Medifast (MED)

Medifast is in for a bumpy ride. Its shrinking sales suggest demand is waning and its lousy free cash flow generation doesn’t do it any favors.― StockStory Analyst Team

1. News

2. Summary

Why We Think Medifast Will Underperform

Known for its Optavia program that combines portion-controlled meal replacements with coaching, Medifast (NYSE:MED) has a broad product portfolio of bars, snacks, drinks, and desserts for those looking to lose weight or consume healthier foods.

- Annual sales declines of 36% for the past three years show its products struggled to connect with the market

- Forecasted revenue decline of 22% for the upcoming 12 months implies demand will fall even further

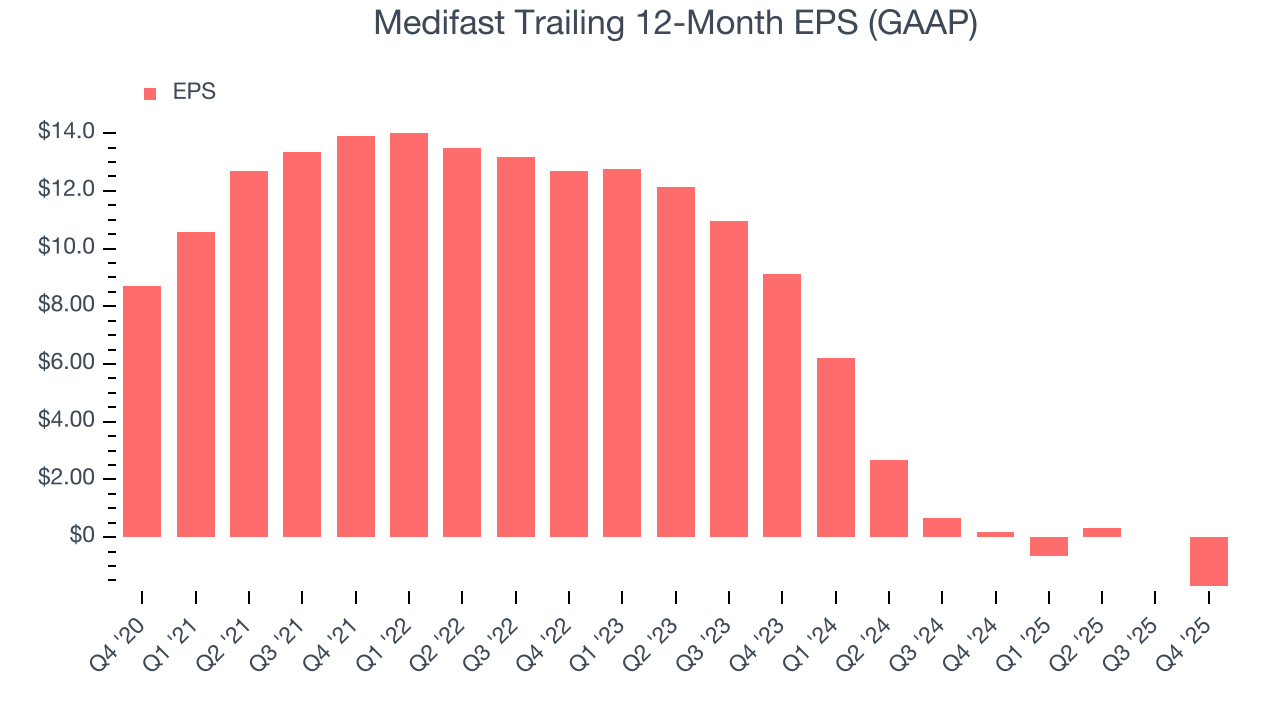

- Earnings per share decreased by more than its revenue over the last three years, showing each sale was less profitable

Medifast is in the penalty box. There are more appealing investments to be made.

Why There Are Better Opportunities Than Medifast

At $10.77 per share, Medifast trades at 3.4x forward EV-to-EBITDA. This sure is a cheap multiple, but you get what you pay for.

We’d rather pay up for companies with elite fundamentals than get a bargain on weak ones. Cheap stocks can be value traps, and as their performance deteriorates, they will stay cheap or get even cheaper.

3. Medifast (MED) Research Report: Q4 CY2025 Update

Wellness company Medifast (NYSE:MED) announced better-than-expected revenue in Q4 CY2025, but sales fell by 36.9% year on year to $75.1 million. On the other hand, next quarter’s revenue guidance of $72.5 million was less impressive, coming in 15.2% below analysts’ estimates. Its GAAP loss of $1.65 per share was significantly below analysts’ consensus estimates.

Medifast (MED) Q4 CY2025 Highlights:

- Revenue: $75.1 million vs analyst estimates of $71.4 million (36.9% year-on-year decline, 5.2% beat)

- EPS (GAAP): -$1.65 vs analyst estimates of -$0.82 (significant miss)

- Revenue Guidance for Q1 CY2026 is $72.5 million at the midpoint, below analyst estimates of $85.5 million

- EPS (GAAP) guidance for the upcoming financial year 2026 is -$2.15 at the midpoint, missing analyst estimates by 33.5%

- Operating Margin: -10.4%, down from 0.6% in the same quarter last year

- Market Capitalization: $110.7 million

Company Overview

Known for its Optavia program that combines portion-controlled meal replacements with coaching, Medifast (NYSE:MED) has a broad product portfolio of bars, snacks, drinks, and desserts for those looking to lose weight or consume healthier foods.

The company was founded in 1980 by Dr. William Vitale. It initially provided weight-loss solutions directly to doctors, who would then pass them on to patients. While the company initially grew organically through its doctor-driven model, a notable 2010 acquisition of a digital platform has allowed Medifast to establish an online presence.

Today, Medifast is known for its Optavia program. The company also offers bars, snacks such as pretzels and puffs, drinks, and soups that help customers maintain or lose weight. Medifast targets individuals looking to adopt a healthier lifestyle. These are individuals who may have struggled with their weight and found other dieting approaches unsuccessful.

In addition to the products themselves, Medifast offers personal coaching. The coaching aspect is how Medifast facilitates a multi-level marketing approach to selling. Coaches are often customers who sign on to make money by purchasing Medifast products at wholesale prices and selling them at retail to clients.

The multi-level marketing model also lets coaches earn a portion of earnings from other coaches they recruit into the Medifast ecosystem. This model is sometimes a source of skepticism, though. Some argue that these models rely mostly on recruitment to sustain themselves rather than actual demand for products.

4. Personal Care

While personal care products products may seem more discretionary than food, consumers tend to maintain or even boost their spending on the category during tough times. This phenomenon is known as "the lipstick effect" by economists, which states that consumers still want some semblance of affordable luxuries like beauty and wellness when the economy is sputtering. Consumer tastes are constantly changing, and personal care companies are currently responding to the public’s increased desire for ethically produced goods by featuring natural ingredients in their products.

Multi-level marketing companies offering health and wellness supplements and products include Herbalife (NYSE:HLF), USANA Health Sciences (NYSE:USNA), and Nature’s Sunshine Products (NASDAQ:NATR).

5. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

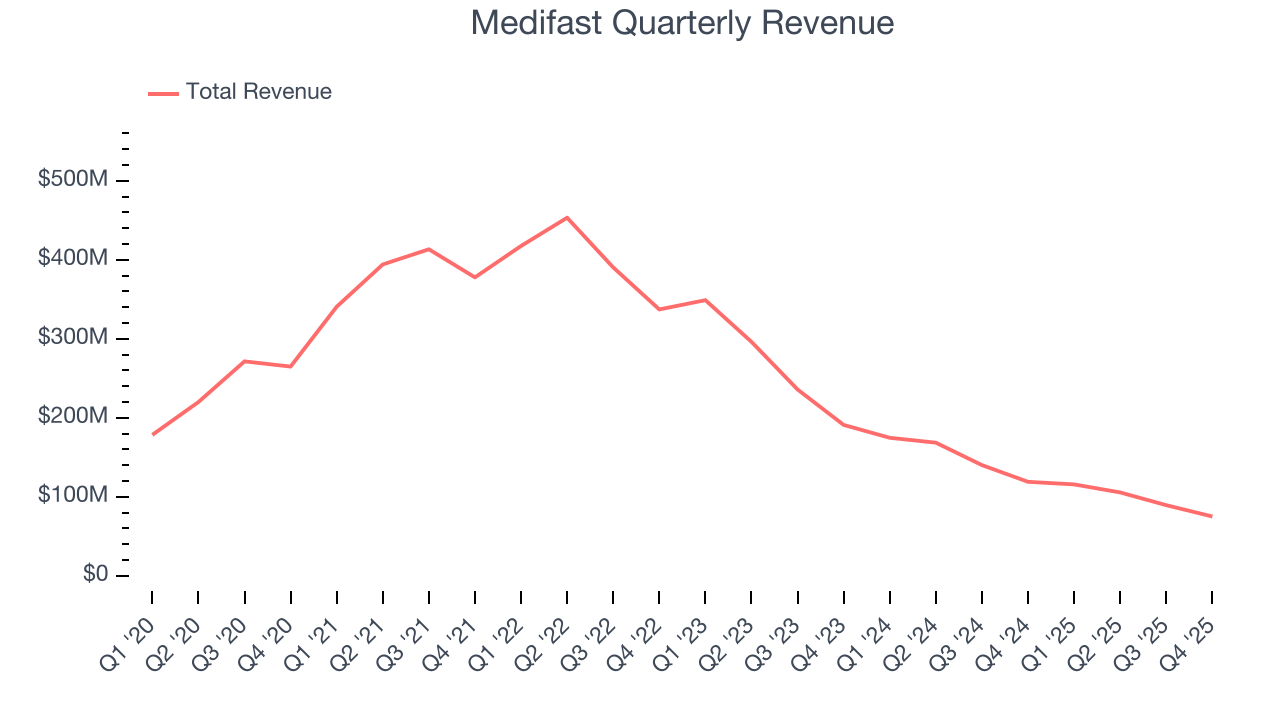

With $385.8 million in revenue over the past 12 months, Medifast is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

As you can see below, Medifast struggled to generate demand over the last three years. Its sales dropped by 37.7% annually, a rough starting point for our analysis.

This quarter, Medifast’s revenue fell by 36.9% year on year to $75.1 million but beat Wall Street’s estimates by 5.2%. Company management is currently guiding for a 37.4% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to decline by 12.5% over the next 12 months. it’s tough to feel optimistic about a company facing demand difficulties.

6. Gross Margin & Pricing Power

At StockStory, we prefer high gross margin businesses because they indicate pricing power or differentiated products, giving the company a chance to generate higher operating profits.

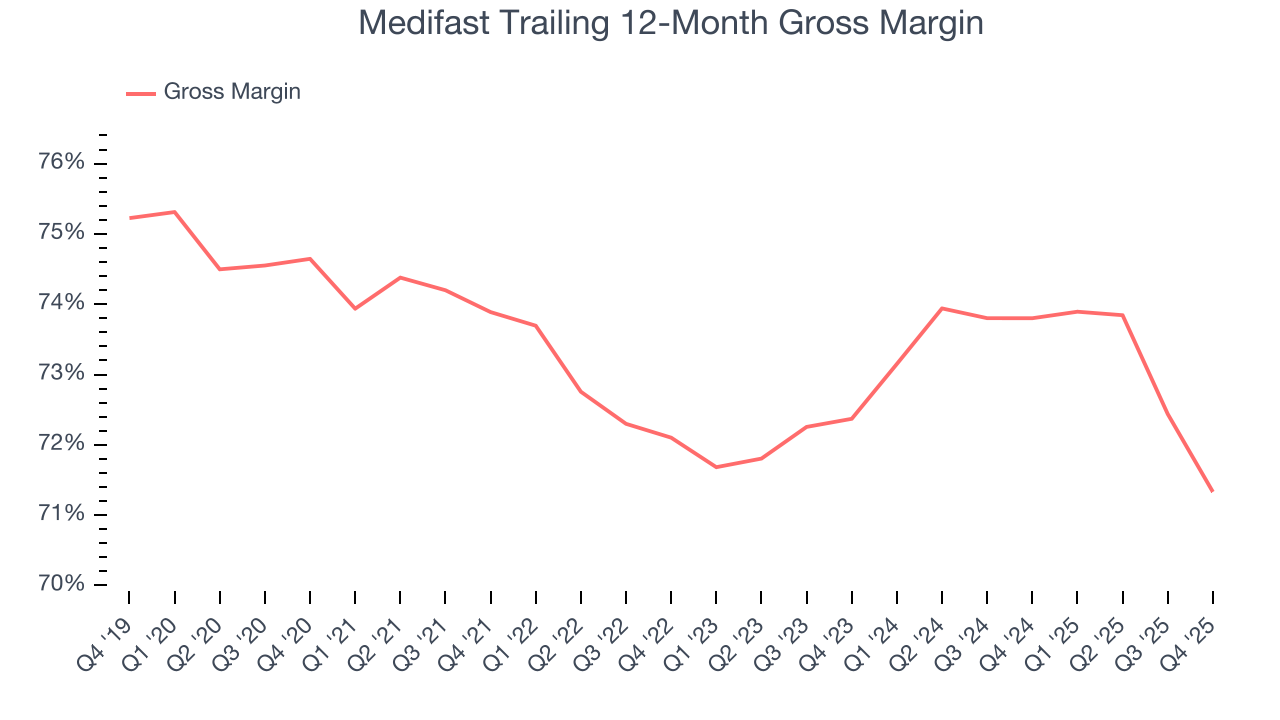

Medifast has best-in-class unit economics for a consumer staples company, enabling it to invest in areas such as marketing and talent to grow its brand. As you can see below, it averaged an elite 72.8% gross margin over the last two years. That means for every $100 in revenue, only $27.16 went towards paying for raw materials, production of goods, transportation, and distribution.

Medifast produced a 69.4% gross profit margin in Q4 , marking a 4.7 percentage point decrease from 74.1% in the same quarter last year. Medifast’s full-year margin has also been trending down over the past 12 months, decreasing by 2.5 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to lower prices and higher input costs (such as raw materials and manufacturing expenses).

7. Operating Margin

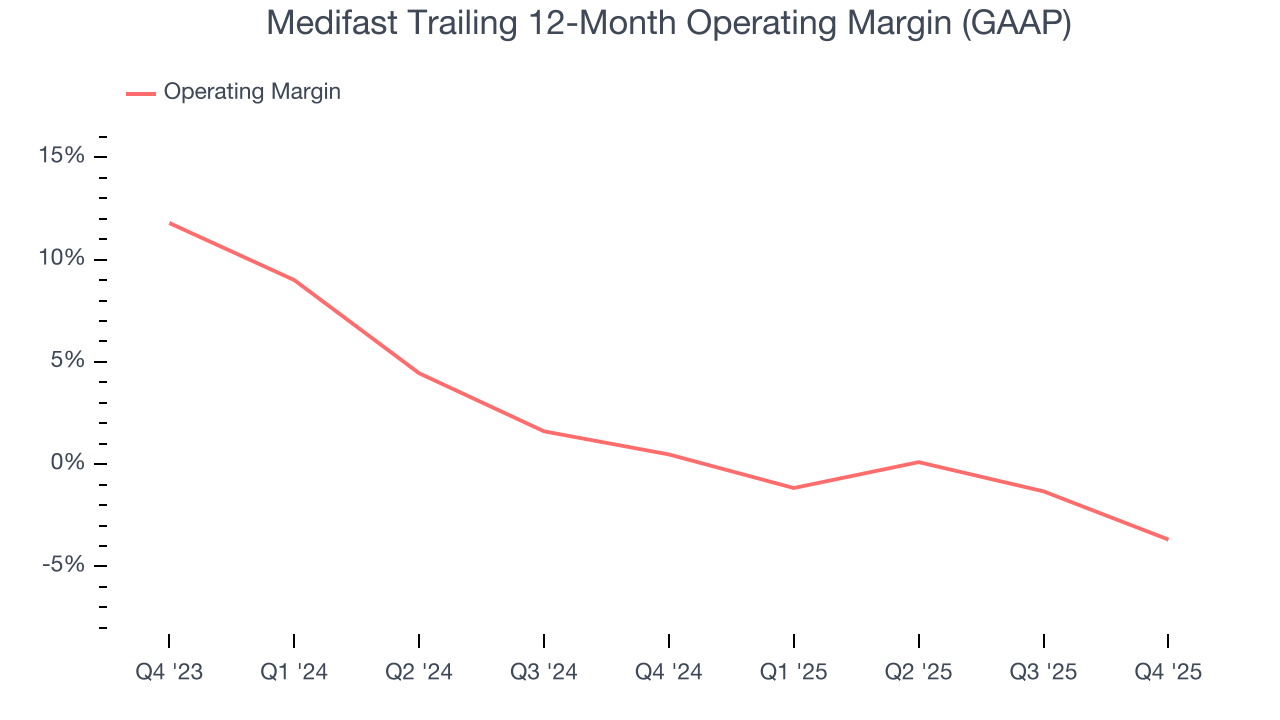

Unprofitable public companies are rare in the defensive consumer staples industry. Unfortunately, Medifast was one of them over the last two years as its high expenses contributed to an average operating margin of negative 1.1%.

Looking at the trend in its profitability, Medifast’s operating margin decreased by 4.2 percentage points over the last year. Medifast’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

In Q4, Medifast generated a negative 10.4% operating margin. The company's consistent lack of profits raise a flag.

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Medifast, its EPS and revenue declined by 28.8% and 37.7% annually over the last three years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Medifast’s low margin of safety could leave its stock price susceptible to large downswings.

In Q4, Medifast reported EPS of negative $1.65, down from $0.07 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Medifast to improve its earnings losses. Analysts forecast its full-year EPS of negative $1.71 will advance to negative $1.61.

9. Cash Is King

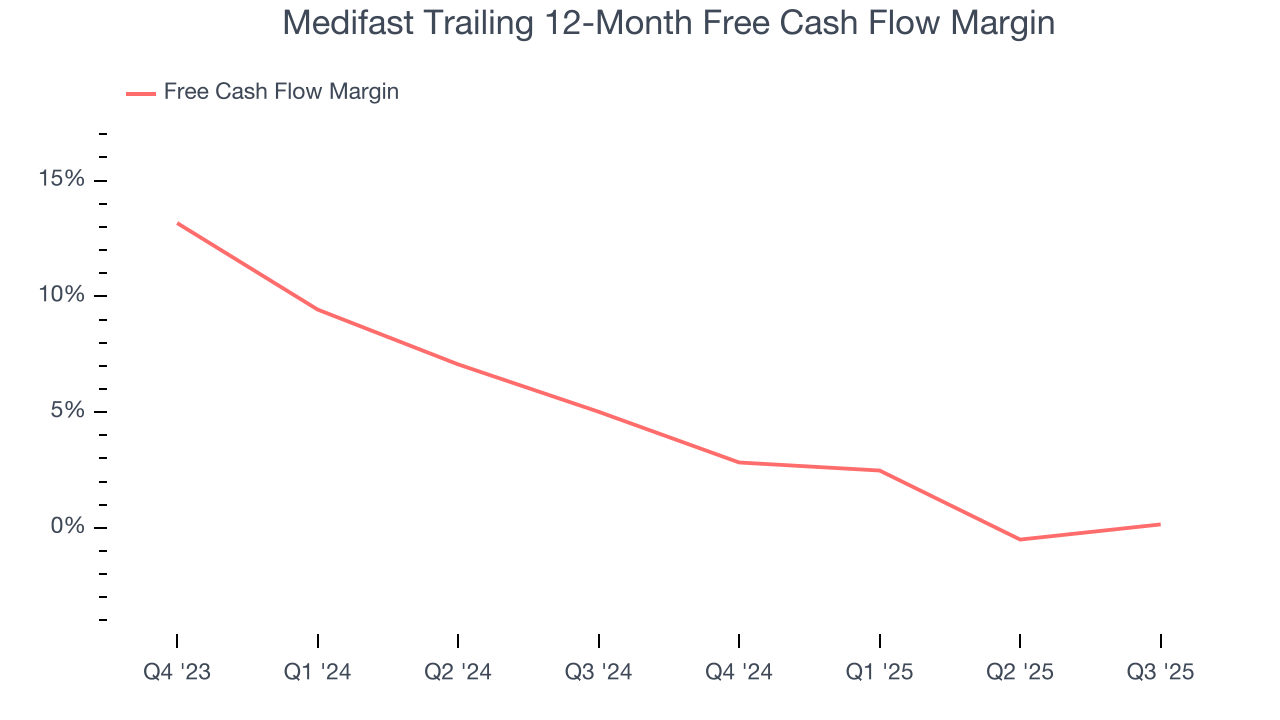

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Medifast has shown weak cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 2.7%, subpar for a consumer staples business.

10. Key Takeaways from Medifast’s Q4 Results

We enjoyed seeing Medifast beat analysts’ revenue expectations this quarter. We were also happy its gross margin outperformed Wall Street’s estimates. On the other hand, its full-year revenue guidance missed and its full-year EPS guidance fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 2.4% to $10.52 immediately following the results.

11. Is Now The Time To Buy Medifast?

Updated: February 17, 2026 at 9:52 PM EST

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Medifast.

We see the value of companies helping consumers, but in the case of Medifast, we’re out. First off, its revenue has declined over the last three years. While its admirable gross margins are a wonderful starting point for the overall profitability of the business, the downside is its brand caters to a niche market. On top of that, its declining EPS over the last three years makes it a less attractive asset to the public markets.

Medifast’s EV-to-EBITDA ratio based on the next 12 months is 3.5x. While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $15 on the company (compared to the current share price of $11.00).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.