Hubbell (HUBB)

Hubbell is an exciting business. Its robust cash flows and returns on capital showcase its management team’s strong investing abilities.― StockStory Analyst Team

1. News

2. Summary

Why We Like Hubbell

A respected player in the electrical segment, Hubbell (NYSE:HUBB) manufactures electronic products for the construction, industrial, utility, and telecommunications markets.

- Additional sales over the last five years increased its profitability as the 17.9% annual growth in its earnings per share outpaced its revenue

- Stellar returns on capital showcase management’s ability to surface highly profitable business ventures, and its returns are climbing as it finds even more attractive growth opportunities

- Excellent operating margin highlights the strength of its business model, and it turbocharged its profits by achieving some fixed cost leverage

We expect great things from Hubbell. The price looks reasonable relative to its quality, so this might be a favorable time to buy some shares.

Why Is Now The Time To Buy Hubbell?

Hubbell is trading at $498 per share, or 24.9x forward P/E. This valuation is fair - even cheap depending on how much you like the story - for the quality you get.

Our analysis and backtests show high-quality businesses routinely outperform the market over a multi-year period, especially when priced like this.

3. Hubbell (HUBB) Research Report: Q4 CY2025 Update

Electrical and electronic products company Hubbell (NYSE:HUBB) met Wall Streets revenue expectations in Q4 CY2025, with sales up 11.9% year on year to $1.49 billion. Its non-GAAP profit of $4.73 per share was in line with analysts’ consensus estimates.

Hubbell (HUBB) Q4 CY2025 Highlights:

- Revenue: $1.49 billion vs analyst estimates of $1.49 billion (11.9% year-on-year growth, in line)

- Adjusted EPS: $4.73 vs analyst estimates of $4.72 (in line)

- Adjusted EBITDA: $373 million vs analyst estimates of $369.2 million (25% margin, 1% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $19.50 at the midpoint, missing analyst estimates by 1.6%

- Operating Margin: 20.9%, up from 19.5% in the same quarter last year

- Free Cash Flow Margin: 26%, down from 27.3% in the same quarter last year

- Organic Revenue rose 8.9% year on year (beat)

- Market Capitalization: $26.34 billion

Company Overview

A respected player in the electrical segment, Hubbell (NYSE:HUBB) manufactures electronic products for the construction, industrial, utility, and telecommunications markets.

In the construction industry, Hubbell provides wiring devices, lighting fixtures, and electrical components. It also sells a range of robust industrial electrical equipment like heavy-duty connectors, motor controls, and power systems designed to withstand harsh environments for the industrial industry.

The company also manufactures power distribution equipment like transformers and insulators, which are crucial for the generation and transmission of electricity, which are sold to companies in the utility and energy industries. Lastly, Hubell produces fiber optic connectors, enclosures, and structured cabling systems to telecommunications companies.

The bulk of Hubbell’s revenue comes from product sales to companies in their respective sectors, along with its associated maintenance and support services. The company also often engages in large contractual projects, especially with utility and construction companies, to help them with comprehensive start-to-finish solutions. It sells its products through a wide network of distributors, wholesalers, and retailers, as well as directly to large institutional customers.

4. Electrical Systems

Like many equipment and component manufacturers, electrical systems companies are buoyed by secular trends such as connectivity and industrial automation. More specific pockets of strong demand include Internet of Things (IoT) connectivity and the 5G telecom upgrade cycle, which can benefit companies whose cables and conduits fit those needs. But like the broader industrials sector, these companies are also at the whim of economic cycles. Interest rates, for example, can greatly impact projects that drive demand for these products.

Competitors of Hubbell include Eaton (NYSE:ETN), ABB (NYSE:ABB), and Schneider Electric (EPA:SU).

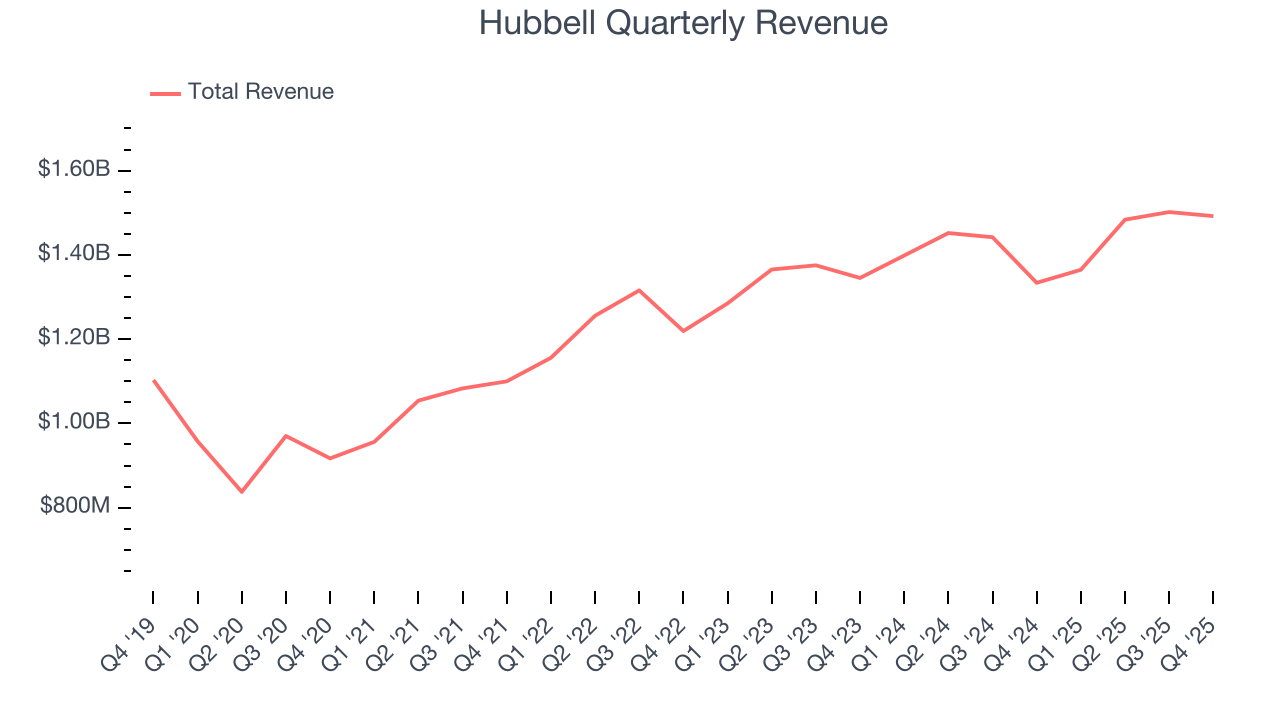

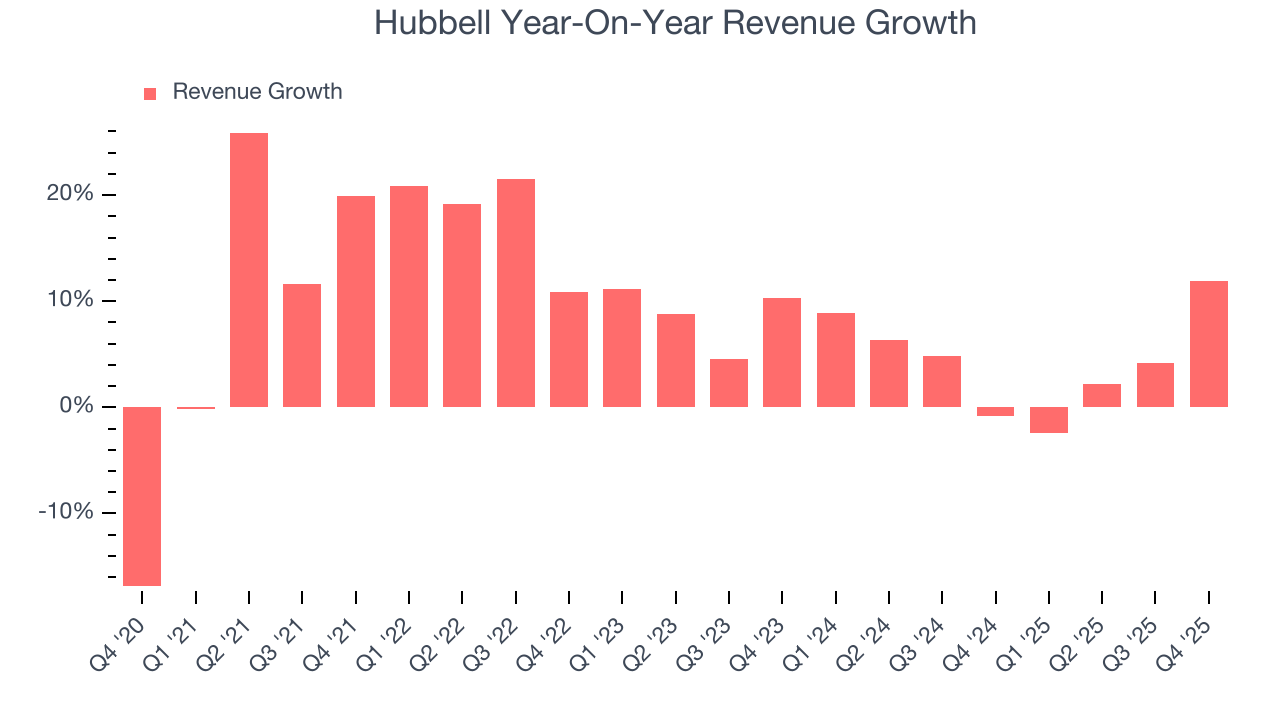

5. Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, Hubbell’s 9.7% annualized revenue growth over the last five years was solid. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Hubbell’s recent performance shows its demand has slowed as its annualized revenue growth of 4.3% over the last two years was below its five-year trend.

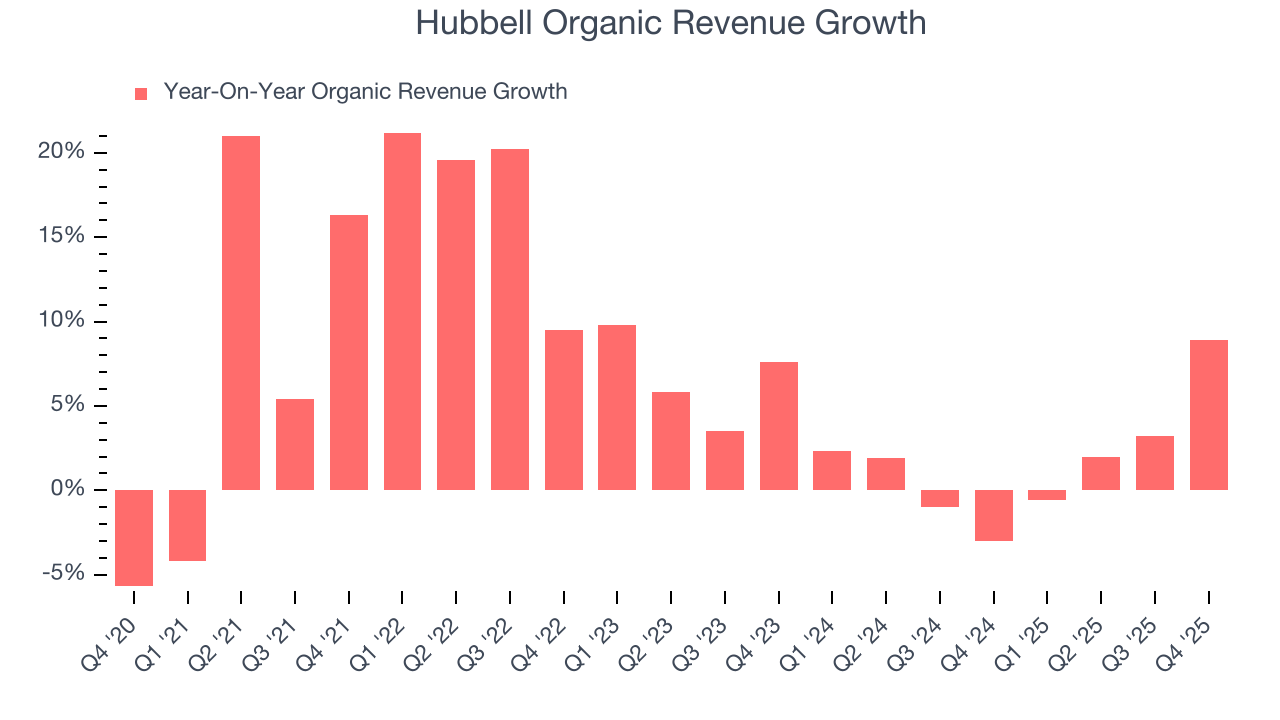

Hubbell also reports organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Hubbell’s organic revenue averaged 1.7% year-on-year growth. Because this number is lower than its two-year revenue growth, we can see that some mixture of acquisitions and foreign exchange rates boosted its headline results.

This quarter, Hubbell’s year-on-year revenue growth was 11.9%, and its $1.49 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 7.8% over the next 12 months, an improvement versus the last two years. This projection is above the sector average and suggests its newer products and services will spur better top-line performance.

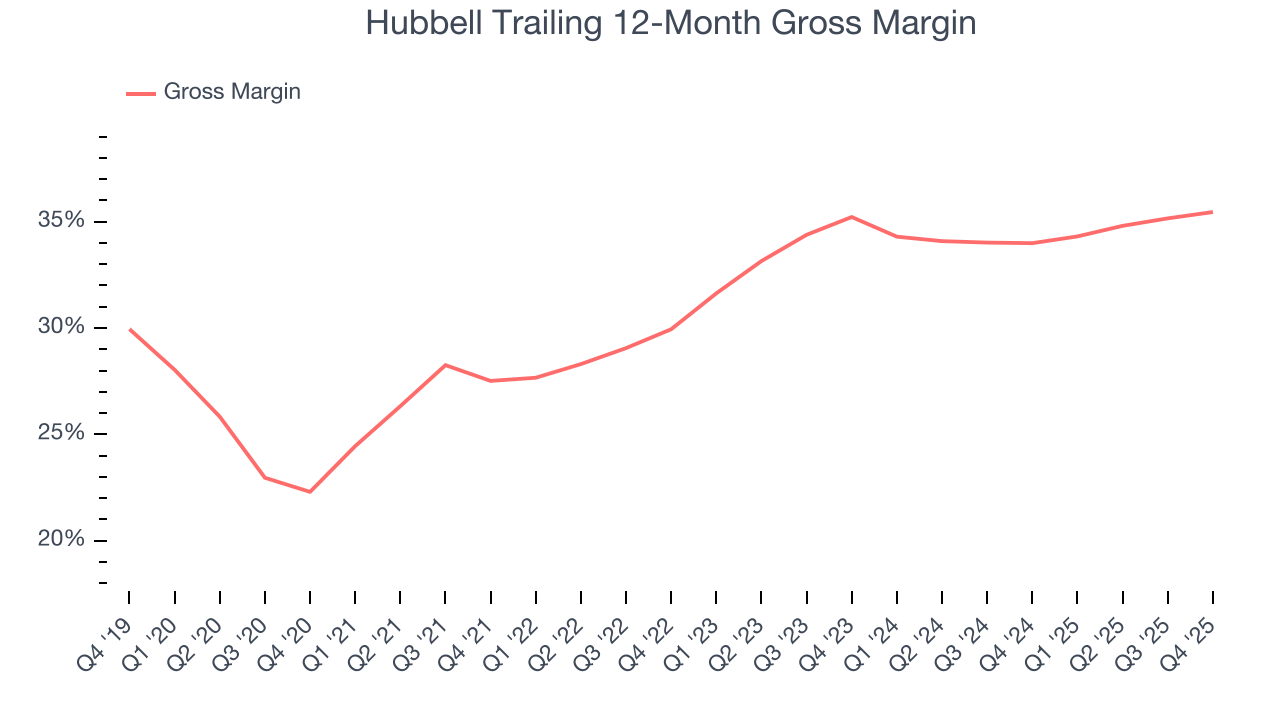

6. Gross Margin & Pricing Power

Hubbell’s unit economics are better than the typical industrials business, signaling its products are somewhat differentiated through quality or brand.As you can see below, it averaged a decent 32.8% gross margin over the last five years. Said differently, Hubbell paid its suppliers $67.24 for every $100 in revenue.

Hubbell produced a 35.2% gross profit margin in Q4, up 1.3 percentage points year on year. Hubbell’s full-year margin has also been trending up over the past 12 months, increasing by 1.5 percentage points. If this move continues, it could suggest better unit economics due to more leverage from its growing sales on the fixed portion of its cost of goods sold (such as manufacturing expenses).

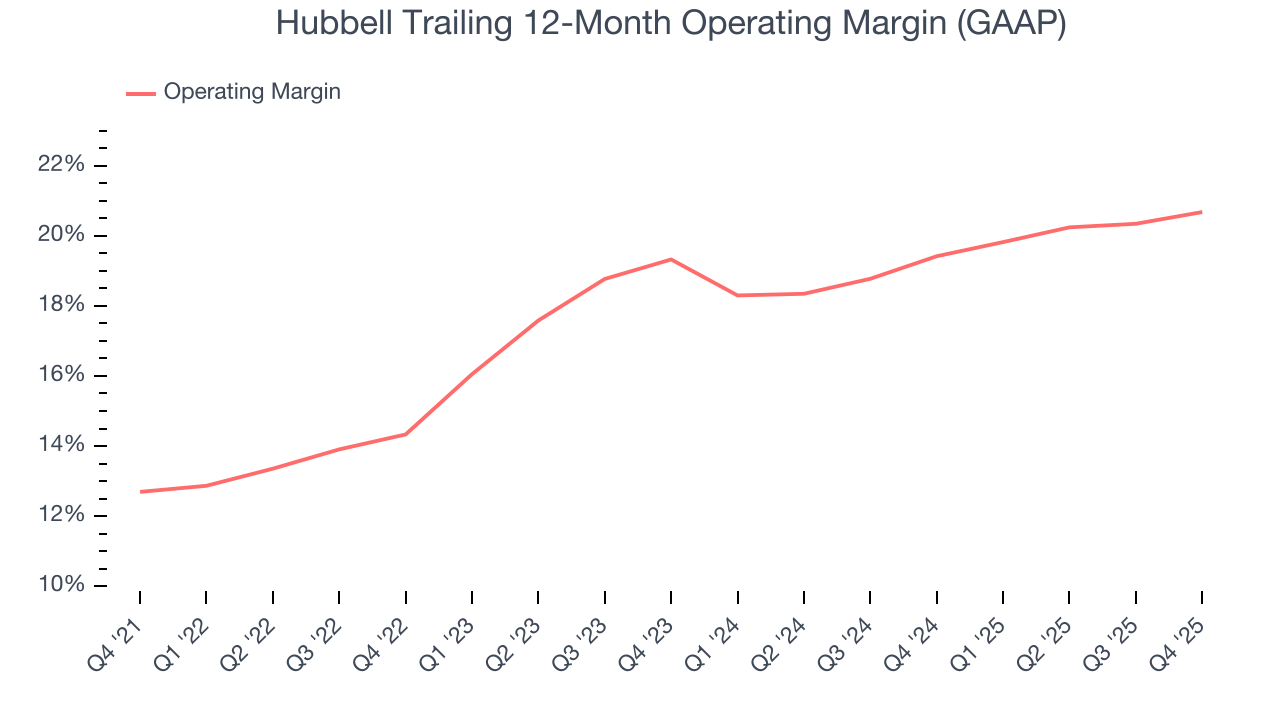

7. Operating Margin

Hubbell has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 17.6%.

Analyzing the trend in its profitability, Hubbell’s operating margin rose by 8 percentage points over the last five years, as its sales growth gave it immense operating leverage.

This quarter, Hubbell generated an operating margin profit margin of 20.9%, up 1.4 percentage points year on year. The increase was encouraging, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

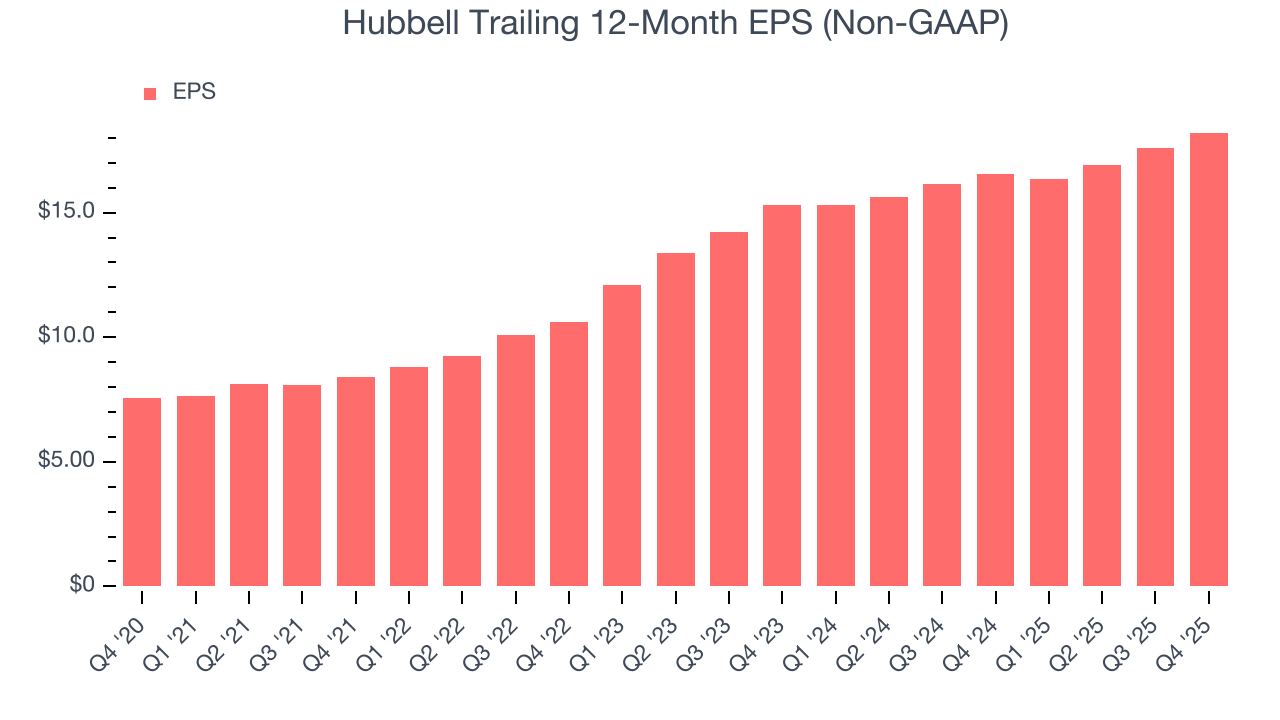

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Hubbell’s EPS grew at an astounding 19.2% compounded annual growth rate over the last five years, higher than its 9.7% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Diving into the nuances of Hubbell’s earnings can give us a better understanding of its performance. As we mentioned earlier, Hubbell’s operating margin expanded by 8 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Hubbell, its two-year annual EPS growth of 9% was lower than its five-year trend. This wasn’t great, but at least the company was successful in other measures of financial health.

In Q4, Hubbell reported adjusted EPS of $4.73, up from $4.10 in the same quarter last year. This print was close to analysts’ estimates. Over the next 12 months, Wall Street expects Hubbell’s full-year EPS of $18.21 to grow 8.8%.

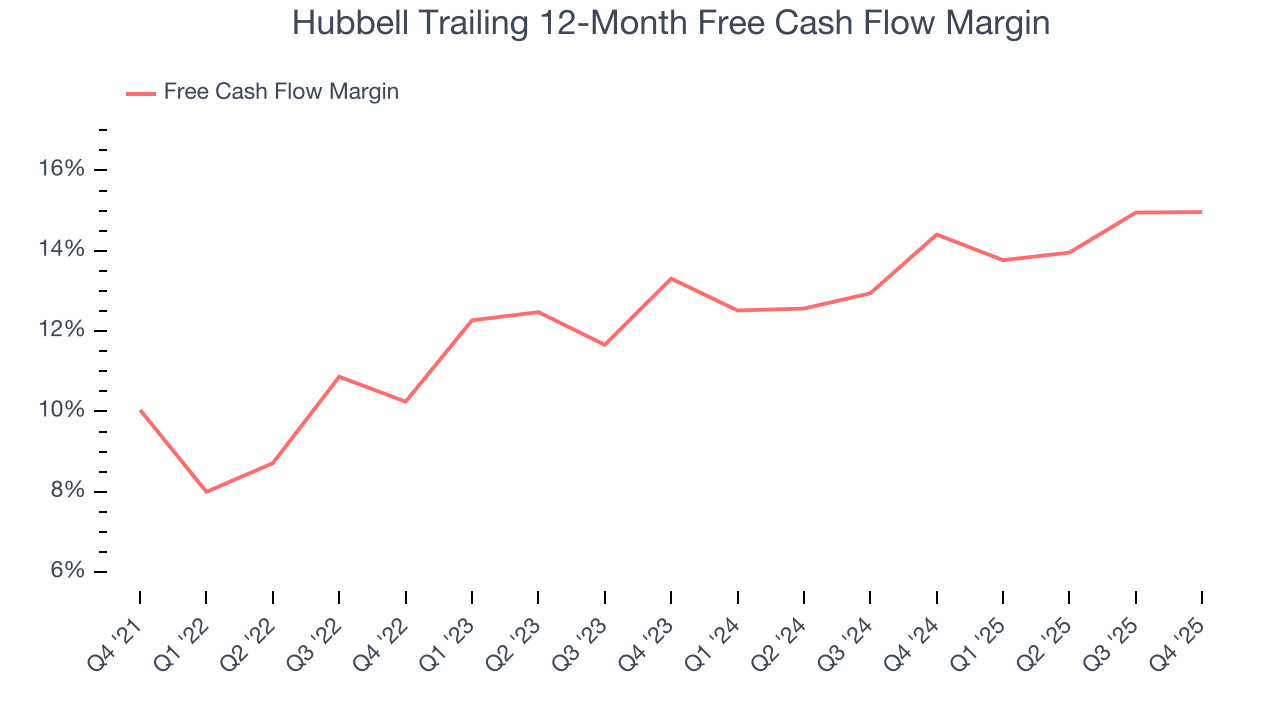

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Hubbell has shown robust cash profitability, enabling it to comfortably ride out cyclical downturns while investing in plenty of new offerings and returning capital to investors. The company’s free cash flow margin averaged 12.8% over the last five years, quite impressive for an industrials business.

Taking a step back, we can see that Hubbell’s margin expanded by 4.9 percentage points during that time. This is encouraging because it gives the company more optionality.

Hubbell’s free cash flow clocked in at $388.8 million in Q4, equivalent to a 26% margin. The company’s cash profitability regressed as it was 1.3 percentage points lower than in the same quarter last year, but it’s still above its five-year average. We wouldn’t read too much into this quarter’s decline because capital expenditures can be seasonal and companies often stockpile inventory in anticipation of higher demand, causing short-term swings. Long-term trends carry greater meaning.

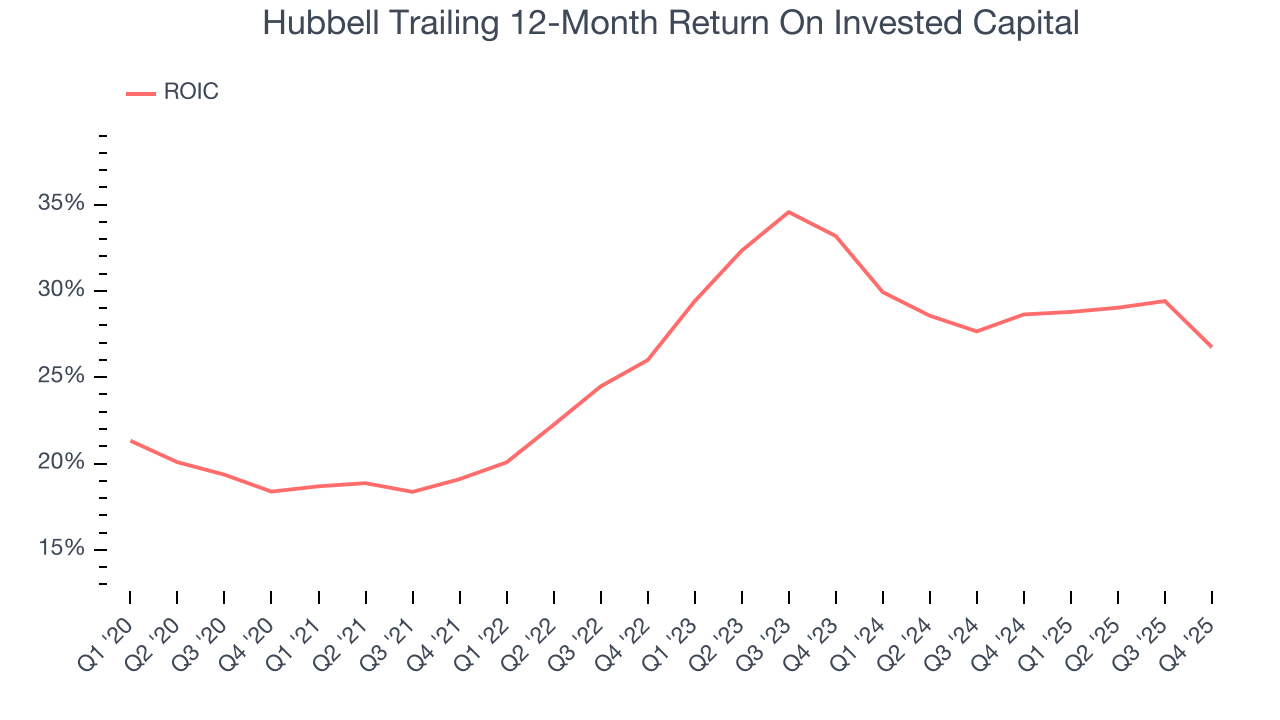

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Hubbell’s five-year average ROIC was 26.7%, placing it among the best industrials companies. This illustrates its management team’s ability to invest in highly profitable ventures and produce tangible results for shareholders.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Hubbell’s ROIC has increased over the last few years. This is a great sign when paired with its already strong returns. It could suggest its competitive advantage or profitable growth opportunities are expanding.

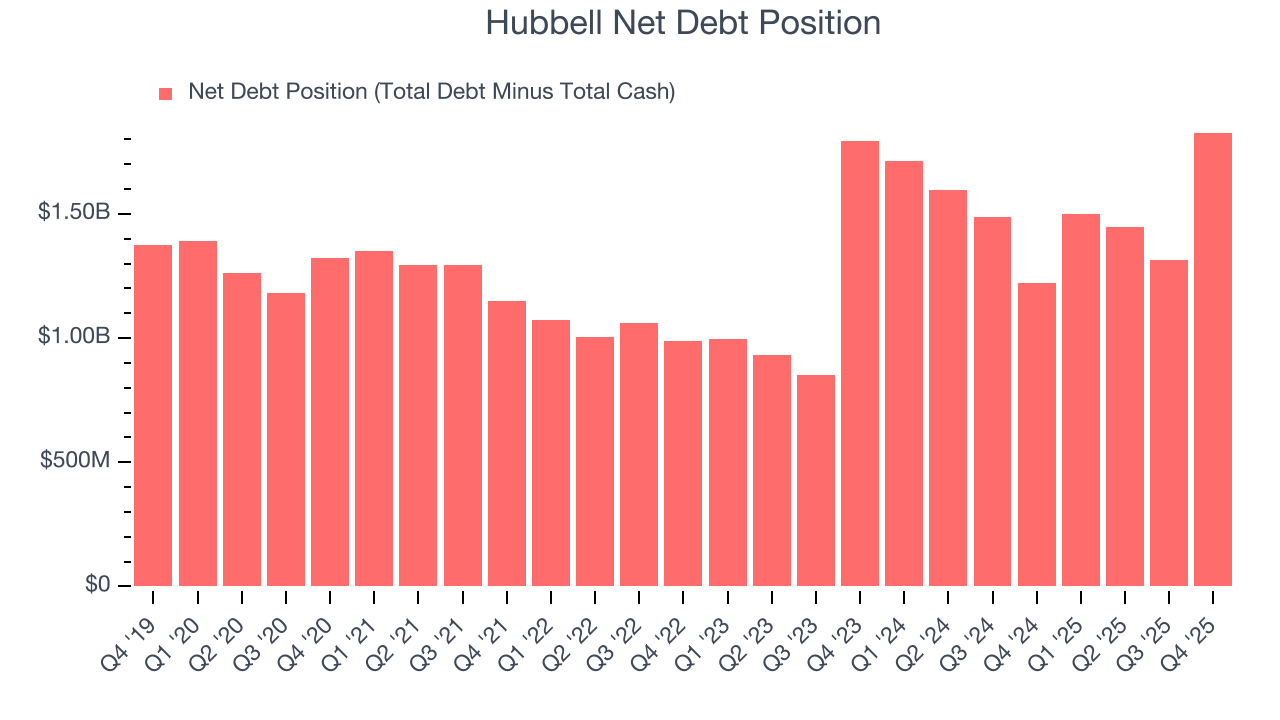

11. Balance Sheet Assessment

Hubbell reported $497.9 million of cash and $2.33 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $1.41 billion of EBITDA over the last 12 months, we view Hubbell’s 1.3× net-debt-to-EBITDA ratio as safe. We also see its $64.1 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Hubbell’s Q4 Results

Revenue and EPS were just in line, and full-year EPS guidance missed. Overall, this was a weaker quarter without any major positive surprises. The stock remained flat at $498 immediately following the results.

13. Is Now The Time To Buy Hubbell?

Updated: February 3, 2026 at 7:48 AM EST

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Hubbell.

Hubbell possesses a number of positive attributes. To kick things off, its revenue growth was solid over the last five years. And while its organic revenue growth has disappointed, its impressive operating margins show it has a highly efficient business model. On top of that, its expanding operating margin shows the business has become more efficient.

Hubbell’s P/E ratio based on the next 12 months is 25x. Analyzing the industrials landscape today, Hubbell’s positive attributes shine bright. We like the stock at this price.

Wall Street analysts have a consensus one-year price target of $503.77 on the company (compared to the current share price of $498).