Herbalife (HLF)

We’re not sold on Herbalife. Not only is its demand weak but also its falling returns on capital suggest it’s becoming less profitable.― StockStory Analyst Team

1. News

2. Summary

Why Herbalife Is Not Exciting

With the first products sold out of the trunk of the founder’s car, Herbalife (NYSE:HLF) today offers a portfolio of shakes, supplements, personal care products, and weight management programs to help customers reach their nutritional and fitness goals.

- Products have few die-hard fans as sales have declined by 1.1% annually over the last three years

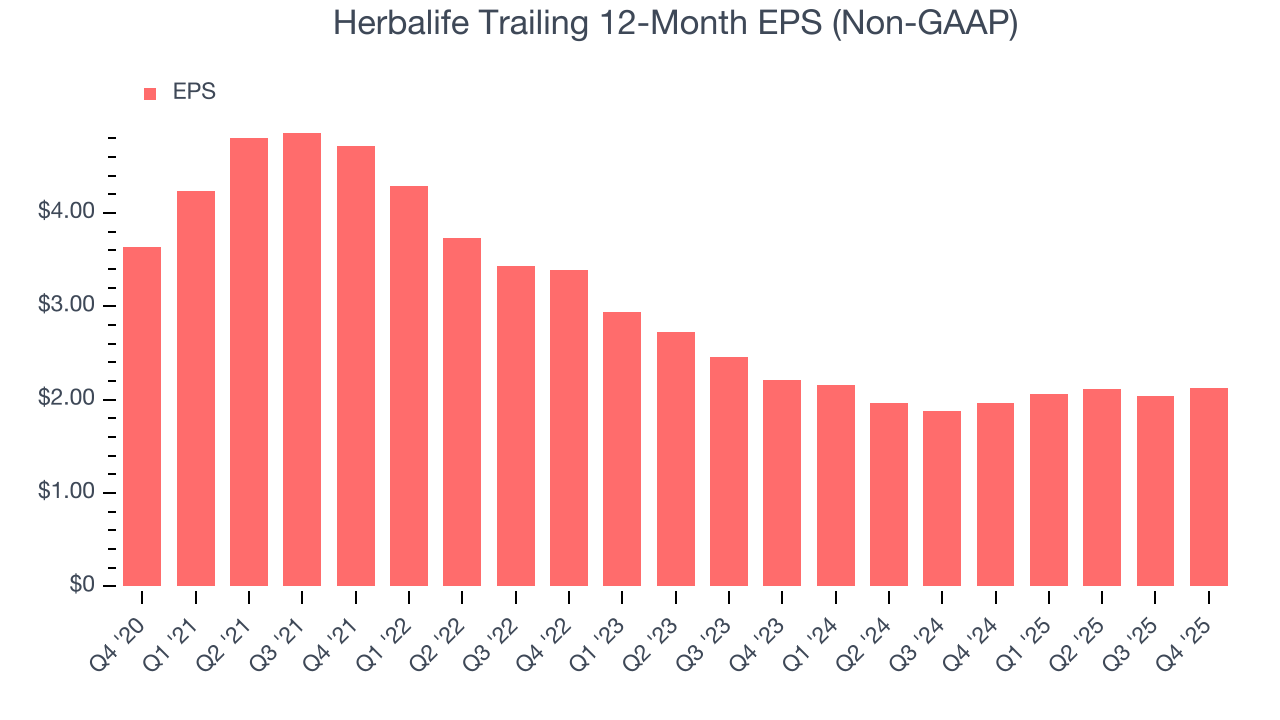

- Earnings per share have contracted by 14.4% annually over the last three years, a headwind for returns as stock prices often echo long-term EPS performance

- On the bright side, its products command premium prices and result in a best-in-class gross margin of 77.9%

Herbalife doesn’t fulfill our quality requirements. We’d search for superior opportunities elsewhere.

Why There Are Better Opportunities Than Herbalife

Herbalife’s stock price of $15.27 implies a valuation ratio of 5.9x forward P/E. This sure is a cheap multiple, but you get what you pay for.

It’s better to pay up for high-quality businesses with higher long-term earnings potential rather than to buy lower-quality stocks because they appear cheap. These challenged businesses often don’t re-rate, a phenomenon known as a “value trap”.

3. Herbalife (HLF) Research Report: Q4 CY2025 Update

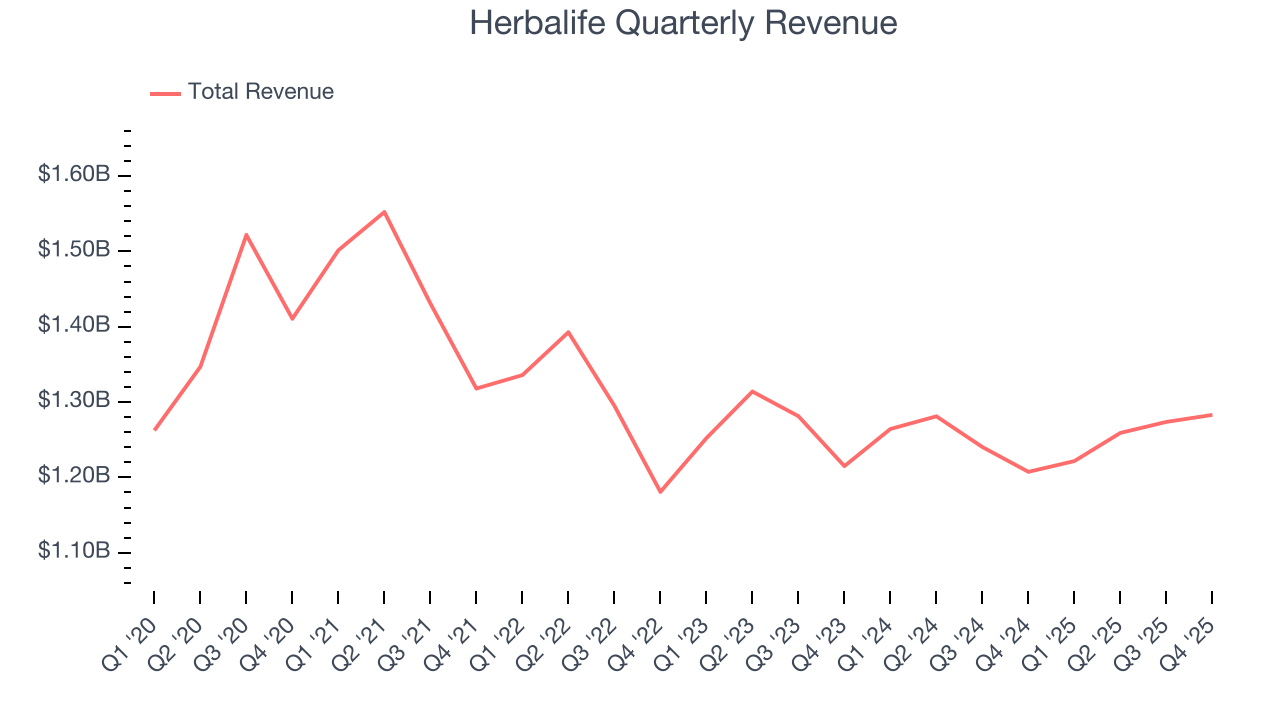

Health and wellness products company Herbalife (NYSE:HLF) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 6.3% year on year to $1.28 billion. Guidance for next quarter’s revenue was better than expected at $1.28 billion at the midpoint, 1.4% above analysts’ estimates. Its non-GAAP profit of $0.45 per share was 5.6% below analysts’ consensus estimates.

Correction note:

The previous version of this report incorrectly estimated adjusted EBITDA at $173.4 million. This version has been updated to reflect the correct figure of $156.1 million.

Herbalife (HLF) Q4 CY2025 Highlights:

- Revenue: $1.28 billion vs analyst estimates of $1.24 billion (6.3% year-on-year growth, 3.6% beat)

- Adjusted EPS: $0.45 vs analyst expectations of $0.48 (5.6% miss)

- Adjusted EBITDA: $156.1 million vs analyst estimates of $150.2 million

- Revenue Guidance for Q1 CY2026 is $1.28 billion at the midpoint, above analyst estimates of $1.26 billion

- EBITDA guidance for the upcoming financial year 2026 is $690 million at the midpoint, above analyst estimates of $680.9 million

- Operating Margin: 7.8%, down from 8.8% in the same quarter last year

- Free Cash Flow Margin: 6.2%, up from 3.6% in the same quarter last year

- Market Capitalization: $1.65 billion

Company Overview

With the first products sold out of the trunk of the founder’s car, Herbalife (NYSE:HLF) today offers a portfolio of shakes, supplements, personal care products, and weight management programs to help customers reach their nutritional and fitness goals.

Specifically, the company was founded in 1980 by Mark Hughes, and the first Herbalife product was a protein shake mix called the "Formula 1 Nutritional Shake Mix”. It was designed to serve as a meal replacement for individuals looking to manage their weight.

Today, Herbalife still offers meal replacement shakes but also sells multivitamins, protein supplements, aloe drinks for gut health, and collagen drink mixes for skin and hair health, among others. The company continues to expand its product portfolio organically with health, wellness, and fitness as the unifying theme.

The company’s go-to-market is unique in that it is a multi-level marketing model. In essence, the products are sold through its network of customers who sign up to sell the product. They often operate from their homes, through dedicated Herbalife nutrition clubs, or via online channels.

This multi-level marketing approach has resulted in controversy, with some claiming the business is nothing more than a pyramid scheme. Pyramid schemes are illegal businesses where returns for older customers or investors are paid using the capital of newer customers and investors, rather than from profit earned. The structure relies heavily on recruitment to sustain itself, rather than actual demand for products.

4. Personal Care

While personal care products products may seem more discretionary than food, consumers tend to maintain or even boost their spending on the category during tough times. This phenomenon is known as "the lipstick effect" by economists, which states that consumers still want some semblance of affordable luxuries like beauty and wellness when the economy is sputtering. Consumer tastes are constantly changing, and personal care companies are currently responding to the public’s increased desire for ethically produced goods by featuring natural ingredients in their products.

Competitors offering health and wellness supplements and products include Usana Health Sciences (NYSE:USNA), Bellring Brands (NYSE:BRBR), and The Simply Good Foods Company (NASDAQ:SMPL).

5. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years.

With $5.04 billion in revenue over the past 12 months, Herbalife carries some recognizable products but is a mid-sized consumer staples company. Its size could bring disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale.

As you can see below, Herbalife’s demand was weak over the last three years. Its sales fell by 1.1% annually as consumers bought less of its products.

This quarter, Herbalife reported year-on-year revenue growth of 6.3%, and its $1.28 billion of revenue exceeded Wall Street’s estimates by 3.6%. Company management is currently guiding for a 5% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 2% over the next 12 months. Although this projection suggests its newer products will fuel better top-line performance, it is still below the sector average.

6. Gross Margin & Pricing Power

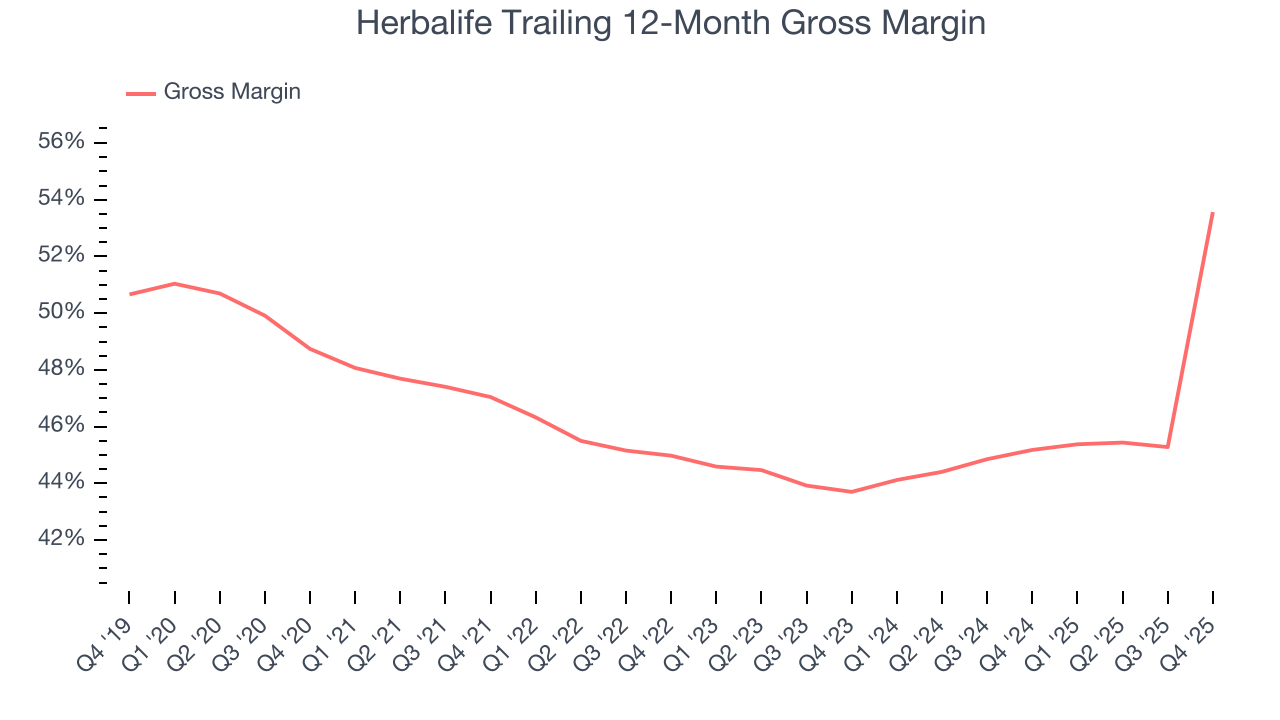

All else equal, we prefer higher gross margins because they make it easier to generate more operating profits and indicate that a company commands pricing power by offering more differentiated products.

Herbalife has great unit economics for a consumer staples company, giving it ample room to invest in areas such as marketing and talent to grow its brand. As you can see below, it averaged an excellent 49.4% gross margin over the last two years. That means Herbalife only paid its suppliers $50.61 for every $100 in revenue.

Herbalife produced a 77.5% gross profit margin in Q4 , marking a 32.6 percentage point increase from 45% in the same quarter last year. Herbalife’s full-year margin has also been trending up over the past 12 months, increasing by 8.4 percentage points. If this move continues, it could suggest a less competitive environment where the company has better pricing power and leverage from its growing sales on the fixed portion of its cost of goods sold (such as manufacturing expenses).

7. Operating Margin

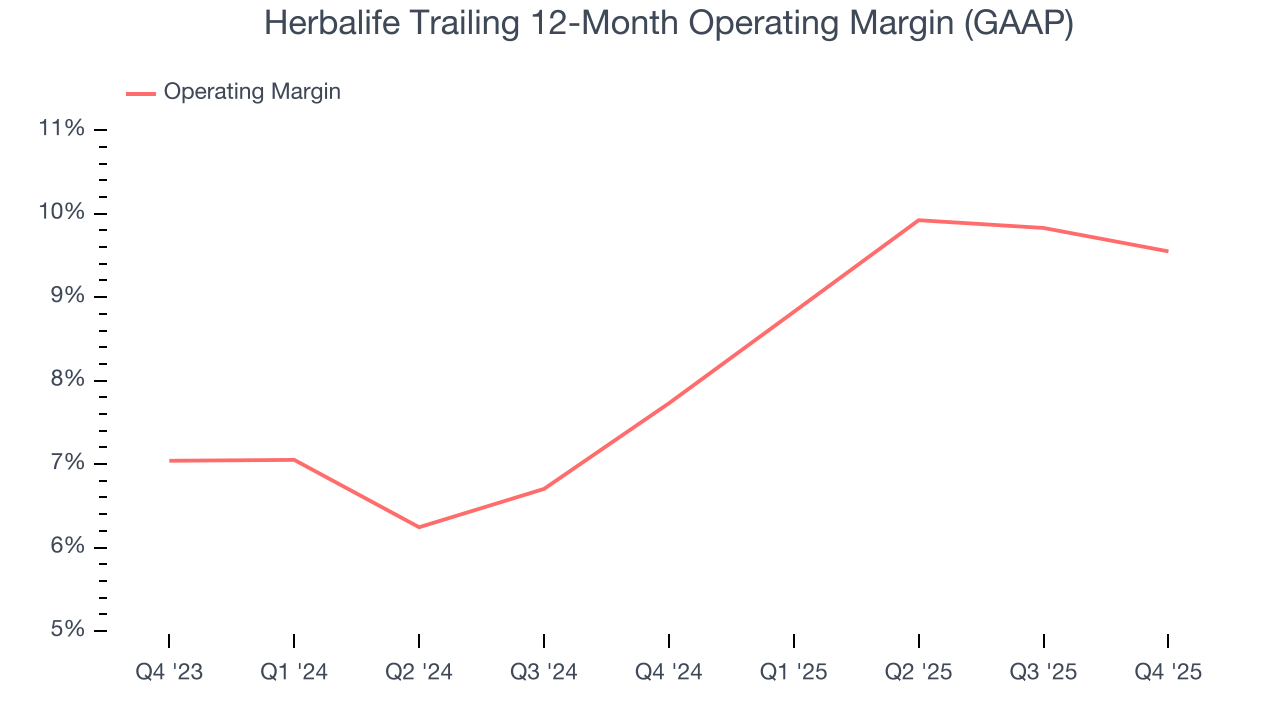

Herbalife has done a decent job managing its cost base over the last two years. The company has produced an average operating margin of 8.6%, higher than the broader consumer staples sector.

Looking at the trend in its profitability, Herbalife’s operating margin rose by 1.8 percentage points over the last year, showing its efficiency has improved.

This quarter, Herbalife generated an operating margin profit margin of 7.8%, down 1 percentage points year on year. Conversely, its revenue and gross margin actually rose, so we can assume it was less efficient because its operating expenses like marketing, and administrative overhead grew faster than its revenue.

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Herbalife, its EPS declined by 14.4% annually over the last three years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

In Q4, Herbalife reported adjusted EPS of $0.45, up from $0.36 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates. Over the next 12 months, Wall Street expects Herbalife’s full-year EPS of $2.13 to grow 32.4%.

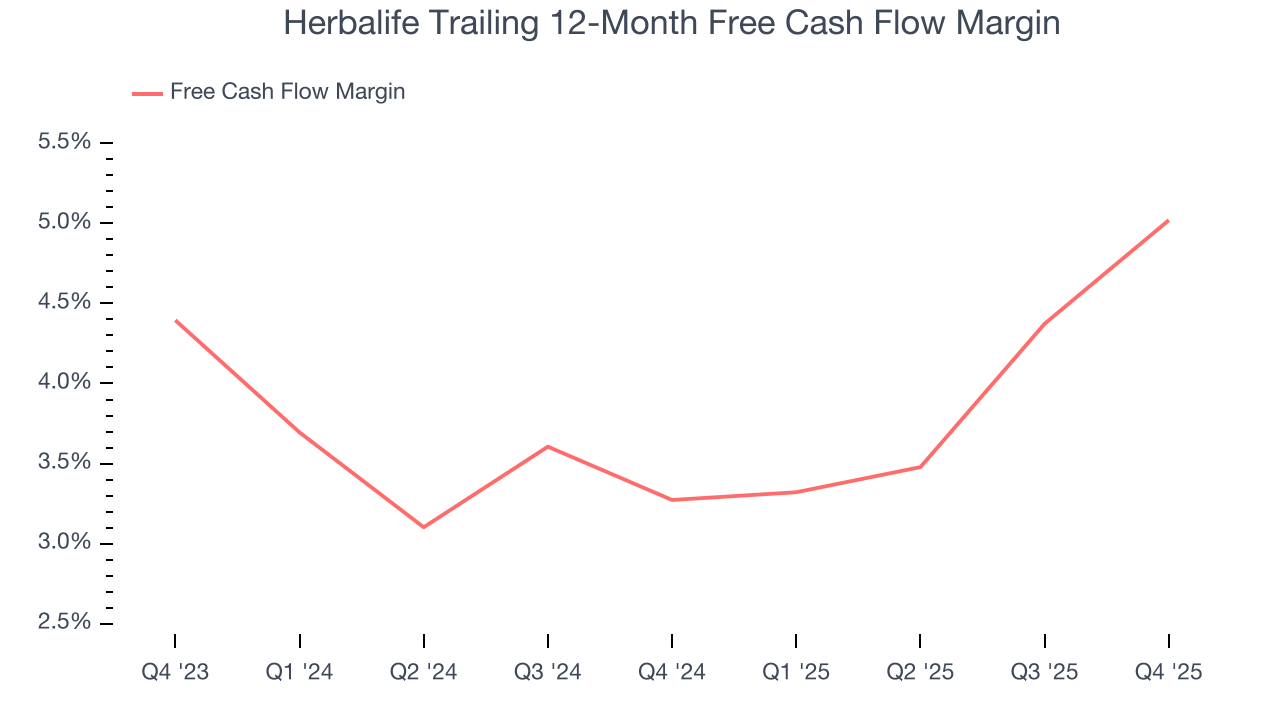

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Herbalife has shown mediocre cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 4.2%, subpar for a consumer staples business.

Taking a step back, an encouraging sign is that Herbalife’s margin expanded by 1.7 percentage points over the last year. We have no doubt shareholders would like to continue seeing its cash conversion rise as it gives the company more optionality.

Herbalife’s free cash flow clocked in at $79.8 million in Q4, equivalent to a 6.2% margin. This result was good as its margin was 2.6 percentage points higher than in the same quarter last year, building on its favorable historical trend.

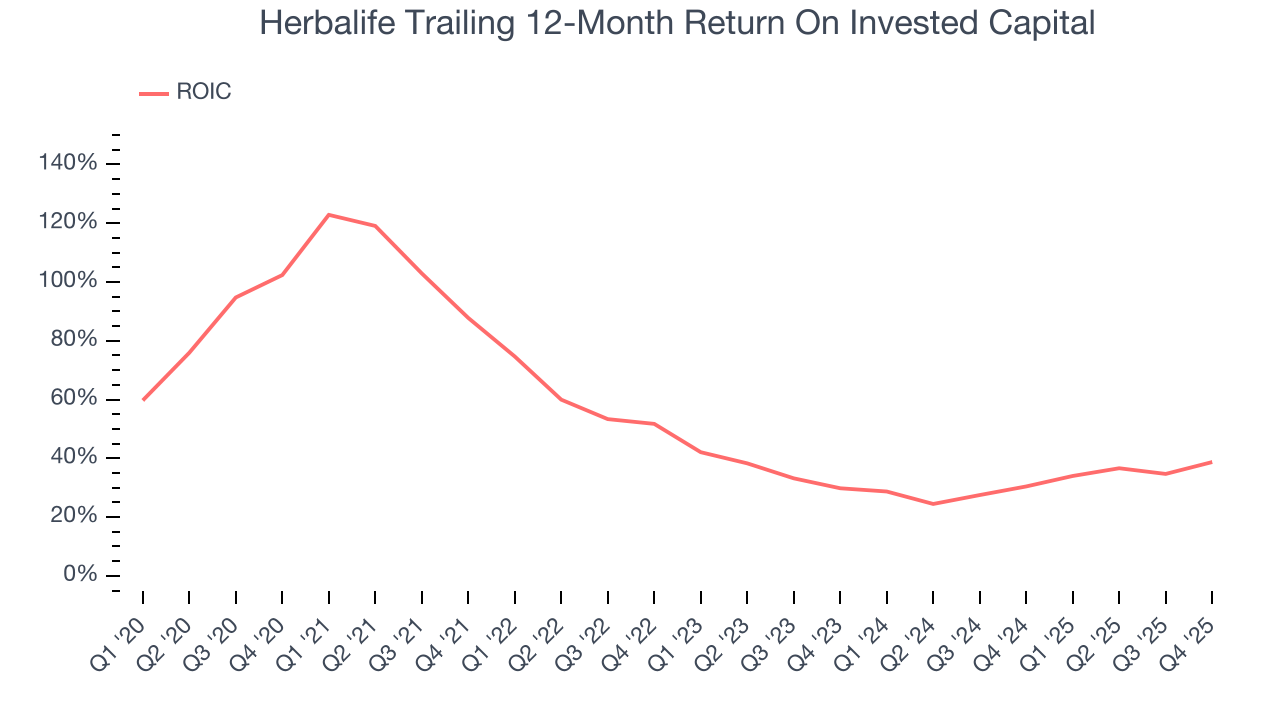

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Although Herbalife hasn’t been the highest-quality company lately because of its poor revenue and EPS performance, it found a few growth initiatives in the past that worked out wonderfully. Its five-year average ROIC was 47.7%, splendid for a consumer staples business.

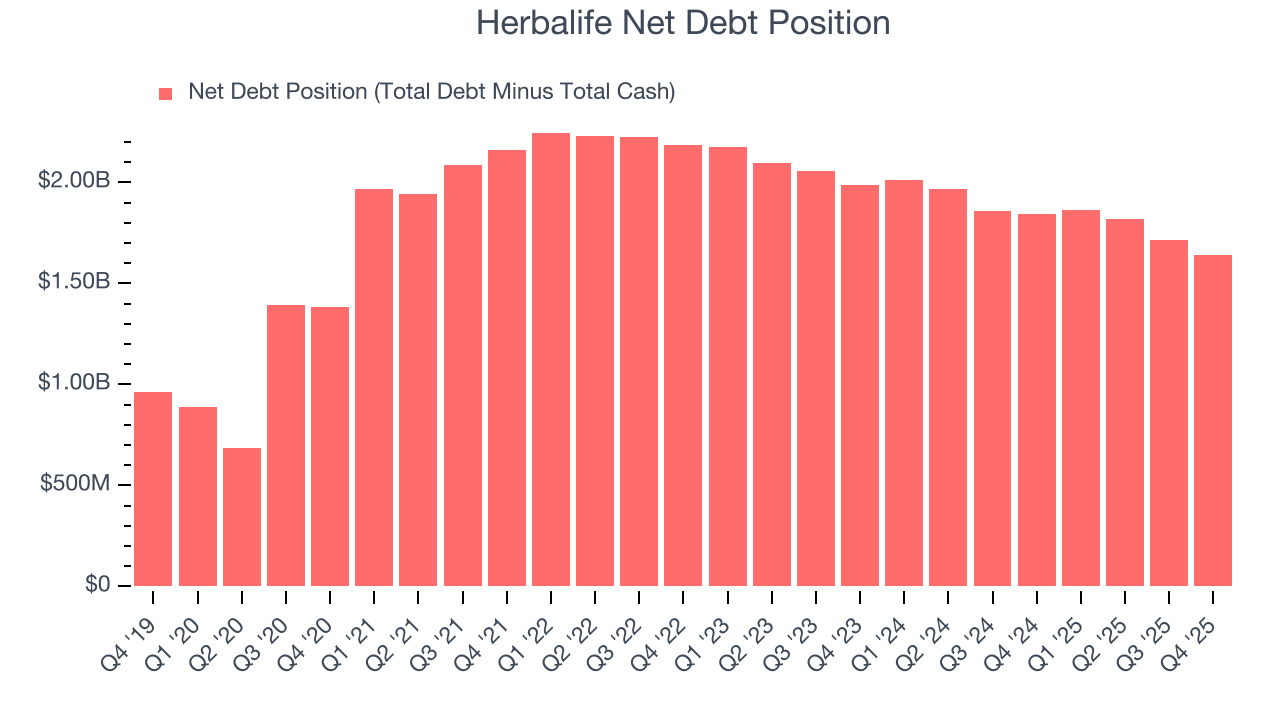

11. Balance Sheet Assessment

Herbalife reported $353.1 million of cash and $1.99 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $674.9 million of EBITDA over the last 12 months, we view Herbalife’s 2.4× net-debt-to-EBITDA ratio as safe. We also see its $107.3 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Herbalife’s Q4 Results

We were impressed by how significantly Herbalife blew past analysts’ EBITDA expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. On the other hand, its EPS missed and its EBITDA guidance for next quarter fell short of Wall Street’s estimates. Overall, this print was mixed but still had some key positives. The stock traded up 11.7% to $18.47 immediately after reporting.

13. Is Now The Time To Buy Herbalife?

Updated: March 25, 2026 at 10:54 PM EDT

When considering an investment in Herbalife, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

Herbalife isn’t a bad business, but we have other favorites. Although its revenue has declined over the last three years, its growth over the next 12 months is expected to be higher. And while Herbalife’s declining EPS over the last three years makes it a less attractive asset to the public markets, its admirable gross margins are a wonderful starting point for the overall profitability of the business.

Herbalife’s P/E ratio based on the next 12 months is 5.9x. This valuation multiple is fair, but we don’t have much faith in the company. We're fairly confident there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $16.50 on the company (compared to the current share price of $15.27).