Kforce (KFRC)

We wouldn’t recommend Kforce. Not only is its demand weak but also its falling returns on capital suggest it’s becoming less profitable.― StockStory Analyst Team

1. News

2. Summary

Why We Think Kforce Will Underperform

With nearly 60 years of matching skilled professionals with the right opportunities, Kforce (NYSE:KFRC) is a professional staffing company that specializes in placing technology and finance experts with businesses on both temporary and permanent bases.

- Products and services are facing significant end-market challenges during this cycle as sales have declined by 1% annually over the last five years

- Sales were less profitable over the last five years as its earnings per share fell by 5.7% annually, worse than its revenue declines

- Demand will likely be weak over the next 12 months as Wall Street expects flat revenue

Kforce is in the doghouse. There are more profitable opportunities elsewhere.

Why There Are Better Opportunities Than Kforce

At $26.12 per share, Kforce trades at 11.7x forward P/E. This multiple is lower than most business services companies, but for good reason.

We’d rather pay up for companies with elite fundamentals than get a bargain on weak ones. Cheap stocks can be value traps, and as their performance deteriorates, they will stay cheap or get even cheaper.

3. Kforce (KFRC) Research Report: Q4 CY2025 Update

Professional staffing firm Kforce (NYSE:KFRC) reported Q4 CY2025 results exceeding the market’s revenue expectations, but sales fell by 3.4% year on year to $332 million. Guidance for next quarter’s revenue was better than expected at $328 million at the midpoint, 2% above analysts’ estimates. Its GAAP profit of $0.30 per share was 35.6% below analysts’ consensus estimates.

Kforce (KFRC) Q4 CY2025 Highlights:

- Revenue: $332 million vs analyst estimates of $329.3 million (3.4% year-on-year decline, 0.8% beat)

- EPS (GAAP): $0.30 vs analyst expectations of $0.47 (35.6% miss)

- Adjusted EBITDA: $16.75 million vs analyst estimates of $17.93 million (5% margin, 6.6% miss)

- Revenue Guidance for Q1 CY2026 is $328 million at the midpoint, above analyst estimates of $321.7 million

- EPS (GAAP) guidance for Q1 CY2026 is $0.41 at the midpoint, beating analyst estimates by 1.7%

- Operating Margin: 2.6%, down from 4.5% in the same quarter last year

- Free Cash Flow Margin: 1.5%, down from 6.6% in the same quarter last year

- Market Capitalization: $609.2 million

Company Overview

With nearly 60 years of matching skilled professionals with the right opportunities, Kforce (NYSE:KFRC) is a professional staffing company that specializes in placing technology and finance experts with businesses on both temporary and permanent bases.

Kforce operates primarily through two business segments: Technology, which generates about 90% of revenue, and Finance and Accounting (FA). The company's Technology segment provides skilled professionals in areas such as systems architecture, data analytics, cloud engineering, artificial intelligence, project management, and network security. Meanwhile, the FA segment offers talent in roles like financial planning and analysis, accounting, business intelligence, and taxation.

The company serves clients across diverse industries, with particular focus on Fortune 500 companies. Kforce's business model extends beyond traditional staffing to include managed teams and project-based solutions, allowing clients to scale their workforce according to specific needs. For example, a financial services company might engage Kforce to provide a team of data analysts for a six-month digital transformation project, or a healthcare organization might hire a cloud architect through Kforce to redesign their patient data systems.

Most consultants placed by Kforce are directly employed by the company, which handles payroll taxes, unemployment taxes, workers' compensation, and benefits including health insurance and retirement plans. This employment structure allows Kforce to maintain quality control while providing consultants with stability between assignments.

Kforce generates revenue by charging clients a premium on the hourly rates paid to consultants for temporary assignments, or by collecting placement fees for permanent hires. The company has been evolving its service delivery model to include nearshore and offshore capabilities, allowing it to offer competitive pricing while maintaining service quality.

As part of its growth strategy, Kforce is investing in back-office transformation and integrating new technologies, particularly artificial intelligence, through partnerships with technology leaders like Workday and Microsoft.

4. Professional Staffing & HR Solutions

The Professional Staffing & HR Solutions subsector within Business Services is set to benefit from evolving workforce trends, including the rise of remote work and the gig economy. With companies casting a wider net to find talent due to remote work, the expertise of staffing and recruiting companies is even more valuable. For those who invest wisely, the use of predictive AI in recruitment and screening as well as automation in HR workflows can enhance efficiency and scalability. On the other hand, digitization means that talent discovery is less of a manual process, opening the door for tech-first platforms. Additionally, regulatory scrutiny around data privacy in HR is evolving and may require companies in this sector to change their go-to-market strategies over time.

Kforce competes with other professional staffing firms including Robert Half (NYSE:RHI), ManpowerGroup (NYSE:MAN), and Randstad (OTC:RANJY), as well as specialized technology staffing companies like TEKsystems (private) and Insight Global (private).

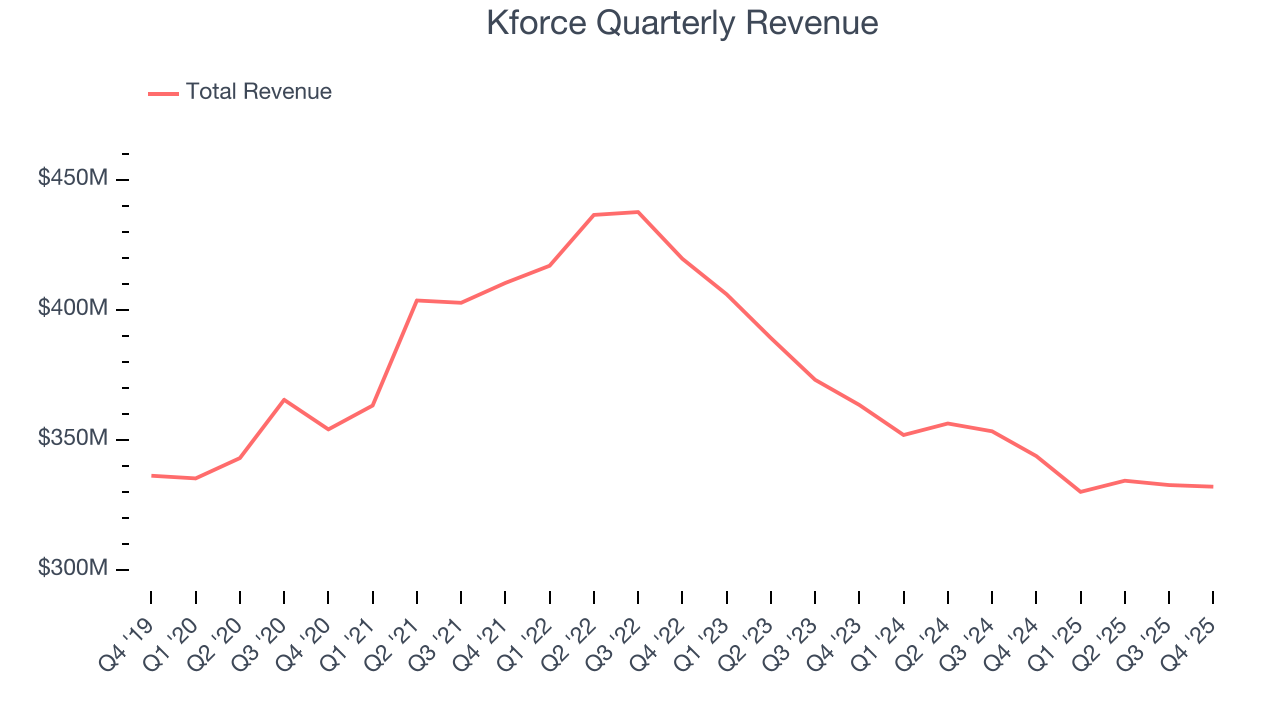

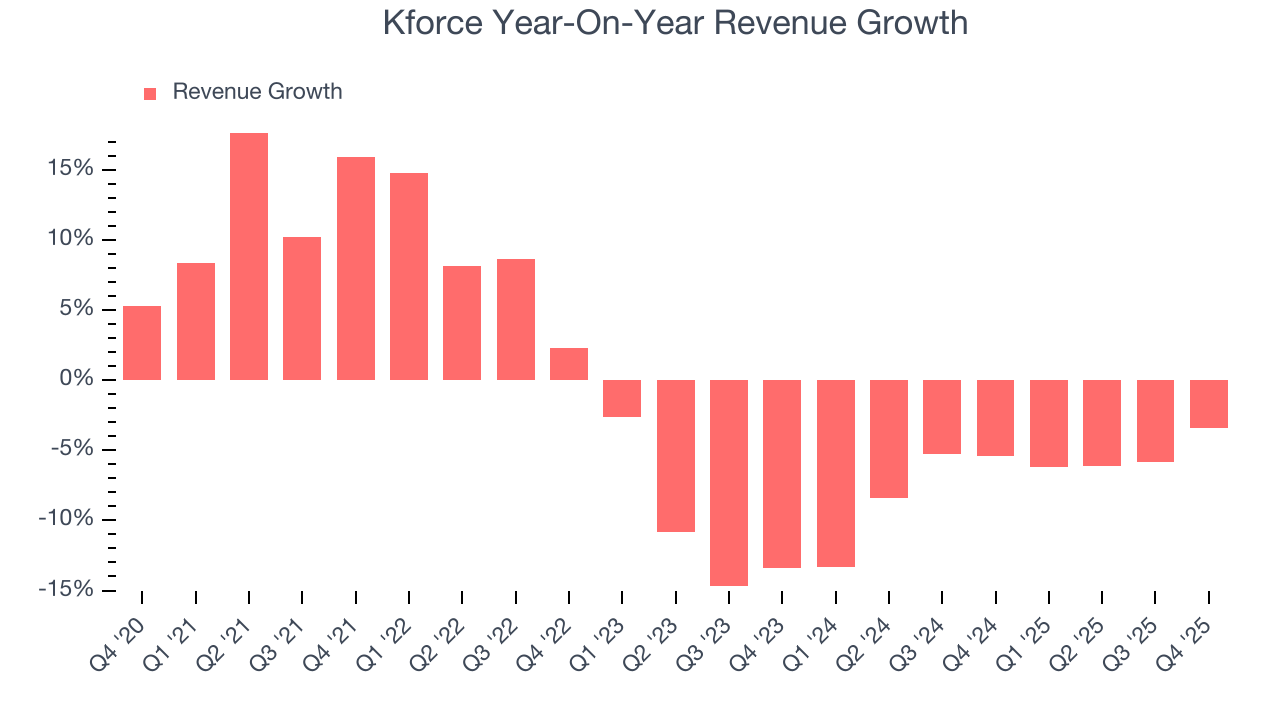

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $1.33 billion in revenue over the past 12 months, Kforce is a mid-sized business services company, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale.

As you can see below, Kforce’s demand was weak over the last five years. Its sales fell by 1% annually, a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Kforce’s recent performance shows its demand remained suppressed as its revenue has declined by 6.9% annually over the last two years.

This quarter, Kforce’s revenue fell by 3.4% year on year to $332 million but beat Wall Street’s estimates by 0.8%. Company management is currently guiding for flat sales next quarter.

Looking further ahead, sell-side analysts expect revenue to remain flat over the next 12 months. While this projection suggests its newer products and services will fuel better top-line performance, it is still below the sector average.

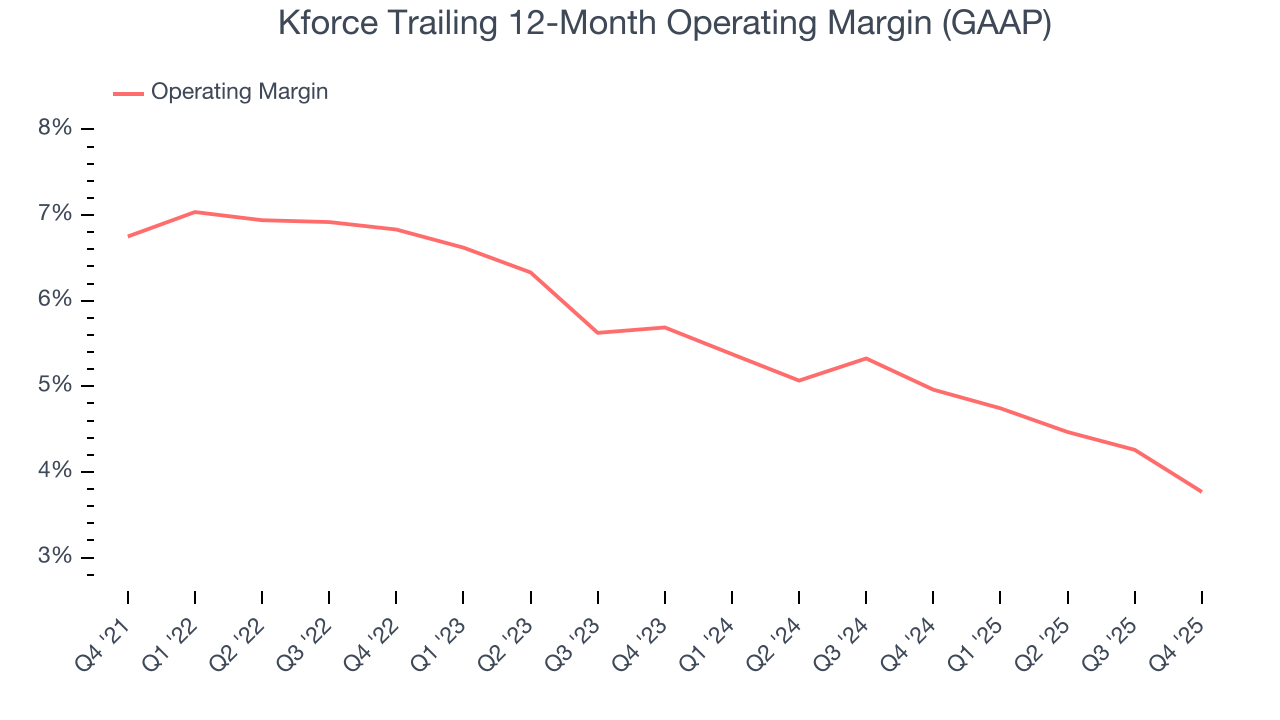

6. Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D.

Kforce was profitable over the last five years but held back by its large cost base. Its average operating margin of 5.7% was weak for a business services business.

Analyzing the trend in its profitability, Kforce’s operating margin decreased by 3 percentage points over the last five years. Kforce’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, Kforce generated an operating margin profit margin of 2.6%, down 2 percentage points year on year. This reduction is quite minuscule and indicates the company’s overall cost structure has been relatively stable.

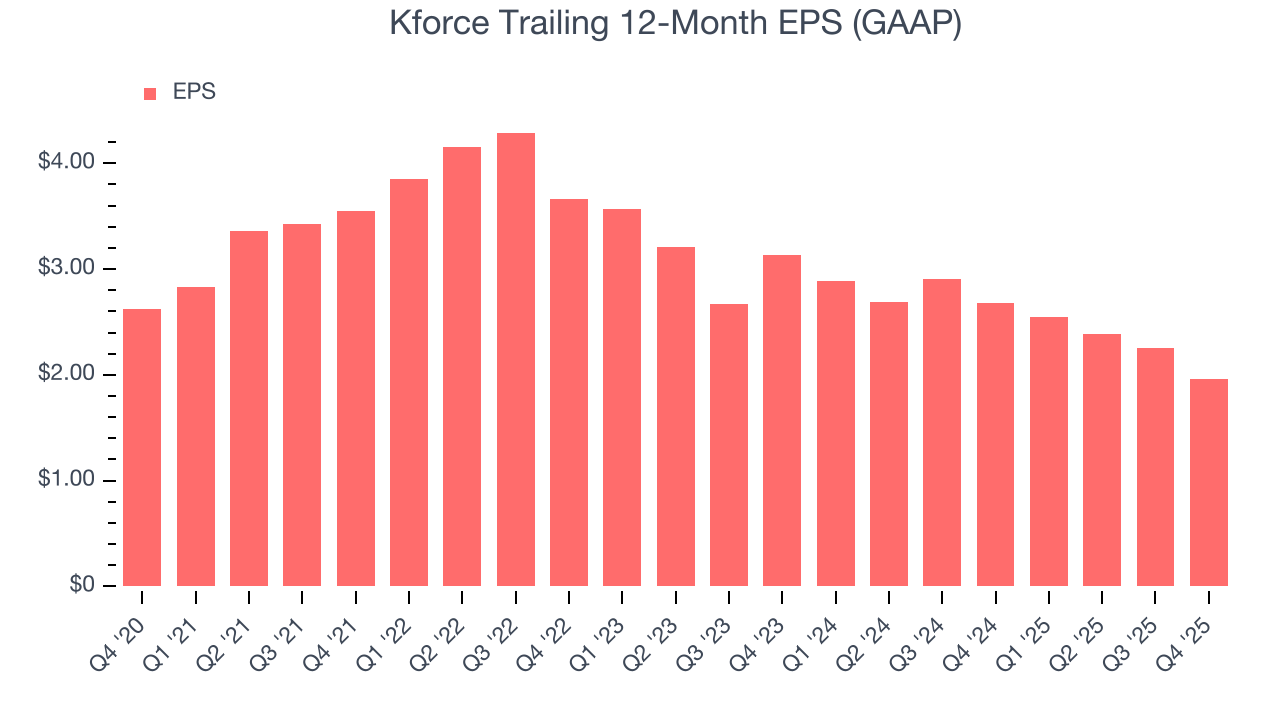

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Kforce, its EPS declined by 5.7% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

Diving into the nuances of Kforce’s earnings can give us a better understanding of its performance. As we mentioned earlier, Kforce’s operating margin declined by 3 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Kforce, its two-year annual EPS declines of 20.8% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q4, Kforce reported EPS of $0.30, down from $0.60 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Kforce’s full-year EPS of $1.96 to grow 17.7%.

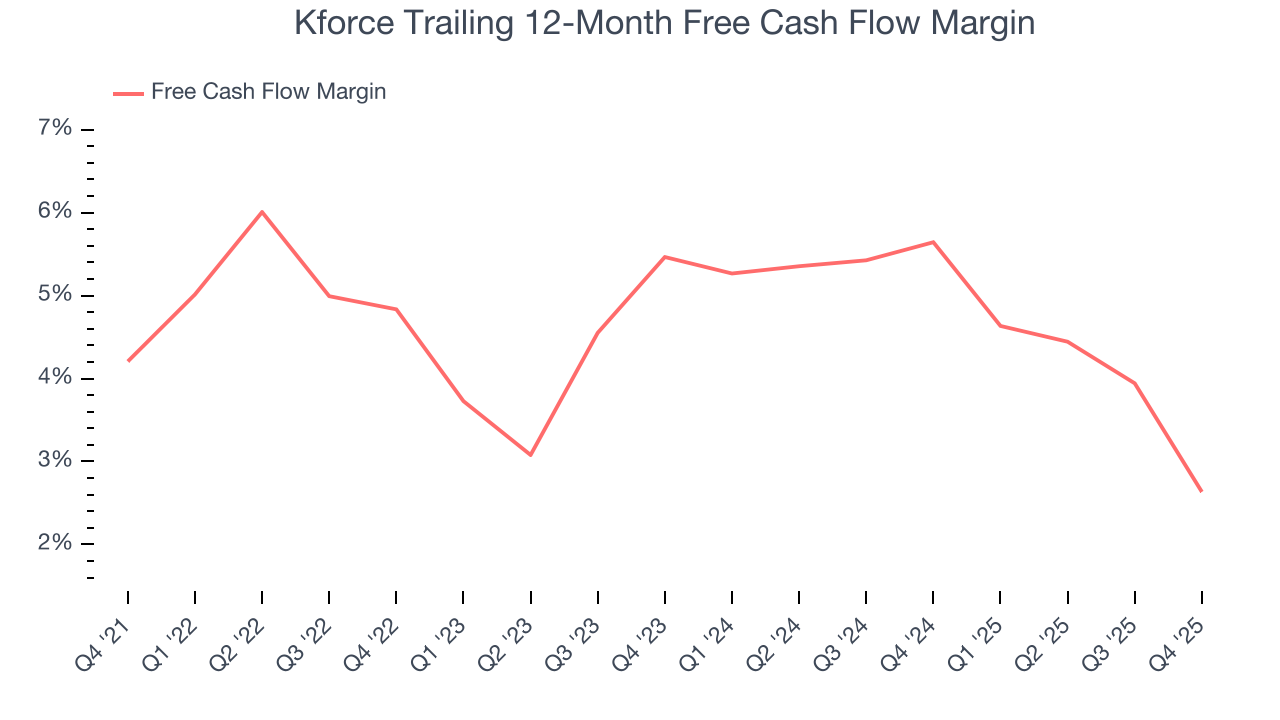

8. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Kforce has shown mediocre cash profitability over the last five years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 4.6%, subpar for a business services business.

Taking a step back, we can see that Kforce’s margin dropped by 1.6 percentage points during that time. This along with its unexciting margin put the company in a tough spot, and shareholders are likely hoping it can reverse course. If the trend continues, it could signal it’s in the middle of an investment cycle.

Kforce’s free cash flow clocked in at $4.87 million in Q4, equivalent to a 1.5% margin. The company’s cash profitability regressed as it was 5.1 percentage points lower than in the same quarter last year, suggesting its historical struggles have dragged on.

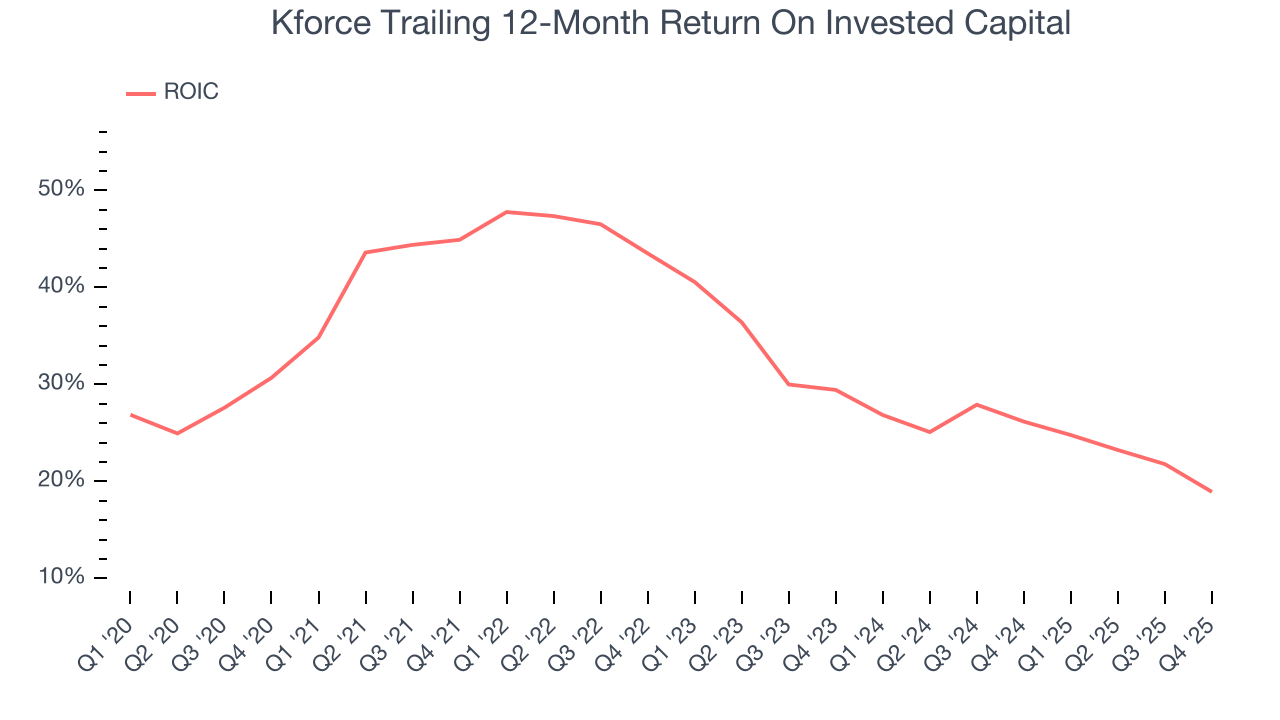

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Although Kforce hasn’t been the highest-quality company lately because of its poor revenue and EPS performance, it found a few growth initiatives in the past that worked out wonderfully. Its five-year average ROIC was 32.6%, splendid for a business services business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Kforce’s ROIC has decreased significantly over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

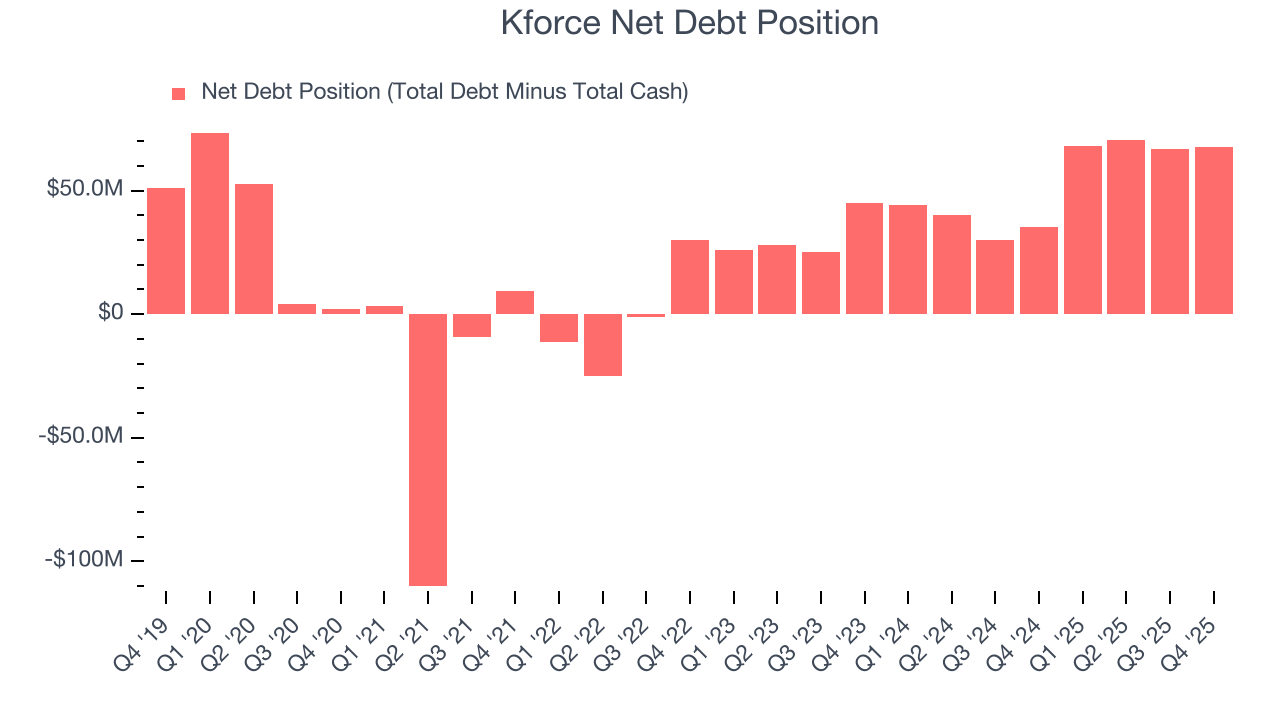

10. Balance Sheet Assessment

Kforce reported $2.14 million of cash and $69.74 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $72.79 million of EBITDA over the last 12 months, we view Kforce’s 0.9× net-debt-to-EBITDA ratio as safe. We also see its $1.56 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from Kforce’s Q4 Results

Revenue beat slightly, but EBITDA and EPS both missed meaningfully. While Q1 guidance was solid, it wasn't enough to overcome the EBITDA and EPS misses in the quarter. Zooming out, we think this was a mixed quarter. Investors were likely hoping for more, and shares traded down 11.7% to $32.36 immediately following the results.

12. Is Now The Time To Buy Kforce?

Updated: March 17, 2026 at 12:35 AM EDT

When considering an investment in Kforce, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

Kforce doesn’t pass our quality test. For starters, its revenue has declined over the last five years. While its stellar ROIC suggests it has been a well-run company historically, the downside is its diminishing returns show management's prior bets haven't worked out. On top of that, its declining EPS over the last five years makes it a less attractive asset to the public markets.

Kforce’s P/E ratio based on the next 12 months is 11.7x. This valuation tells us a lot of optimism is priced in - we think there are better opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $39 on the company (compared to the current share price of $26.12).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.