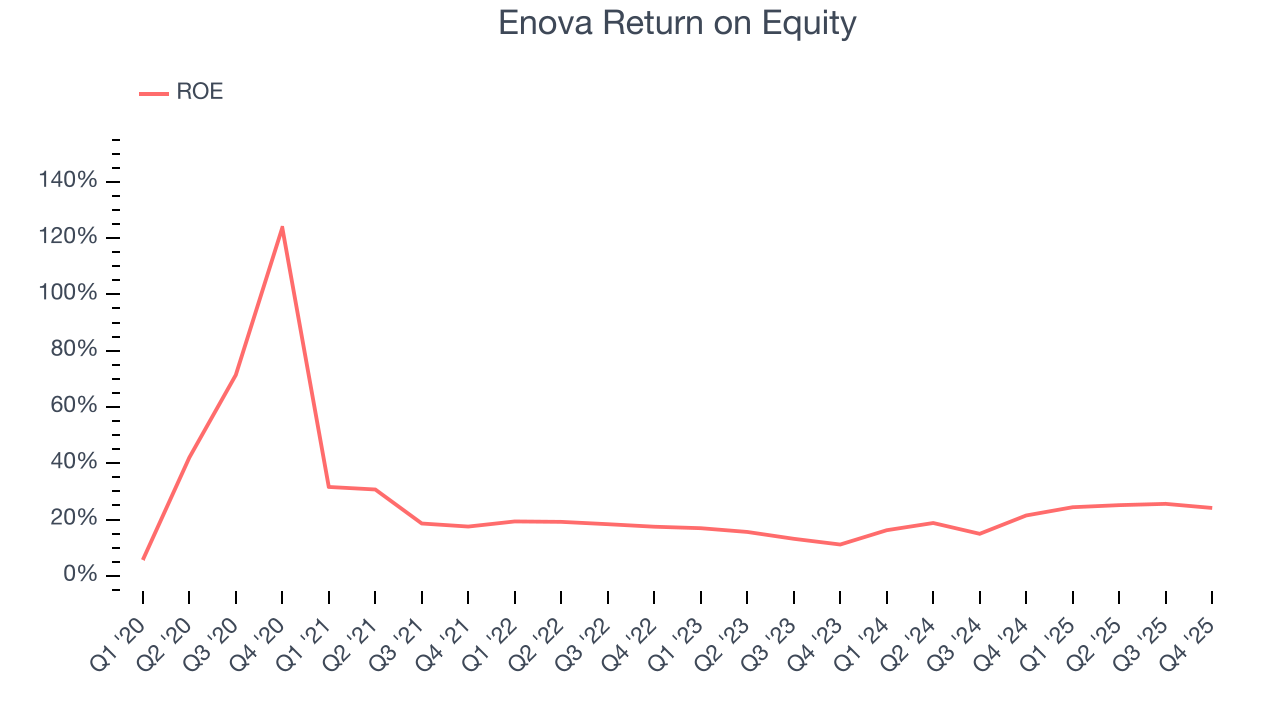

9. Return on Equity

Return on equity (ROE) measures how effectively banks generate profit from each dollar of shareholder equity - a critical funding source. High-ROE institutions typically compound shareholder wealth faster over time through retained earnings, share repurchases, and dividend payments.

Over the last five years, Enova has averaged an ROE of 20%, excellent for a company operating in a sector where the average shakes out around 10% and those putting up 25%+ are greatly admired. This is a bright spot for Enova.

10. Balance Sheet Risk

Enova reported $407.9 million of cash and $4.53 billion of debt on its balance sheet in the most recent quarter.

As investors in high-quality companies, we primarily focus on whether a company’s profits can support its debt.

With $820.9 million of EBITDA over the last 12 months, we view Enova’s 5.0× net-debt-to-EBITDA ratio as inadequate. The company’s lacking profits relative to its borrowings give it little breathing room, raising red flags.

11. Key Takeaways from Enova’s Q4 Results

It was good to see Enova beat analysts’ EPS expectations this quarter. We were also happy its EBITDA narrowly outperformed Wall Street’s estimates. Overall, this print had some key positives. The stock remained flat at $165.17 immediately following the results.

12. Is Now The Time To Buy Enova?

When considering an investment in Enova, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

Aside from its balance sheet, Enova is a pretty good company. First of all, the company’s revenue growth was exceptional over the last five years. And while its declining pre-tax profit margin shows the business has become less efficient, its BVPS growth was impressive over the last five years. On top of that, Enova’s market-beating ROE suggests it has been a well-managed company historically.

Enova’s P/E ratio based on the next 12 months is 10.6x. Despite its notable business characteristics, we’d hold off for now because its balance sheet concerns us. We think a potential buyer of the stock should wait until the company generates sufficient cash flows or raises money.

Wall Street analysts have a consensus one-year price target of $193.71 on the company (compared to the current share price of $165.17).