LendingClub (LC)

We’d invest in LendingClub. Its superb revenue growth indicates its market share is increasing.― StockStory Analyst Team

1. News

2. Summary

Why We Like LendingClub

Pioneering peer-to-peer lending in the US before evolving into a digital bank, LendingClub (NYSE:LC) operates a marketplace that connects borrowers with lenders, offering personal loans, auto refinancing, and banking services.

- Annual revenue growth of 25.7% over the past five years was outstanding, reflecting market share gains this cycle

- Incremental sales over the last two years have been highly profitable as its earnings per share increased by 79.1% annually, topping its revenue gains

- The stock is a timely buy because it’s trading at a reasonable price relative to its growth prospects

We’re fond of companies like LendingClub. The price looks fair based on its quality, so this could be a favorable time to buy some shares.

Why Is Now The Time To Buy LendingClub?

LendingClub’s stock price of $15.05 implies a valuation ratio of 9.7x forward P/E. The valuation sure appears attractive, and we suspect the stock is trading below its intrinsic value when factoring in its business quality.

A powerful one-two punch is a company that can both grow earnings and earn a higher multiple over time. High-quality companies trading at big discounts to intrinsic value are good ways to set up this combination.

3. LendingClub (LC) Research Report: Q4 CY2025 Update

Digital lending platform LendingClub (NYSE:LC) reported revenue ahead of Wall Streets expectations in Q4 CY2025, with sales up 22.7% year on year to $266.5 million. Its GAAP profit of $0.35 per share was 3.3% above analysts’ consensus estimates.

LendingClub (LC) Q4 CY2025 Highlights:

- Revenue: $266.5 million vs analyst estimates of $261.9 million (22.7% year-on-year growth, 1.8% beat)

- Pre-tax Profit: $50.03 million (18.8% margin)

- EPS (GAAP): $0.35 vs analyst estimates of $0.34 (3.3% beat)

- EPS (GAAP) guidance for the upcoming financial year 2026 is $1.73 at the midpoint, beating analyst estimates by 3.7%

- Market Capitalization: $2.40 billion

Company Overview

Pioneering peer-to-peer lending in the US before evolving into a digital bank, LendingClub (NYSE:LC) operates a marketplace that connects borrowers with lenders, offering personal loans, auto refinancing, and banking services.

LendingClub's primary business revolves around its consumer lending products, which include unsecured personal loans, patient and education financing, and secured auto refinance loans. The company uses data and technology to streamline the lending process, offering features like balance transfers, joint applications, and its "TopUp" product that allows borrowers to combine existing loans with additional funds into a single payment loan.

The company operates through a hybrid model where loans are either sold to marketplace investors or retained on its own balance sheet through LendingClub Bank (LC Bank). Marketplace investors include banks, institutional funds, private credit funds, asset managers, and insurance companies. LendingClub has developed innovative structures like "Structured Certificates" where it retains senior securities while selling residual certificates to investors, creating benefits for both parties.

For depositors, LendingClub offers FDIC-insured high-yield savings accounts, checking accounts, and certificates of deposit. Its checking accounts feature ATM fee rebates, no overdraft fees, and early direct deposits. The company recently launched "LevelUp Savings" to reward members with better interest rates for positive savings behavior.

LendingClub attracts customers through its website and mobile app, using channels like online affiliate partners, direct mail, paid search, display advertising, email, social media, and strategic relationship referrals. The company's proprietary LCX platform facilitates loan sales through real-time electronic settlement technology, allowing for dynamically priced loans at scale that can be customized to meet individual investor needs.

4. Personal Loan

Personal loan providers offer unsecured credit for various consumer needs. The sector benefits from digital application processes, increasing consumer comfort with online financial services, and opportunities in underserved credit segments. Headwinds include credit risk management in unsecured lending, regulatory oversight of lending practices, and intense competition affecting margins from both traditional and fintech lenders.

LendingClub's competitors include digital lending platforms like SoFi (NASDAQ:SOFI) and Upstart (NASDAQ:UPST), traditional banks offering online lending services such as Marcus by Goldman Sachs (NYSE:GS), and fintech companies like Prosper Marketplace and Avant.

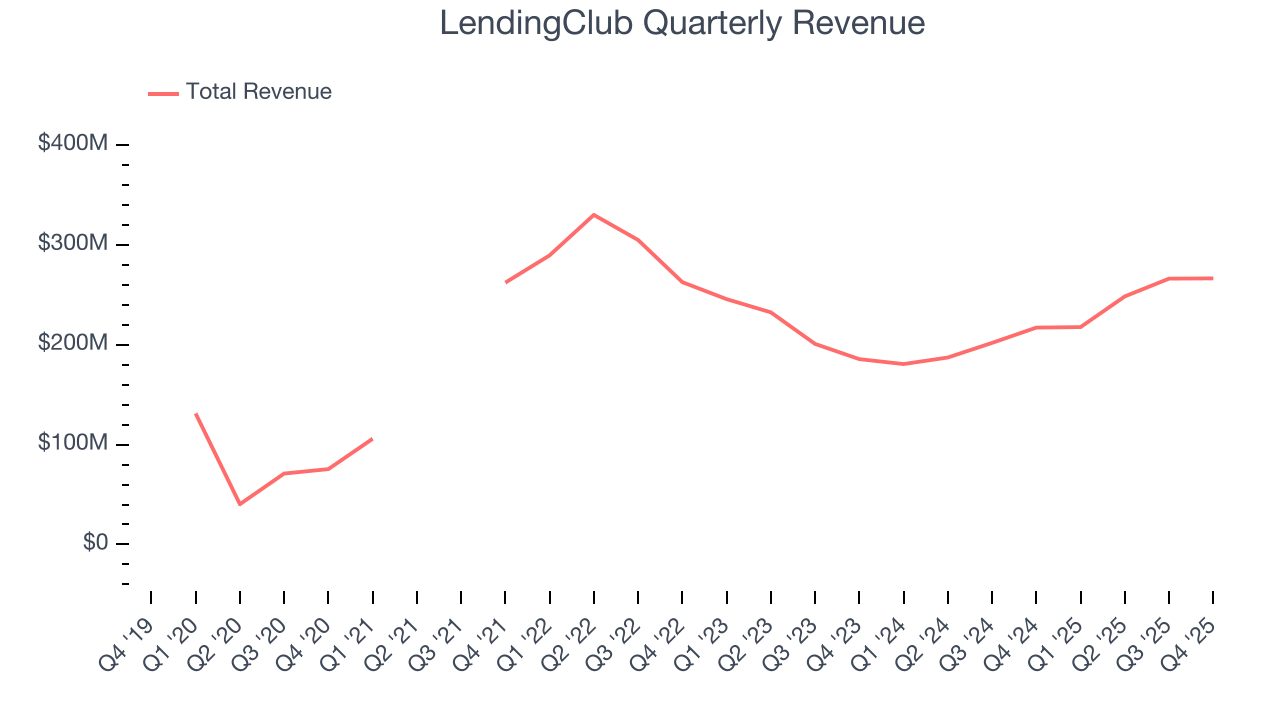

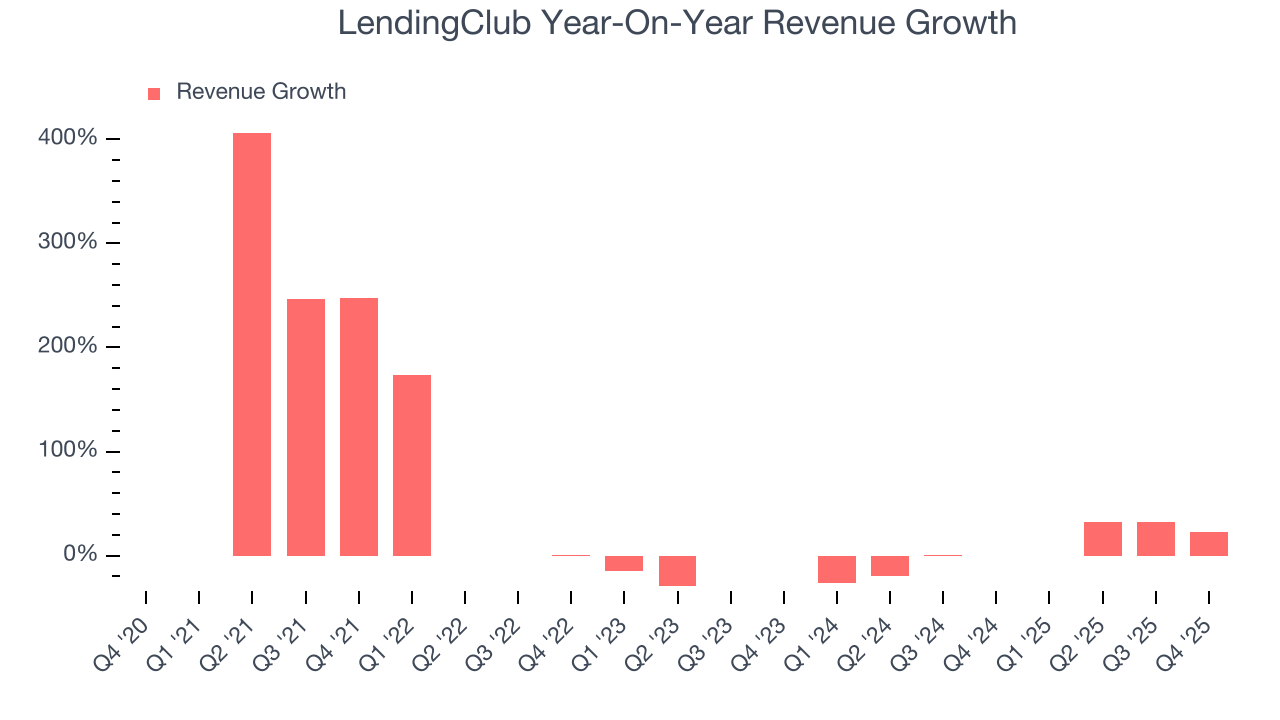

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Luckily, LendingClub’s revenue grew at an incredible 25.7% compounded annual growth rate over the last five years. Its growth surpassed the average financials company and shows its offerings resonate with customers, a great starting point for our analysis.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. LendingClub’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 7.5% over the last two years was well below its five-year trend.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, LendingClub reported robust year-on-year revenue growth of 22.7%, and its $266.5 million of revenue topped Wall Street estimates by 1.8%.

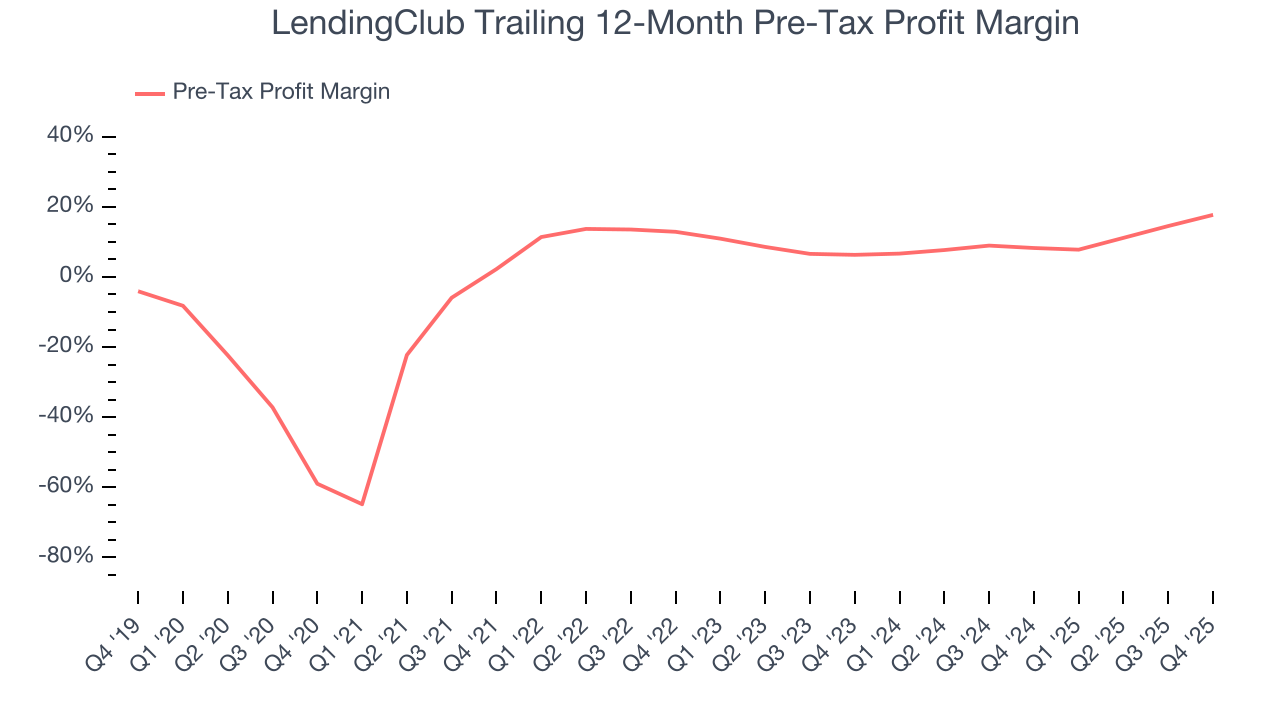

6. Pre-Tax Profit Margin

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For Personal Loan companies, we look at pre-tax profit rather than the operating margin that defines sectors such as consumer, tech, and industrials.

Interest income and expenses play a big role in financial institutions' profitability, so they should be factored into the definition of profit. Taxes, however, should not as they are largely out of a company's control. This is pre-tax profit by definition.

Over the last five years, LendingClub’s pre-tax profit margin has fallen by 76.7 percentage points, going from 2.3% to 17.7%. It has also expanded by 11.4 percentage points on a two-year basis, showing its expenses have consistently grown at a slower rate than revenue. This typically signals prudent management.

LendingClub’s pre-tax profit margin came in at 18.8% this quarter. This result was 13.7 percentage points better than the same quarter last year.

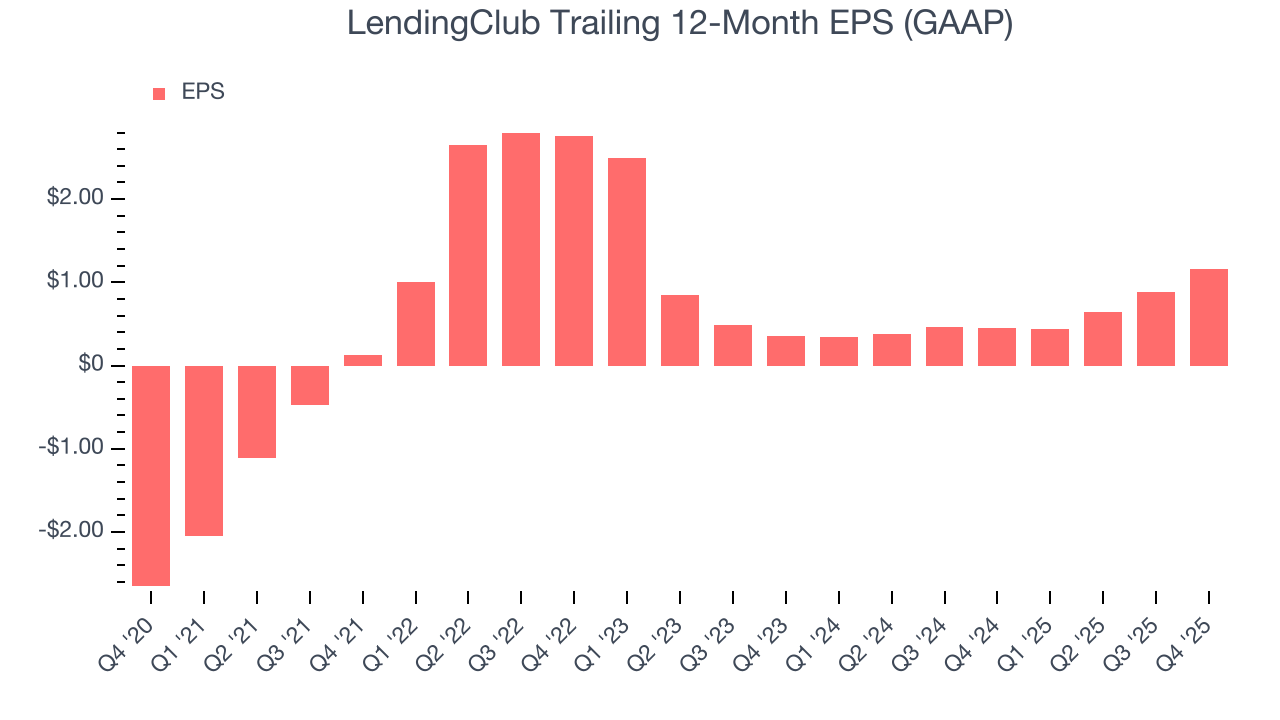

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

LendingClub’s full-year EPS flipped from negative to positive over the last five years. This is a good sign and shows it’s at an inflection point.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

LendingClub’s EPS grew at an astounding 79.2% compounded annual growth rate over the last two years, higher than its 7.5% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

We can take a deeper look into LendingClub’s earnings quality to better understand the drivers of its performance. LendingClub’s pre-tax profit margin has expanded over the last two years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, LendingClub reported EPS of $0.35, up from $0.08 in the same quarter last year. This print beat analysts’ estimates by 5.8%. Over the next 12 months, Wall Street expects LendingClub’s full-year EPS of $1.16 to grow 45.1%.

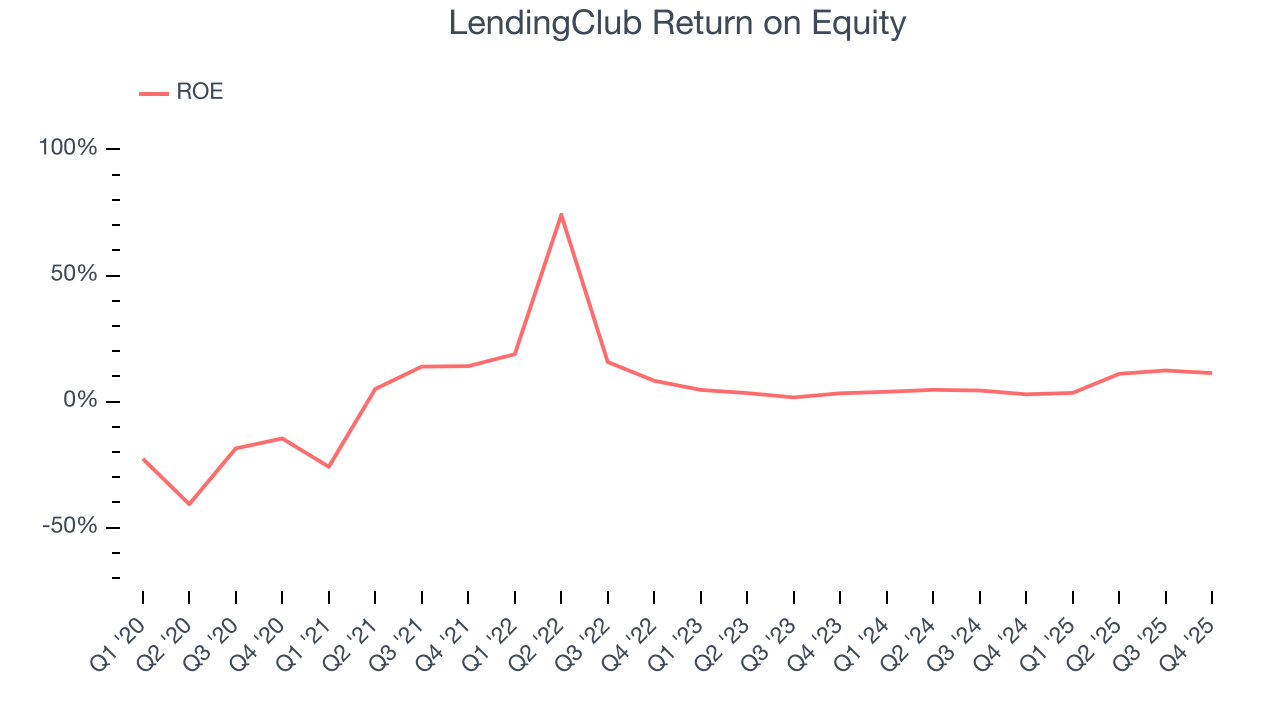

8. Return on Equity

Return on equity, or ROE, tells us how much profit a company generates for each dollar of shareholder equity, a key funding source for banks. Over a long period, banks with high ROE tend to compound shareholder wealth faster through retained earnings, buybacks, and dividends.

Over the last five years, LendingClub has averaged an ROE of 9.5%, uninspiring for a company operating in a sector where the average shakes out around 10%. We’re optimistic LendingClub can turn the ship around given its success in other measures of financial health.

9. Balance Sheet Assessment

Leverage is core to a financial firm’s business model (loans funded by deposits). To ensure economic stability and avoid a repeat of the 2008 GFC, regulators require certain levels of capital and liquidity, focusing on the Tier 1 capital ratio.

Tier 1 capital is the highest-quality capital that a firm holds, consisting primarily of common stock and retained earnings, but also physical gold. It serves as the primary cushion against losses and is the first line of defense in times of financial distress.

This capital is divided by risk-weighted assets to derive the Tier 1 capital ratio. Risk-weighted means that cash and US treasury securities are assigned little risk while unsecured consumer loans and equity investments get much higher risk weights, for example.

New regulation after the 2008 financial crisis requires that all firms must maintain a Tier 1 capital ratio greater than 4.5%. On top of this, there are additional buffers based on scale, risk profile, and other regulatory classifications, so that at the end of the day, firms generally must maintain a 7-10% ratio at minimum.

Over the last two years, LendingClub has averaged a Tier 1 capital ratio of 17.4%, which is considered safe and well capitalized in the event that macro or market conditions suddenly deteriorate.

10. Key Takeaways from LendingClub’s Q4 Results

It was great to see LendingClub’s full-year EPS guidance top analysts’ expectations. We were also happy its revenue outperformed Wall Street’s estimates. Overall, we think this was a solid quarter with some key areas of upside. The market seemed to be hoping for more, and the stock traded down 5.1% to $18.55 immediately after reporting.

11. Is Now The Time To Buy LendingClub?

Updated: March 1, 2026 at 12:45 AM EST

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in LendingClub.

LendingClub is a rock-solid business worth owning. First of all, the company’s revenue growth was exceptional over the last five years. On top of that, its expanding pre-tax profit margin shows the business has become more efficient, and its remarkable EPS growth over the last five years shows its profits are trickling down to shareholders.

LendingClub’s P/E ratio based on the next 12 months is 9.7x. Looking at the financials space today, LendingClub’s fundamentals really stand out, and we like it at this bargain price.

Wall Street analysts have a consensus one-year price target of $24.20 on the company (compared to the current share price of $15.05), implying they see 60.8% upside in buying LendingClub in the short term.