Lowe's (LOW)

Lowe's doesn’t excite us. Not only is its demand weak but also its falling returns on capital suggest it’s becoming less profitable.― StockStory Analyst Team

1. News

2. Summary

Why We Think Lowe's Will Underperform

Founded in North Carolina as Lowe's North Wilkesboro Hardware, the company is a home improvement retailer that sells everything from paint to tools to building materials.

- Sales tumbled by 3.8% annually over the last three years, showing consumer trends are working against its favor

- Weak same-store sales trends over the past two years suggest there may be few opportunities in its core markets to open new locations

- A bright spot is that its ROIC punches in at 35.1%, illustrating management’s expertise in identifying profitable investments

Lowe's doesn’t satisfy our quality benchmarks. We’re hunting for superior stocks elsewhere.

Why There Are Better Opportunities Than Lowe's

At $226.30 per share, Lowe's trades at 18.2x forward P/E. This multiple is quite expensive for the quality you get.

It’s better to pay up for high-quality businesses with strong long-term earnings potential rather than to buy lower-quality companies with open questions and big downside risks.

3. Lowe's (LOW) Research Report: Q4 CY2025 Update

Home improvement retailer Lowe’s (NYSE:LOW) reported Q4 CY2025 results topping the market’s revenue expectations, with sales up 10.9% year on year to $20.58 billion. The company expects the full year’s revenue to be around $93 billion, close to analysts’ estimates. Its non-GAAP profit of $1.98 per share was 1.9% above analysts’ consensus estimates.

Lowe's (LOW) Q4 CY2025 Highlights:

- Revenue: $20.58 billion vs analyst estimates of $20.36 billion (10.9% year-on-year growth, 1.1% beat)

- Adjusted EPS: $1.98 vs analyst estimates of $1.94 (1.9% beat)

- Adjusted EBITDA: $2.52 billion vs analyst estimates of $2.33 billion (12.2% margin, 8% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $12.50 at the midpoint, missing analyst estimates by 3.4%

- Operating Margin: 8.3%, down from 9.9% in the same quarter last year

- Free Cash Flow Margin: 4.7%, up from 2% in the same quarter last year

- Same-Store Sales rose 1.3% year on year (0.2% in the same quarter last year)

- Market Capitalization: $156.3 billion

Company Overview

Founded in North Carolina as Lowe's North Wilkesboro Hardware, the company is a home improvement retailer that sells everything from paint to tools to building materials.

The core Lowe’s customer is the do-it-yourself (DIY) homeowner, often shopping for design, remodeling, or home decor needs. The company also serves professional contractors as well. Like its closest competitor Home Depot, Lowe’s has a broad range of home improvement and design products at competitive prices. For the DIY shopper, Lowe’s offers installation services for products such as cabinets and flooring as well as design consultation services. For the professional contractor, Lowe’s has loyalty programs and volume discounts. There is also a Pro Desk in most stores, where contractors can place large or custom orders and consult with specialists trained to specifically assist professionals.

Since Lowe’s and Home Depot are the two largest home improvement retailers in North America with many similarities, a common question is how they differ. One difference is that Home Depot has a larger selection of appliances and power tools, while Lowe's may have a better selection of home decor and seasonal items. Another difference is the store aesthetic. When you walk into a Home Depot, it looks like a sprawling warehouse, and the feel is very utilitarian. Lowe’s stores, on the other hand, are slightly smaller and have a more traditional retail aesthetic with brighter colors.

4. Home Improvement Retailer

Home improvement retailers serve the maintenance and repair needs of do-it-yourself homeowners as well as professional contractors. Home is where the heart is, so any homeowner will want to keep that home in good shape by maintaining the yard, fixing leaks, or improving lighting fixtures, for example. Home improvement stores win with depth and breadth of product, in-store consultations for customers who need help, and services that cater to professionals. It is hard for non-focused retailers and e-commerce competitors to match these. However, the research, convenience, and prices of online platforms means they can’t be fully written off, either.

Home improvement retail competitors include Home Depot (NYSE:HD) and private company Ace Hardware. Amazon.com (NASDAQ:AMZN) and Wayfair (NYSE:W) also offer some home improvement products.

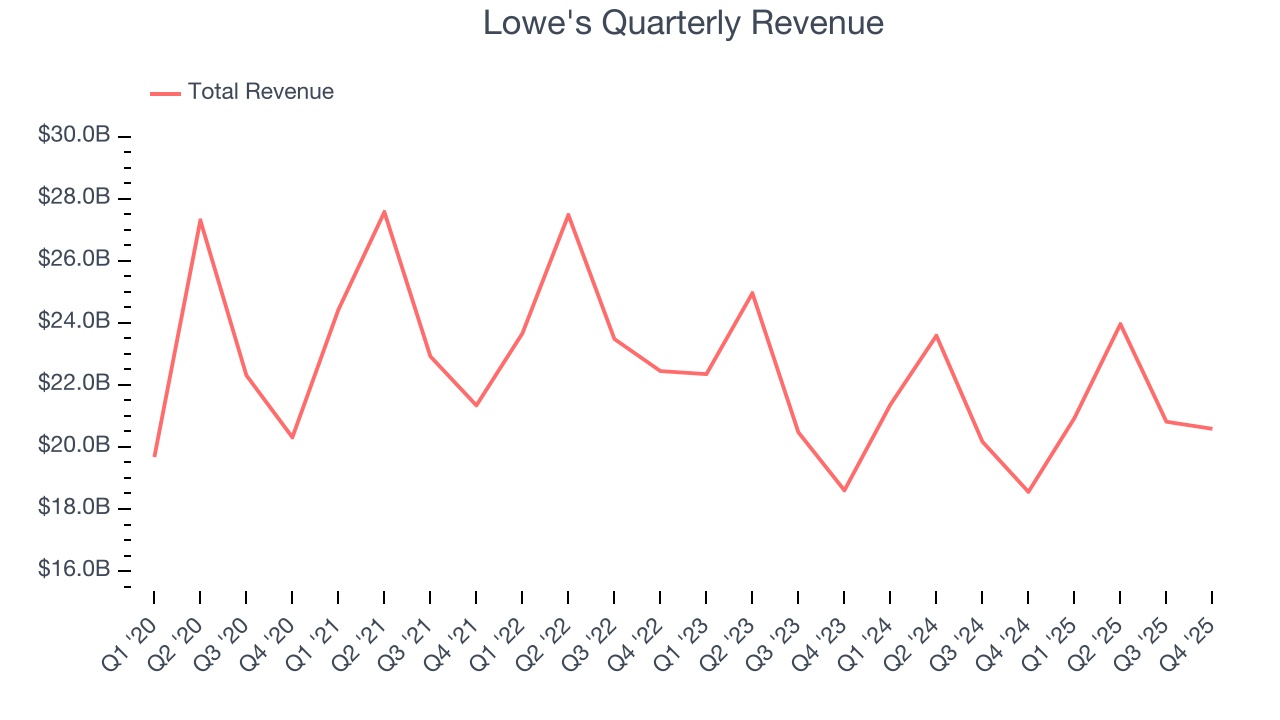

5. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $86.29 billion in revenue over the past 12 months, Lowe's is a behemoth in the consumer retail sector and benefits from economies of scale, giving it an edge in distribution. This also enables it to gain more leverage on its fixed costs than smaller competitors and the flexibility to offer lower prices. However, its scale is a double-edged sword because there is only so much real estate to build new stores, placing a ceiling on its growth. To expand meaningfully, Lowe's likely needs to tweak its prices or enter new markets.

As you can see below, Lowe's struggled to generate demand over the last three years. Its sales dropped by 3.8% annually as it didn’t open many new stores and observed lower sales at existing, established locations.

This quarter, Lowe's reported year-on-year revenue growth of 10.9%, and its $20.58 billion of revenue exceeded Wall Street’s estimates by 1.1%.

Looking ahead, sell-side analysts expect revenue to grow 8.1% over the next 12 months, an acceleration versus the last three years. This projection is particularly noteworthy for a company of its scale and indicates its newer products will catalyze better top-line performance.

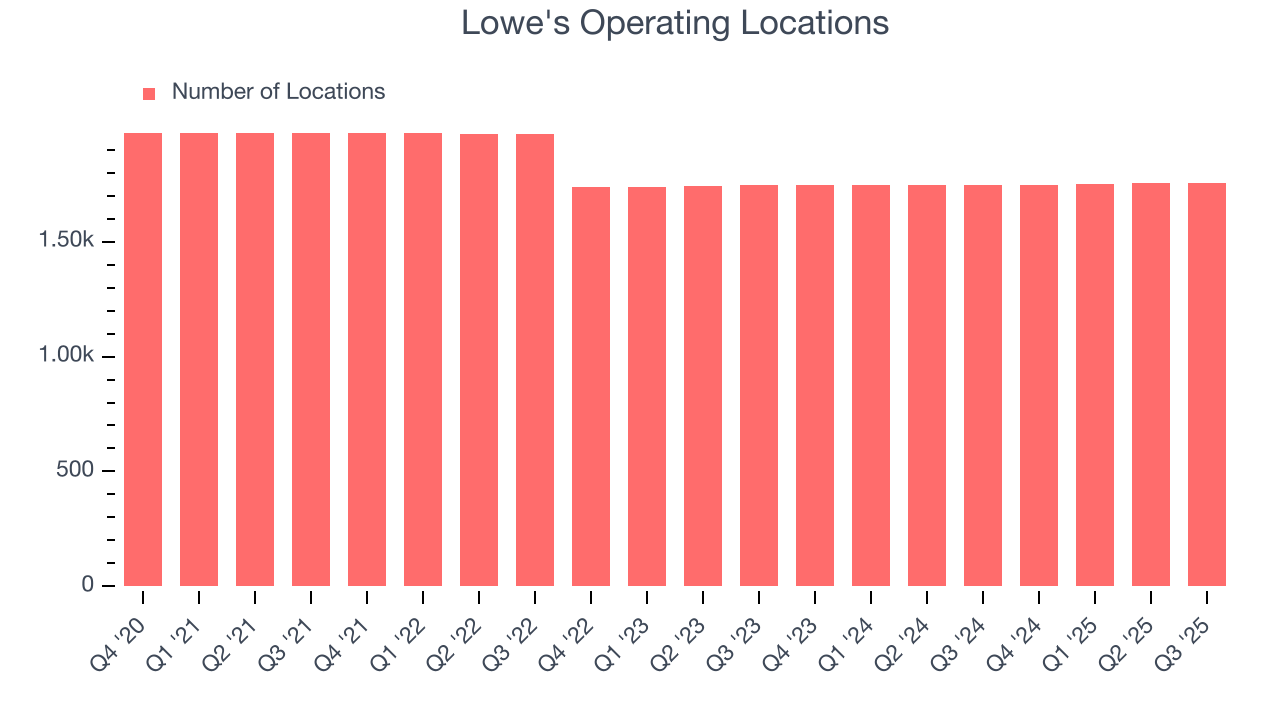

6. Store Performance

Number of Stores

Lowe's has kept its store count flat over the last two years while other consumer retail businesses have opted for growth.

When a retailer keeps its store footprint steady, it usually means demand is stable and it’s focusing on operational efficiency to increase profitability.

Note that Lowe's reports its store count intermittently, so some data points are missing in the chart below.

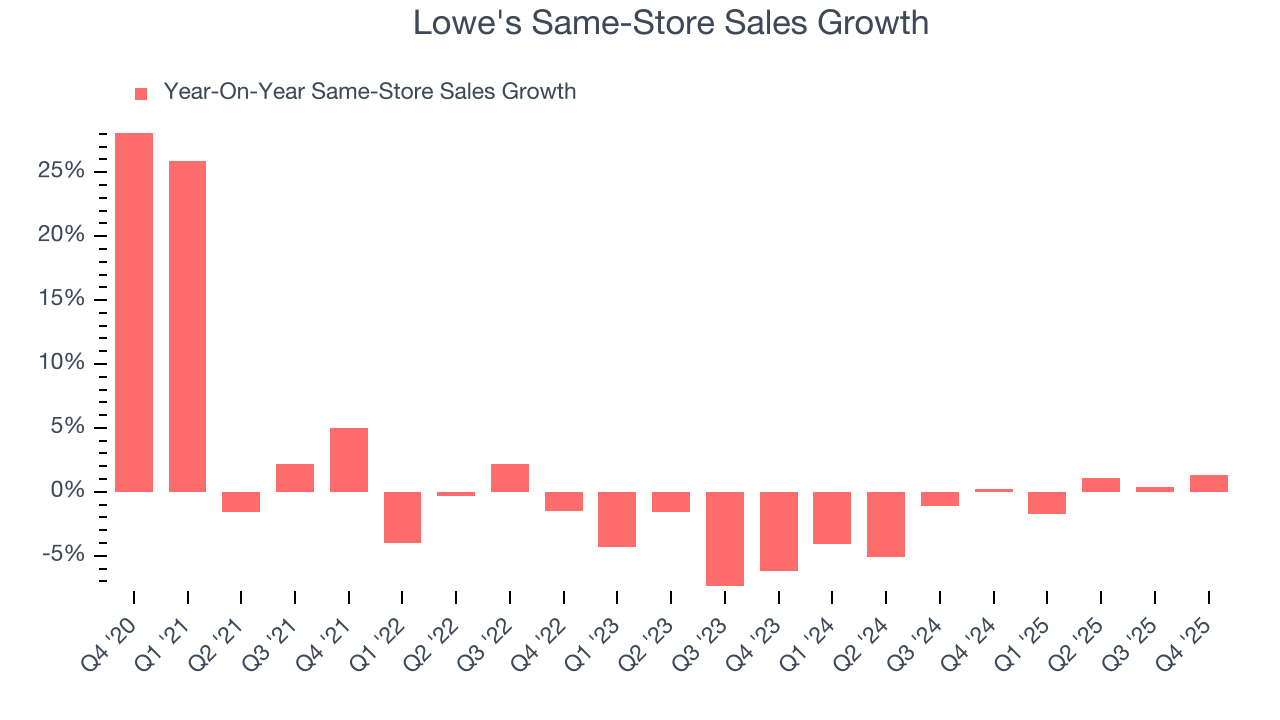

Same-Store Sales

A company's store base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales provides a deeper understanding of this issue because it measures organic growth at brick-and-mortar shops for at least a year.

Lowe’s demand has been shrinking over the last two years as its same-store sales have averaged 1.1% annual declines. This performance isn’t ideal, and we’d be concerned if Lowe's starts opening new stores to artificially boost revenue growth.

In the latest quarter, Lowe’s same-store sales rose 1.3% year on year. This growth was a well-appreciated turnaround from its historical levels, showing the business is regaining momentum.

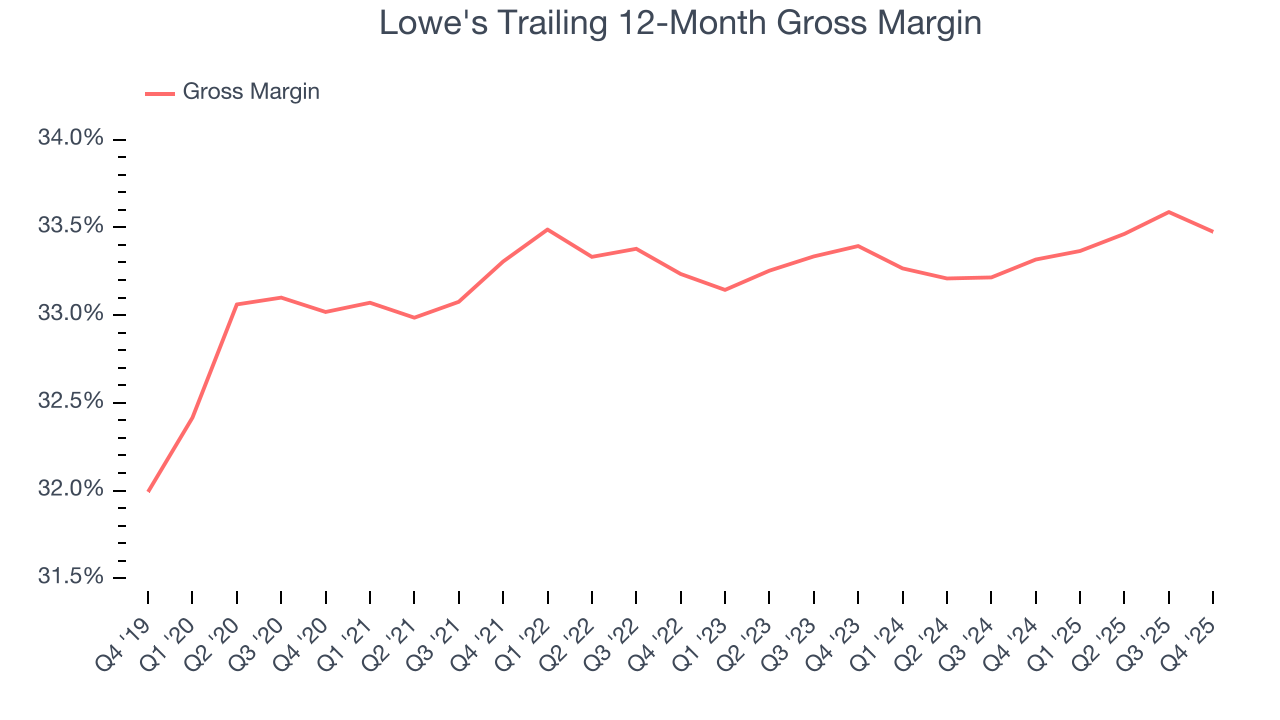

7. Gross Margin & Pricing Power

Lowe's has bad unit economics for a retailer, signaling it operates in a competitive market and lacks pricing power because its inventory is sold in many places. As you can see below, it averaged a 33.4% gross margin over the last two years. That means Lowe's paid its suppliers a lot of money ($66.60 for every $100 in revenue) to run its business.

Lowe’s gross profit margin came in at 32.5% this quarter, in line with the same quarter last year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting it strives to keep prices low for customers and has stable input costs (such as labor and freight expenses to transport goods).

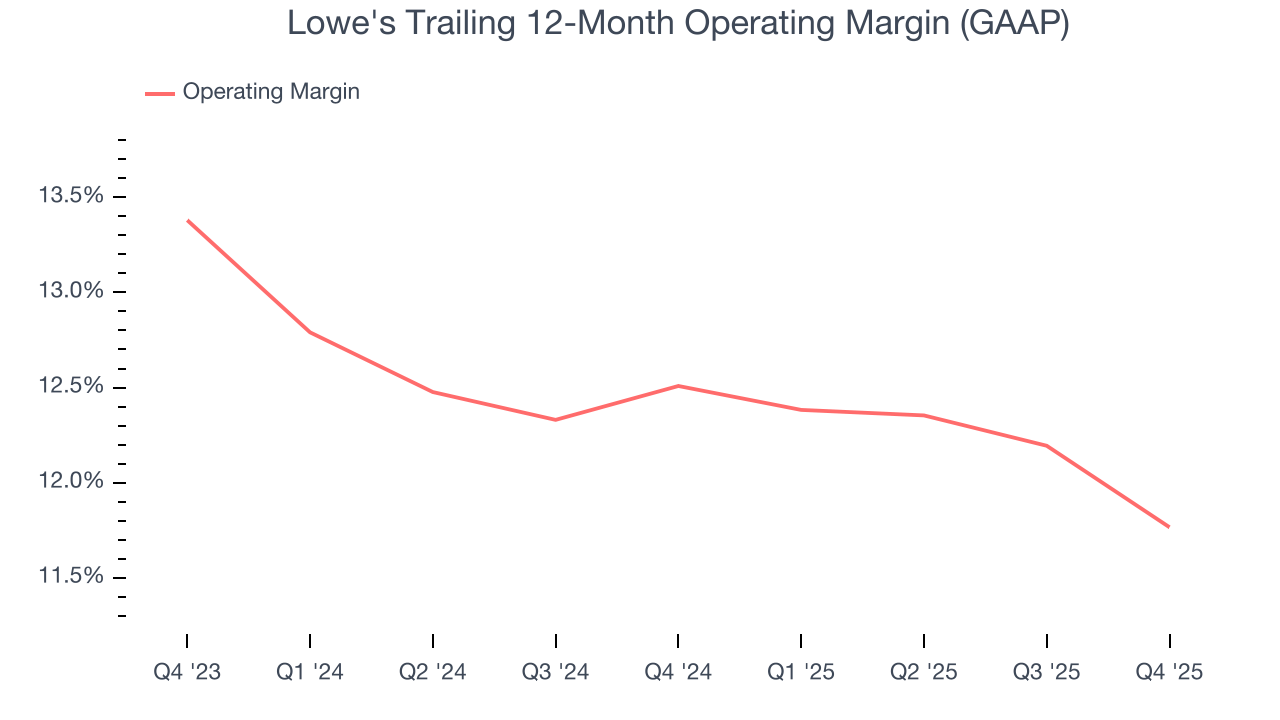

8. Operating Margin

Operating margin is an important measure of profitability for retailers as it accounts for all expenses necessary to run a store, including wages, inventory, rent, advertising, and other administrative costs.

Lowe’s operating margin might fluctuated slightly over the last 12 months but has generally stayed the same, averaging 12.1% over the last two years. This profitability was top-notch for a consumer retail business, showing it’s an well-run company with an efficient cost structure. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Looking at the trend in its profitability, Lowe’s operating margin might fluctuated slightly but has generally stayed the same over the last year, highlighting the consistency of its expense base.

This quarter, Lowe's generated an operating margin profit margin of 8.3%, down 1.6 percentage points year on year. Since Lowe’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, and administrative overhead increased.

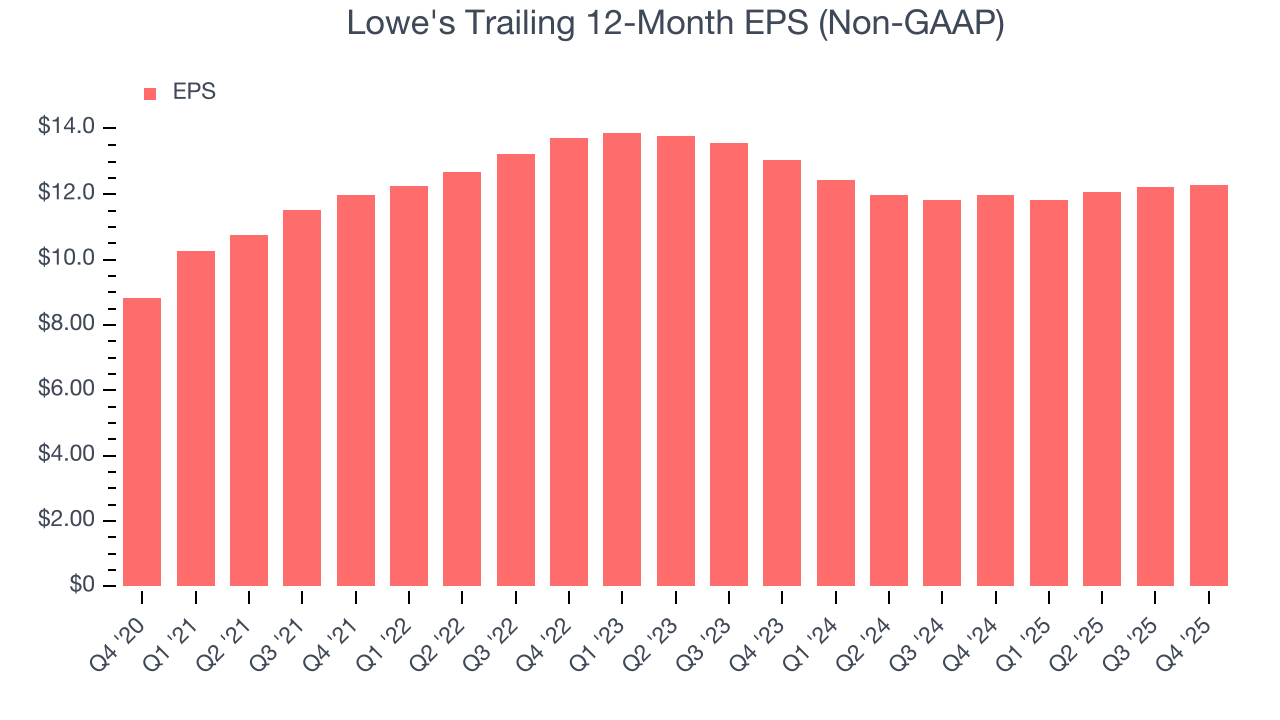

9. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Lowe's, its EPS and revenue declined by 3.6% and 3.8% annually over the last three years. In a mature sector such as consumer retail, we tend to steer our readers away from companies with falling EPS because it could imply changing secular trends and preferences. If the tide turns unexpectedly, Lowe’s low margin of safety could leave its stock price susceptible to large downswings.

In Q4, Lowe's reported adjusted EPS of $1.98, up from $1.93 in the same quarter last year. This print beat analysts’ estimates by 1.9%. Over the next 12 months, Wall Street expects Lowe’s full-year EPS of $12.29 to grow 4.9%.

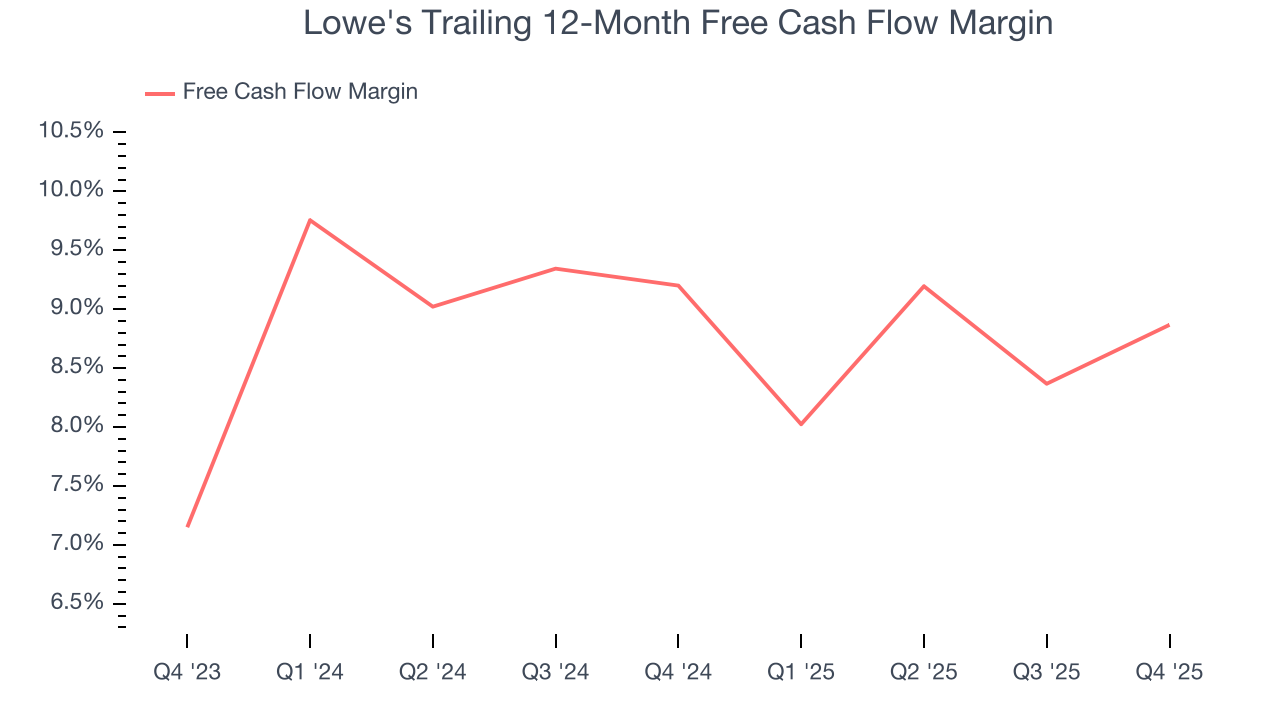

10. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Lowe's has shown robust cash profitability, giving it an edge over its competitors and the ability to reinvest or return capital to investors. The company’s free cash flow margin averaged 9% over the last two years, quite impressive for a consumer retail business.

Lowe’s free cash flow clocked in at $964 million in Q4, equivalent to a 4.7% margin. This result was good as its margin was 2.7 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, causing temporary swings. Long-term trends are more important.

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Although Lowe's hasn’t been the highest-quality company lately because of its poor top-line performance, it found a few growth initiatives in the past that worked out wonderfully. Its five-year average ROIC was 35.1%, splendid for a consumer retail business.

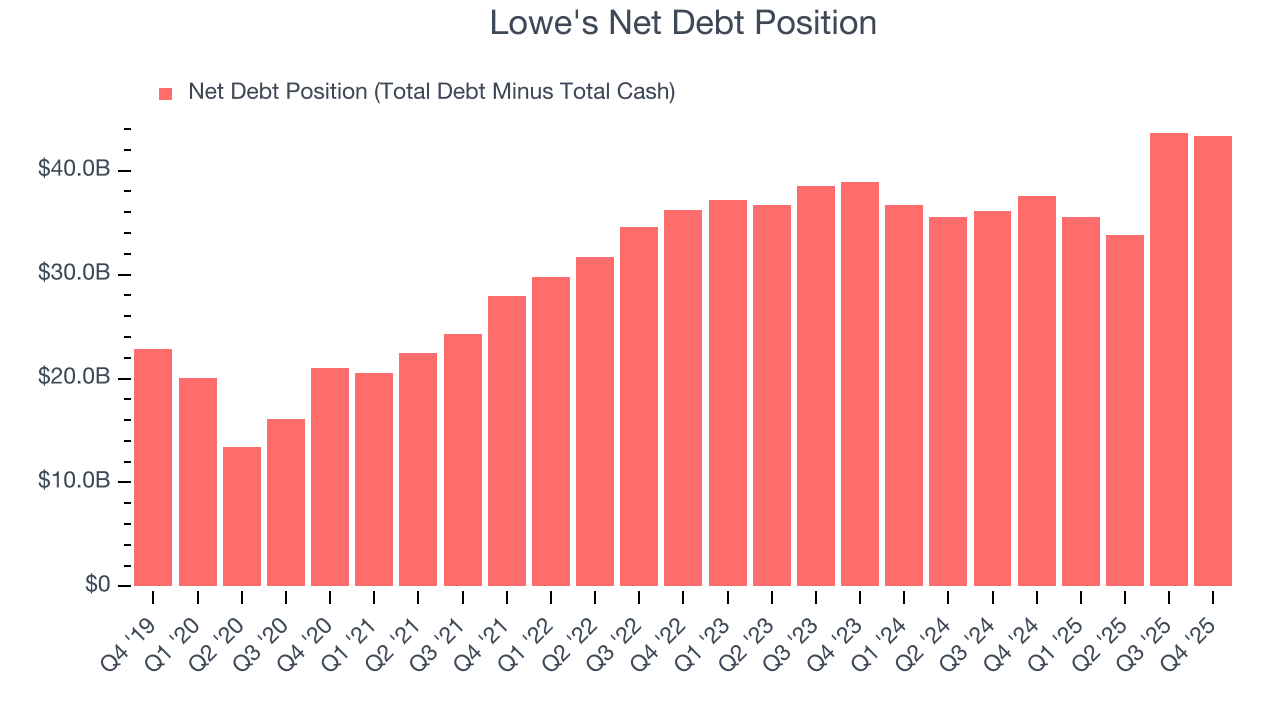

12. Balance Sheet Assessment

Lowe's reported $1.35 billion of cash and $44.68 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $12.51 billion of EBITDA over the last 12 months, we view Lowe’s 3.5× net-debt-to-EBITDA ratio as safe. We also see its $599 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

13. Key Takeaways from Lowe’s Q4 Results

We were impressed by how significantly Lowe's blew past analysts’ EBITDA expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. On the other hand, its full-year EPS guidance missed. Overall, this print had some key positives. Investors were likely hoping for more, and shares traded down 1.6% to $274.04 immediately after reporting.

14. Is Now The Time To Buy Lowe's?

Updated: March 22, 2026 at 10:31 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Lowe's.

Lowe's isn’t a terrible business, but it doesn’t pass our quality test. For starters, its revenue has declined over the last three years. While its stellar ROIC suggests it has been a well-run company historically, the downside is its shrinking same-store sales tell us it will need to change its strategy to succeed. On top of that, its gross margins make it more challenging to reach positive operating profits compared to other consumer retail businesses.

Lowe’s P/E ratio based on the next 12 months is 18.2x. Beauty is in the eye of the beholder, but we don’t really see a big opportunity at the moment. We're fairly confident there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $286.48 on the company (compared to the current share price of $226.30).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.