McDonald's (MCD)

McDonald's is intriguing. Its high free cash flow margin and returns on capital show it can produce cash and invest it wisely.― StockStory Analyst Team

1. News

2. Summary

Why McDonald's Is Interesting

With nicknames spanning Mickey D's in the U.S. to Makku in Japan, McDonald’s (NYSE:MCD) is a fast-food behemoth known for its convenience and broken ice cream machines.

- Highly-profitable franchise model results in strong unit economics and a best-in-class gross margin of 57.1%

- Disciplined cost controls and effective management have materialized in a strong operating margin

- A drawback is its large revenue base makes it harder to increase sales quickly, and its annual revenue growth of 4.1% over the last six years was below our standards for the restaurant sector

McDonald's has some noteworthy aspects. If you believe in the company, the price looks fair.

Why Is Now The Time To Buy McDonald's?

At $315.72 per share, McDonald's trades at 24.7x forward P/E. Scanning the restaurant peers, we conclude that McDonald’s valuation is warranted for the business quality.

If you think the market is not giving the company enough credit for its fundamentals, now could be a good time to invest.

3. McDonald's (MCD) Research Report: Q4 CY2025 Update

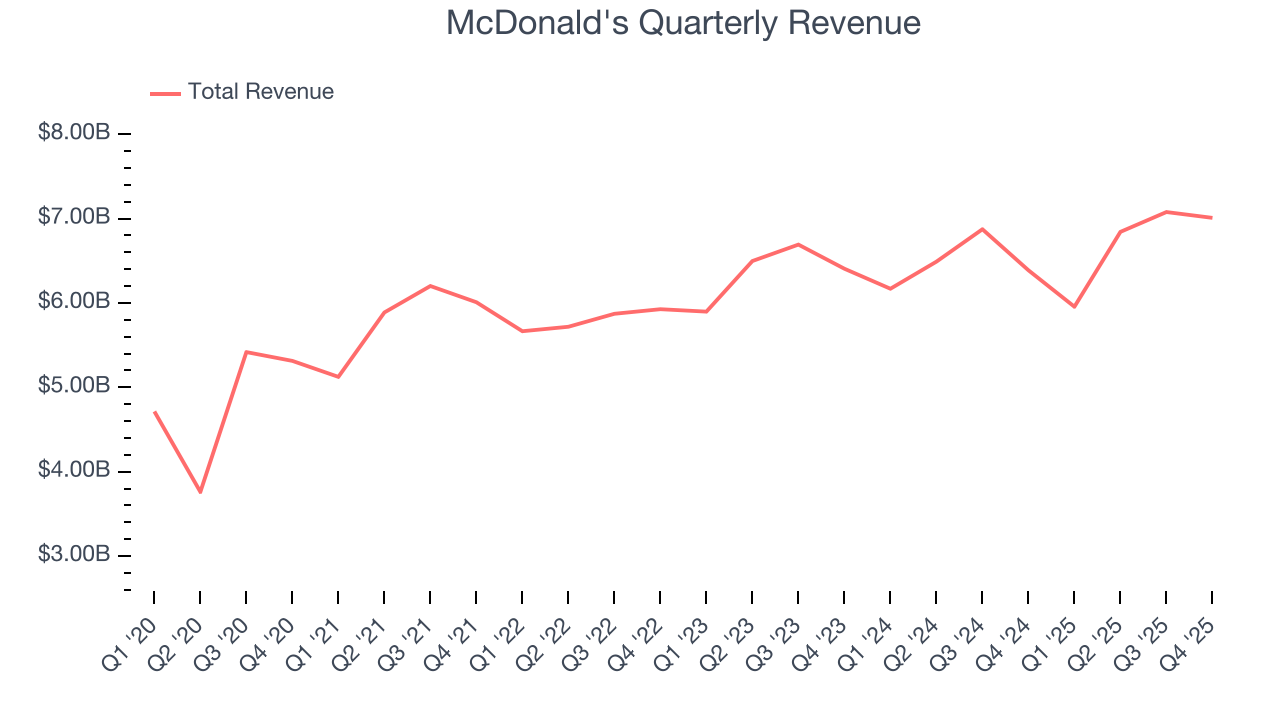

Fast-food chain McDonald’s (NYSE:MCD) reported Q4 CY2025 results topping the market’s revenue expectations, with sales up 9.7% year on year to $7.01 billion. Its non-GAAP profit of $3.12 per share was 2.2% above analysts’ consensus estimates.

McDonald's (MCD) Q4 CY2025 Highlights:

- Revenue: $7.01 billion vs analyst estimates of $6.83 billion (9.7% year-on-year growth, 2.6% beat)

- Adjusted EPS: $3.12 vs analyst estimates of $3.05 (2.2% beat)

- Adjusted EBITDA: $3.28 billion vs analyst estimates of $3.72 billion (46.8% margin, 11.8% miss)

- Operating Margin: 45%, in line with the same quarter last year

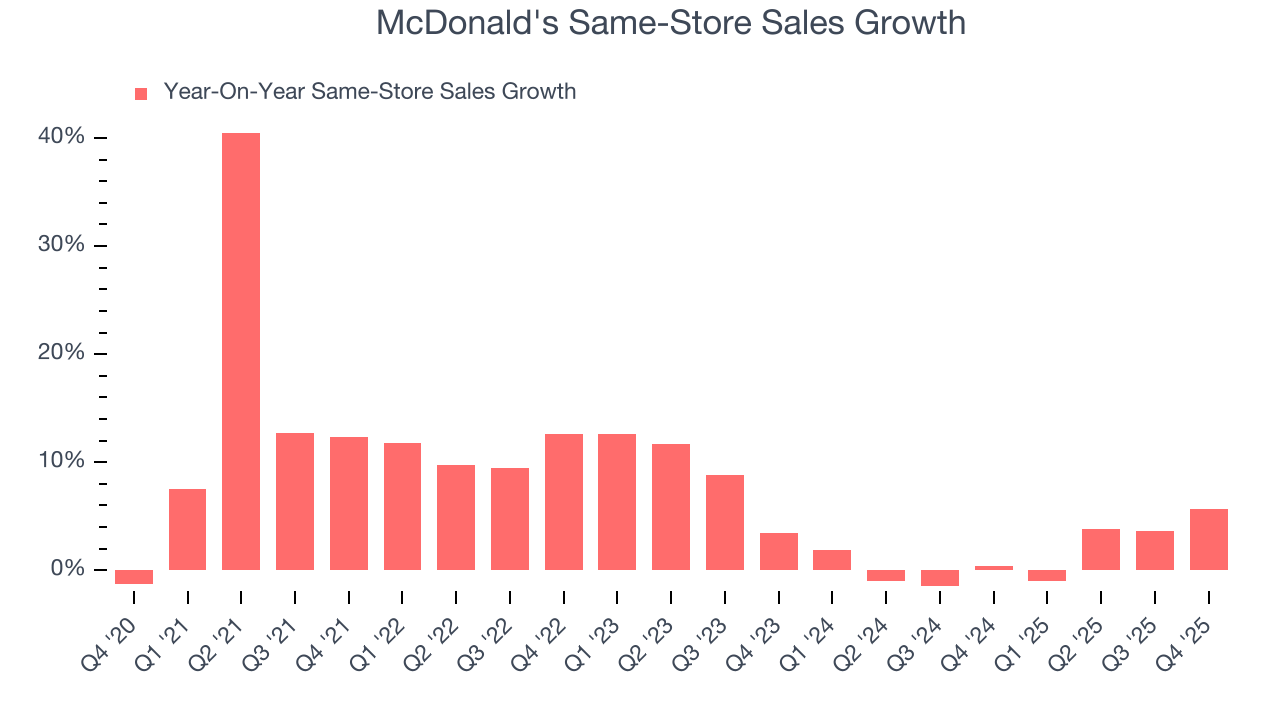

- Same-Store Sales rose 5.7% year on year (0.4% in the same quarter last year)

- Market Capitalization: $232.1 billion

Company Overview

With nicknames spanning Mickey D's in the U.S. to Makku in Japan, McDonald’s (NYSE:MCD) is a fast-food behemoth known for its convenience and broken ice cream machines.

The famous golden arches were first raised in 1940 by brothers Richard and Maurice McDonald. After achieving initial success at their flagship California location, the McDonald’s brothers were hungry for growth and reinvented their business in 1948 with the “Speedee Service System”, which used an assembly-line process to prepare food.

This invention laid the foundation for the fast-food concept we know today and enabled McDonald’s to deliver on its core value proposition of quick, affordable meals that don’t compromise on taste or quality. Since then, the company has evolved into the Zeitgeist of fast-food culture and expanded its menu to include not only burgers and french fries but also salads, wraps, breakfasts, and desserts.

The average McDonald’s store size varies, but most locations feature a counter for ordering, a seating area with a mix of booths and tables, and a drive-thru for added convenience. The layout is designed to serve both dine-in and takeout customers, with digital kiosks near the cash register to accommodate self-service customers who don’t want to wait in line.

The company has restaurants around the globe and is a leader in restaurant technology. It's not only built a popular mobile app but also has partnerships with leading delivery platforms such as DoorDash, Uber Eats, and Seamless (Grubhub) to meet consumers wherever they may be.

4. Traditional Fast Food

Traditional fast-food restaurants are renowned for their speed and convenience, boasting menus filled with familiar and budget-friendly items. Their reputations for on-the-go consumption make them favored destinations for individuals and families needing a quick meal. This class of restaurants, however, is fighting the perception that their meals are unhealthy and made with inferior ingredients, a battle that's especially relevant today given the consumers increasing focus on health and wellness.

Fast-food competitors include Burger King and Popeyes (owned by Restaurant Brands International, NYSE:QSR), Jack in the Box (NASDAQ:JACK), Taco Bell and KFC (owned by Yum! Brands, NYSE:YUM), and Wendy’s (NASDAQ:WEN).

5. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $26.89 billion in revenue over the past 12 months, McDonald's is one of the most widely recognized restaurant chains and benefits from customer loyalty, a luxury many don’t have. Its scale also gives it negotiating leverage with suppliers, enabling it to source its ingredients at a lower cost. However, its scale is a double-edged sword because it’s harder to find incremental growth when your existing restaurant banners have penetrated most of the market. To accelerate system-wide sales, McDonald's likely needs to optimize its pricing or lean into new chains and international expansion.

As you can see below, McDonald’s sales grew at a sluggish 4.1% compounded annual growth rate over the last six years as it barely increased sales at existing, established dining locations.

This quarter, McDonald's reported year-on-year revenue growth of 9.7%, and its $7.01 billion of revenue exceeded Wall Street’s estimates by 2.6%.

Looking ahead, sell-side analysts expect revenue to grow 5.2% over the next 12 months, similar to its six-year rate. Although this projection implies its newer menu offerings will catalyze better top-line performance, it is still below the sector average. At least the company is tracking well in other measures of financial health.

6. Restaurant Performance

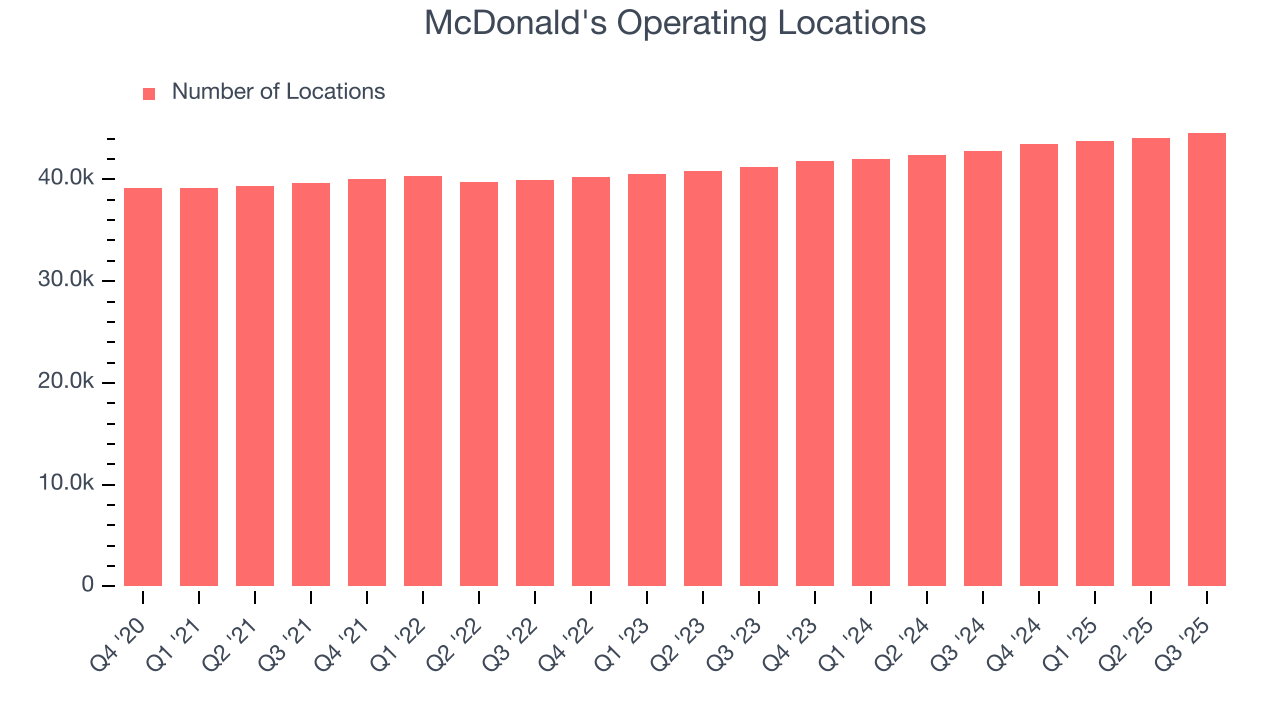

Number of Restaurants

A restaurant chain’s total number of dining locations often determines how much revenue it can generate.

McDonald's opened new restaurants at a rapid clip over the last two years, averaging 4% annual growth, much faster than the broader restaurant sector. Furthermore, one dynamic making expansion more seamless is the company’s franchise model, where franchisees are primarily responsible for opening new restaurants while McDonald's provides support.

When a chain opens new restaurants, it usually means it’s investing for growth because there’s healthy demand for its meals and there are markets where its concepts have few or no locations.

Note that McDonald's reports its restaurant count intermittently, so some data points are missing in the chart below.

Same-Store Sales

A company's restaurant base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales is an industry measure of whether revenue is growing at those existing restaurants and is driven by customer visits (often called traffic) and the average spending per customer (ticket).

McDonald’s demand within its existing dining locations has been relatively stable over the last two years but was below most restaurant chains. On average, the company’s same-store sales have grown by 1.5% per year. This performance suggests it should consider improving its foot traffic and efficiency before expanding its restaurant base.

In the latest quarter, McDonald’s same-store sales rose 5.7% year on year. This growth was an acceleration from its historical levels, which is always an encouraging sign.

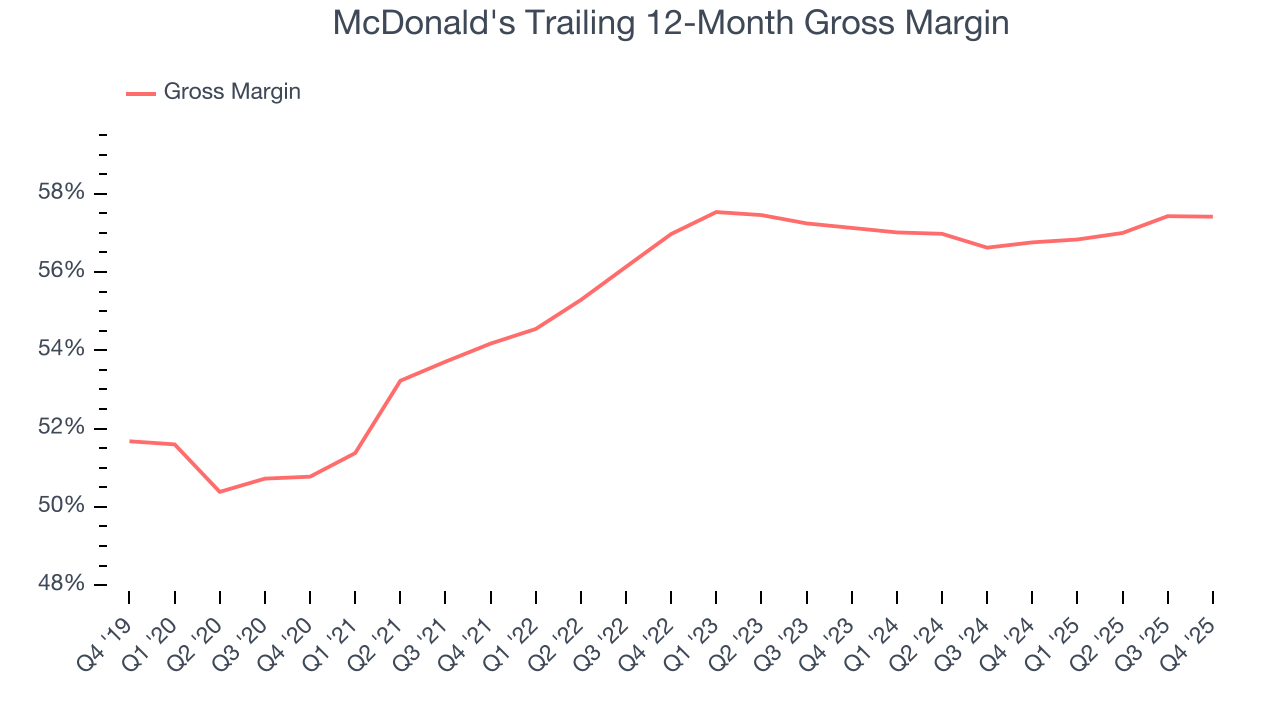

7. Gross Margin & Pricing Power

We prefer higher gross margins because they not only make it easier to generate more operating profits but also indicate pricing power and differentiation, whether it be the dining experience or quality and taste of food.

McDonald's has best-in-class unit economics for a restaurant company, enabling it to invest in areas such as marketing and talent to grow its brand. As you can see below, it averaged an elite 57.1% gross margin over the last two years. Said differently, roughly $57.09 was left to spend on selling, marketing, and general administrative overhead for every $100 in revenue.

In Q4, McDonald's produced a 57.5% gross profit margin, in line with the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs (such as ingredients and transportation expenses) have been stable and it isn’t under pressure to lower prices.

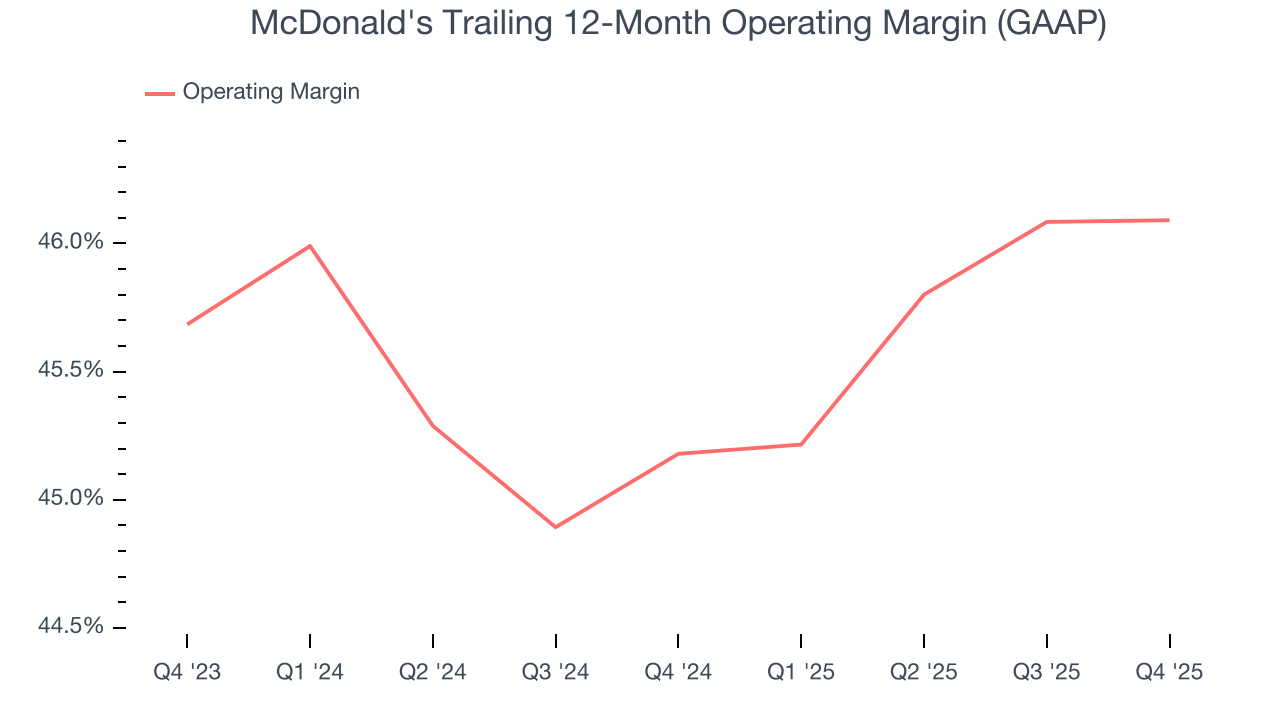

8. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

McDonald’s operating margin might fluctuated slightly over the last 12 months but has generally stayed the same, averaging 45.6% over the last two years. This profitability was elite for a restaurant business thanks to its efficient cost structure and economies of scale. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Looking at the trend in its profitability, McDonald’s operating margin might fluctuated slightly but has generally stayed the same over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q4, McDonald's generated an operating margin profit margin of 45%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

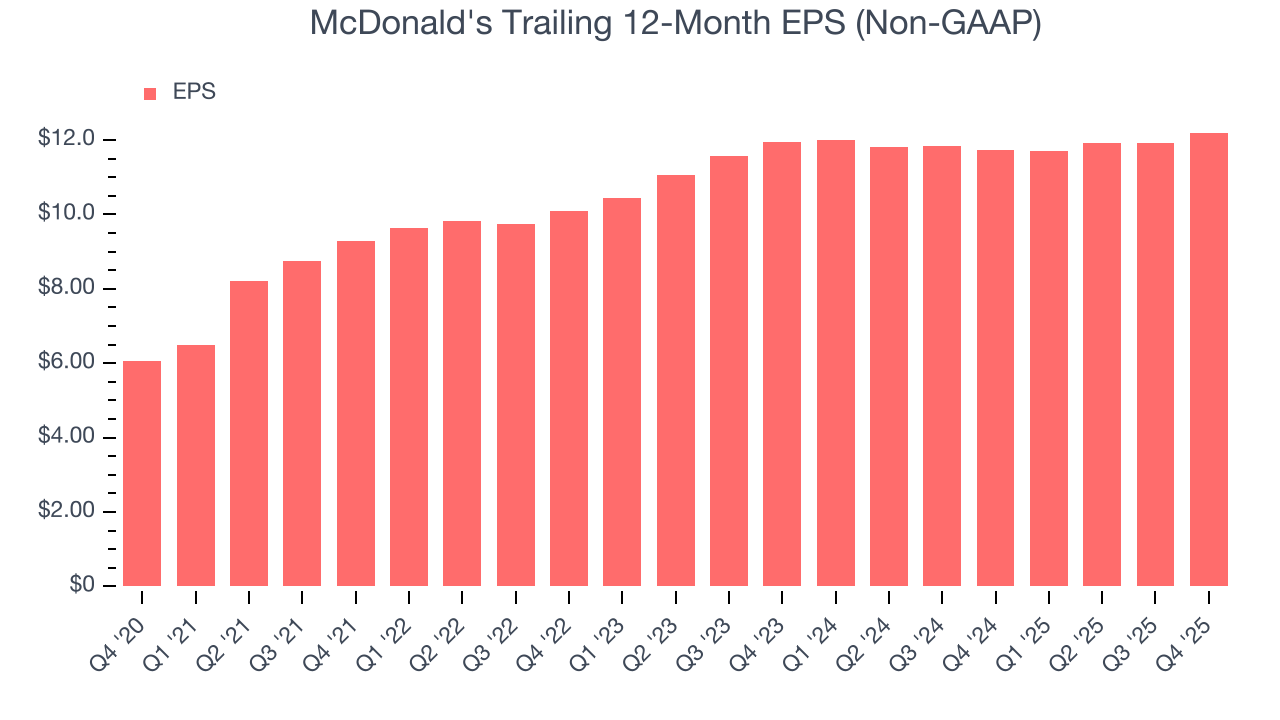

9. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

McDonald’s EPS grew at an unimpressive 7.6% compounded annual growth rate over the last six years. On the bright side, this performance was better than its 4.1% annualized revenue growth and tells us the company became more profitable on a per-share basis as it expanded.

In Q4, McDonald's reported adjusted EPS of $3.12, up from $2.83 in the same quarter last year. This print beat analysts’ estimates by 2.2%. Over the next 12 months, Wall Street expects McDonald’s full-year EPS of $12.20 to grow 9%.

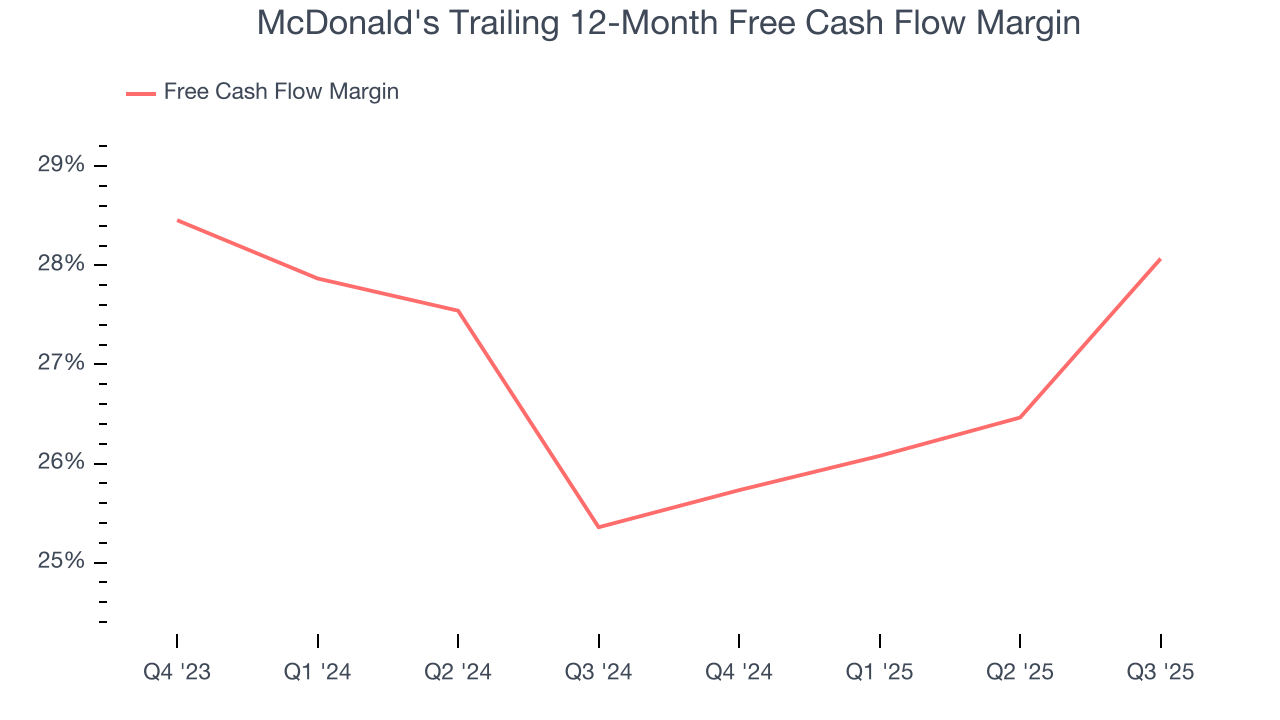

10. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

McDonald's has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition. The company’s free cash flow margin was among the best in the restaurant sector, averaging 26.7% over the last two years.

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

McDonald’s five-year average ROIC was 27.7%, placing it among the best restaurant companies. This illustrates its management team’s ability to invest in highly profitable ventures and produce tangible results for shareholders.

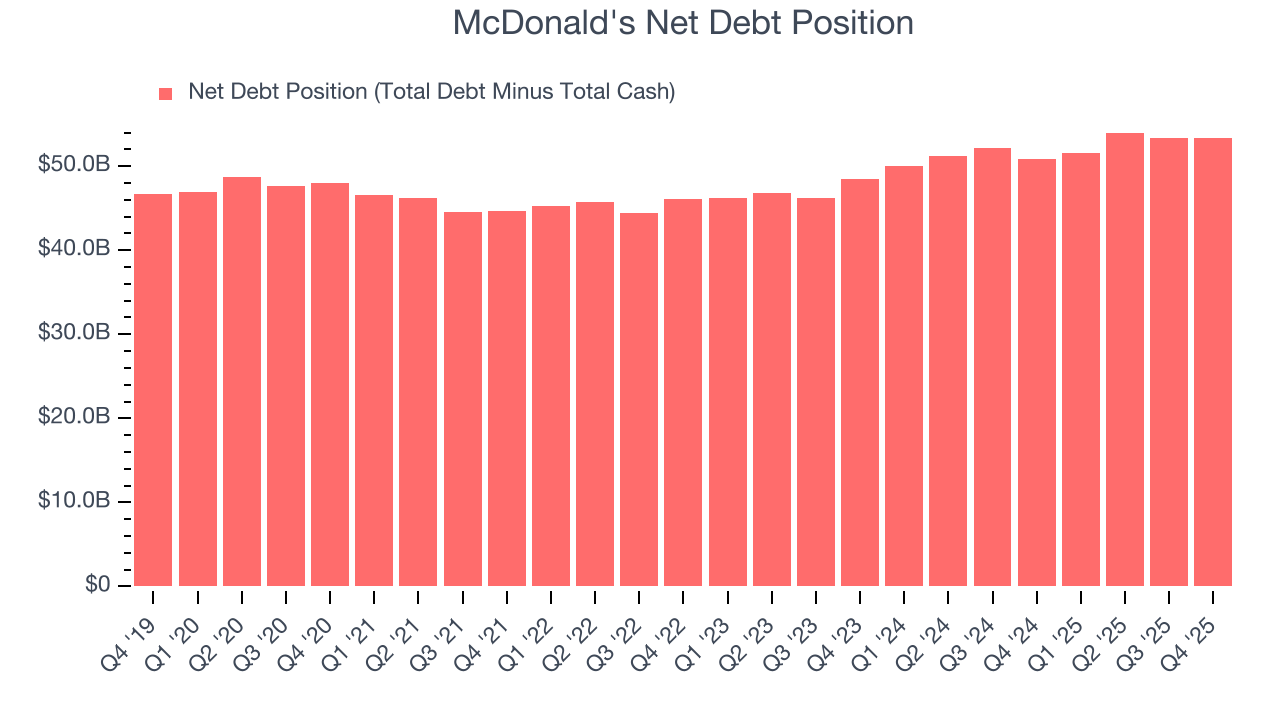

12. Balance Sheet Assessment

McDonald's reported $774 million of cash and $54.12 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $14.29 billion of EBITDA over the last 12 months, we view McDonald’s 3.7× net-debt-to-EBITDA ratio as safe. We also see its $699 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

13. Key Takeaways from McDonald’s Q4 Results

We were impressed by how significantly McDonald's blew past analysts’ same-store sales expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. On the other hand, its EBITDA missed. Overall, this print had some key positives. The stock remained flat at $321.20 immediately following the results.

14. Is Now The Time To Buy McDonald's?

Updated: March 18, 2026 at 10:51 PM EDT

Are you wondering whether to buy McDonald's or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

McDonald's is a fine business. Although its revenue growth was uninspiring over the last six years, its growth over the next 12 months is expected to be higher. And while McDonald’s projected EPS for the next year is lacking, its new restaurant openings have increased its brand equity. On top of that, its admirable gross margins are a wonderful starting point for the overall profitability of the business.

McDonald’s P/E ratio based on the next 12 months is 24.7x. Looking at the restaurant landscape right now, McDonald's trades at a pretty interesting price. If you trust the business and its direction, this is an ideal time to buy.

Wall Street analysts have a consensus one-year price target of $343.28 on the company (compared to the current share price of $315.72), implying they see 8.7% upside in buying McDonald's in the short term.