ManpowerGroup (MAN)

We wouldn’t recommend ManpowerGroup. Not only are its sales cratering but also its low returns on capital suggest it struggles to generate profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think ManpowerGroup Will Underperform

Founded during the post-World War II economic boom when businesses needed temporary workers, ManpowerGroup (NYSE:MAN) connects millions of people to employment opportunities through its global network of staffing, recruitment, and workforce management services.

- Sales were flat over the last five years, indicating it’s failed to expand this cycle

- Performance over the past five years shows each sale was less profitable, as its earnings per share fell by 18.4% annually

- Absence of organic revenue growth over the past two years suggests it may have to lean into acquisitions to drive its expansion

ManpowerGroup doesn’t fulfill our quality requirements. You should search for better opportunities.

Why There Are Better Opportunities Than ManpowerGroup

At $29.01 per share, ManpowerGroup trades at 8.8x forward P/E. This certainly seems like a cheap stock, but we think there are valid reasons why it trades this way.

Cheap stocks can look like a great deal at first glance, but they can be value traps. They often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. ManpowerGroup (MAN) Research Report: Q4 CY2025 Update

Workforce solutions provider ManpowerGroup (NYSE:MAN) reported Q4 CY2025 results topping the market’s revenue expectations, with sales up 7.1% year on year to $4.71 billion. Its GAAP profit of $0.64 per share was 22.2% below analysts’ consensus estimates.

ManpowerGroup (MAN) Q4 CY2025 Highlights:

- Revenue: $4.71 billion vs analyst estimates of $4.63 billion (7.1% year-on-year growth, 1.8% beat)

- EPS (GAAP): $0.64 vs analyst expectations of $0.82 (22.2% miss)

- Adjusted EBITDA: $107.2 million vs analyst estimates of $108.7 million (2.3% margin, 1.4% miss)

- EPS (GAAP) guidance for Q1 CY2026 is $0.50 at the midpoint, roughly in line with what analysts were expecting

- Management noted out "improving market demand"

- Operating Margin: 1.7%, in line with the same quarter last year

- Free Cash Flow Margin: 3.6%, down from 5.4% in the same quarter last year

- Organic Revenue rose 2% year on year (beat)

- Market Capitalization: $1.34 billion

Company Overview

Founded during the post-World War II economic boom when businesses needed temporary workers, ManpowerGroup (NYSE:MAN) connects millions of people to employment opportunities through its global network of staffing, recruitment, and workforce management services.

The company operates through three main brands that address different segments of the labor market. Manpower focuses on contingent staffing and permanent recruitment across administrative, industrial, and office positions. Experis specializes in professional resourcing for technology fields, including IT infrastructure, cybersecurity, cloud computing, and digital transformation projects. Talent Solutions provides enterprise-level workforce management through recruitment process outsourcing (RPO), managed service provider (MSP) programs, and career transition services.

ManpowerGroup serves as an intermediary in the labor market, helping both job seekers and employers navigate changing workforce needs. For job seekers, the company provides access to temporary assignments, permanent positions, skills assessments, and training programs to enhance employability. For employers, it offers flexible staffing solutions during peak periods, specialized recruitment for hard-to-fill positions, and comprehensive workforce strategy consulting.

A manufacturing company might engage ManpowerGroup to quickly staff a production line during a seasonal surge, while a technology firm might use Experis to find specialized software developers for a specific project. Meanwhile, a multinational corporation could utilize Talent Solutions to manage its entire contingent workforce across multiple countries.

The company generates revenue primarily through markup on the wages of temporary workers it places, fees for permanent placements, and ongoing service contracts for its outsourcing and consulting offerings. With operations in approximately 75 countries and territories, ManpowerGroup maintains a truly global footprint, allowing it to serve multinational clients with consistent service delivery across regions while also addressing local market needs.

4. Professional Staffing & HR Solutions

The Professional Staffing & HR Solutions subsector within Business Services is set to benefit from evolving workforce trends, including the rise of remote work and the gig economy. With companies casting a wider net to find talent due to remote work, the expertise of staffing and recruiting companies is even more valuable. For those who invest wisely, the use of predictive AI in recruitment and screening as well as automation in HR workflows can enhance efficiency and scalability. On the other hand, digitization means that talent discovery is less of a manual process, opening the door for tech-first platforms. Additionally, regulatory scrutiny around data privacy in HR is evolving and may require companies in this sector to change their go-to-market strategies over time.

ManpowerGroup competes with global staffing and workforce solutions providers like Adecco Group, Randstad, and Robert Half (NYSE:RHI), as well as specialized firms such as Kelly Services (NASDAQ:KELYA), Korn Ferry (NYSE:KFY), and Recruit Holdings (owner of Indeed and Glassdoor).

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

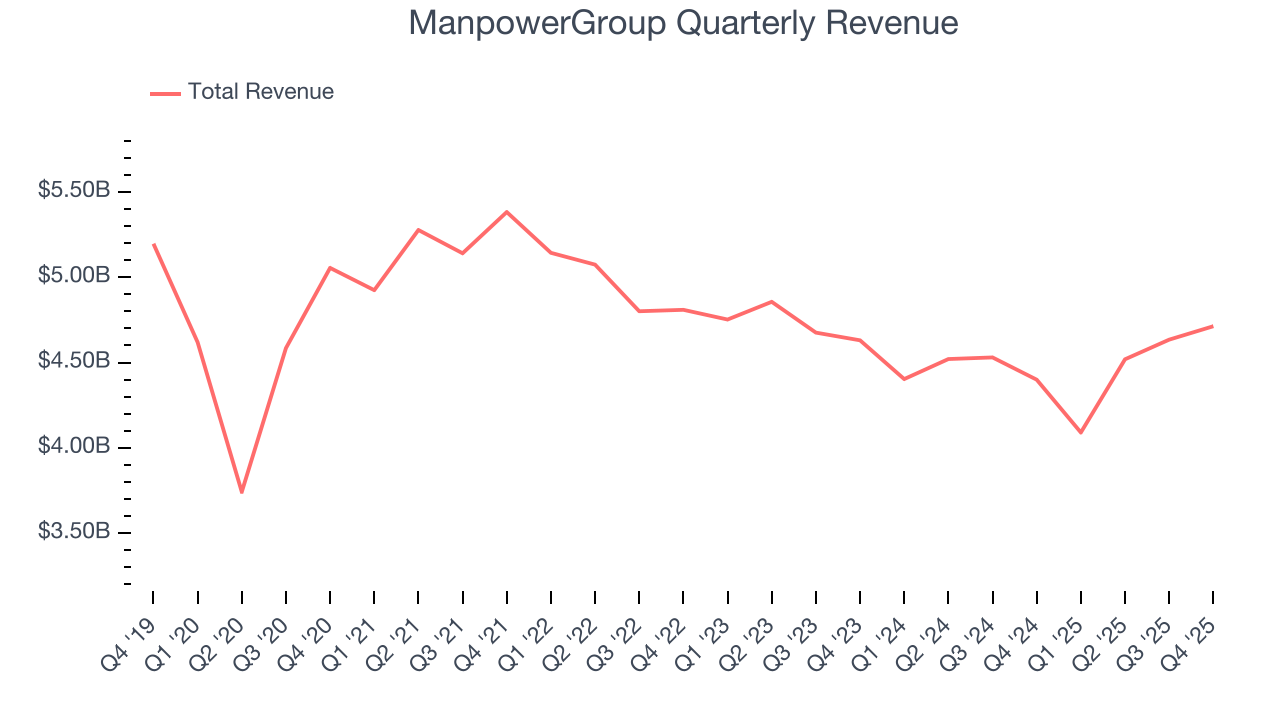

With $17.96 billion in revenue over the past 12 months, ManpowerGroup is a behemoth in the business services sector and benefits from economies of scale, giving it an edge in distribution. This also enables it to gain more leverage on its fixed costs than smaller competitors and the flexibility to offer lower prices. However, its scale is a double-edged sword because finding new avenues for growth becomes difficult when you already have a substantial market presence. To accelerate sales, ManpowerGroup likely needs to optimize its pricing or lean into new offerings and international expansion.

As you can see below, ManpowerGroup struggled to increase demand as its $17.96 billion of sales for the trailing 12 months was close to its revenue five years ago. This shows demand was soft, a tough starting point for our analysis.

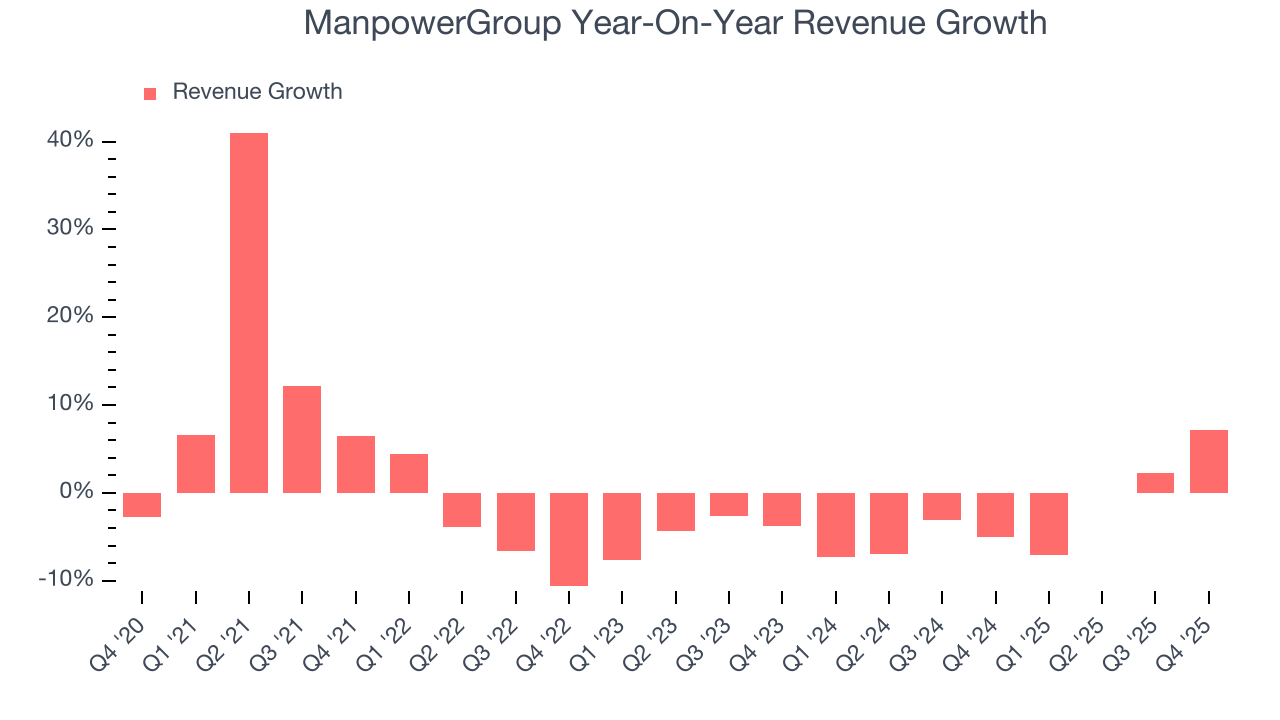

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. ManpowerGroup’s recent performance shows its demand remained suppressed as its revenue has declined by 2.6% annually over the last two years.

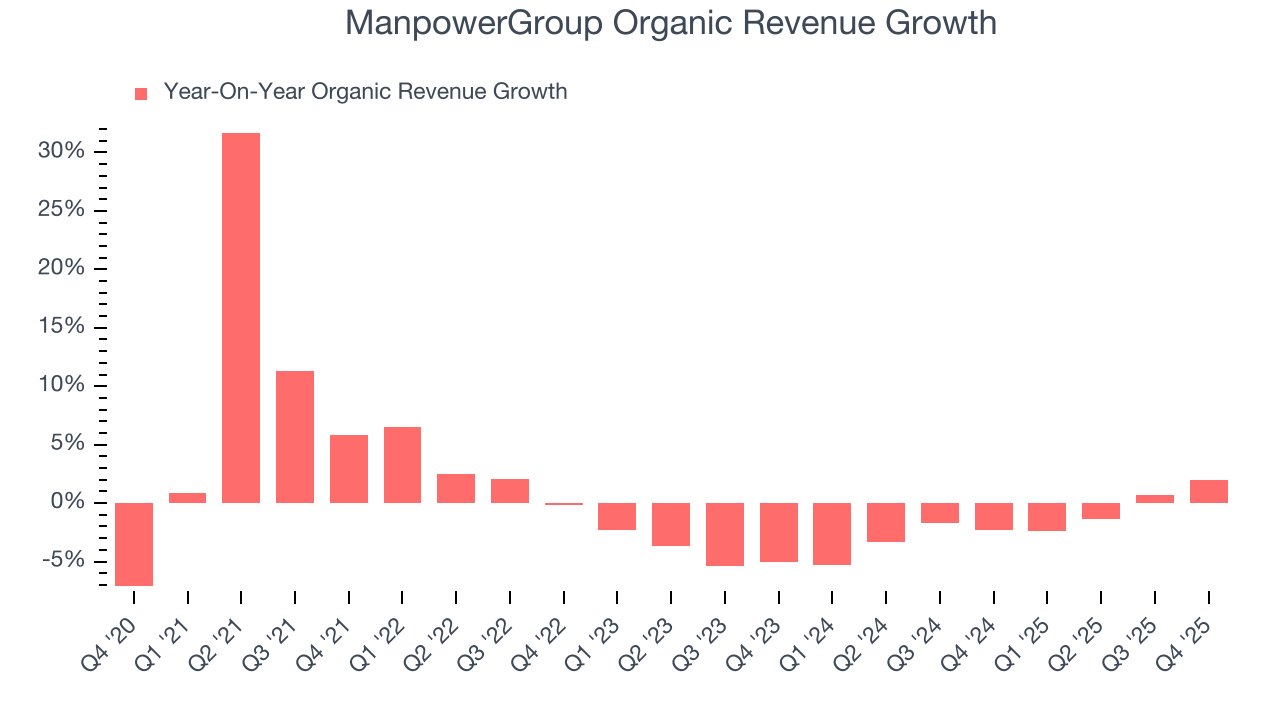

We can better understand the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, ManpowerGroup’s organic revenue averaged 1.7% year-on-year declines. Because this number aligns with its two-year revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, ManpowerGroup reported year-on-year revenue growth of 7.1%, and its $4.71 billion of revenue exceeded Wall Street’s estimates by 1.8%.

Looking ahead, sell-side analysts expect revenue to grow 3% over the next 12 months. Although this projection suggests its newer products and services will catalyze better top-line performance, it is still below average for the sector.

6. Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D.

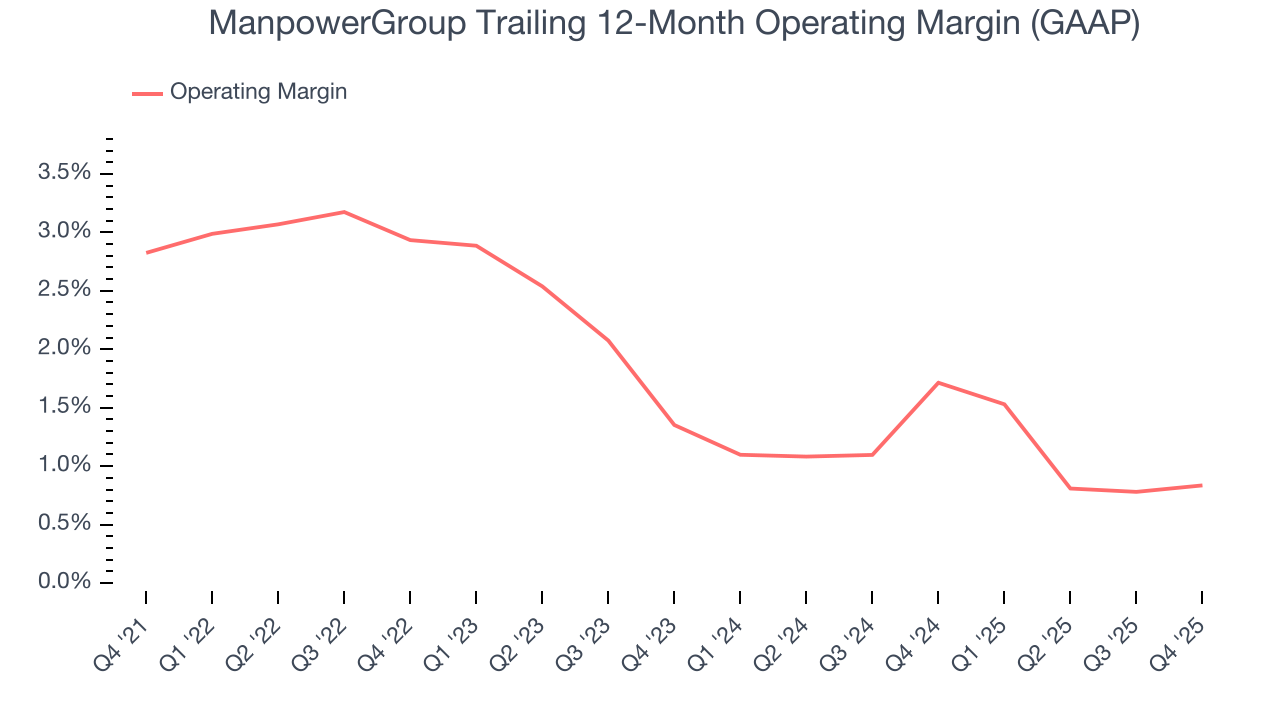

ManpowerGroup was profitable over the last five years but held back by its large cost base. Its average operating margin of 2% was weak for a business services business.

Analyzing the trend in its profitability, ManpowerGroup’s operating margin decreased by 2 percentage points over the last five years. ManpowerGroup’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, ManpowerGroup generated an operating margin profit margin of 1.7%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

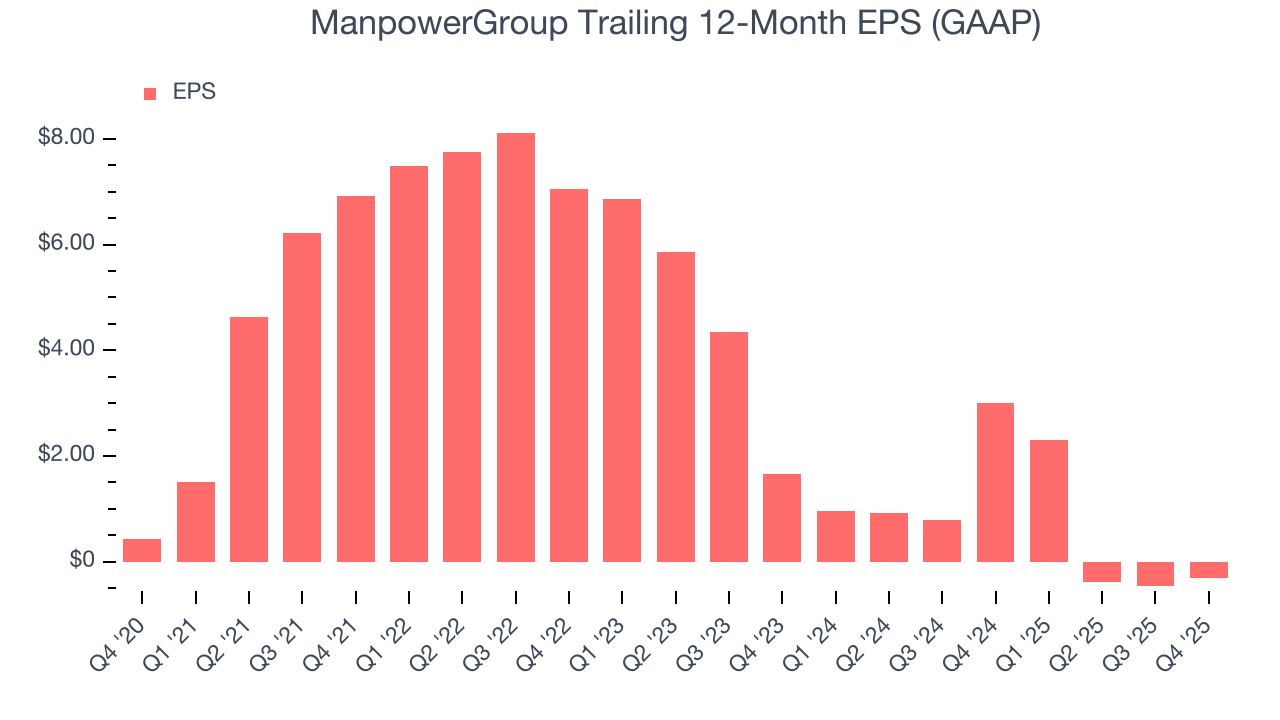

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for ManpowerGroup, its EPS declined by 22% annually over the last five years while its revenue was flat. This tells us the company struggled because its fixed cost base made it difficult to adjust to choppy demand.

Diving into the nuances of ManpowerGroup’s earnings can give us a better understanding of its performance. As we mentioned earlier, ManpowerGroup’s operating margin was flat this quarter but declined by 2 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For ManpowerGroup, its two-year annual EPS declines of 47.7% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q4, ManpowerGroup reported EPS of $0.64, up from $0.47 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates. Over the next 12 months, Wall Street is optimistic. Analysts forecast ManpowerGroup’s full-year EPS of negative $0.30 will flip to positive $3.56.

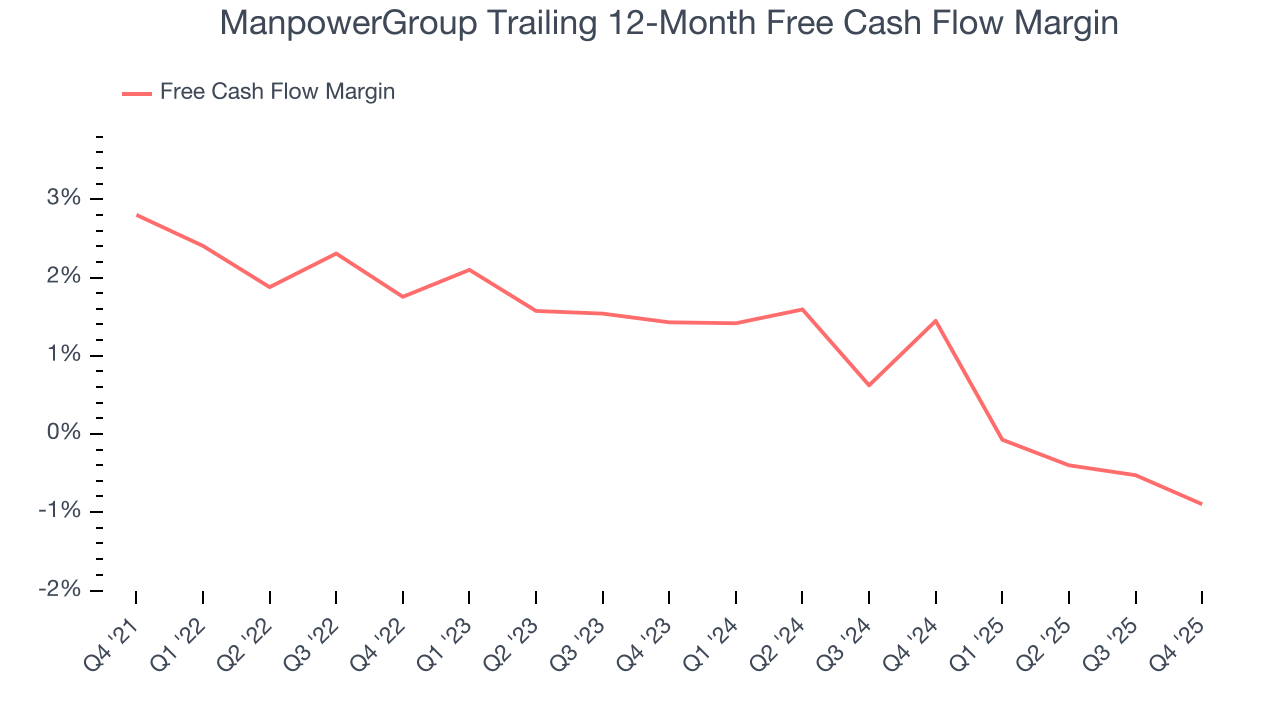

8. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

ManpowerGroup has shown poor cash profitability over the last five years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 1.4%, lousy for a business services business.

Taking a step back, we can see that ManpowerGroup’s margin dropped by 3.7 percentage points during that time. Almost any movement in the wrong direction is undesirable because of its already low cash conversion. If the trend continues, it could signal it’s becoming a more capital-intensive business.

ManpowerGroup’s free cash flow clocked in at $168 million in Q4, equivalent to a 3.6% margin. The company’s cash profitability regressed as it was 1.8 percentage points lower than in the same quarter last year, but it’s still above its five-year average. We wouldn’t read too much into this quarter’s decline because investment needs can be seasonal, leading to short-term swings. Long-term trends are more important.

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

ManpowerGroup’s management team makes decent investment decisions and generates value for shareholders. Its five-year average ROIC was 10.8%, slightly better than typical business services business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, ManpowerGroup’s ROIC has decreased significantly over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

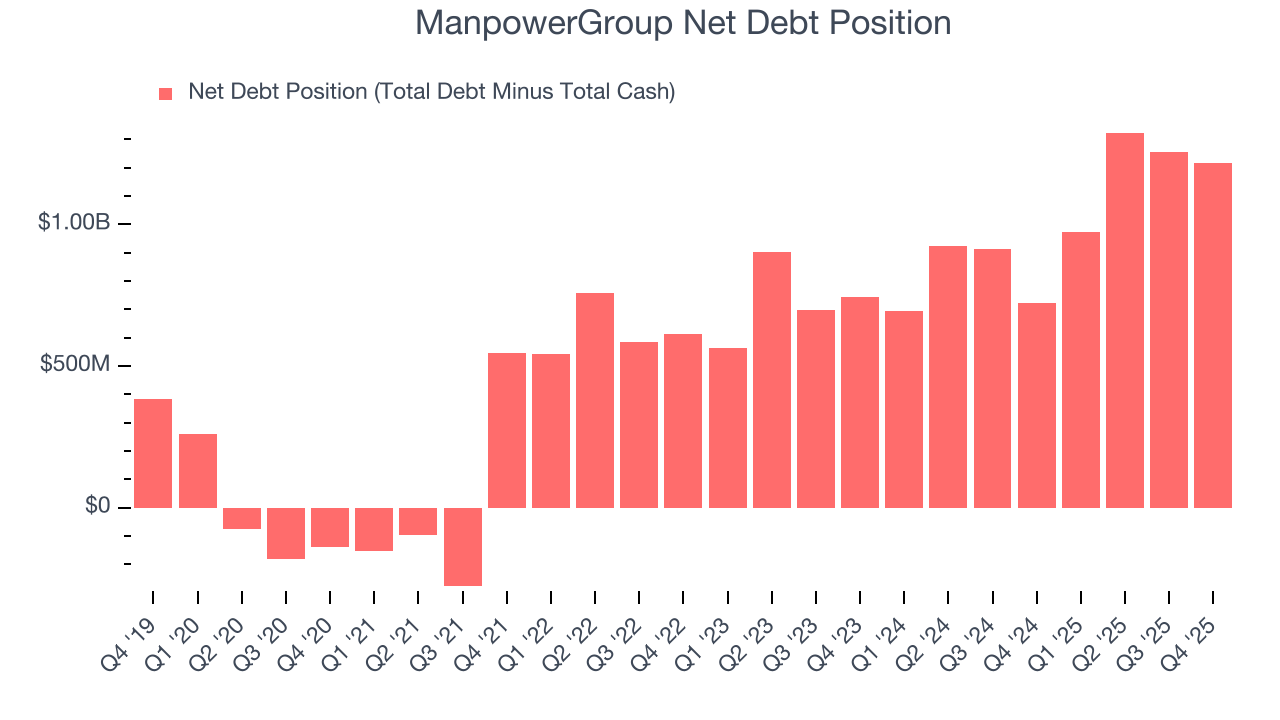

10. Balance Sheet Assessment

ManpowerGroup reported $871 million of cash and $2.09 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $384.9 million of EBITDA over the last 12 months, we view ManpowerGroup’s 3.2× net-debt-to-EBITDA ratio as safe. We also see its $65.5 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from ManpowerGroup’s Q4 Results

We enjoyed seeing ManpowerGroup beat analysts’ organic revenue expectations this quarter, leading to a revenue beat. Management also called out "improving market demand". On the other hand, its EPS missed. Overall, this was a mixedquarter. Still, the stock traded up 10.2% to $31.90 immediately after reporting.

12. Is Now The Time To Buy ManpowerGroup?

Updated: January 29, 2026 at 8:50 AM EST

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in ManpowerGroup.

We cheer for all companies making their customers lives easier, but in the case of ManpowerGroup, we’ll be cheering from the sidelines. First off, its revenue growth was weak over the last five years. And while its scale makes it a trusted partner with negotiating leverage, the downside is its diminishing returns show management's prior bets haven't worked out. On top of that, its declining EPS over the last five years makes it a less attractive asset to the public markets.

ManpowerGroup’s P/E ratio based on the next 12 months is 7.7x. While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $38.67 on the company (compared to the current share price of $31.90).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.