Samsara (IOT)

Samsara is a special business. Its financials show it’s a customer acquisition machine that can expand both quickly and organically.― StockStory Analyst Team

1. News

2. Summary

Why We Like Samsara

From sensors on vehicles to AI-powered cameras that help prevent accidents, Samsara (NYSE:IOT) is a cloud-based Internet of Things platform that helps businesses improve the safety, efficiency, and sustainability of their physical operations.

- Annual revenue growth of 45.3% over the last five years was superb and indicates its market share is rising

- ARR trends over the last year show it’s maintaining a steady flow of long-term contracts that contribute positively to its revenue predictability

- Estimated revenue growth of 21.8% for the next 12 months implies its momentum over the last two years will continue

Samsara is a top-tier company. The price seems reasonable in light of its quality, and we think now is a favorable time to invest.

Why Is Now The Time To Buy Samsara?

Samsara is trading at $29.63 per share, or 9.5x forward price-to-sales. Most companies in the software sector may feature a cheaper multiple, but we think Samsara is priced fairly given its fundamentals.

Entry price certainly impacts returns, but over a long-term, multi-year period, business quality matters much more than where you buy a stock.

3. Samsara (IOT) Research Report: Q4 CY2025 Update

IoT solutions provider Samsara (NYSE:IOT) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 28.3% year on year to $444.3 million. Guidance for next quarter’s revenue was optimistic at $455 million at the midpoint, 2.6% above analysts’ estimates. Its non-GAAP profit of $0.18 per share was 40.9% above analysts’ consensus estimates.

Samsara (IOT) Q4 CY2025 Highlights:

- Revenue: $444.3 million vs analyst estimates of $422.3 million (28.3% year-on-year growth, 5.2% beat)

- Adjusted EPS: $0.18 vs analyst estimates of $0.13 (40.9% beat)

- Adjusted Operating Income: $91.84 million vs analyst estimates of $67.33 million (20.7% margin, 36.4% beat)

- Revenue Guidance for Q1 CY2026 is $455 million at the midpoint, above analyst estimates of $443.5 million

- Adjusted EPS guidance for the upcoming financial year 2027 is $0.67 at the midpoint, beating analyst estimates by 15.2%

- Operating Margin: 2%, up from -5.3% in the same quarter last year

- Free Cash Flow Margin: 13.9%, similar to the previous quarter

- Annual Recurring Revenue: $1.89 billion (29.6% year-on-year growth, beat)

- Billings: $444.3 million at quarter end, up 13.3% year on year

- Market Capitalization: $16.55 billion

Company Overview

From sensors on vehicles to AI-powered cameras that help prevent accidents, Samsara (NYSE:IOT) is a cloud-based Internet of Things platform that helps businesses improve the safety, efficiency, and sustainability of their physical operations.

Samsara's technology connects physical assets to the digital world through a combination of hardware devices and software applications. The company's hardware includes vehicle telematics, equipment monitors, environmental sensors, and AI-enabled safety cameras that collect real-time data from trucks, construction equipment, factories, and other physical infrastructure. This data is then processed on Samsara's cloud platform, providing actionable insights through intuitive dashboards and mobile apps.

Transportation and logistics companies use Samsara to track vehicle locations, monitor driver behavior, optimize routes, and ensure compliance with safety regulations. For example, a trucking company might use Samsara to identify unsafe driving practices, reduce idle time, and improve fuel efficiency across their fleet. Similarly, construction firms deploy Samsara sensors on heavy equipment to prevent theft, schedule maintenance based on actual usage, and maximize equipment utilization.

Samsara operates on a subscription-based model, charging customers for both hardware devices and access to its cloud software platform. The company serves thousands of customers across diverse industries including transportation, logistics, construction, field services, utilities, and manufacturing. As physical operations become increasingly digitized, Samsara positions itself at the intersection of the Internet of Things, artificial intelligence, and cloud computing—enabling businesses to transform traditionally analog operations with digital intelligence.

4. Data Analytics

Organizations generate a lot of data that is stored in silos, often in incompatible formats, making it slow and costly to extract actionable insights, which in turn drives demand for modern cloud-based data analysis platforms that can efficiently analyze the siloed data.

Samsara competes with established industrial technology providers like Trimble (NASDAQ:TRMB), Verizon Connect (NYSE:VZ), and Geotab in the fleet management space, as well as Honeywell (NASDAQ:HON) and Rockwell Automation (NYSE:ROK) in industrial IoT applications.

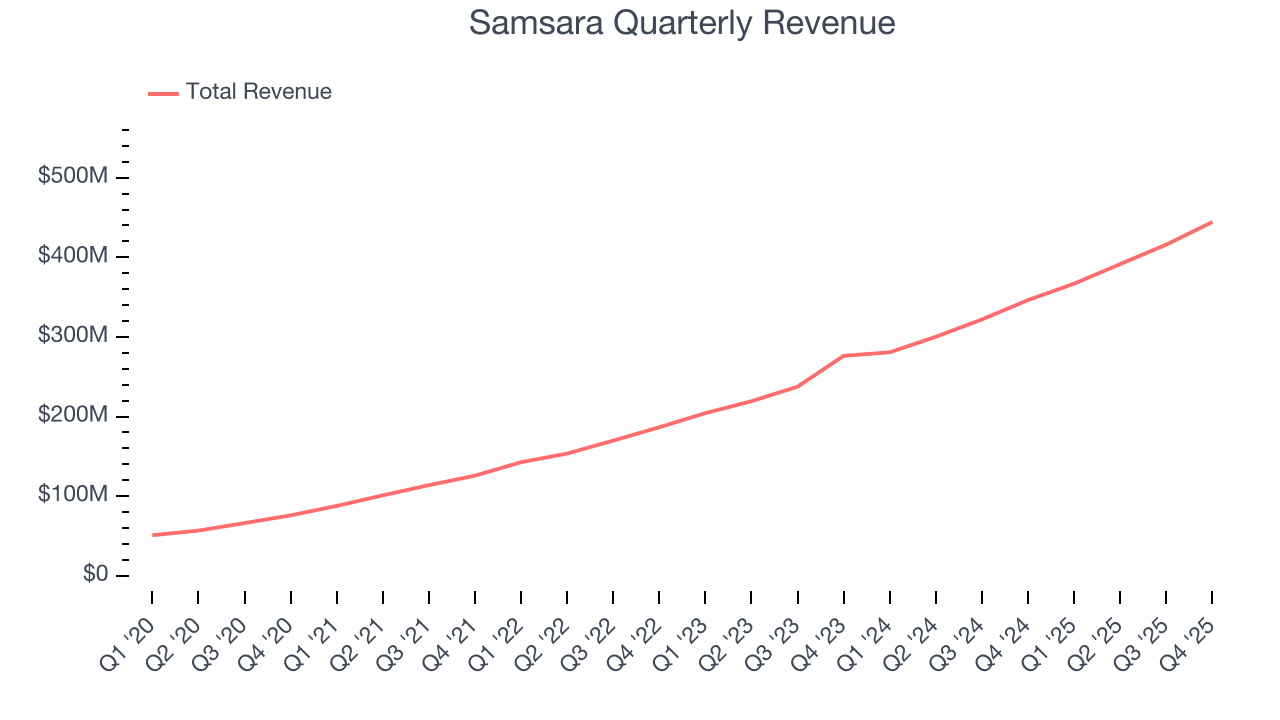

5. Revenue Growth

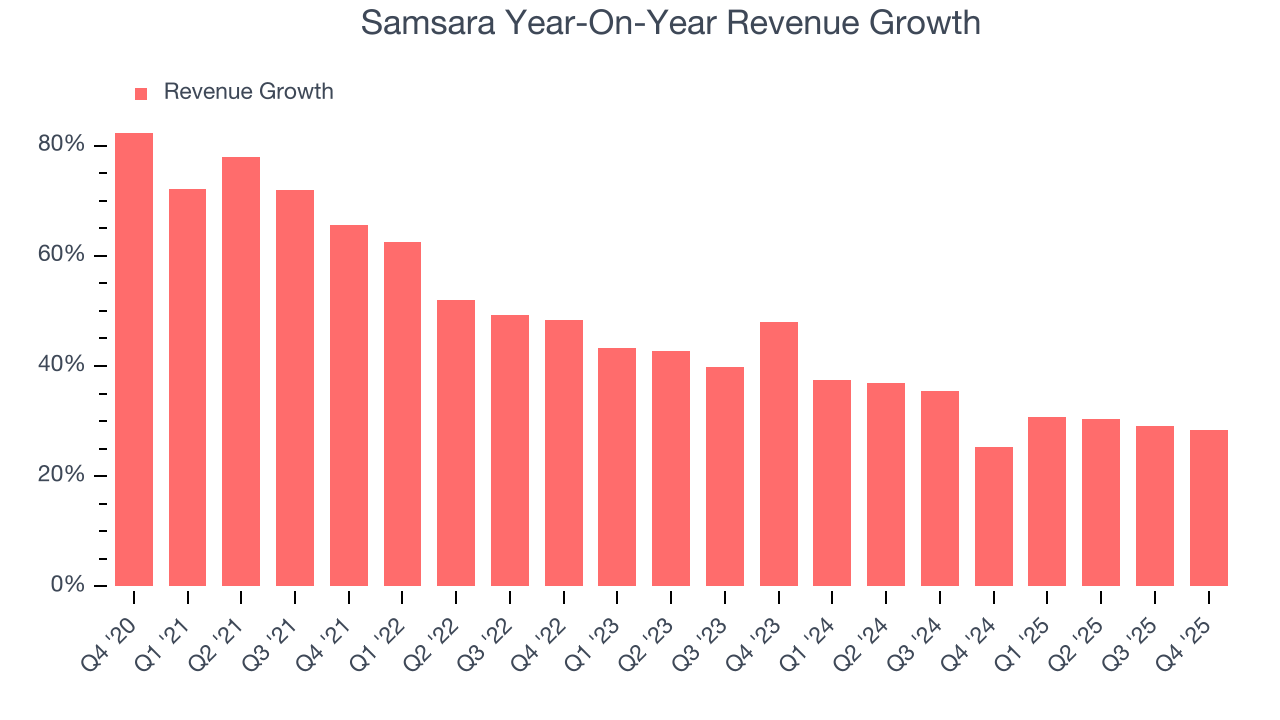

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Luckily, Samsara’s sales grew at an incredible 45.3% compounded annual growth rate over the last five years. Its growth surpassed the average software company and shows its offerings resonate with customers, a great starting point for our analysis.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. Samsara’s annualized revenue growth of 31.4% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Samsara reported robust year-on-year revenue growth of 28.3%, and its $444.3 million of revenue topped Wall Street estimates by 5.2%. Company management is currently guiding for a 24% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 18.3% over the next 12 months, a deceleration versus the last two years. Despite the slowdown, this projection is admirable and indicates the market is forecasting success for its products and services.

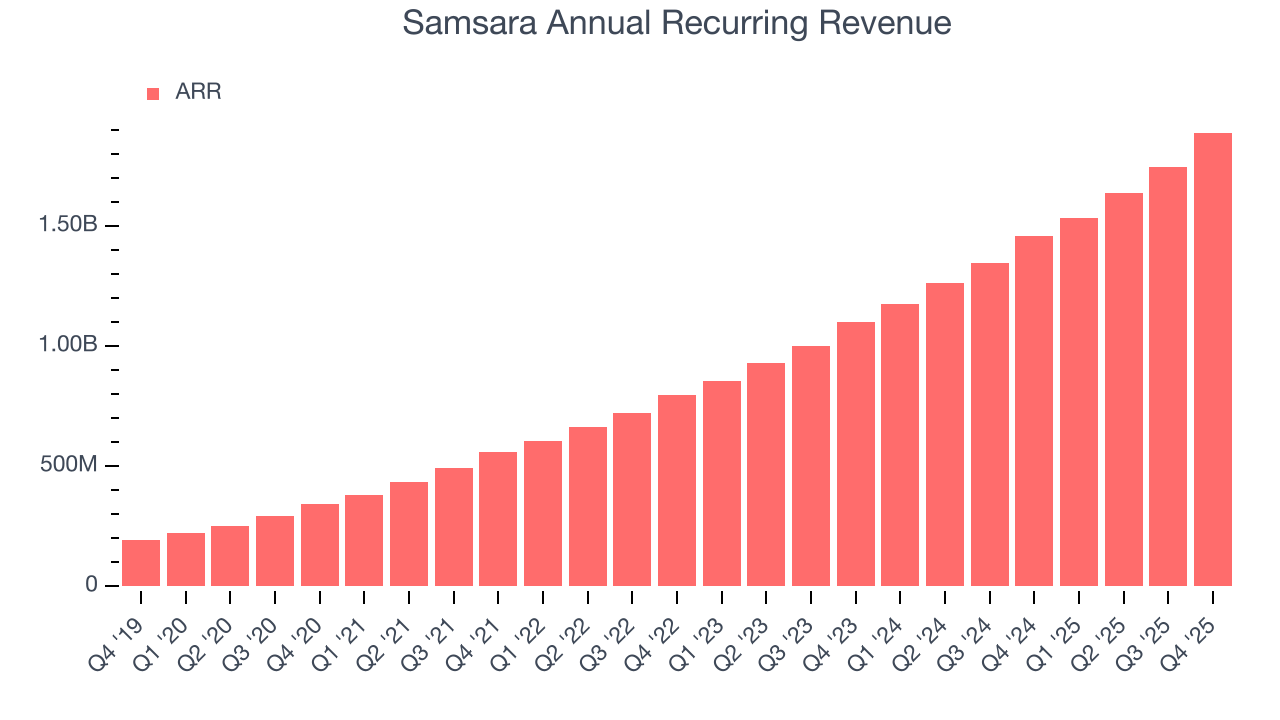

6. Annual Recurring Revenue

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

Samsara’s ARR punched in at $1.89 billion in Q4, and over the last four quarters, its growth was fantastic as it averaged 29.8% year-on-year increases. This performance aligned with its total sales growth and shows that customers are willing to take multi-year bets on the company’s technology. Its growth also makes Samsara a more predictable business, a tailwind for its valuation as investors typically prefer businesses with recurring revenue.

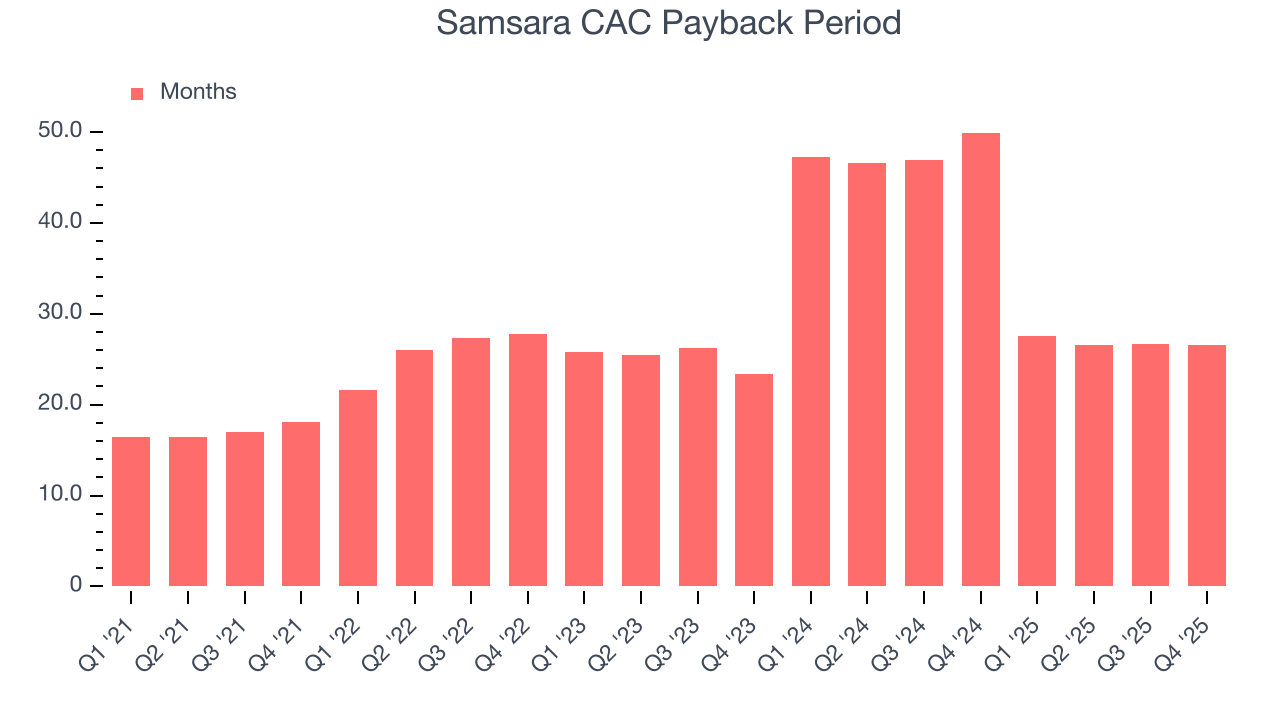

7. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

Samsara is very efficient at acquiring new customers, and its CAC payback period checked in at 26.5 months this quarter. The company’s rapid recovery of its customer acquisition costs indicates it has a highly differentiated product offering and a strong brand reputation. These dynamics give Samsara more resources to pursue new product initiatives while maintaining the flexibility to increase its sales and marketing investments.

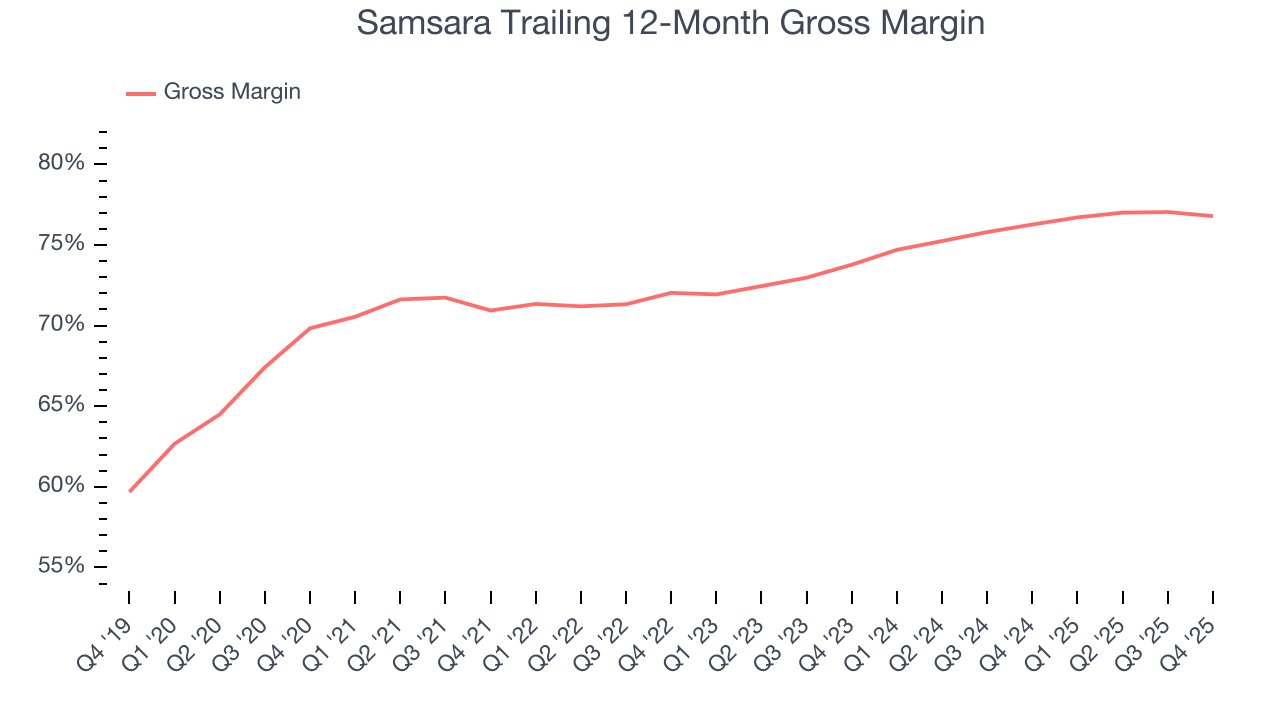

8. Gross Margin & Pricing Power

What makes the software-as-a-service model so attractive is that once the software is developed, it usually doesn’t cost much to provide it as an ongoing service. These minimal costs can include servers, licenses, and certain personnel.

Samsara’s gross margin is good for a software business and points to its solid unit economics, competitive products and services, and lack of meaningful pricing pressure. As you can see below, it averaged an impressive 76.8% gross margin over the last year. That means for every $100 in revenue, roughly $76.79 was left to spend on selling, marketing, and R&D.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. Samsara has seen gross margins improve by 3 percentage points over the last 2 year, which is very good in the software space.

In Q4, Samsara produced a 76.2% gross profit margin, in line with the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs have been stable and it isn’t under pressure to lower prices.

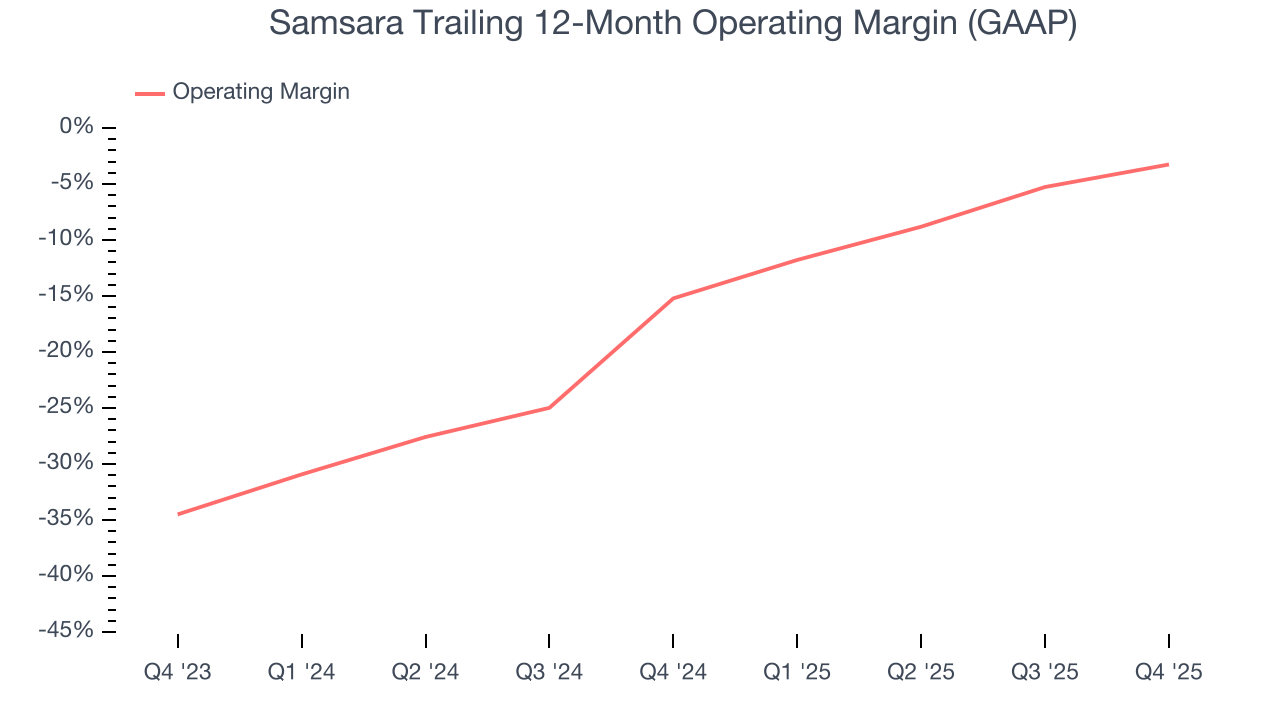

9. Operating Margin

Although Samsara was profitable this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 3.2% over the last year. Unprofitable, high-growth software companies require extra attention because they spend heaps of money to capture market share. This happened because the company spent loads of money to capture market share. As seen in its fast revenue growth, the aggressive strategy has paid off so far, and Wall Street’s estimates suggest the party will continue. We tend to agree and believe the business has a good chance of reaching profitability upon scale.

Over the last two years, Samsara’s expanding sales gave it operating leverage as its margin rose by 12 percentage points. Still, it will take much more for the company to show consistent profitability.

In Q4, Samsara generated an operating margin profit margin of 2%, up 7.3 percentage points year on year. The increase was solid, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

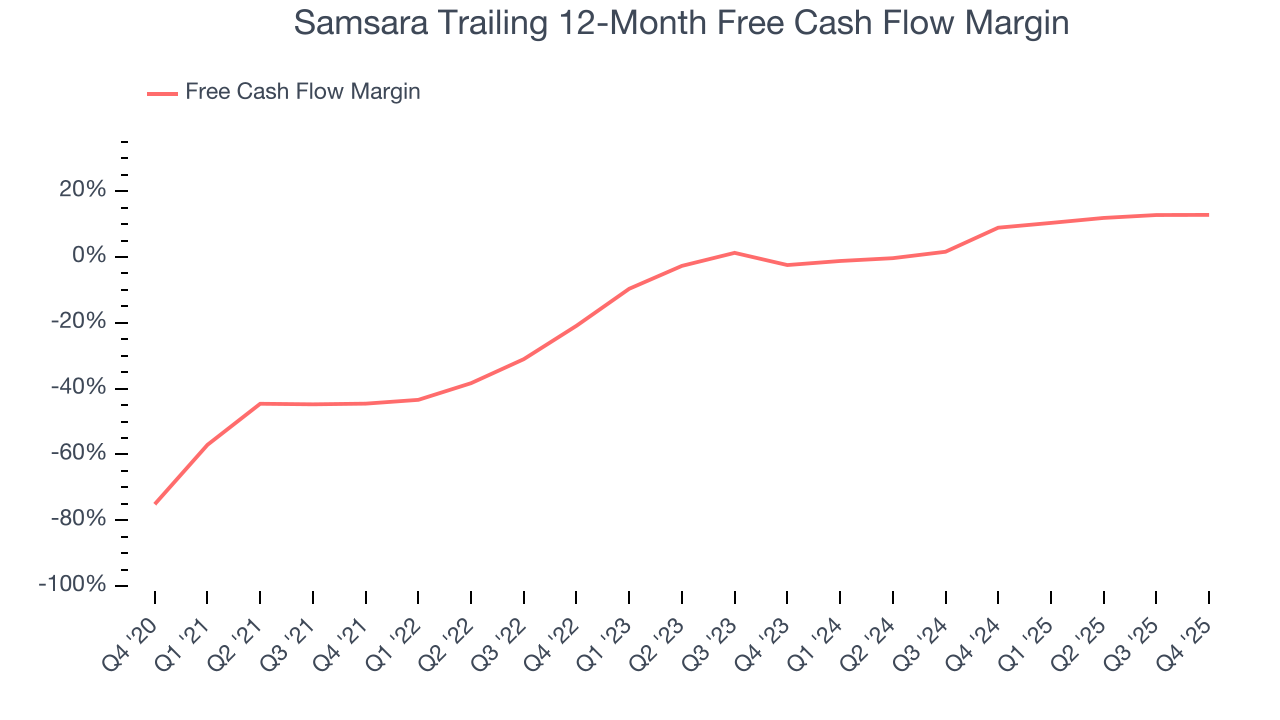

10. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Samsara has shown mediocre cash profitability relative to peers over the last year, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 12.8%, below what we’d expect for a software business.

Samsara’s free cash flow clocked in at $61.72 million in Q4, equivalent to a 13.9% margin. This cash profitability was in line with the comparable period last year and above its one-year average.

Over the next year, analysts’ consensus estimates show they’re expecting Samsara’s free cash flow margin of 12.8% for the last 12 months to remain the same.

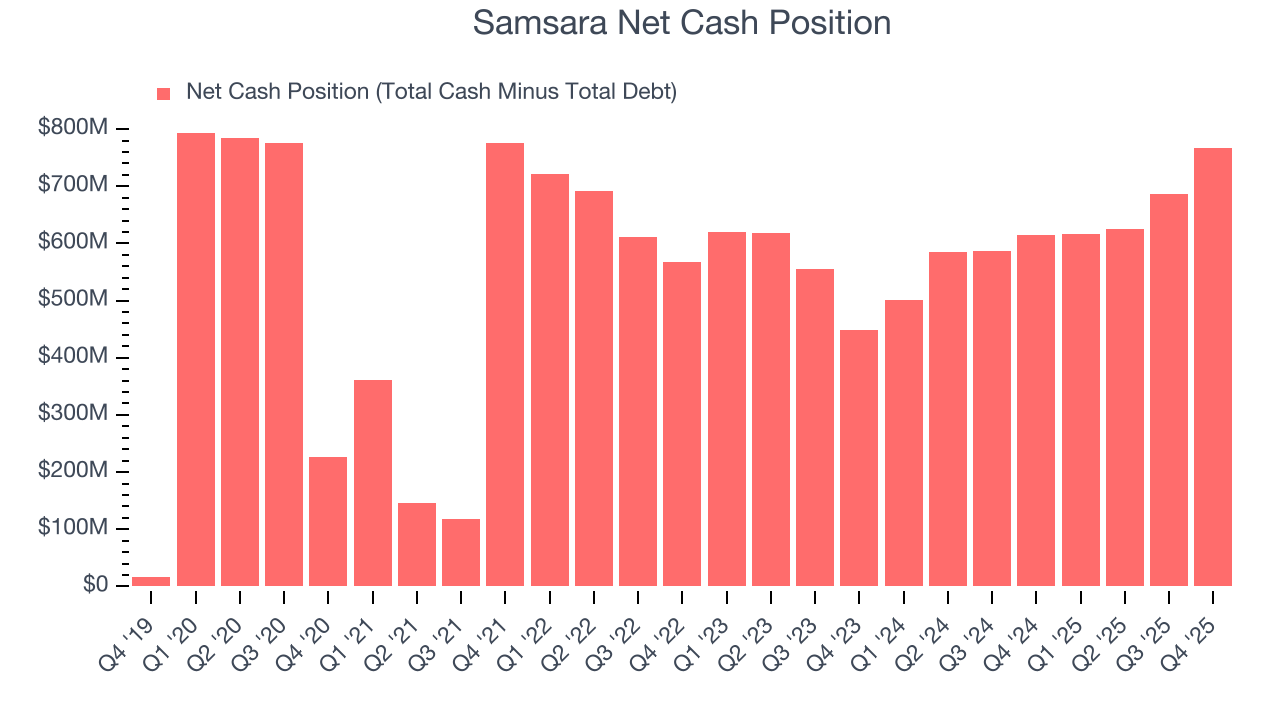

11. Balance Sheet Assessment

Companies with more cash than debt have lower bankruptcy risk.

Samsara is a well-capitalized company with $839.8 million of cash and $72.77 million of debt on its balance sheet. This $767.1 million net cash position is 4.6% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from Samsara’s Q4 Results

We were impressed by how significantly Samsara blew past analysts’ EBITDA expectations this quarter. We were also glad its full-year EPS guidance trumped Wall Street’s estimates. On the other hand, its billings missed and its revenue guidance for next year suggests growth will slow. Overall, we think this was still a solid quarter with some key areas of upside. The stock traded up 14.2% to $34.01 immediately after reporting.

13. Is Now The Time To Buy Samsara?

Updated: March 29, 2026 at 10:36 PM EDT

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

There is a lot to like about Samsara. For starters, its revenue growth was exceptional over the last five years. On top of that, its surging ARR shows its fundamentals and revenue predictability are improving, and its efficient sales strategy allows it to target and onboard new users at scale.

Samsara’s price-to-sales ratio based on the next 12 months is 9.5x. Scanning the software landscape today, Samsara’s fundamentals clearly illustrate that it’s an elite business, and we like it at this price.

Wall Street analysts have a consensus one-year price target of $44.17 on the company (compared to the current share price of $29.63), implying they see 49.1% upside in buying Samsara in the short term.