First American Financial (FAF)

First American Financial doesn’t excite us. Its sales have underperformed and its low returns on capital show it has few growth opportunities.― StockStory Analyst Team

1. News

2. Summary

Why We Think First American Financial Will Underperform

Tracing its roots back to 1889 when California was experiencing its first major real estate boom, First American Financial (NYSE:FAF) provides title insurance, settlement services, and risk solutions for residential and commercial real estate transactions across the United States and internationally.

- Net premiums earned remained stagnant over the last five years, indicating expansion challenges this cycle

- Muted 1% annual revenue growth over the last five years shows its demand lagged behind its insurance peers

- A silver lining is that its forecasted revenue growth of 7.3% for the next 12 months indicates its momentum over the last two years is sustainable

First American Financial doesn’t meet our quality standards. There are more promising prospects in the market.

Why There Are Better Opportunities Than First American Financial

At $58.66 per share, First American Financial trades at 1x forward P/B. This multiple is cheaper than most insurance peers, but we think this is justified.

Cheap stocks can look like great bargains at first glance, but you often get what you pay for. These mediocre businesses often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. First American Financial (FAF) Research Report: Q4 CY2025 Update

Title insurance provider First American Financial (NYSE:FAF) reported Q4 CY2025 results topping the market’s revenue expectations, with sales up 21.6% year on year to $2.05 billion. Its non-GAAP profit of $1.99 per share was 38.8% above analysts’ consensus estimates.

First American Financial (FAF) Q4 CY2025 Highlights:

- Revenue: $2.05 billion vs analyst estimates of $1.78 billion (21.6% year-on-year growth, 15.2% beat)

- Pre-tax Profit: $287.4 million (14% margin)

- Adjusted EPS: $1.99 vs analyst estimates of $1.43 (38.8% beat)

- Market Capitalization: $6.78 billion

Company Overview

Tracing its roots back to 1889 when California was experiencing its first major real estate boom, First American Financial (NYSE:FAF) provides title insurance, settlement services, and risk solutions for residential and commercial real estate transactions across the United States and internationally.

The company operates through two main segments: Title Insurance and Services, which generates over 95% of its revenue, and Home Warranty. In its core business, First American examines public records to verify property ownership and identify potential issues like liens or encumbrances that could affect a real estate transaction. This research culminates in title insurance policies that protect buyers and lenders against financial losses from defects in a title that weren't discovered during the initial search.

First American distributes its services through both direct operations and a network of authorized agents across 49 states and several international markets including Canada, the United Kingdom, Australia, and South Korea. The company maintains extensive proprietary title plants—databases of property records organized geographically rather than by owner name—which allows for more efficient searching than public records.

For example, when a family purchases a home, First American might discover a previously undisclosed lien against the property during its title search. By identifying this issue before closing, the company helps resolve the problem, ensuring the buyers receive clear ownership. Beyond basic title insurance, First American offers closing and escrow services, property valuation, document generation, and banking services through its federal savings bank subsidiary.

The company's Home Warranty segment provides residential service contracts covering home systems and appliances against normal wear and tear, giving homeowners protection against unexpected repair costs for items like heating systems, air conditioners, and major appliances.

4. Property & Casualty Insurance

Property & Casualty (P&C) insurers protect individuals and businesses against financial loss from damage to property or from legal liability. This is a cyclical industry, and the sector benefits when there is 'hard market', characterized by strong premium rate increases that outpace loss and cost inflation, resulting in robust underwriting margins. The opposite is true in a 'soft market'. Interest rates also matter, as they determine the yields earned on fixed-income portfolios. On the other hand, P&C insurers face a major secular headwind from the increasing frequency and severity of catastrophe losses due to climate change. Furthermore, the liability side of the business is pressured by 'social inflation'—the trend of rising litigation costs and larger jury awards.

First American Financial's primary competitors in the title insurance industry include Fidelity National Financial (NYSE:FNF), Old Republic International (NYSE:ORI), and Stewart Information Services (NYSE:STC). In the home warranty segment, it competes with American Home Shield (NYSE:AHS) and Frontdoor (NASDAQ:FTDR).

5. Revenue Growth

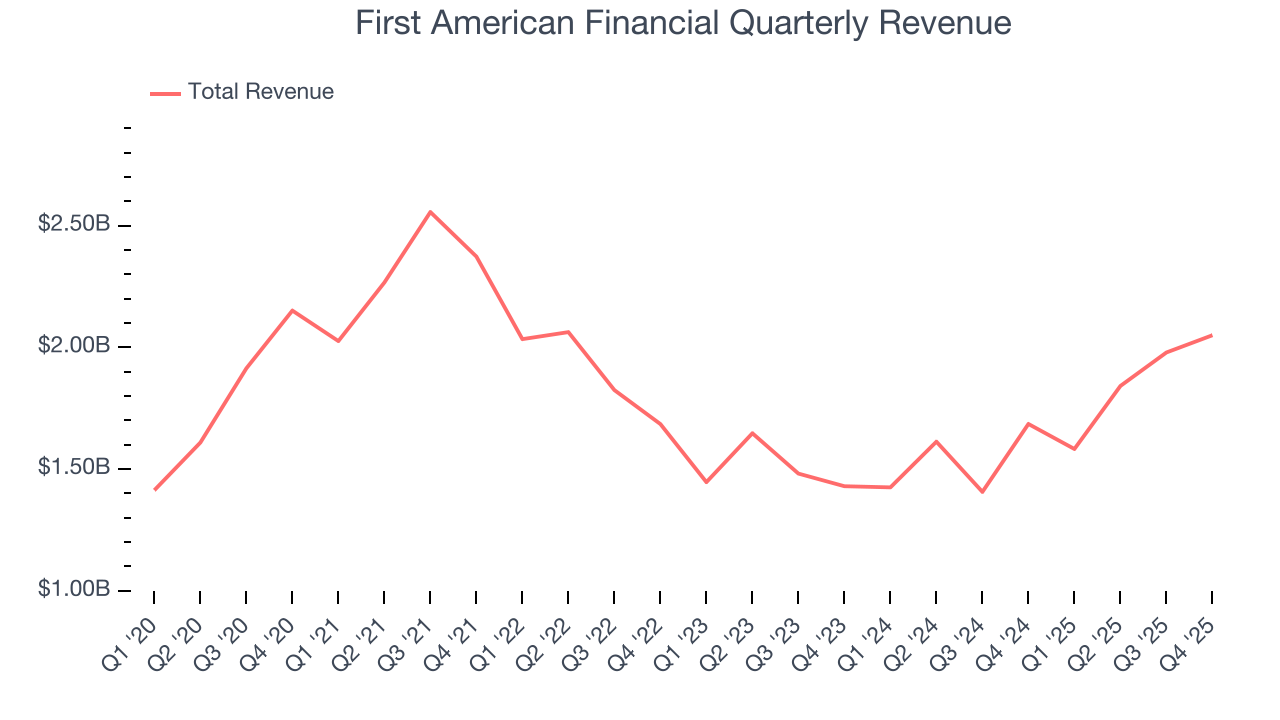

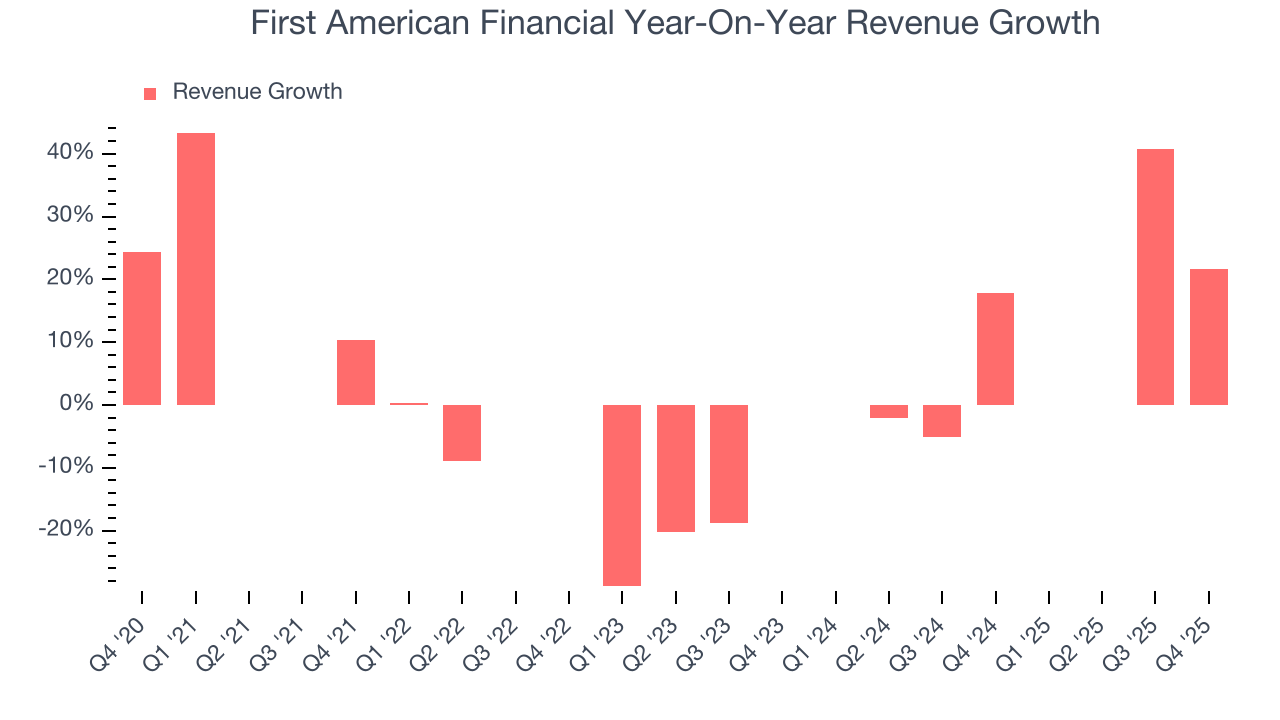

Insurance companies earn revenue from three primary sources: 1) The core insurance business itself, often called underwriting and represented in the income statement as premiums 2) Income from investing the “float” (premiums collected upfront not yet paid out as claims) in assets such as fixed-income assets and equities 3) Fees from various sources such as policy administration, annuities, or other value-added services. Unfortunately, First American Financial’s 1% annualized revenue growth over the last five years was weak. This fell short of our benchmarks and is a poor baseline for our analysis.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. First American Financial’s annualized revenue growth of 11.4% over the last two years is above its five-year trend, suggesting its demand recently accelerated.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, First American Financial reported robust year-on-year revenue growth of 21.6%, and its $2.05 billion of revenue topped Wall Street estimates by 15.2%.

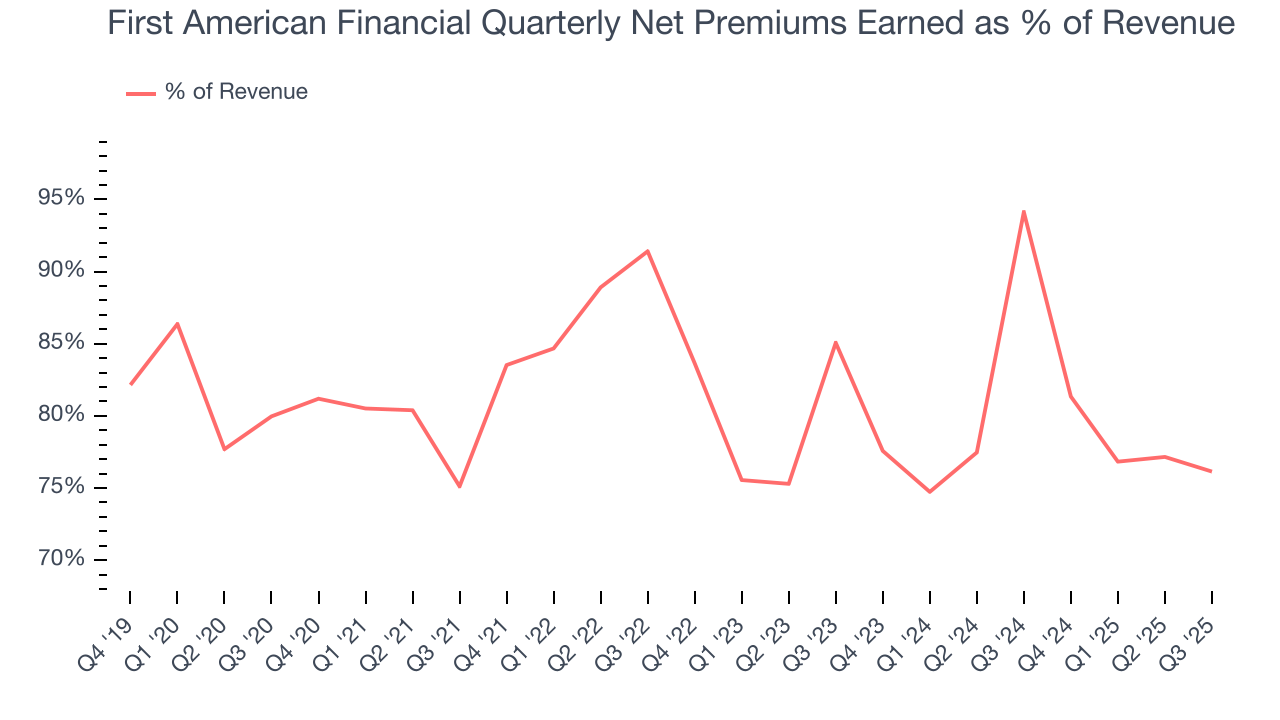

Net premiums earned made up 81% of the company’s total revenue during the last five years, meaning First American Financial barely relies on non-insurance activities to drive its overall growth.

Net premiums earned commands greater market attention due to its reliability and consistency, whereas investment and fee income are often seen as more volatile revenue streams that fluctuate with market conditions.

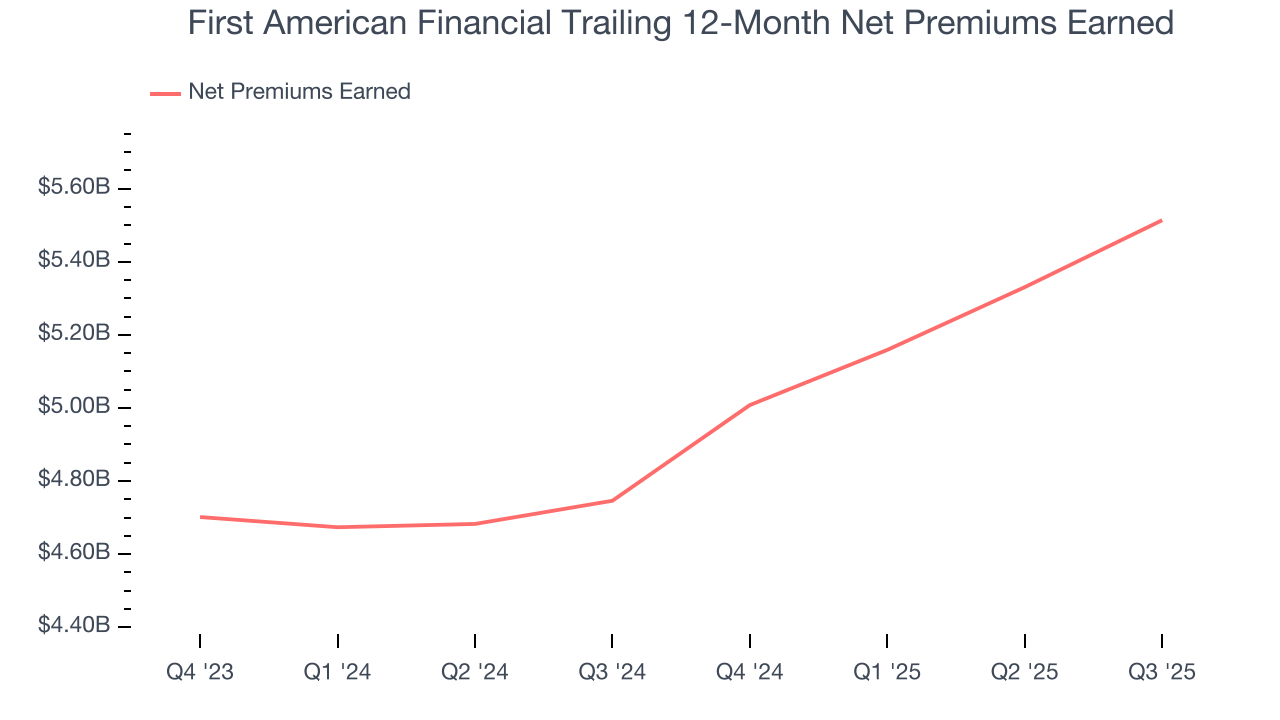

6. Net Premiums Earned

Net premiums earned are net of what’s paid to reinsurers (insurance for insurance companies), which are used by insurers to protect themselves from large losses.

First American Financial’s net premiums earned was flat over the last five years, much worse than the broader insurance industry and in line with its total revenue.

When analyzing First American Financial’s net premiums earned over the last two years, we can see that growth accelerated to 7.4% annually. Since two-year net premiums earned grew slower than total revenue over this period, it’s implied that other line items such as investment income grew at a faster rate. These extra revenue streams are important to the bottom line, yet their performance can be inconsistent. Some firms have been more successful and consistent in managing their float, but sharp fluctuations in the fixed income and equity markets can dramatically affect short-term results.

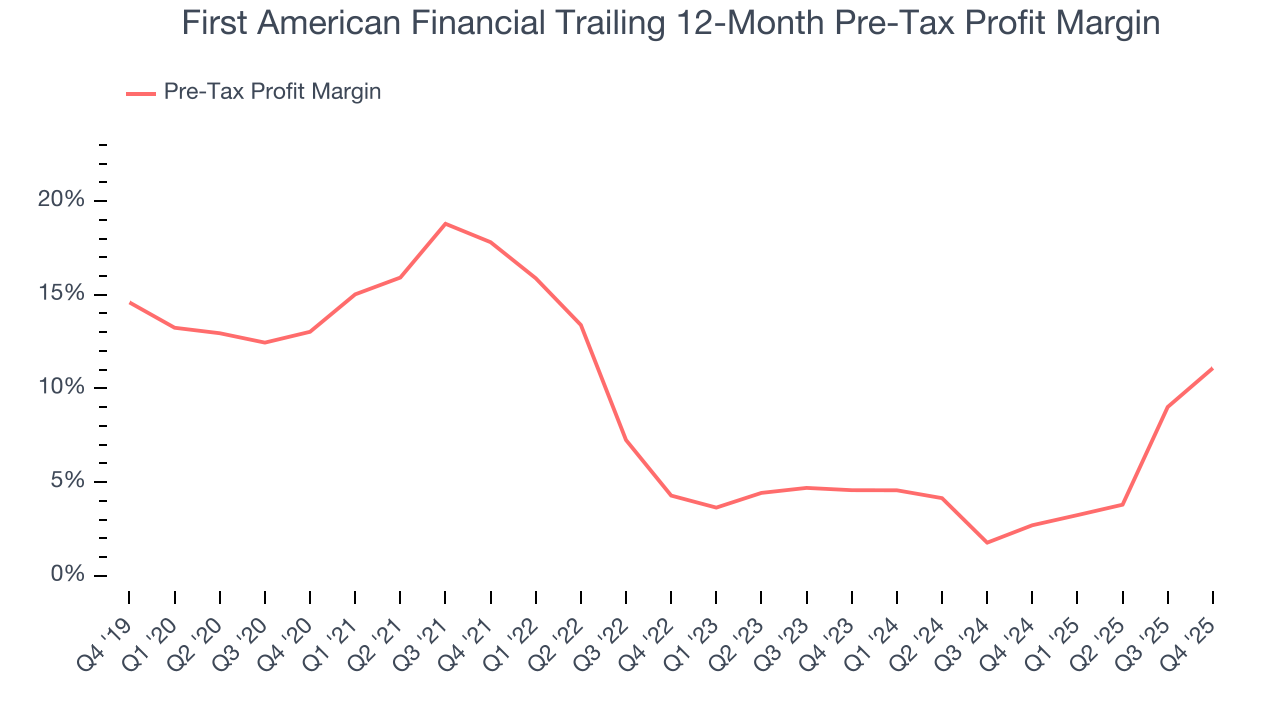

7. Pre-Tax Profit Margin

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For insurance companies, we look at pre-tax profit rather than the operating margin that defines sectors such as consumer, tech, and industrials.

Insurance companies are balance sheet businesses, where assets and liabilities define the economics. Interest income and expense should therefore be factored into the definition of profit but taxes - which are largely out of a company’s control - should not. This is pre-tax profit by definition.

Over the last five years, First American Financial’s pre-tax profit margin has risen by 1.9 percentage points, going from 17.8% to 11.1%. Luckily, it seems the company has recently taken steps to address its expense base as its pre-tax profit margin expanded by 6.5 percentage points on a two-year basis.

In Q4, First American Financial’s pre-tax profit margin was 14%. This result was 8.1 percentage points better than the same quarter last year.

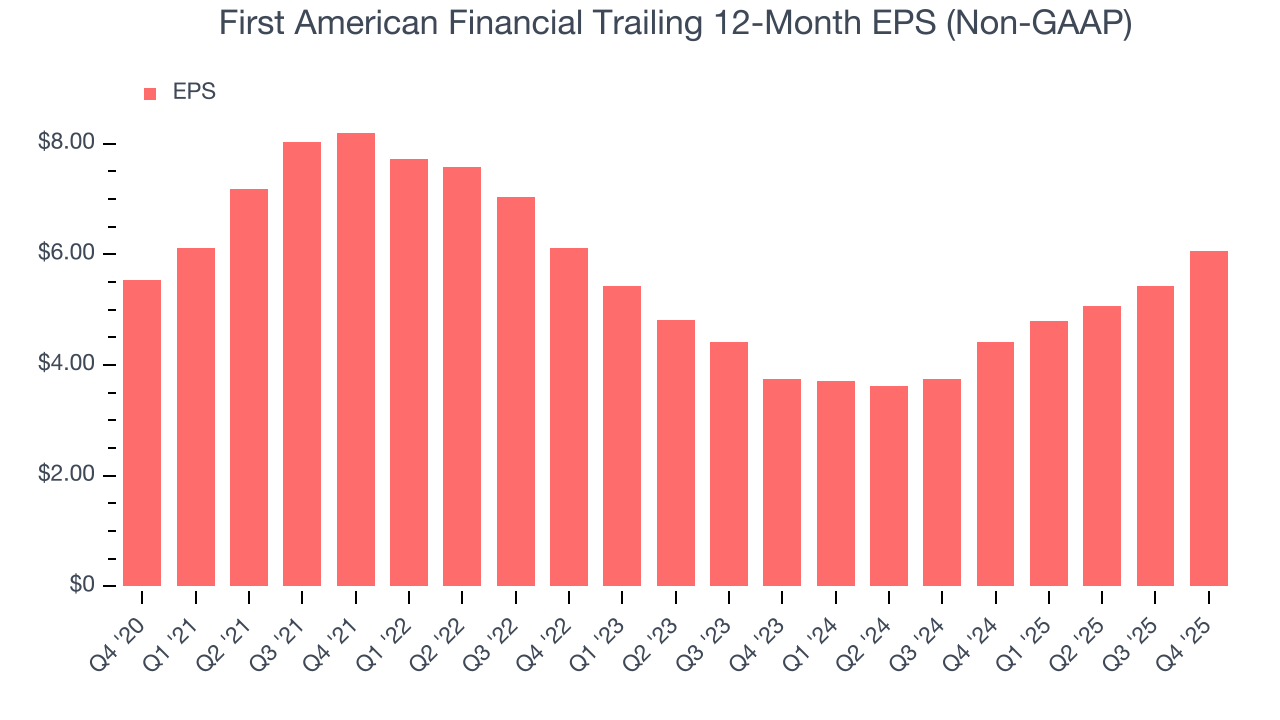

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

First American Financial’s weak 1.8% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

First American Financial’s two-year annual EPS growth of 27.1% was great and topped its 11.4% two-year revenue growth.

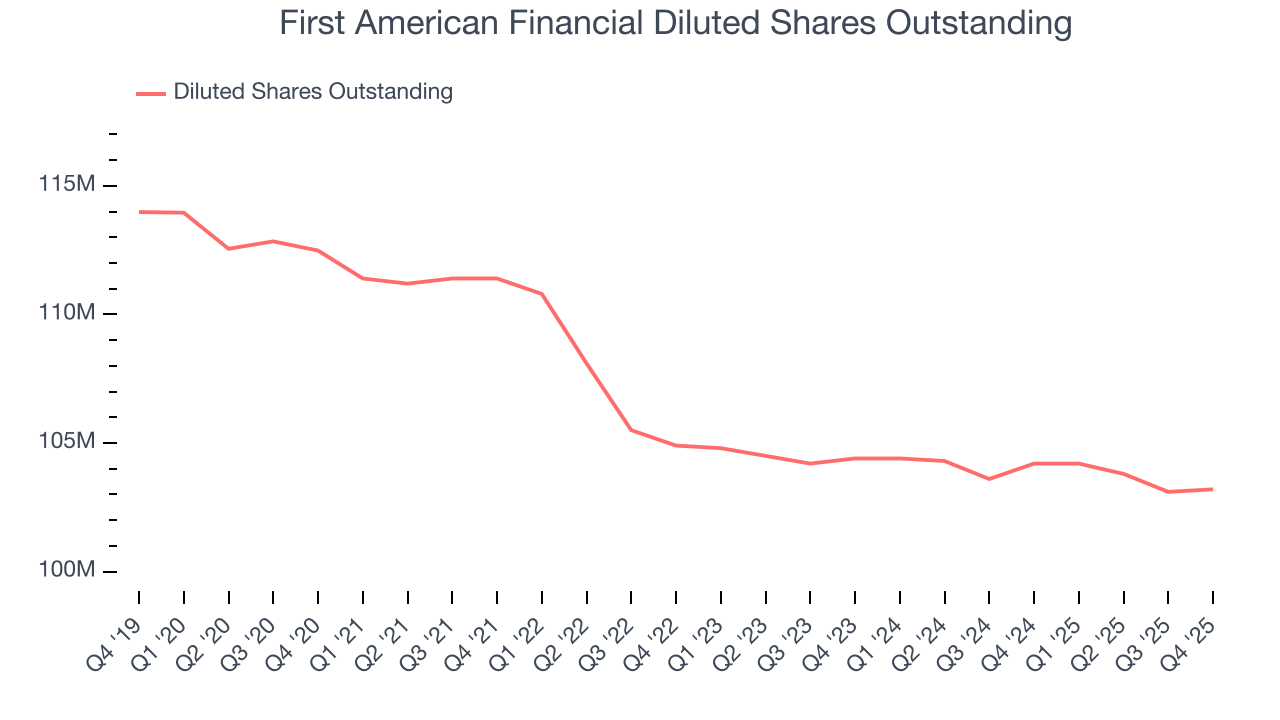

Diving into the nuances of First American Financial’s earnings can give us a better understanding of its performance. First American Financial’s pre-tax profit margin has expanded over the last two yearswhile its share count has shrunk 1.1%. Improving profitability and share buybacks are positive signs for shareholders as they juice EPS growth relative to revenue growth.

In Q4, First American Financial reported adjusted EPS of $1.99, up from $1.35 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects First American Financial’s full-year EPS of $6.06 to stay about the same.

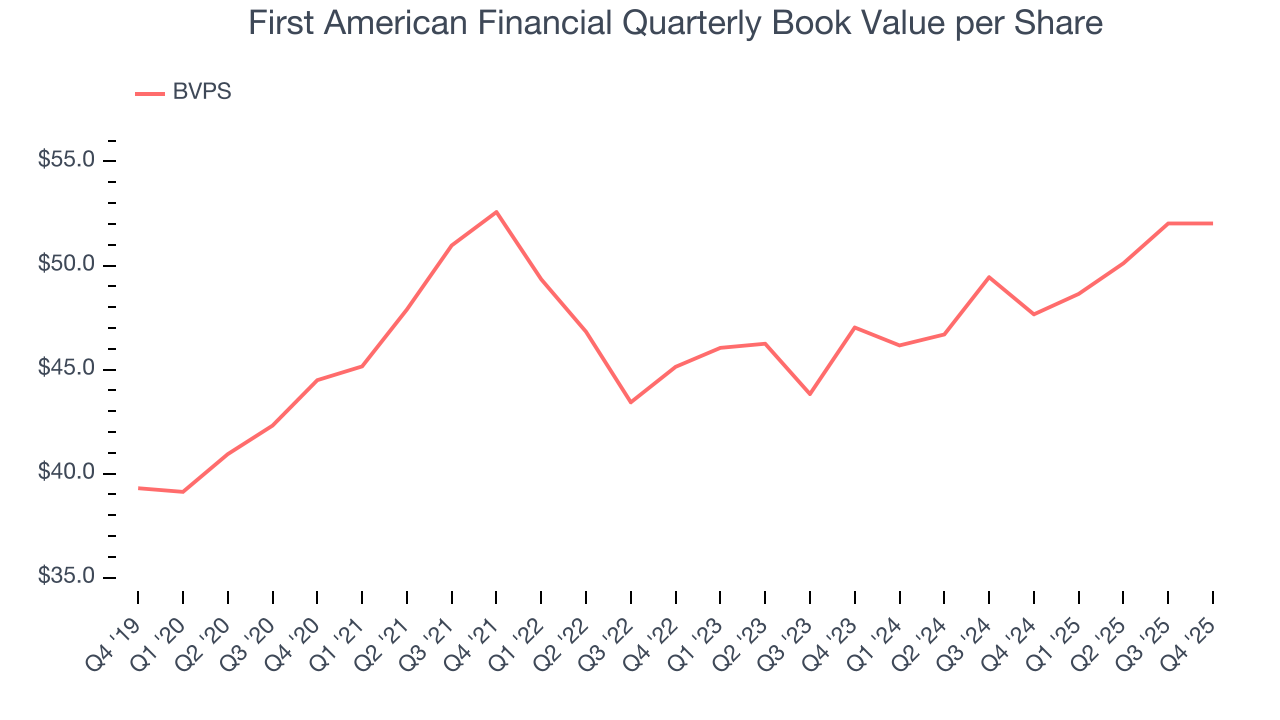

9. Book Value Per Share (BVPS)

Insurance companies are balance sheet businesses, collecting premiums upfront and paying out claims over time. The float – premiums collected but not yet paid out – are invested, creating an asset base supported by a liability structure. Book value captures this dynamic by measuring:

- Assets (investment portfolio, cash, reinsurance recoverables) - liabilities (claim reserves, debt, future policy benefits)

BVPS is essentially the residual value for shareholders.

We therefore consider BVPS very important to track for insurers and a metric that sheds light on business quality. While other (and more commonly known) per-share metrics like EPS can sometimes be lumpy due to reserve releases or one-time items and can be managed or skewed while still following accounting rules, BVPS reflects long-term capital growth and is harder to manipulate.

First American Financial’s BVPS grew at a sluggish 3.2% annual clip over the last five years. However, BVPS growth has accelerated recently, growing by 5.2% annually over the last two years from $47.02 to $52.02 per share.

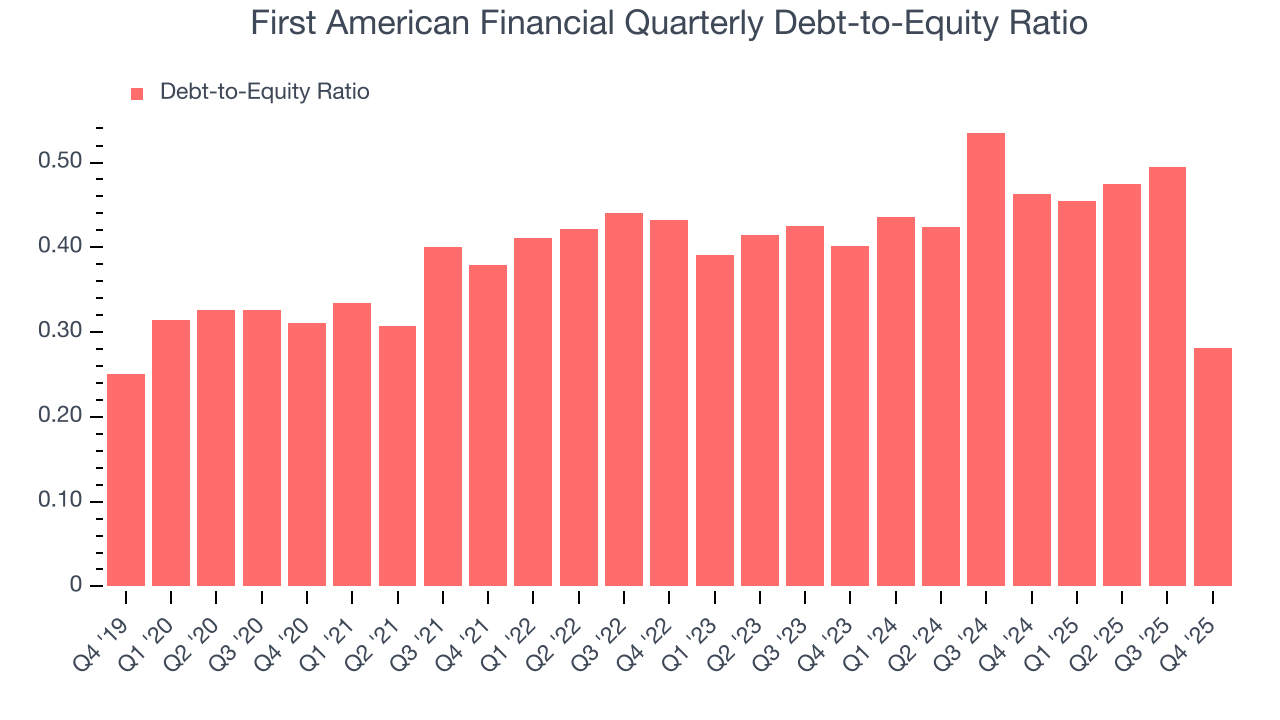

10. Balance Sheet Assessment

The debt-to-equity ratio is a widely used measure to assess a company's balance sheet health. A higher ratio means that a business aggressively financed its growth with debt. This can result in higher earnings (if the borrowed funds are invested profitably) but also increases risk.

If debt levels are too high, there could be difficulties in meeting obligations, especially during economic downturns or periods of rising interest rates if the debt has variable-rate payments.

First American Financial currently has $1.55 billion of debt and $5.5 billion of shareholder's equity on its balance sheet, and over the past four quarters, has averaged a debt-to-equity ratio of 0.4×. We think this is safe and raises no red flags. In general, we’re comfortable with any ratio below 1.0× for an insurance business. Anything below 0.5× is a bonus.

11. Return on Equity

Return on equity (ROE) is a crucial yardstick for insurance companies, measuring their ability to generate returns on the capital provided by shareholders. Insurers that consistently deliver superior ROE tend to create more value for their investors over time through strategic capital allocation and shareholder-friendly policies.

Over the last five years, First American Financial has averaged an ROE of 9.3%, uninspiring for a company operating in a sector where the average shakes out around 12.5%.

12. Key Takeaways from First American Financial’s Q4 Results

It was good to see First American Financial beat analysts’ EPS expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 2.3% to $65.80 immediately following the results.

13. Is Now The Time To Buy First American Financial?

Updated: March 30, 2026 at 12:56 AM EDT

Before deciding whether to buy First American Financial or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

First American Financial’s business quality ultimately falls short of our standards. For starters, its revenue growth was weak over the last five years. On top of that, First American Financial’s net premiums earned growth was weak over the last five years, and its weak EPS growth over the last five years shows it’s failed to produce meaningful profits for shareholders.

First American Financial’s P/B ratio based on the next 12 months is 1x. This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're pretty confident there are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $81.60 on the company (compared to the current share price of $58.66).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.