IMAX (IMAX)

We’re firm believers in IMAX. Its impressive revenue growth indicates the value of its offerings.― StockStory Analyst Team

1. News

2. Summary

Why We Like IMAX

Originally developed for World Expo '67 in Montreal as an innovative projection system, IMAX (NYSE:IMAX) provides proprietary large-format cinema technology and systems that deliver immersive movie experiences with enhanced image quality and sound.

- Annual revenue growth of 24.5% over the last five years was superb and indicates its market share increased during this cycle

- Earnings per share grew by 22.6% annually over the last five years and trumped its peers

- Projected revenue growth of 7.3% for the next 12 months indicates demand will rise above its two-year trend

IMAX is a market leader. The price seems fair relative to its quality, so this could be an opportune time to buy some shares.

Why Is Now The Time To Buy IMAX?

IMAX is trading at $37.47 per share, or 23x forward P/E. While this multiple is higher than most business services companies, we think the valuation is fair given its quality characteristics.

Entry price certainly impacts returns, but over a long-term, multi-year period, business quality matters much more than where you buy a stock.

3. IMAX (IMAX) Research Report: Q4 CY2025 Update

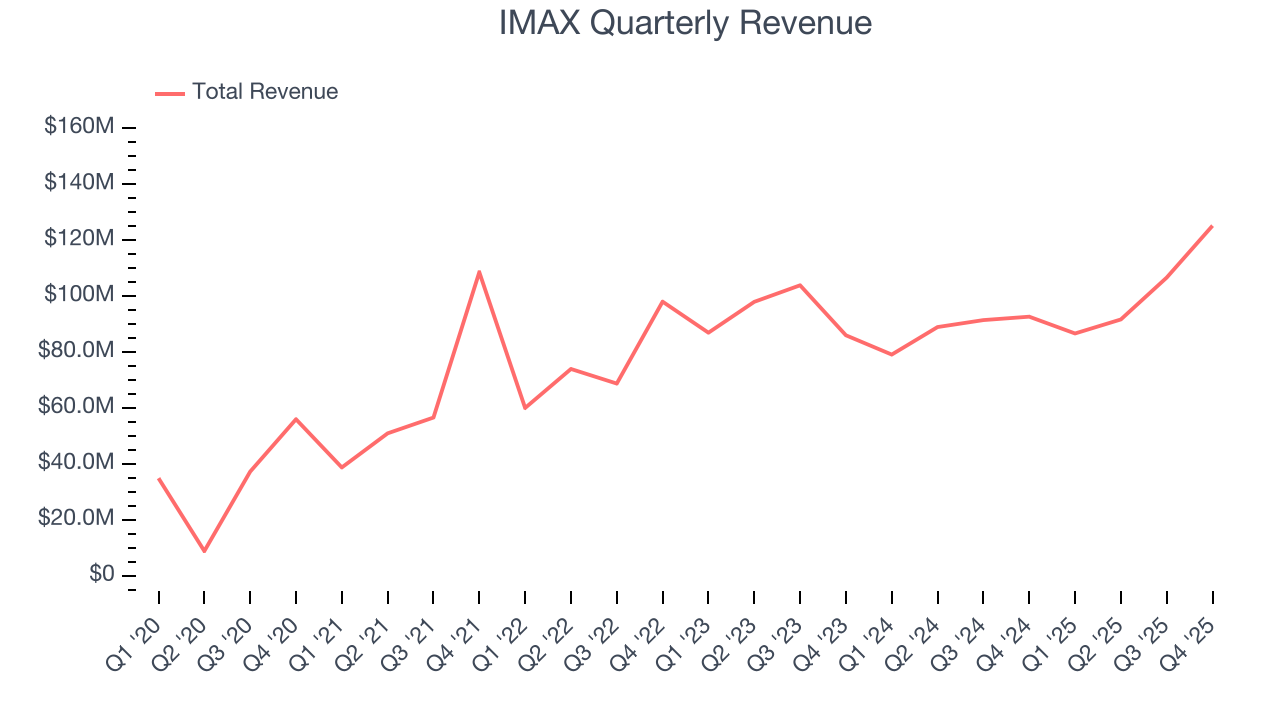

Premium cinema technology company IMAX (NYSE:IMAX) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, with sales up 35.1% year on year to $125.2 million. Its non-GAAP profit of $0.58 per share was 22.9% above analysts’ consensus estimates.

IMAX (IMAX) Q4 CY2025 Highlights:

- Revenue: $125.2 million vs analyst estimates of $120.6 million (35.1% year-on-year growth, 3.8% beat)

- Adjusted EPS: $0.58 vs analyst estimates of $0.47 (22.9% beat)

- Adjusted EBITDA: $53.06 million vs analyst estimates of $49.54 million (42.4% margin, 7.1% beat)

- Operating Margin: 19.3%, up from 10.3% in the same quarter last year

- Free Cash Flow Margin: 22.3%, up from 0.7% in the same quarter last year

- Market Capitalization: $1.98 billion

Company Overview

Originally developed for World Expo '67 in Montreal as an innovative projection system, IMAX (NYSE:IMAX) provides proprietary large-format cinema technology and systems that deliver immersive movie experiences with enhanced image quality and sound.

IMAX operates as a technology platform that transforms conventional films into visually stunning, immersive experiences through its proprietary digital remastering process. The company's business model centers on selling or leasing its premium projection systems to theater operators worldwide, while also generating revenue from film distribution and maintenance services.

The IMAX system includes specialized projectors, screens, sound systems, and theater designs that collectively create what the company markets as "The IMAX Experience." Its laser-based digital projection systems deliver sharper images with deeper contrast and wider color ranges than standard cinema projectors. The company's proprietary sound technology uses uncompressed audio and custom speaker configurations to ensure optimal sound quality throughout the theater.

Filmmakers increasingly collaborate with IMAX through its "Filmed For IMAX" program, where movies are shot using IMAX-certified cameras to take advantage of the format's expanded aspect ratio, showing up to 26% more image on standard IMAX screens and up to 67% more in select locations. For example, Christopher Nolan's "Oppenheimer" was filmed with IMAX 70mm cameras, creating a distinctive viewing experience that drove significant audience demand.

IMAX generates revenue through multiple channels: selling or leasing its systems to exhibitors, collecting fees for digitally remastering films, providing ongoing maintenance services, and distributing documentary films. The company has also expanded into streaming technology with its IMAX Enhanced program, which brings aspects of the IMAX experience to home entertainment through partnerships with streaming platforms and device manufacturers.

With a global network spanning 90 countries and territories, IMAX has established particularly strong presence in international markets, which represent 76% of its commercial multiplex installations. The company has been especially successful in China, where it operates 807 systems through partnerships with major exhibitors like Wanda Film.

4. Traditional Media & Publishing

The sector faces structural headwinds from declining linear TV viewership, shifts in advertising spend toward digital platforms, and ongoing challenges in monetizing print and broadcast content. However, for companies that invest wisely, tailwinds can include AI, the power of which can result in more personalized content creation and more detailed audience analysis. These can create a flywheel of success where one feeds into the other. Still there are outstanding questions around AI-generated content oversight, and the regulatory framework around this could evolve in unseen ways over the next few years.

IMAX competes with premium cinema format providers like Dolby Laboratories' Dolby Cinema (NYSE:DLB), 4DX by CJ 4DPLEX, and ScreenX. In the broader theatrical exhibition space, it also faces competition from major theater chains with their own premium large format offerings, such as AMC's (NYSE:AMC) Dolby Cinema and PRIME at AMC, and Regal's RPX.

5. Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $410.2 million in revenue over the past 12 months, IMAX is a small player in the business services space, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and numerous distribution channels. On the bright side, it can grow faster because it has more room to expand.

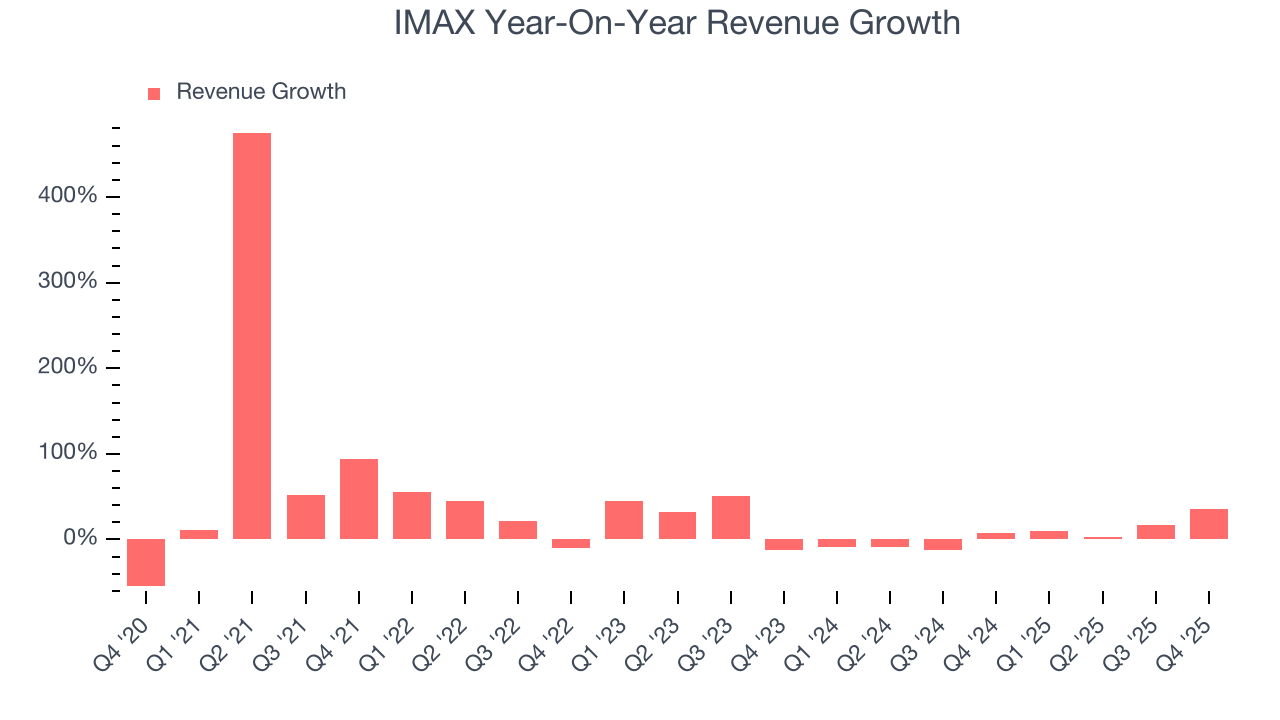

As you can see below, IMAX grew its sales at an incredible 24.5% compounded annual growth rate over the last five years. This shows it had high demand, a useful starting point for our analysis.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. IMAX’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 4.6% over the last two years was well below its five-year trend.

This quarter, IMAX reported wonderful year-on-year revenue growth of 35.1%, and its $125.2 million of revenue exceeded Wall Street’s estimates by 3.8%.

Looking ahead, sell-side analysts expect revenue to grow 7.2% over the next 12 months, an improvement versus the last two years. This projection is commendable and implies its newer products and services will spur better top-line performance.

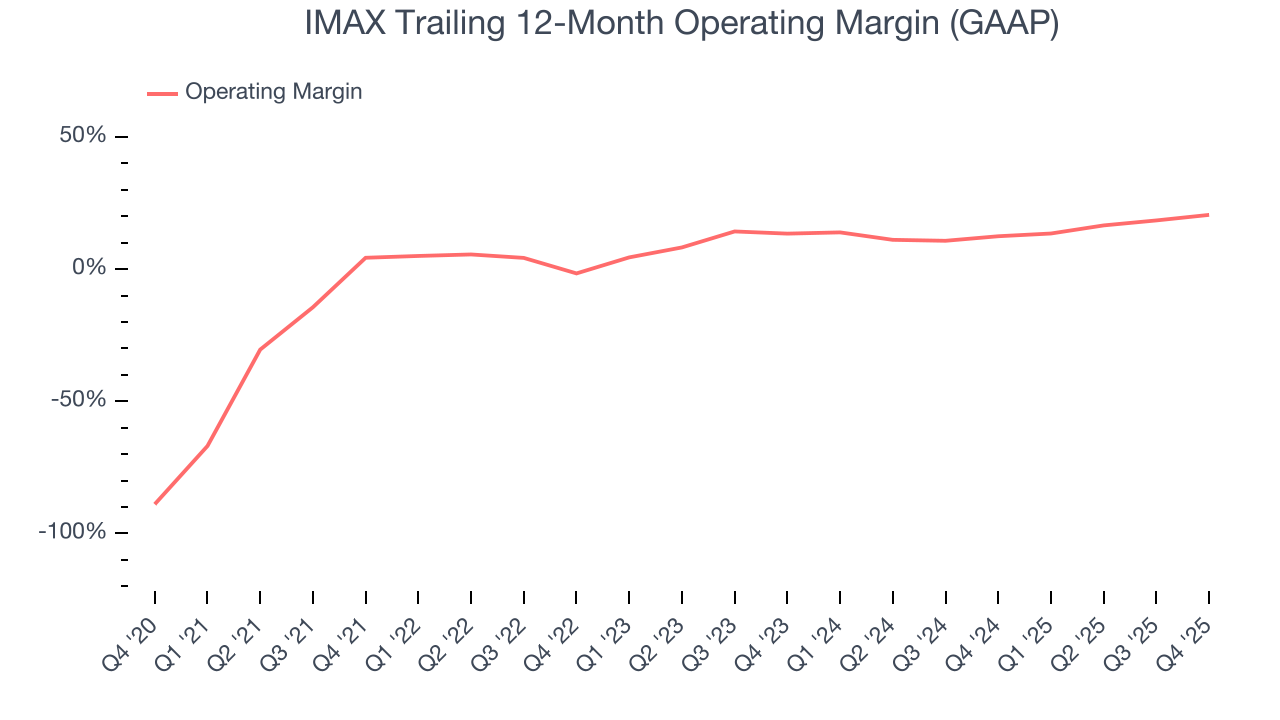

6. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

IMAX has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 10.9%, higher than the broader business services sector.

Looking at the trend in its profitability, IMAX’s operating margin rose by 16.2 percentage points over the last five years, as its sales growth gave it immense operating leverage.

This quarter, IMAX generated an operating margin profit margin of 19.3%, up 9 percentage points year on year. This increase was a welcome development and shows it was more efficient.

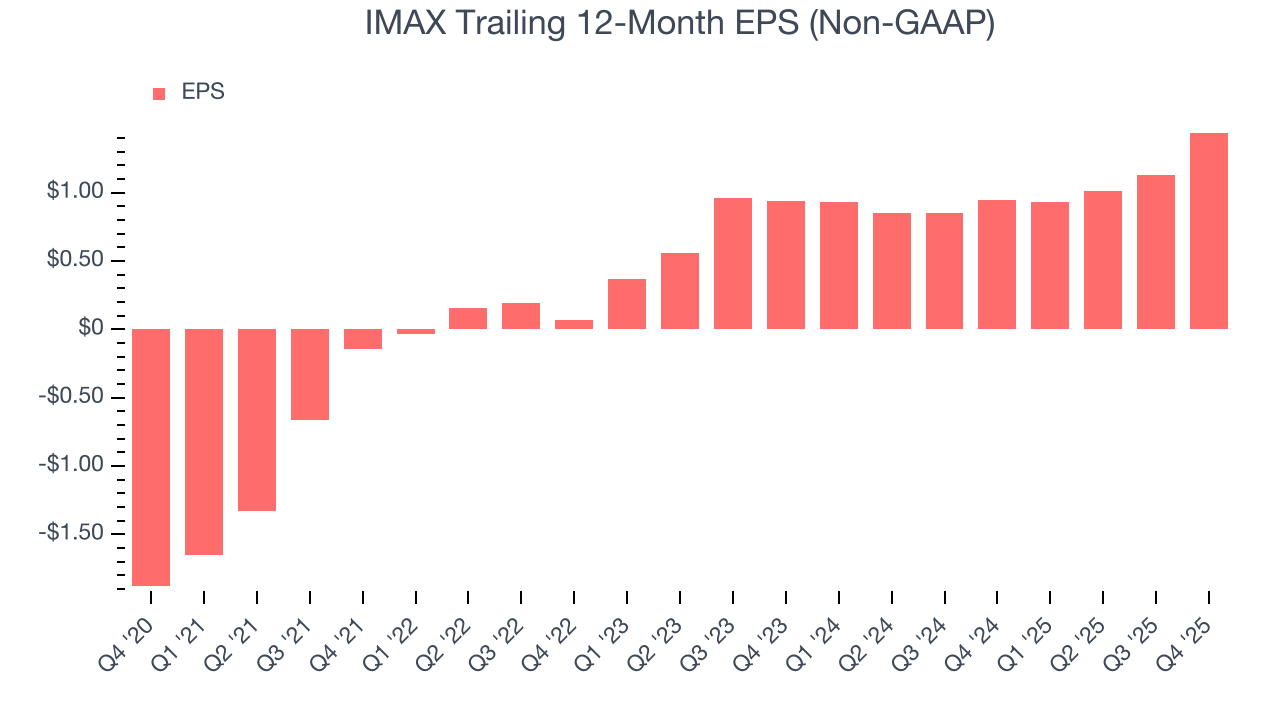

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

IMAX’s full-year EPS flipped from negative to positive over the last five years. This is a good sign and shows it’s at an inflection point.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

IMAX’s EPS grew at an astounding 23.8% compounded annual growth rate over the last two years, higher than its 4.6% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

We can take a deeper look into IMAX’s earnings quality to better understand the drivers of its performance. IMAX’s operating margin has expanded over the last two years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, IMAX reported adjusted EPS of $0.58, up from $0.27 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects IMAX’s full-year EPS of $1.44 to grow 16.7%.

8. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

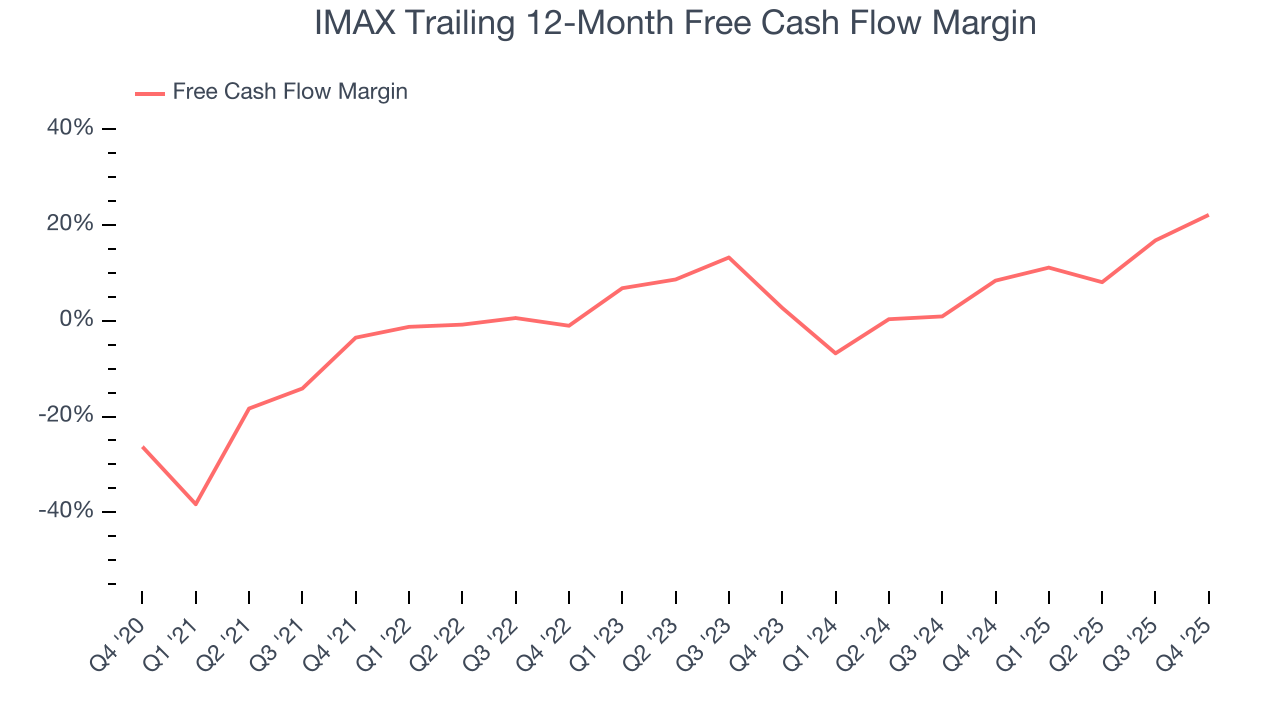

IMAX has shown impressive cash profitability, giving it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 7% over the last five years, better than the broader business services sector.

Taking a step back, we can see that IMAX’s margin expanded by 25.7 percentage points during that time. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

IMAX’s free cash flow clocked in at $27.96 million in Q4, equivalent to a 22.3% margin. This result was good as its margin was 21.7 percentage points higher than in the same quarter last year, building on its favorable historical trend.

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

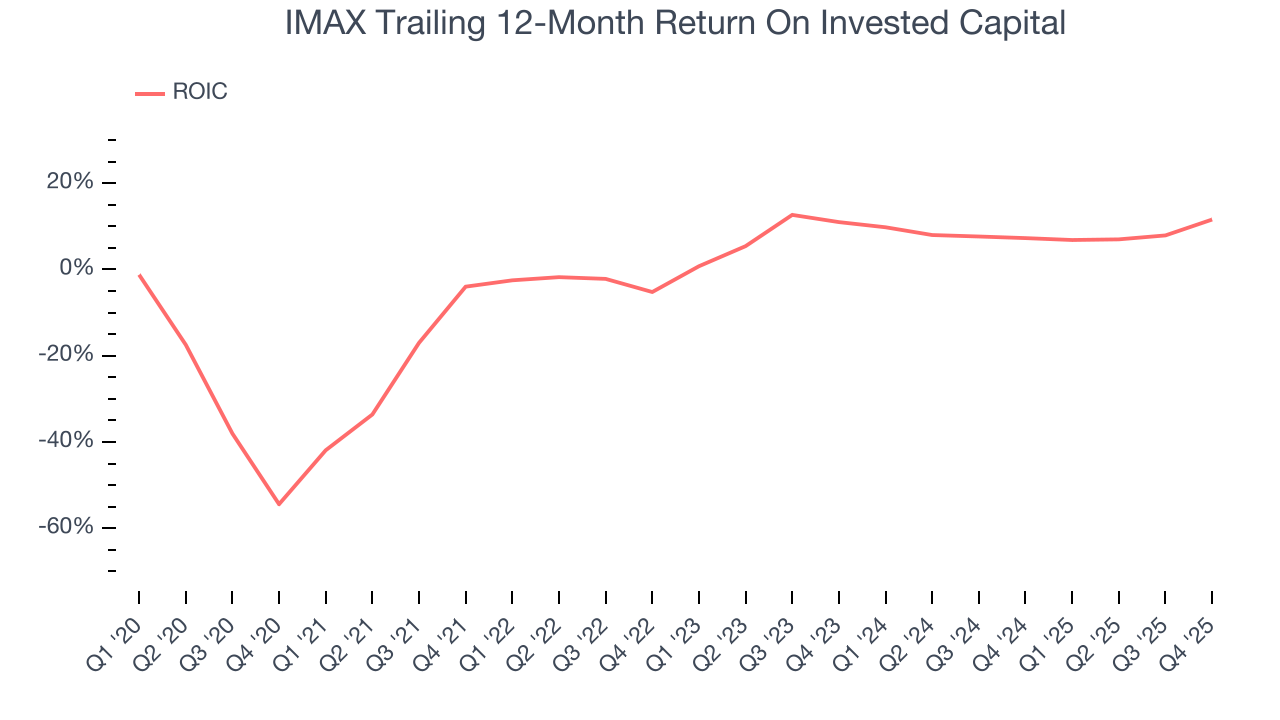

IMAX historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 4.1%, lower than the typical cost of capital (how much it costs to raise money) for business services companies.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Fortunately, IMAX’s ROIC has increased significantly over the last few years. This is a good sign, and if its returns keep rising, there’s a chance it could evolve into an investable business.

10. Balance Sheet Assessment

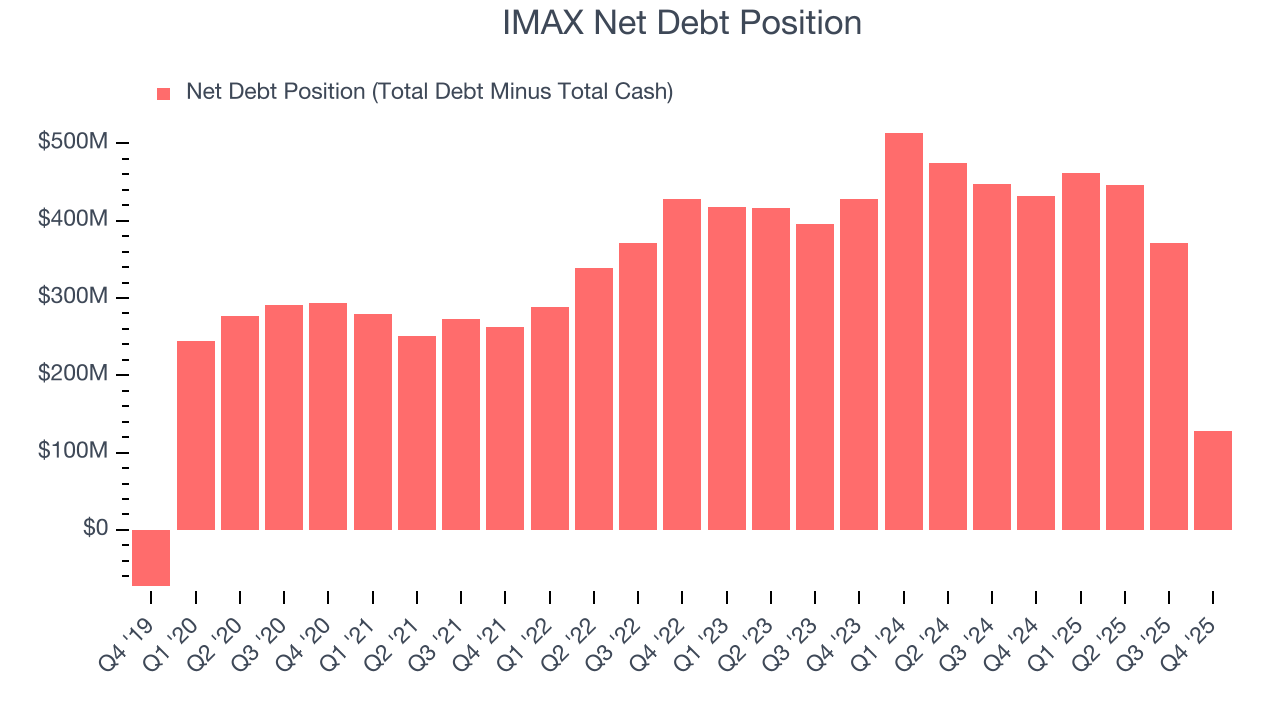

IMAX reported $151.2 million of cash and $278.6 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $165.8 million of EBITDA over the last 12 months, we view IMAX’s 0.8× net-debt-to-EBITDA ratio as safe. We also see its $2.14 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from IMAX’s Q4 Results

It was good to see IMAX beat analysts’ EPS expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock traded up 5.5% to $38.51 immediately after reporting.

12. Is Now The Time To Buy IMAX?

Updated: March 19, 2026 at 12:12 AM EDT

Before investing in or passing on IMAX, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

IMAX is a rock-solid business worth owning. First of all, the company’s revenue growth was exceptional over the last five years. And while its subscale operations give it fewer distribution channels than its larger rivals, its rising cash profitability gives it more optionality. Additionally, IMAX’s expanding adjusted operating margin shows the business has become more efficient.

IMAX’s P/E ratio based on the next 12 months is 23x. Looking across the spectrum of business services companies today, IMAX’s fundamentals shine bright. We like the stock at this price.

Wall Street analysts have a consensus one-year price target of $45 on the company (compared to the current share price of $37.47), implying they see 20.1% upside in buying IMAX in the short term.