JBT Marel (JBTM)

We see potential in JBT Marel. Its impressive revenue growth indicates the value of its offerings.― StockStory Analyst Team

1. News

2. Summary

Why JBT Marel Is Interesting

Tracing back to its invention of the mechanical milk bottle filler in 1884, JBT Marel (NYSE:JBTM) designs, manufactures, and sells equipment used for food processing and aviation.

- Impressive 17.1% annual revenue growth over the last five years indicates it’s winning market share this cycle

- Sound unit economics and 34.9% gross margin allow for higher marketing and R&D budgets versus competitors

- A downside is its ROIC of 6.4% reflects management’s challenges in identifying attractive investment opportunities, and its falling returns suggest its earlier profit pools are drying up

JBT Marel has some noteworthy aspects. If you like the story, the valuation looks fair.

Why Is Now The Time To Buy JBT Marel?

JBT Marel is trading at $123.43 per share, or 15.8x forward P/E. This multiple is lower than the broader industrials space, and we think it’s fair given the revenue growth.

If you think the market is undervaluing the company, now could be a good time to build a position.

3. JBT Marel (JBTM) Research Report: Q4 CY2025 Update

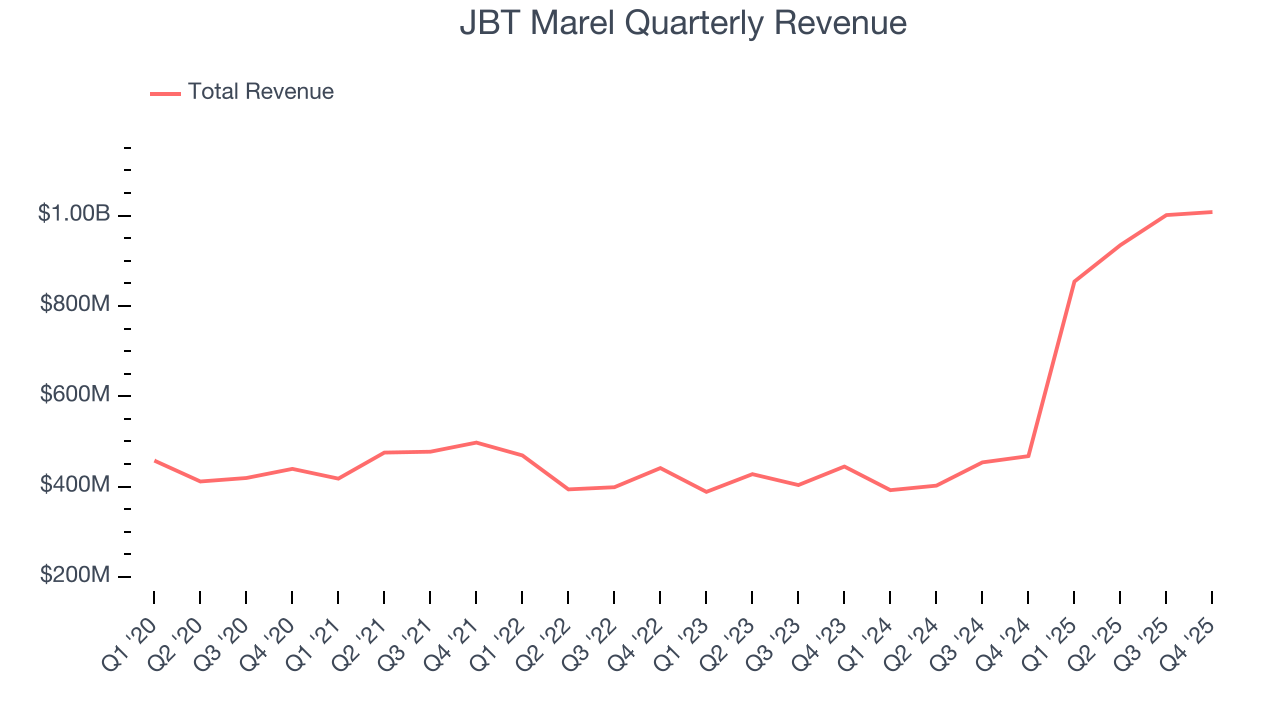

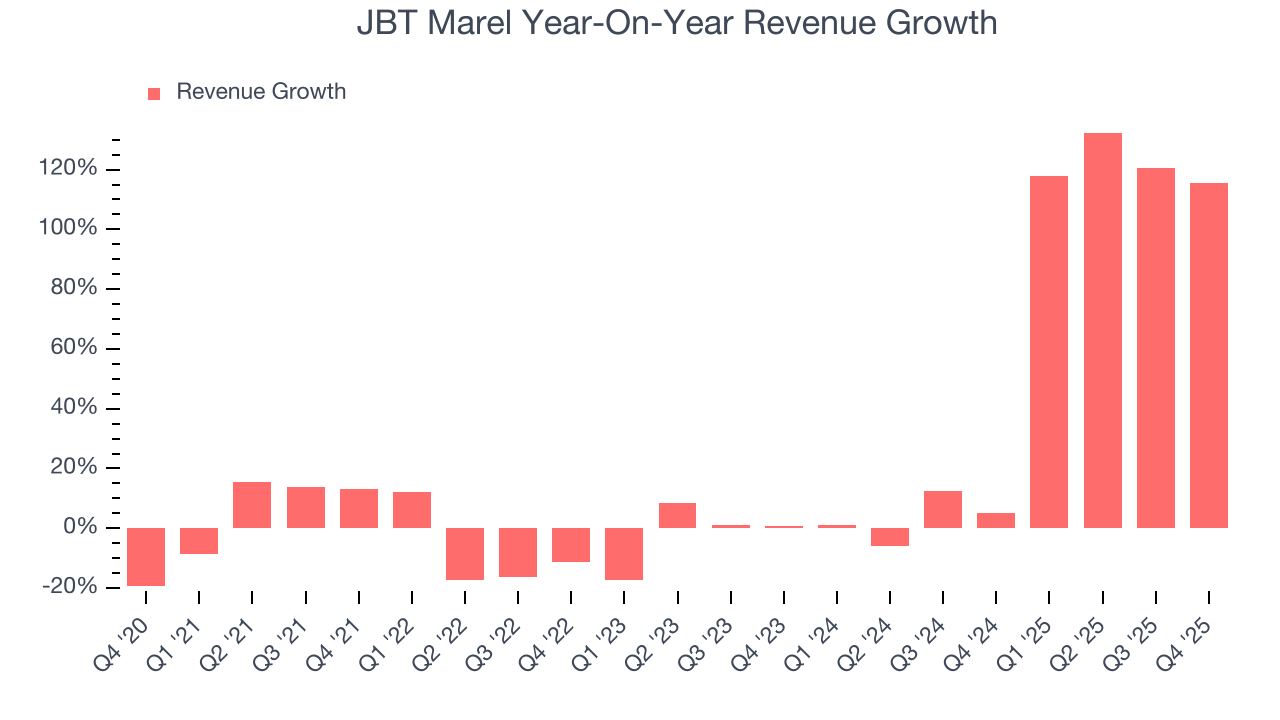

Food processing and aviation equipment manufacturer JBT Marel (NYSE:JBTM) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 116% year on year to $1.01 billion. The company’s full-year revenue guidance of $4.03 billion at the midpoint came in 1.8% above analysts’ estimates. Its non-GAAP profit of $1.98 per share was 2.7% above analysts’ consensus estimates.

JBT Marel (JBTM) Q4 CY2025 Highlights:

- Revenue: $1.01 billion vs analyst estimates of $996.9 million (116% year-on-year growth, 1.1% beat)

- Adjusted EPS: $1.98 vs analyst estimates of $1.93 (2.7% beat)

- Adjusted EBITDA: $161.1 million vs analyst estimates of $167.1 million (16% margin, 3.6% miss)

- Adjusted EPS guidance for the upcoming financial year 2026 is $8.25 at the midpoint, beating analyst estimates by 5.3%

- EBITDA guidance for the upcoming financial year 2026 is $692.5 million at the midpoint, above analyst estimates of $683.4 million

- Operating Margin: 7.2%, up from 3.4% in the same quarter last year

- Free Cash Flow Margin: 8.6%, down from 25.7% in the same quarter last year

- Market Capitalization: $7.94 billion

Company Overview

Tracing back to its invention of the mechanical milk bottle filler in 1884, JBT Marel (NYSE:JBTM) designs, manufactures, and sells equipment used for food processing and aviation.

JBT Marel (JBTM) originated from the Bean Spray Pump Company, founded in 1884. Initially producing piston pumps for orchard insecticide applications, the company evolved significantly over the decades. In 1928, it was renamed Food Machinery Corporation (FMC) after acquiring Anderson-Barngrover and Sprague-Sells. FMC expanded into various industries, including aerospace, where it developed technologies for airport ground support. However, in 2023, JBT decided to sell its AeroTech segment as part of its strategic shift to focus entirely on becoming a pure-play provider of food and beverage solutions.

The company provides integrated solutions for the food industry, offering equipment for every stage of the food processing cycle. From primary processing, such as poultry overhead and conveyance systems, to further processing technologies like high-capacity industrial cookers and freezers, JBT supports the production of a variety of food products.

The company’s equipment portfolio extends to automated systems, including robotic automated guided vehicle systems used in various industries for material movement, enhancing operational efficiency and productivity. JBT's automated systems are utilized in industries such as automotive and food and beverage, where precision and reliability are critical. These systems are designed to optimize material handling, reduce labor costs, and improve workplace safety, making them essential in modern manufacturing and warehousing operations.

JBT Marel also generates significant recurring revenue through aftermarket services, which include parts supply, maintenance, and rebuild services for customer-owned equipment. An example of its aftermarket offerings is the OmniBlu™ digital solution, a subscription service that combines service, parts availability, and machine optimization, powered by AI and machine learning. This focus on providing continuous and proactive service strengthens JBT's revenue streams, providing steady income and improved customer retention.

4. General Industrial Machinery

Automation that increases efficiency and connected equipment that collects analyzable data have been trending, creating new demand for general industrial machinery companies. Those who innovate and create digitized solutions can spur sales and speed up replacement cycles, but all general industrial machinery companies are still at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

Competitors offering similar products include Middleby (NASDAQ:MIDD), Illinois Tool Works (NYSE:ITW), and Colfax (NYSE:CFX).

5. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Thankfully, JBT Marel’s 17.1% annualized revenue growth over the last five years was incredible. Its growth beat the average industrials company and shows its offerings resonate with customers, a helpful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. JBT Marel’s annualized revenue growth of 51.1% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, JBT Marel reported magnificent year-on-year revenue growth of 116%, and its $1.01 billion of revenue beat Wall Street’s estimates by 1.1%.

Looking ahead, sell-side analysts expect revenue to grow 5.9% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and indicates its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

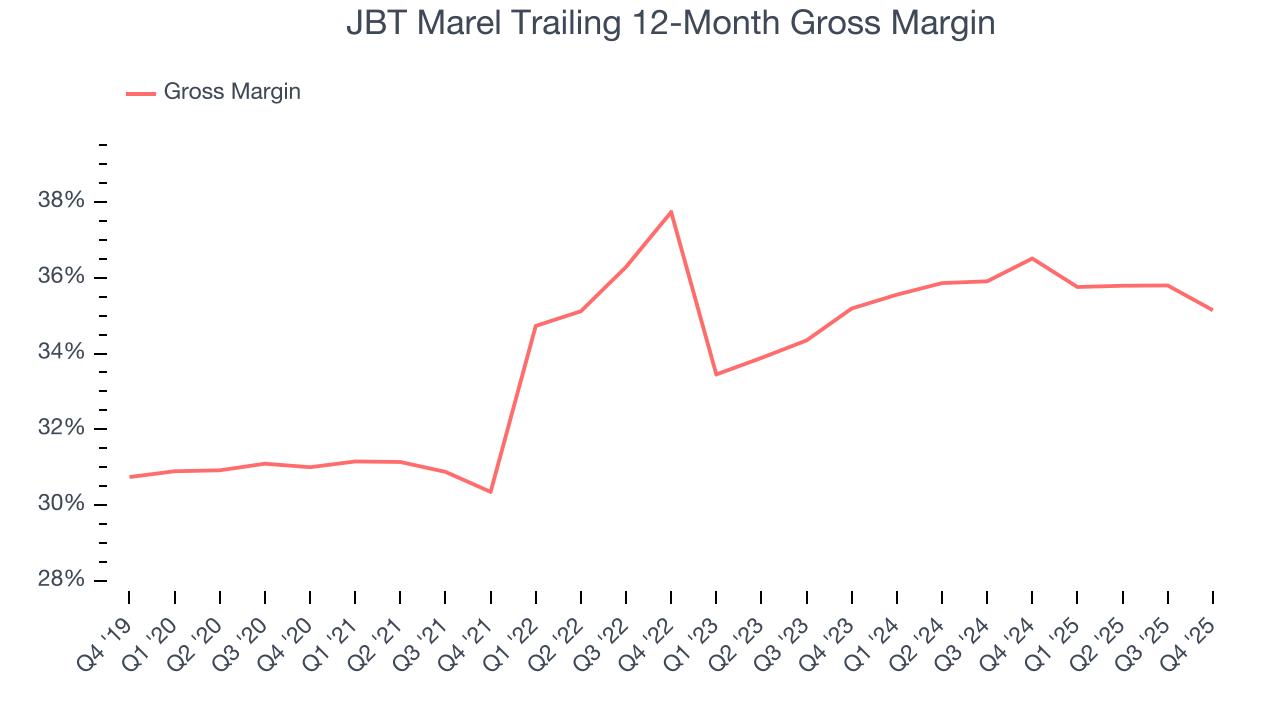

6. Gross Margin & Pricing Power

For industrials businesses, cost of sales is usually comprised of the direct labor, raw materials, and supplies needed to offer a product or service. These costs can be impacted by inflation and supply chain dynamics in the short term and a company’s purchasing power and scale over the long term.

JBT Marel’s gross margin is good compared to other industrials businesses and signals it sells differentiated products, not commodities. As you can see below, it averaged an impressive 34.9% gross margin over the last five years. That means for every $100 in revenue, roughly $34.95 was left to spend on selling, marketing, R&D, and general administrative overhead.

In Q4, JBT Marel produced a 34.5% gross profit margin , marking a 3.8 percentage point decrease from 38.4% in the same quarter last year. JBT Marel’s full-year margin has also been trending down over the past 12 months, decreasing by 1.4 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to lower prices and higher input costs (such as raw materials and manufacturing expenses).

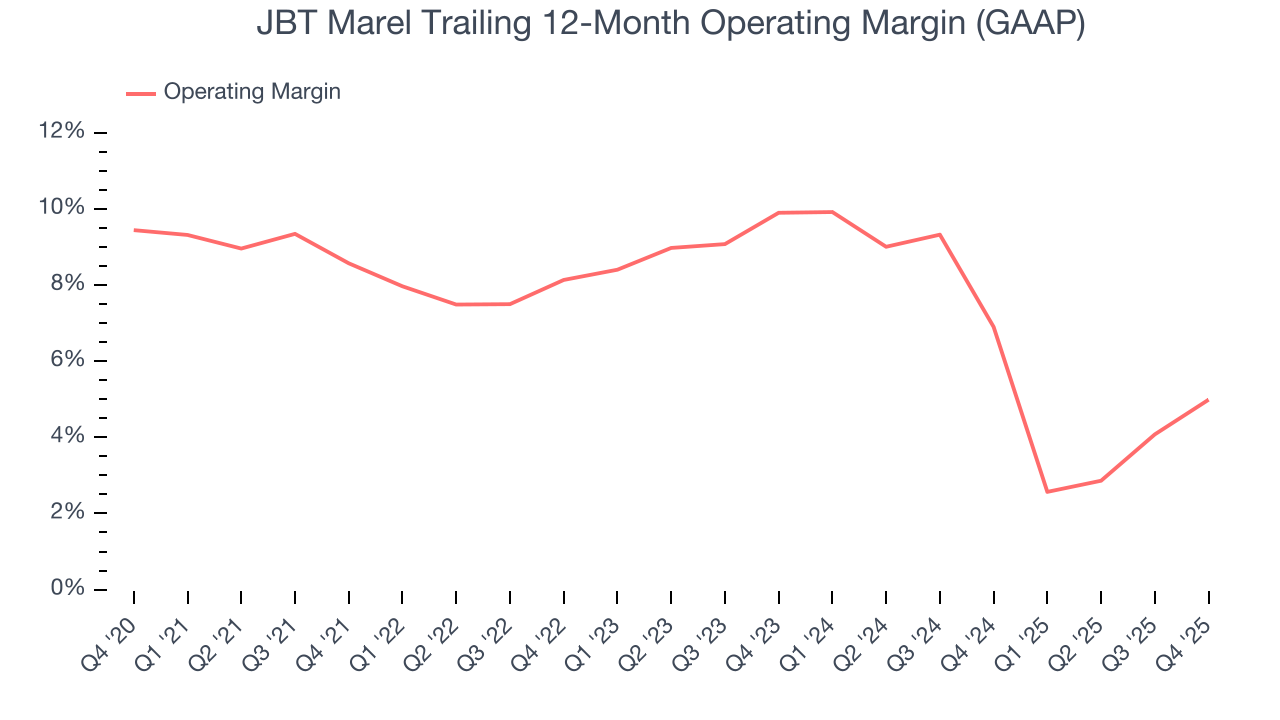

7. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

JBT Marel was profitable over the last five years but held back by its large cost base. Its average operating margin of 7.2% was weak for an industrials business. This result is surprising given its high gross margin as a starting point.

Looking at the trend in its profitability, JBT Marel’s operating margin decreased by 3.6 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. JBT Marel’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, JBT Marel generated an operating margin profit margin of 7.2%, up 3.8 percentage points year on year. The increase was encouraging, and because its gross margin actually decreased, we can assume it was more efficient because its operating expenses like marketing, R&D, and administrative overhead grew slower than its revenue.

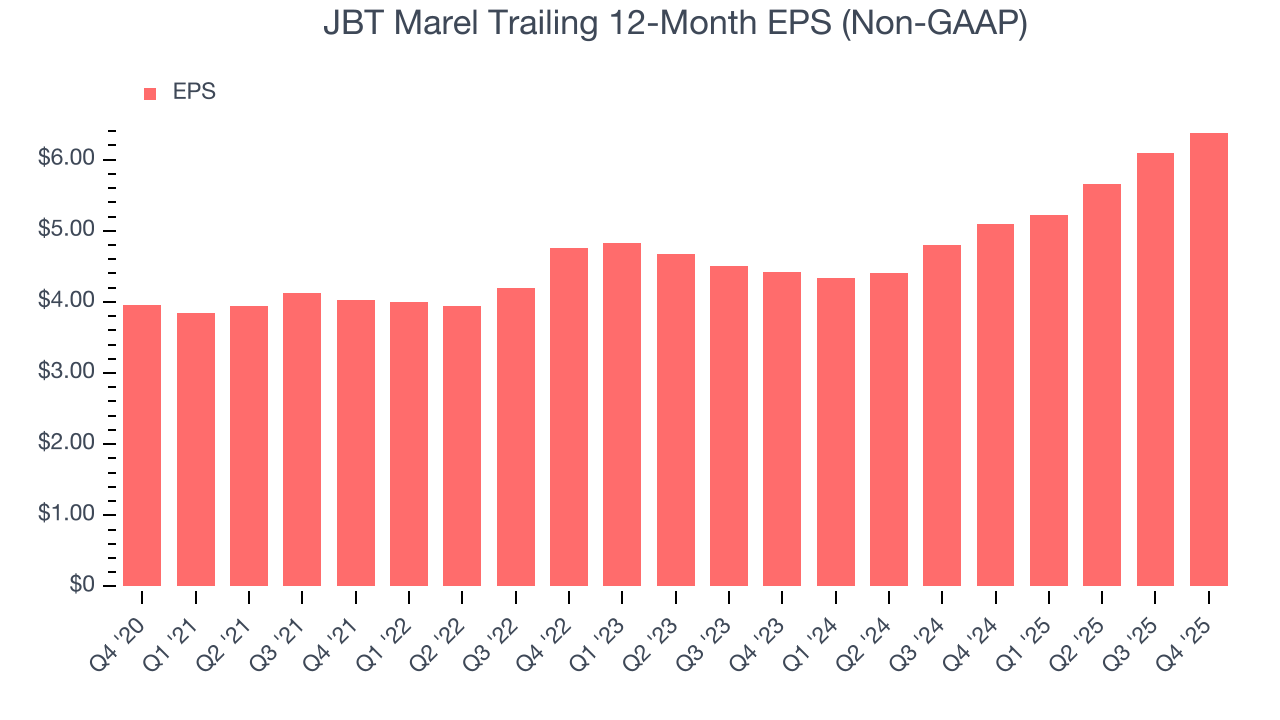

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

JBT Marel’s EPS grew at a solid 10.1% compounded annual growth rate over the last five years. However, this performance was lower than its 17.1% annualized revenue growth, telling us the company became less profitable on a per-share basis as it expanded.

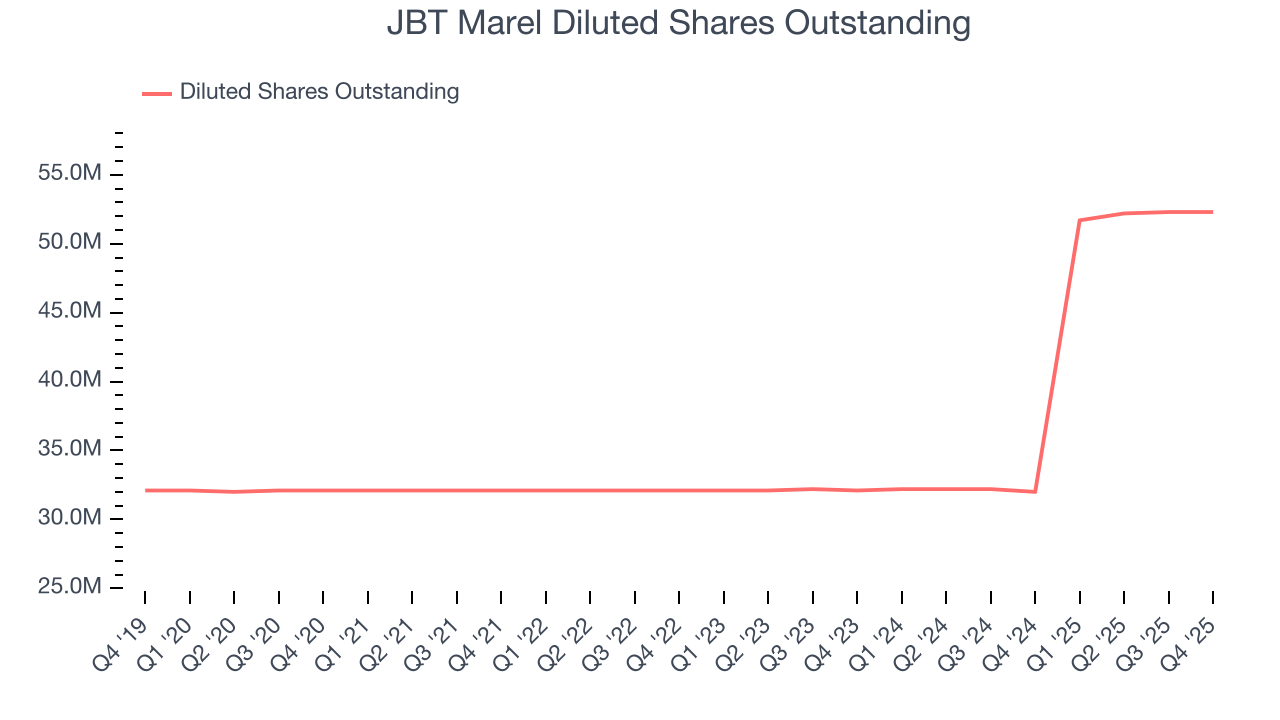

Diving into JBT Marel’s quality of earnings can give us a better understanding of its performance. As we mentioned earlier, JBT Marel’s operating margin expanded this quarter but declined by 3.6 percentage points over the last five years. Its share count also grew by 62.9%, meaning the company not only became less efficient with its operating expenses but also diluted its shareholders.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For JBT Marel, its two-year annual EPS growth of 20.1% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q4, JBT Marel reported adjusted EPS of $1.98, up from $1.70 in the same quarter last year. This print beat analysts’ estimates by 2.7%. Over the next 12 months, Wall Street expects JBT Marel’s full-year EPS of $6.38 to grow 29.9%.

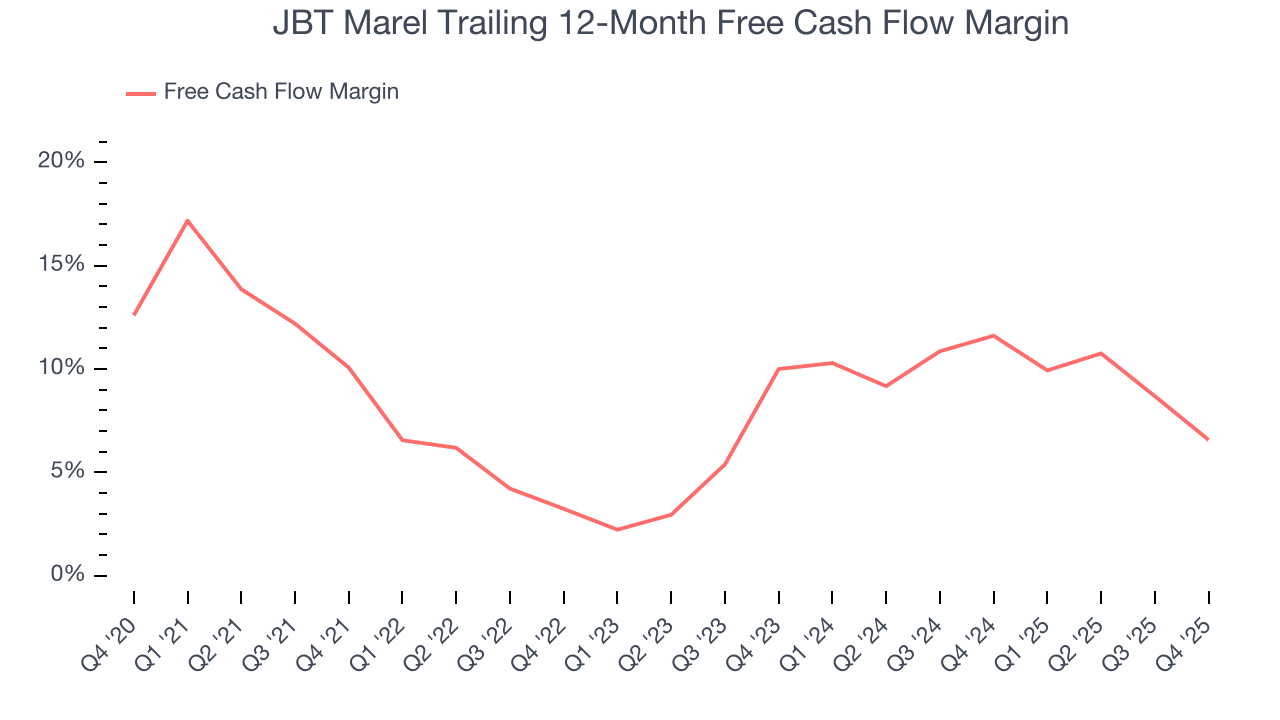

9. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

JBT Marel has shown impressive cash profitability, enabling it to ride out cyclical downturns more easily while maintaining its investments in new and existing offerings. The company’s free cash flow margin averaged 8% over the last five years, better than the broader industrials sector. JBT Marel has shown impressive cash profitability relative to peers over the last five years, giving the company fewer opportunities to return capital to shareholders. The divergence from its underwhelming operating margin stems from the add-back of non-cash charges like depreciation and stock-based compensation. GAAP operating profit expenses these line items, but free cash flow does not.

Taking a step back, we can see that JBT Marel’s margin dropped by 3.5 percentage points during that time. Continued declines could signal it is in the middle of an investment cycle.

JBT Marel’s free cash flow clocked in at $86.8 million in Q4, equivalent to a 8.6% margin. The company’s cash profitability regressed as it was 17.1 percentage points lower than in the same quarter last year, which isn’t ideal considering its longer-term trend.

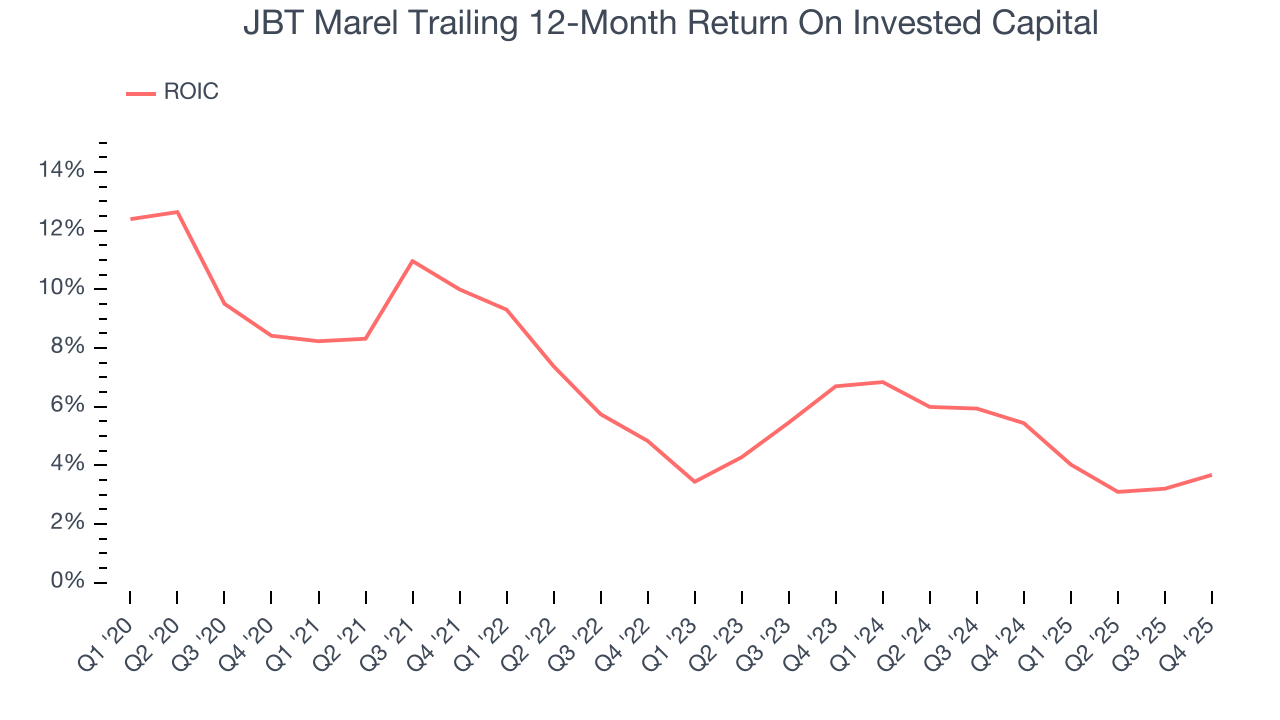

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Although JBT Marel has shown solid fundamentals lately, it historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 6.1%, somewhat low compared to the best industrials companies that consistently pump out 20%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. On average, JBT Marel’s ROIC decreased by 2.9 percentage points annually each year over the last few years. If its returns keep falling, it could suggest its profitable growth opportunities are drying up. We’ll keep a close eye.

11. Balance Sheet Assessment

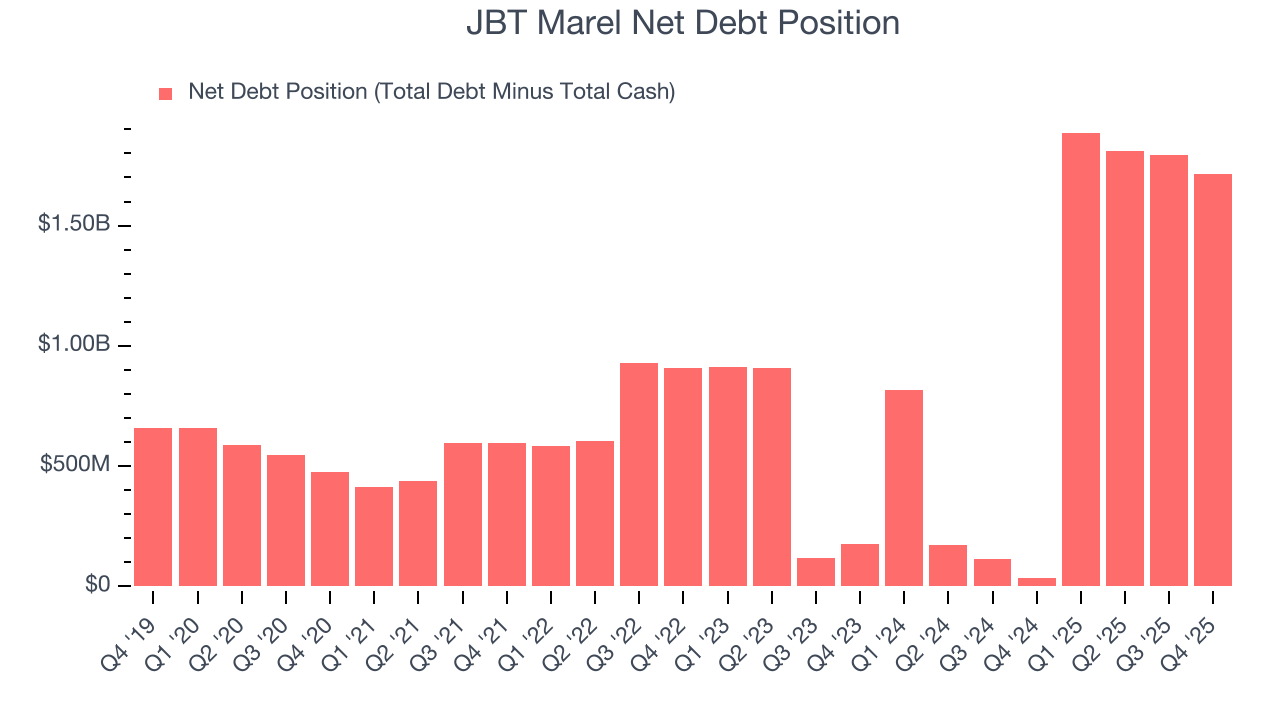

JBT Marel reported $167.9 million of cash and $1.88 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $600.4 million of EBITDA over the last 12 months, we view JBT Marel’s 2.9× net-debt-to-EBITDA ratio as safe. We also see its $103.3 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from JBT Marel’s Q4 Results

It was great to see JBT Marel’s full-year revenue guidance top analysts’ expectations. We were also glad its full-year EBITDA guidance slightly exceeded Wall Street’s estimates. On the other hand, its adjusted operating income missed and its EBITDA fell short of Wall Street’s estimates. Zooming out, we think this was a mixed quarter. The stock remained flat at $151.99 immediately after reporting.

13. Is Now The Time To Buy JBT Marel?

Updated: March 28, 2026 at 11:51 PM EDT

Are you wondering whether to buy JBT Marel or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

JBT Marel possesses a number of positive attributes. First off, its revenue growth was exceptional over the last five years. And while its diminishing returns show management's recent bets still have yet to bear fruit, its projected EPS for the next year implies the company’s fundamentals will improve. On top of that, its gross margins indicate healthy unit economics.

JBT Marel’s P/E ratio based on the next 12 months is 15.8x. When scanning the industrials space, JBT Marel trades at a fair valuation. If you believe in the company and its growth potential, now is an opportune time to buy shares.

Wall Street analysts have a consensus one-year price target of $182.08 on the company (compared to the current share price of $123.43), implying they see 47.5% upside in buying JBT Marel in the short term.