Kohl's (KSS)

We wouldn’t recommend Kohl's. Its weak profitability and declining sales not only show demand is fading but also illustrate poor fundamentals.― StockStory Analyst Team

1. News

2. Summary

Why We Think Kohl's Will Underperform

Founded as a corner grocery store in Milwaukee, Wisconsin, Kohl’s (NYSE:KSS) is a department store chain that sells clothing, cosmetics, electronics, and home goods.

- Annual sales declines of 5% for the past three years show its products struggled to connect with the market

- Poor expense management has led to an operating margin that is below the industry average

- Sales are projected to tank by 1.2% over the next 12 months as its demand continues evaporating

Kohl's doesn’t pass our quality test. More profitable opportunities exist elsewhere.

Why There Are Better Opportunities Than Kohl's

Kohl's is trading at $13.18 per share, or 9.8x forward P/E. Kohl’s valuation may seem like a great deal, but we think there are valid reasons why it’s so cheap.

Cheap stocks can look like great bargains at first glance, but you often get what you pay for. These mediocre businesses often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. Kohl's (KSS) Research Report: Q4 CY2025 Update

Department store chain Kohl’s (NYSE:KSS) met Wall Street’s revenue expectations in Q4 CY2025, but sales fell by 4.2% year on year to $5.17 billion. Its non-GAAP profit of $1.07 per share was 26.7% above analysts’ consensus estimates.

Kohl's (KSS) Q4 CY2025 Highlights:

- Revenue: $5.17 billion vs analyst estimates of $5.18 billion (4.2% year-on-year decline, in line)

- Adjusted EPS: $1.07 vs analyst estimates of $0.84 (26.7% beat)

- Same-store sales guidance for the upcoming financial year 2026 is -1% at the midpoint, in line with analyst estimates

- Adjusted EPS guidance for the upcoming financial year 2026 is $1.30 at the midpoint, in line with analyst estimates

- Operating Margin: 4.1%, up from 2.3% in the same quarter last year

- Free Cash Flow Margin: 13.3%, up from 9.2% in the same quarter last year

- Same-Store Sales fell 2.8% year on year (-6.1% in the same quarter last year)

- Market Capitalization: $1.66 billion

Company Overview

Founded as a corner grocery store in Milwaukee, Wisconsin, Kohl’s (NYSE:KSS) is a department store chain that sells clothing, cosmetics, electronics, and home goods.

As the name suggests, a department store offers a wide variety of merchandise organized into different departments or sections. Before the introduction of department stores in the 19th century, consumers would have to visit three different stores to buy a pair of shoes, nail polish, and towels for the home.

Today, the core Kohl’s customer is a middle-income woman shopping for herself and for her family. This customer can find prominent brands such as Nike, Levi’s, Keurig, and Samsung in a typical Kohl’s store or on its e-commerce site. Stores tend to be between 80,000 and 100,000 square feet and located in strip shopping centers rather than the traditional suburban malls that many department stores anchor. Common departments in a Kohl’s store include women’s/men’s/children’s apparel, beauty/cosmetics, and electronics. Additionally, Kohl's has an e-commerce presence which was launched in 2001 and today enables both online orders to be shipped to a customer’s home as well as buy online for store pickup.

Since the introduction of e-commerce, Kohl’s and peers have faced increased competition. Evolving specialty retailers and developments such as fast fashion have also pressured the department store model.

4. Department Store

Department stores emerged in the 19th century to provide customers with a wide variety of merchandise under one roof, offering a convenient and luxurious shopping experience. They played an important role in the history of American retail and urbanization, and prior to department stores, retailers tended to sell narrow specialty and niche items. But what was once new is now old, and department stores are somewhat considered a relic of the past. They are being attacked from multiple angles–stagnant foot traffic at malls where they’ve served as anchors; more nimble off-price and fast-fashion retailers; and e-commerce-first competitors not burdened by large physical footprints.

Department or general merchandise retail competitors include Macy’s (NYSE:M), Nordstrom (NYSE:JWN), and Dillard’s (NYSE:DDS).

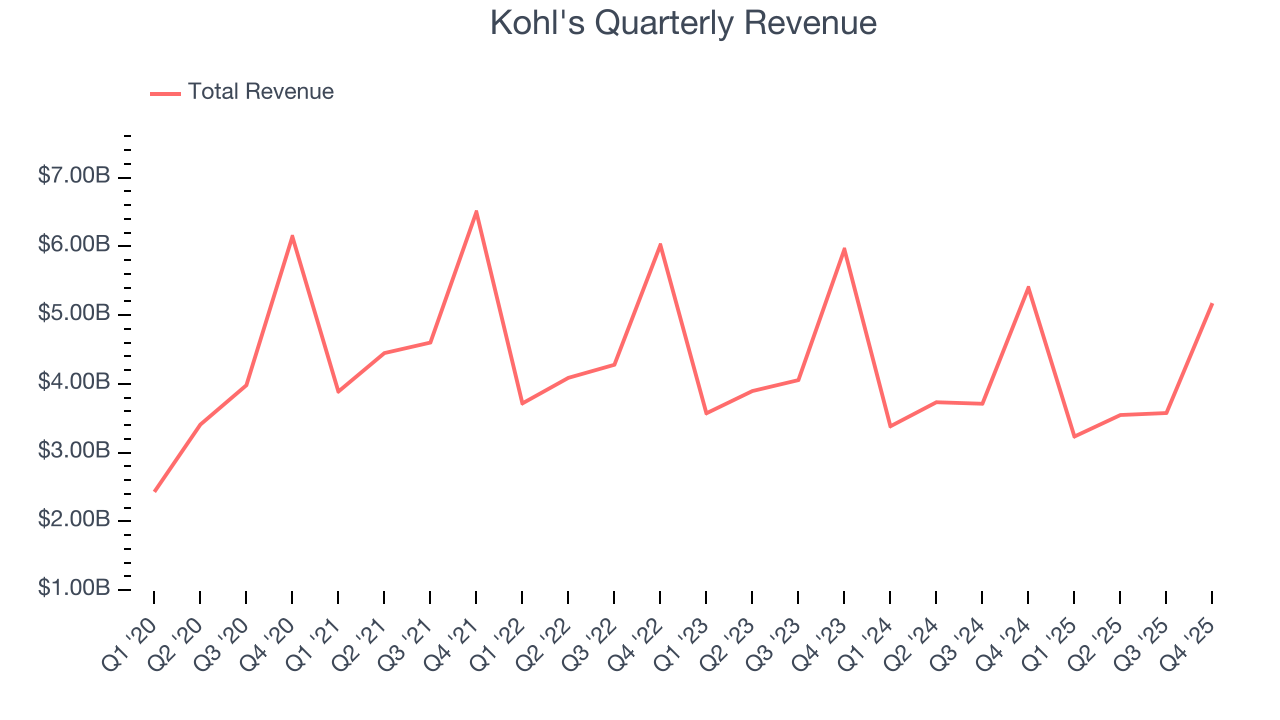

5. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $15.53 billion in revenue over the past 12 months, Kohl's is one of the larger companies in the consumer retail industry and benefits from a well-known brand that influences purchasing decisions. However, its scale is a double-edged sword because it’s harder to find incremental growth when you’ve penetrated most of the market. To expand meaningfully, Kohl's likely needs to tweak its prices or enter new markets.

As you can see below, Kohl’s revenue declined by 5% per year over the last three years as it didn’t open many new stores and observed lower sales at existing, established locations.

This quarter, Kohl's reported a rather uninspiring 4.2% year-on-year revenue decline to $5.17 billion of revenue, in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to decline by 1.2% over the next 12 months. it’s tough to feel optimistic about a company facing demand difficulties.

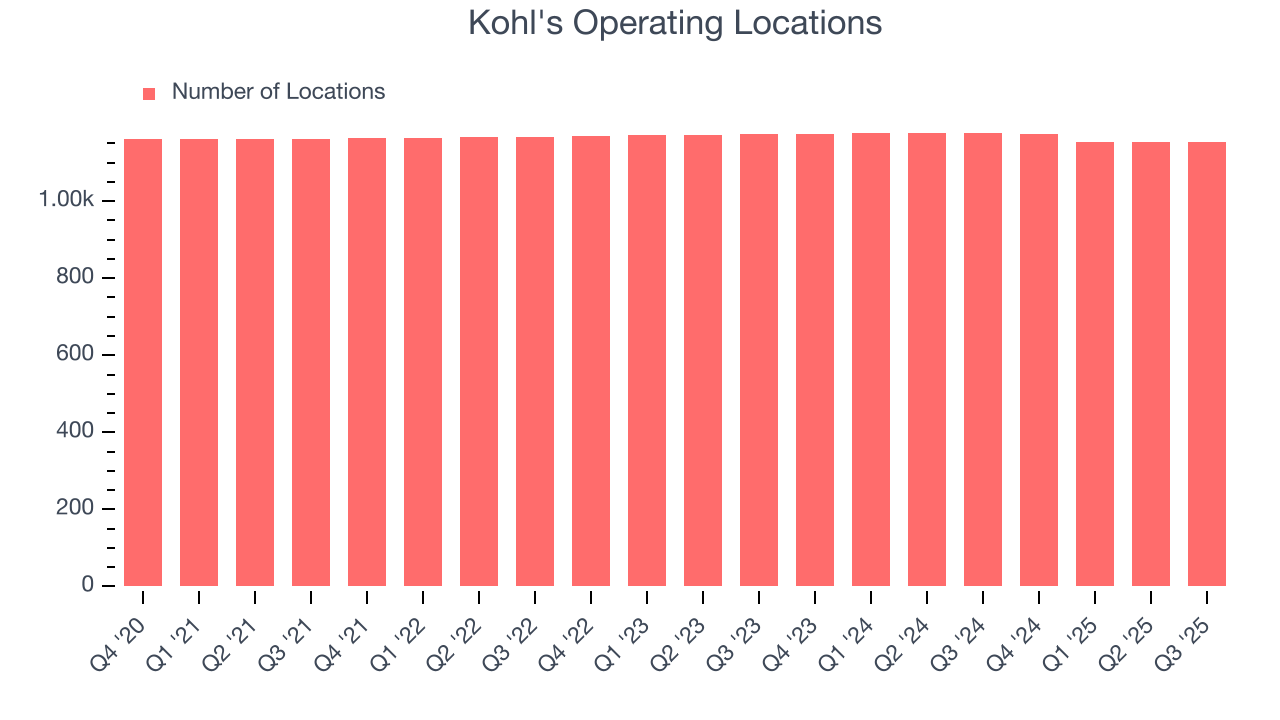

6. Store Performance

Number of Stores

The number of stores a retailer operates is a critical driver of how quickly company-level sales can grow.

Kohl's has kept its store count flat over the last two years while other consumer retail businesses have opted for growth.

When a retailer keeps its store footprint steady, it usually means demand is stable and it’s focusing on operational efficiency to increase profitability.

Note that Kohl's reports its store count intermittently, so some data points are missing in the chart below.

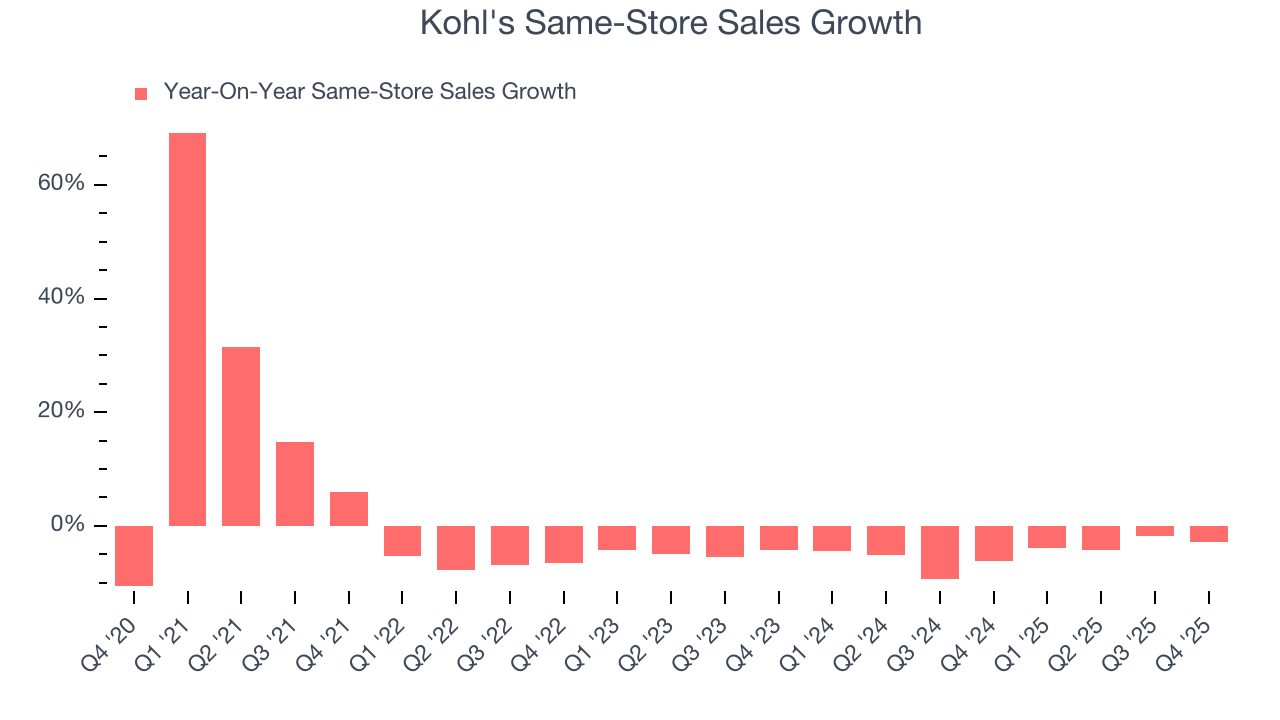

Same-Store Sales

The change in a company's store base only tells one side of the story. The other is the performance of its existing locations and e-commerce sales, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales provides a deeper understanding of this issue because it measures organic growth at brick-and-mortar shops for at least a year.

Kohl’s demand has been shrinking over the last two years as its same-store sales have averaged 4.7% annual declines. This performance isn’t ideal, and we’d be concerned if Kohl's starts opening new stores to artificially boost revenue growth.

In the latest quarter, Kohl’s same-store sales fell by 2.8% year on year. This decrease represents a further deceleration from its historical levels. We hope the business can get back on track.

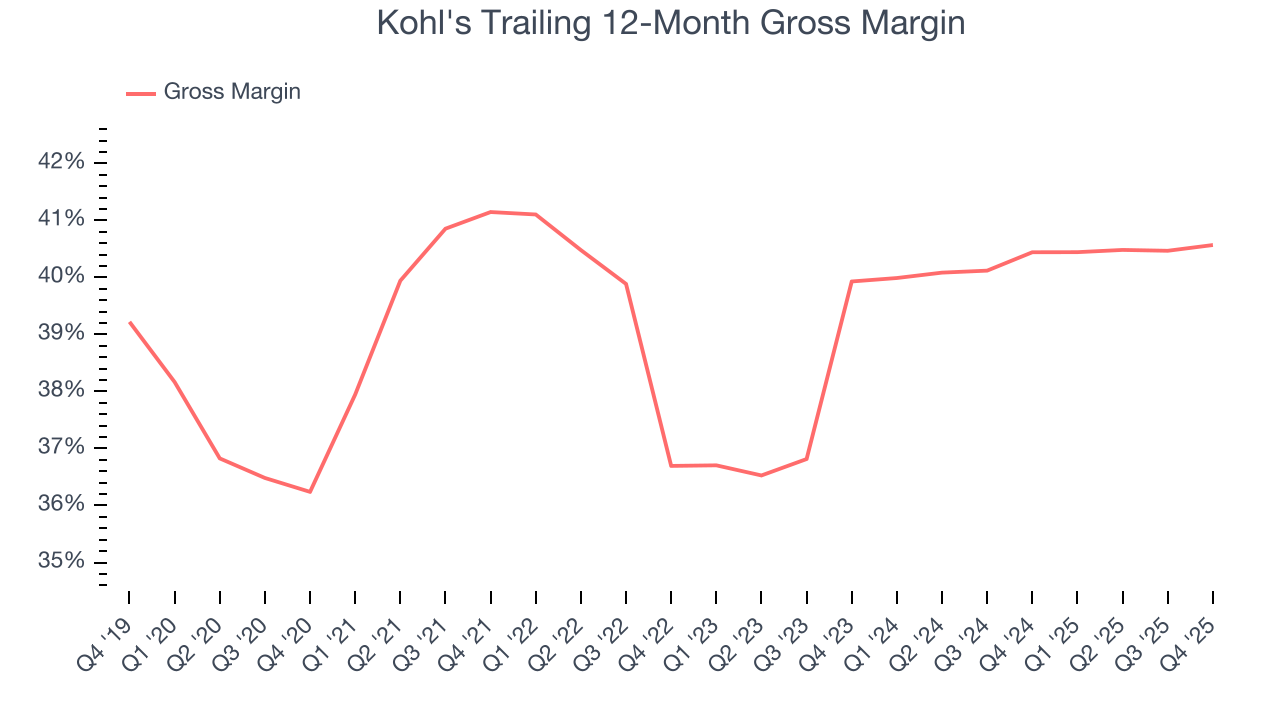

7. Gross Margin & Pricing Power

Kohl’s unit economics are higher than the typical retailer, giving it the flexibility to invest in areas such as marketing and talent to reach more consumers. As you can see below, it averaged a decent 40.5% gross margin over the last two years. That means for every $100 in revenue, $59.50 went towards paying for inventory, transportation, and distribution.

This quarter, Kohl’s gross profit margin was 35.7%, in line with the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting it strives to keep prices low for customers and has stable input costs (such as labor and freight expenses to transport goods).

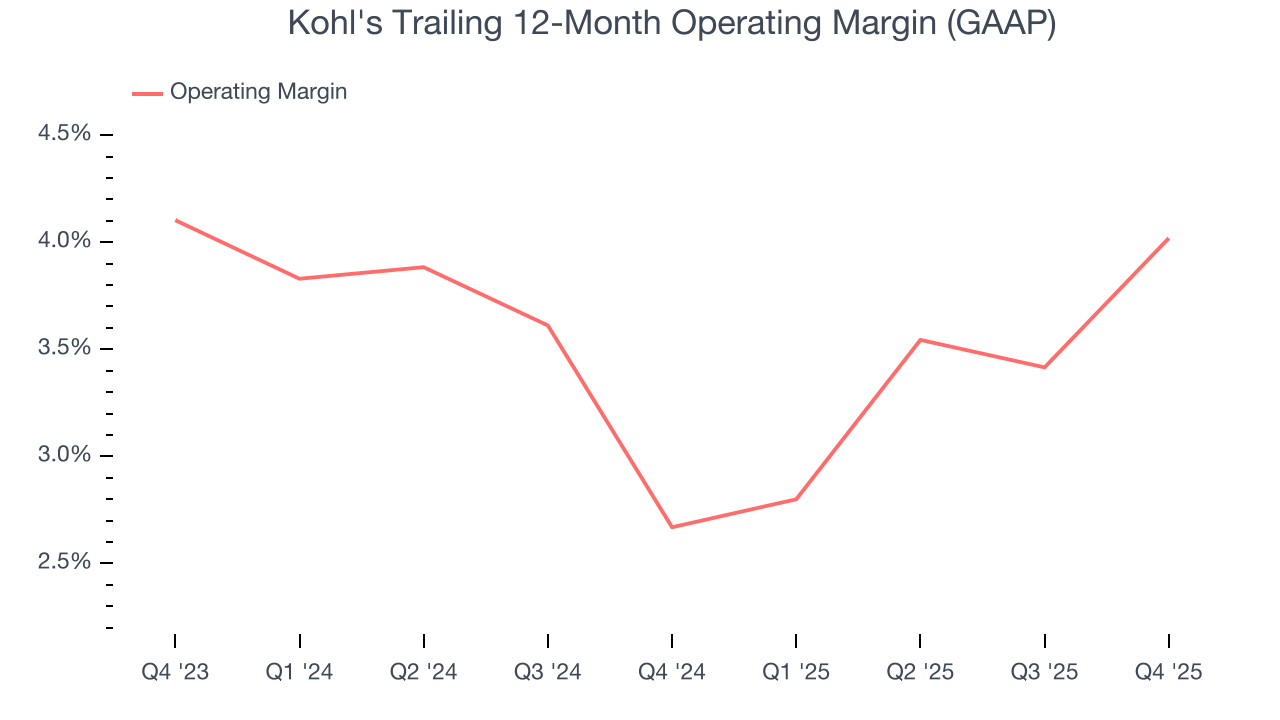

8. Operating Margin

Operating margin is a key profitability metric because it accounts for all expenses necessary to run a store, including wages, inventory, rent, advertising, and other administrative costs.

Kohl's was profitable over the last two years but held back by its large cost base. Its average operating margin of 3.3% was weak for a consumer retail business.

On the plus side, Kohl’s operating margin rose by 1.3 percentage points over the last year.

In Q4, Kohl's generated an operating margin profit margin of 4.1%, up 1.8 percentage points year on year. The increase was encouraging, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, and administrative overhead.

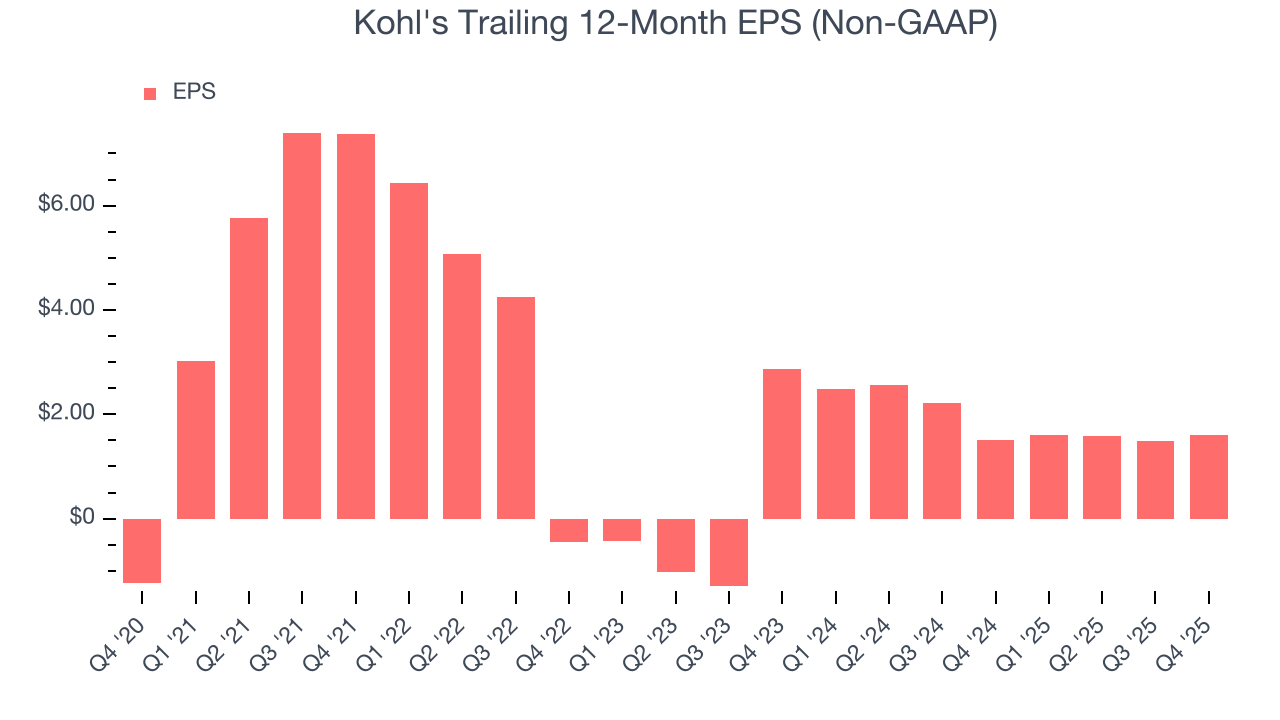

9. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Kohl’s full-year EPS flipped from negative to positive over the last three years. This is encouraging and shows it’s at a critical moment in its life.

In Q4, Kohl's reported adjusted EPS of $1.07, up from $0.95 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Kohl’s full-year EPS of $1.60 to shrink by 11.3%.

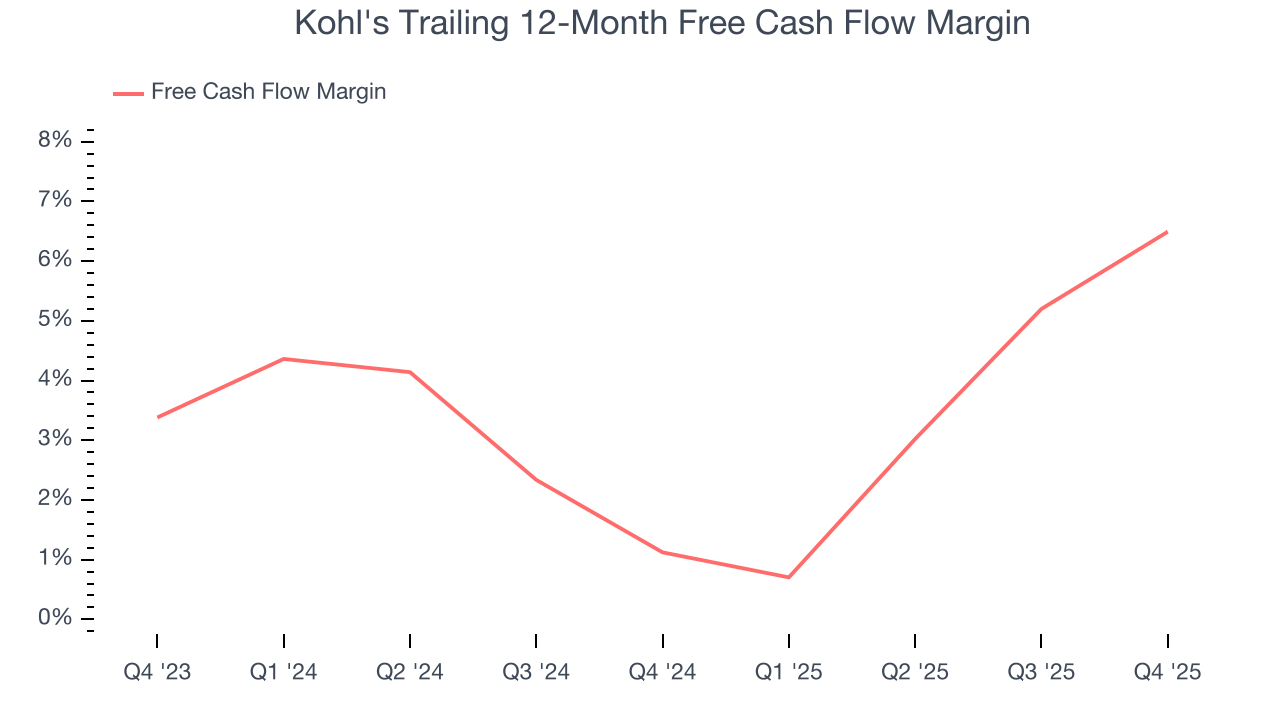

10. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Kohl's has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 3.7% over the last two years, slightly better than the broader consumer retail sector.

Taking a step back, we can see that Kohl’s margin expanded by 5.4 percentage points over the last year. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

Kohl’s free cash flow clocked in at $686 million in Q4, equivalent to a 13.3% margin. This result was good as its margin was 4.1 percentage points higher than in the same quarter last year, building on its favorable historical trend.

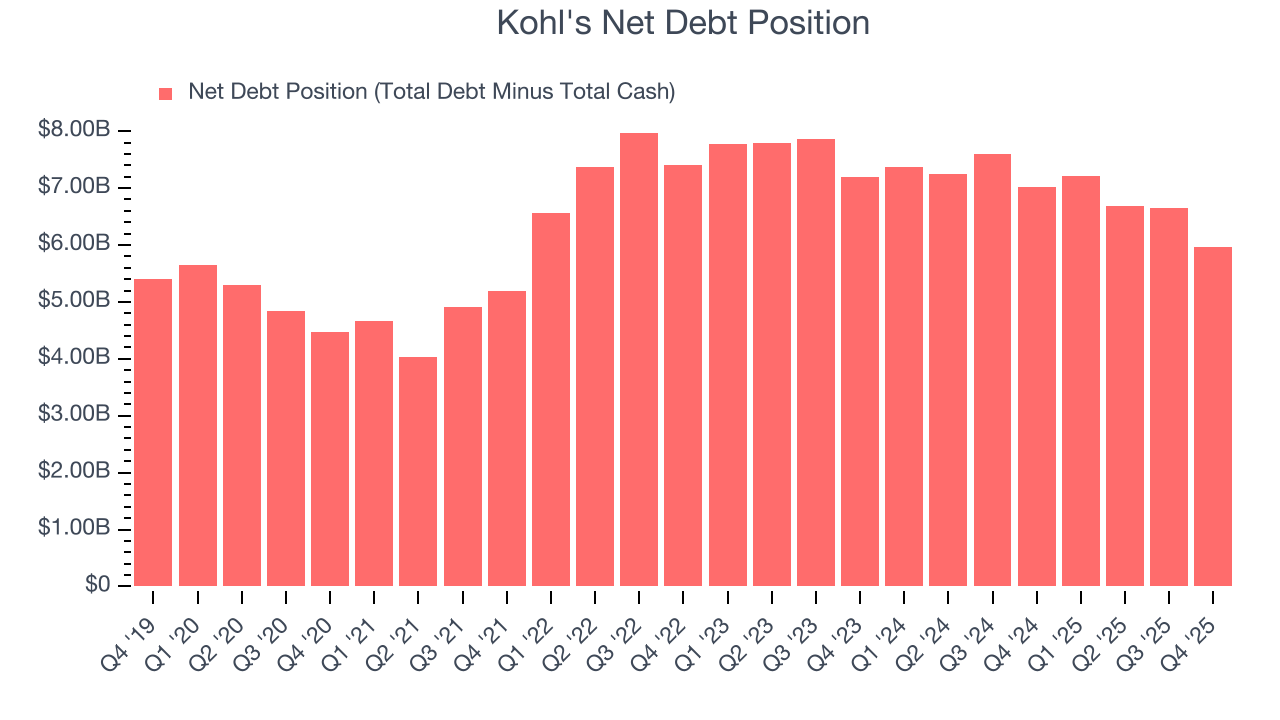

11. Balance Sheet Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

Kohl’s $6.63 billion of debt exceeds the $674 million of cash on its balance sheet. Furthermore, its 5× net-debt-to-EBITDA ratio (based on its EBITDA of $1.18 billion over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. Kohl's could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope Kohl's can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

12. Key Takeaways from Kohl’s Q4 Results

Same store sales declined and was below expectations, which is a bad sign for a retailer. Looking ahead, the company expects a same-store sales decline for the upcoming fiscal year, in line with expectation. Full-year EPS guidance was also in line with expectations. Overall, this print didn't have any positive surprises. Investors were likely hoping for more, and shares traded down 10.1% to $13.30 immediately following the results.

13. Is Now The Time To Buy Kohl's?

Updated: March 15, 2026 at 10:43 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Kohl's.

Kohl's falls short of our quality standards. First off, its revenue has declined over the last three years. While its EPS growth over the last three years has been fantastic, the downside is its shrinking same-store sales tell us it will need to change its strategy to succeed. On top of that, its operating margins reveal poor profitability compared to other retailers.

Kohl’s P/E ratio based on the next 12 months is 9.8x. While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $17.75 on the company (compared to the current share price of $13.18).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.