Methode Electronics (MEI)

Methode Electronics faces an uphill battle. Not only are its sales cratering but also its low returns on capital suggest it struggles to generate profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think Methode Electronics Will Underperform

Founded in 1946, Methode Electronics (NYSE:MEI) is a global supplier of custom-engineered solutions for Original Equipment Manufacturers (OEMs).

- Products and services are facing end-market challenges during this cycle, as seen in its flat sales over the last five years

- Performance over the past five years shows each sale was less profitable, as its earnings per share fell by 19.5% annually

- 6× net-debt-to-EBITDA ratio makes lenders less willing to extend additional capital, potentially necessitating dilutive equity offerings

Methode Electronics’s quality is not up to our standards. We see more lucrative opportunities elsewhere.

Why There Are Better Opportunities Than Methode Electronics

At $7.30 per share, Methode Electronics trades at 126.3x forward P/E. This valuation multiple seems a bit much considering the tepid revenue growth profile.

We’d rather invest in similarly-priced but higher-quality companies with more reliable earnings growth.

3. Methode Electronics (MEI) Research Report: Q3 CY2025 Update

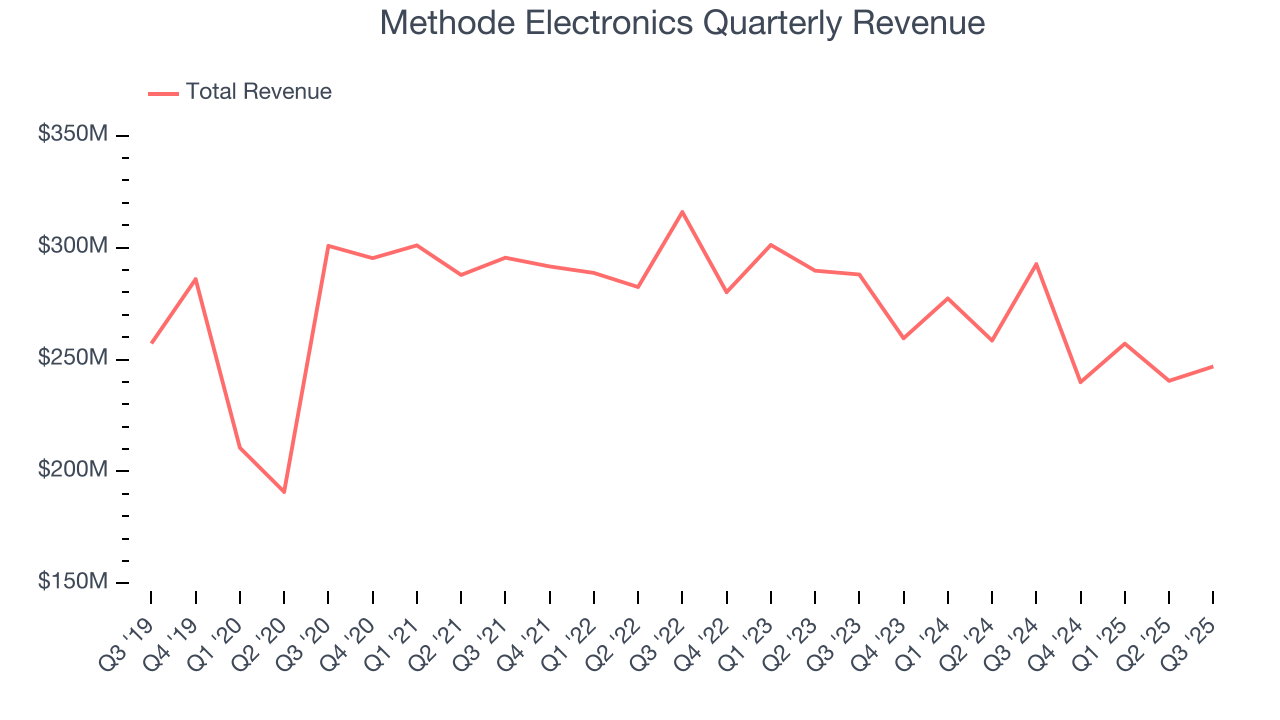

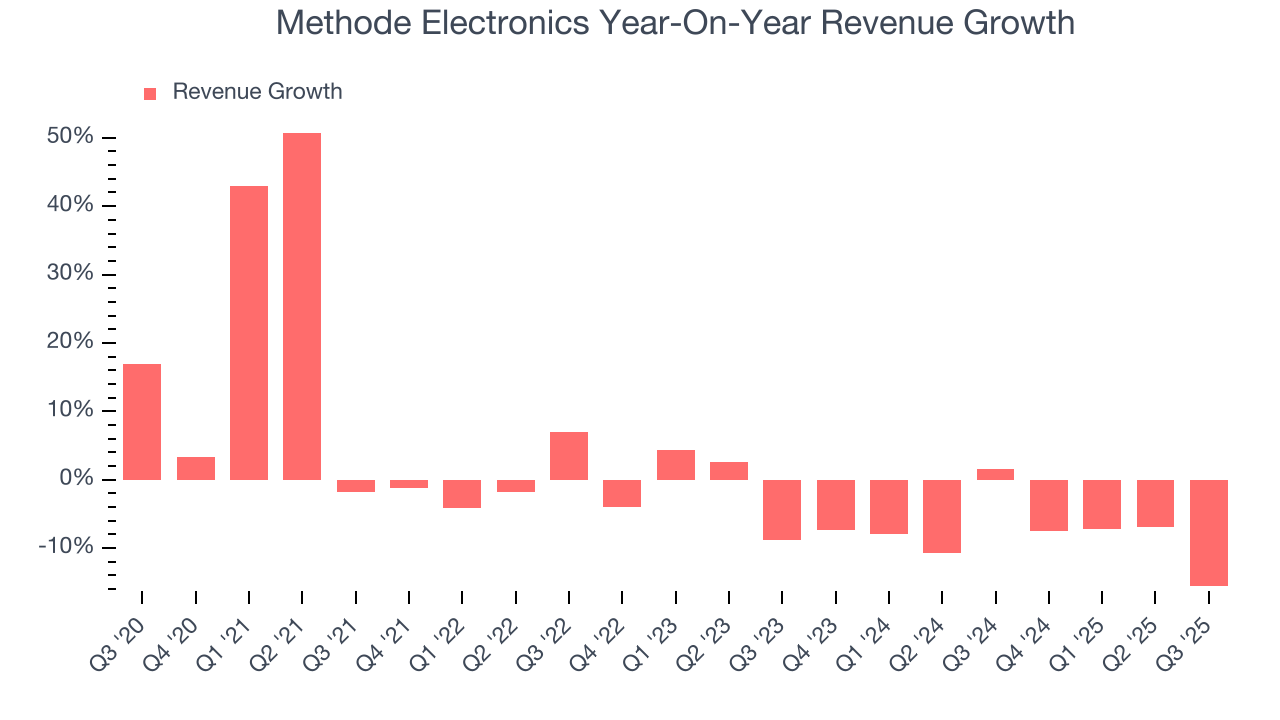

Custom-engineered solutions manufacturer Methode Electronics (NYSE:MEI) beat Wall Street’s revenue expectations in Q3 CY2025, but sales fell by 15.6% year on year to $246.9 million. The company expects the full year’s revenue to be around $950 million, close to analysts’ estimates. Its non-GAAP loss of $0.19 per share was in line with analysts’ consensus estimates.

Methode Electronics (MEI) Q3 CY2025 Highlights:

- Revenue: $246.9 million vs analyst estimates of $237.7 million (15.6% year-on-year decline, 3.9% beat)

- Adjusted EPS: -$0.19 vs analyst estimates of -$0.20 (in line)

- Adjusted EBITDA: $17.6 million vs analyst estimates of $15.27 million (7.1% margin, 15.2% beat)

- The company reconfirmed its revenue guidance for the full year of $950 million at the midpoint

- EBITDA guidance for the full year is $75 million at the midpoint, above analyst estimates of $73.53 million

- Operating Margin: 1.2%, down from 3.2% in the same quarter last year

- Free Cash Flow was -$11.6 million compared to -$58.4 million in the same quarter last year

- Market Capitalization: $292.3 million

Company Overview

Founded in 1946, Methode Electronics (NYSE:MEI) is a global supplier of custom-engineered solutions for Original Equipment Manufacturers (OEMs).

Founded in 1946, the company serves diverse markets including automotive, cloud computing, construction equipment, consumer appliances, and medical devices. It maintains manufacturing and engineering locations across North America, Europe, the Middle East, and Asia.

Methode Electronics operates through four segments: 1) Automotive, which supplies electronic and electro-mechanical devices to automobile OEMs, 2) Industrial, which manufactures lighting solutions, safety controls, and power distribution products, 3) Interface, which provides transceivers, user interface solutions, and sensors for various markets, and 4) Medical, which develops injury prevention equipment.

Methode Electronics builds long-term relationships with its customers, particularly in the automotive industry where its largest customer is General Motors. The company's revenue comes primarily from selling custom-engineered solutions to OEMs, with their top five customers accounting for about half of sales.

The company will occasionally make acquisitions to grow its product portfolio, such as in April 2023 when it significantly expanded its industrial lighting capabilities by acquiring Nordic Lights Group Corporation.

4. Electrical Systems

Like many equipment and component manufacturers, electrical systems companies are buoyed by secular trends such as connectivity and industrial automation. More specific pockets of strong demand include Internet of Things (IoT) connectivity and the 5G telecom upgrade cycle, which can benefit companies whose cables and conduits fit those needs. But like the broader industrials sector, these companies are also at the whim of economic cycles. Interest rates, for example, can greatly impact projects that drive demand for these products.

Competitors of Methode Electronics include Amphenol Corporation (NYSE: APH), TE Connectivity Ltd. (NYSE: TEL), and Molex Incorporated (NASDAQ: MOLX).

5. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Unfortunately, Methode Electronics struggled to consistently increase demand as its $984.4 million of sales for the trailing 12 months was close to its revenue five years ago. This wasn’t a great result and suggests it’s a low quality business.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Methode Electronics’s recent performance shows its demand remained suppressed as its revenue has declined by 7.8% annually over the last two years.

This quarter, Methode Electronics’s revenue fell by 15.6% year on year to $246.9 million but beat Wall Street’s estimates by 3.9%.

Looking ahead, sell-side analysts expect revenue to decline by 1.3% over the next 12 months. Although this projection is better than its two-year trend, it’s hard to get excited about a company that is struggling with demand.

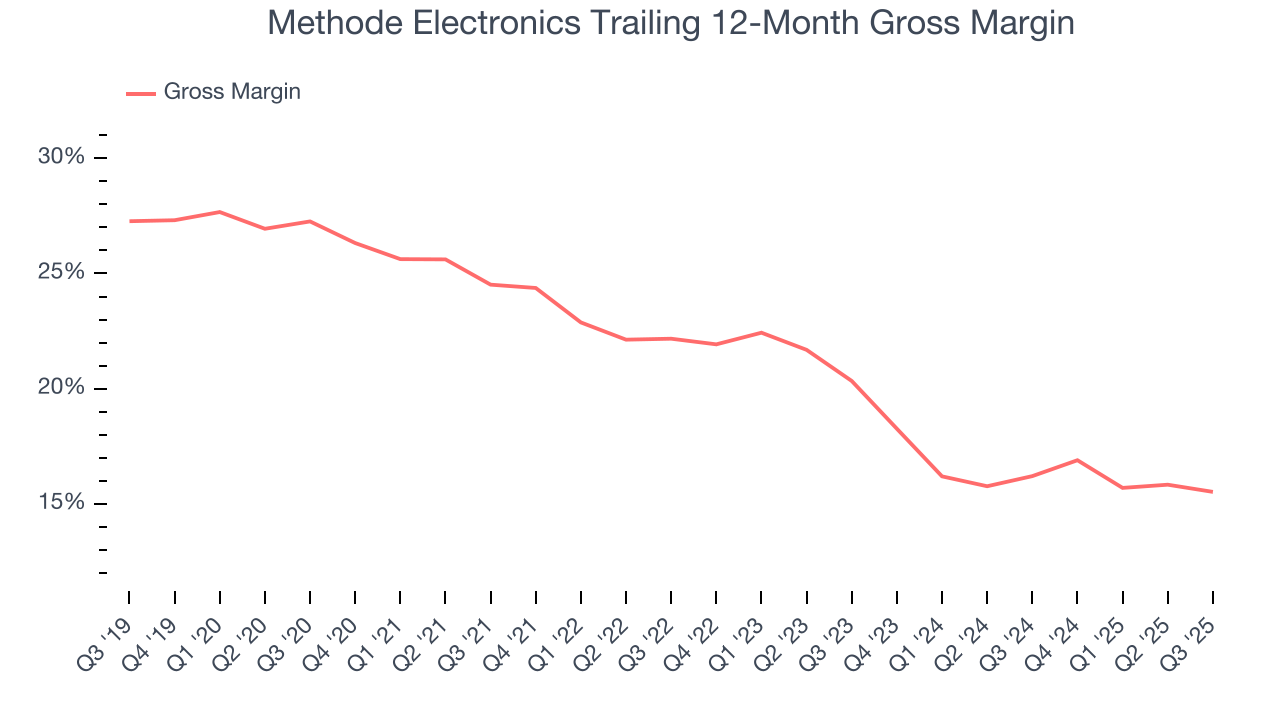

6. Gross Margin & Pricing Power

All else equal, we prefer higher gross margins because they usually indicate that a company sells more differentiated products and commands stronger pricing power.

Methode Electronics has bad unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a 20% gross margin over the last five years. Said differently, Methode Electronics had to pay a chunky $80.05 to its suppliers for every $100 in revenue.

This quarter, Methode Electronics’s gross profit margin was 19.3%, in line with the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

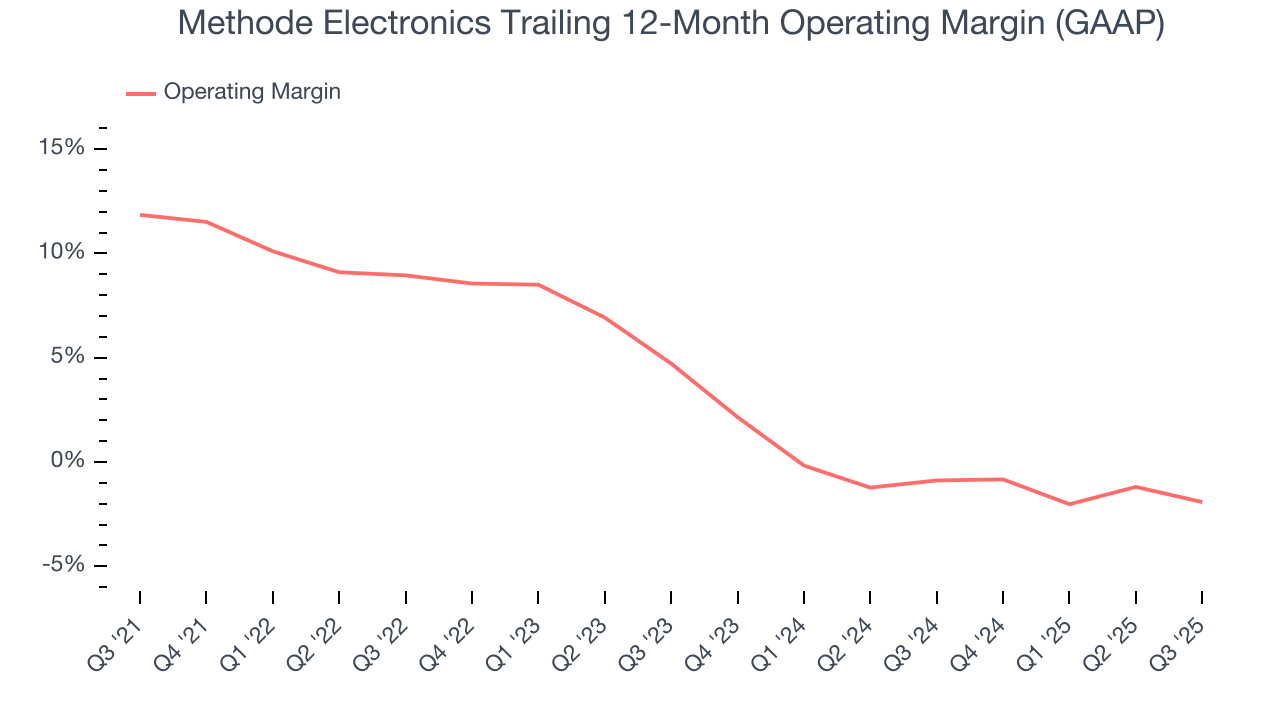

7. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Methode Electronics was profitable over the last five years but held back by its large cost base. Its average operating margin of 4.9% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

Looking at the trend in its profitability, Methode Electronics’s operating margin decreased by 13.8 percentage points over the last five years. Methode Electronics’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

In Q3, Methode Electronics generated an operating margin profit margin of 1.2%, down 2.1 percentage points year on year. Since Methode Electronics’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

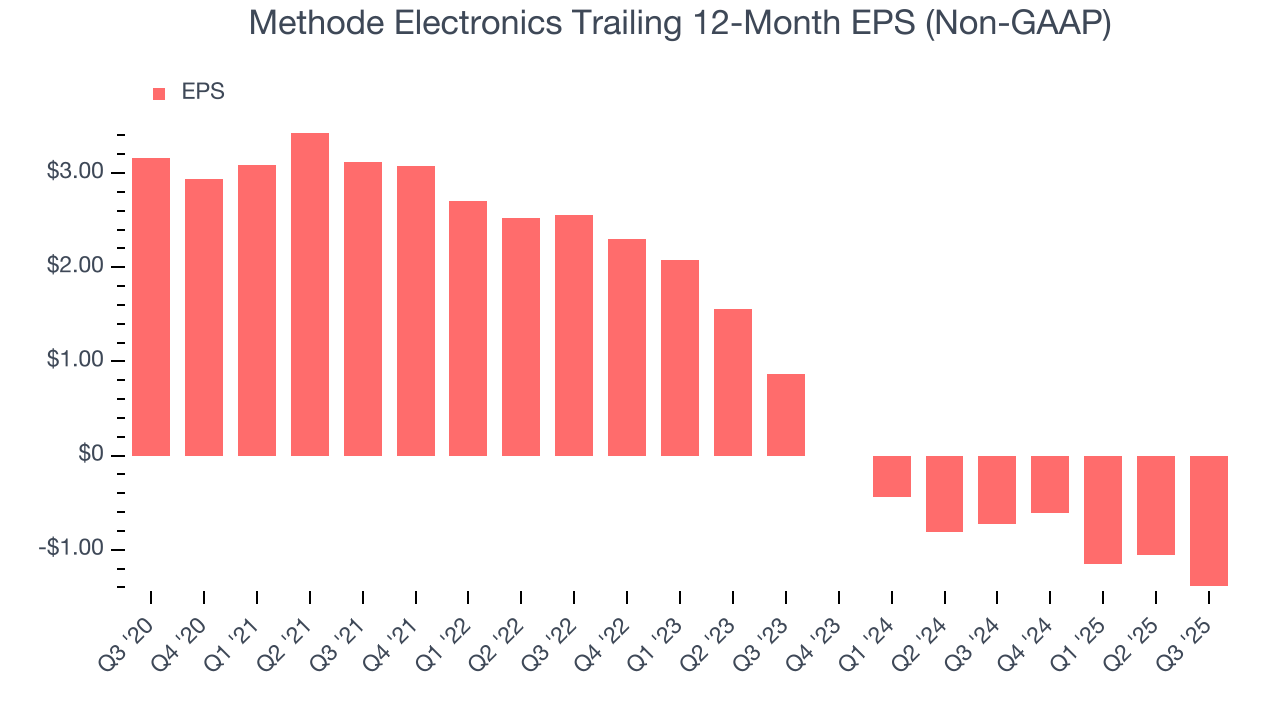

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Methode Electronics, its EPS declined by 19.5% annually over the last five years while its revenue was flat. This tells us the company struggled because its fixed cost base made it difficult to adjust to choppy demand.

Diving into the nuances of Methode Electronics’s earnings can give us a better understanding of its performance. As we mentioned earlier, Methode Electronics’s operating margin declined by 13.8 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Methode Electronics, its two-year annual EPS declines of 89.7% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q3, Methode Electronics reported adjusted EPS of negative $0.19, down from $0.14 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 2.6%. Over the next 12 months, Wall Street is optimistic. Analysts forecast Methode Electronics’s full-year EPS of negative $1.39 will flip to positive $0.41.

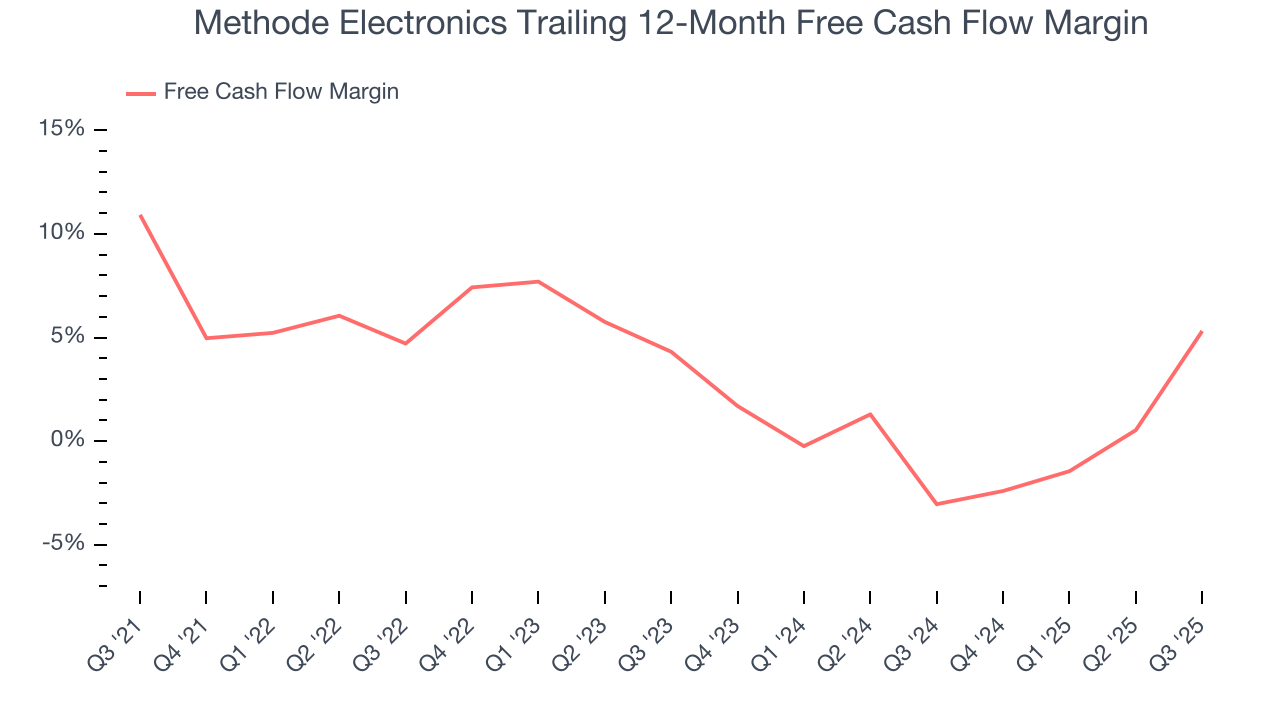

9. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Methode Electronics has shown weak cash profitability over the last five years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 4.5%, subpar for an industrials business.

Taking a step back, we can see that Methode Electronics’s margin dropped by 5.6 percentage points during that time. It may have ticked higher more recently, but shareholders are likely hoping for its margin to at least revert to its historical level. Almost any movement in the wrong direction is undesirable because of its relatively low cash conversion. If the longer-term trend returns, it could signal it’s in the middle of a big investment cycle.

Methode Electronics burned through $11.6 million of cash in Q3, equivalent to a negative 4.7% margin. The company’s cash burn slowed from $58.4 million of lost cash in the same quarter last year. These numbers deviate from its longer-term margin, indicating it is a seasonal business that must build up inventory during certain quarters.

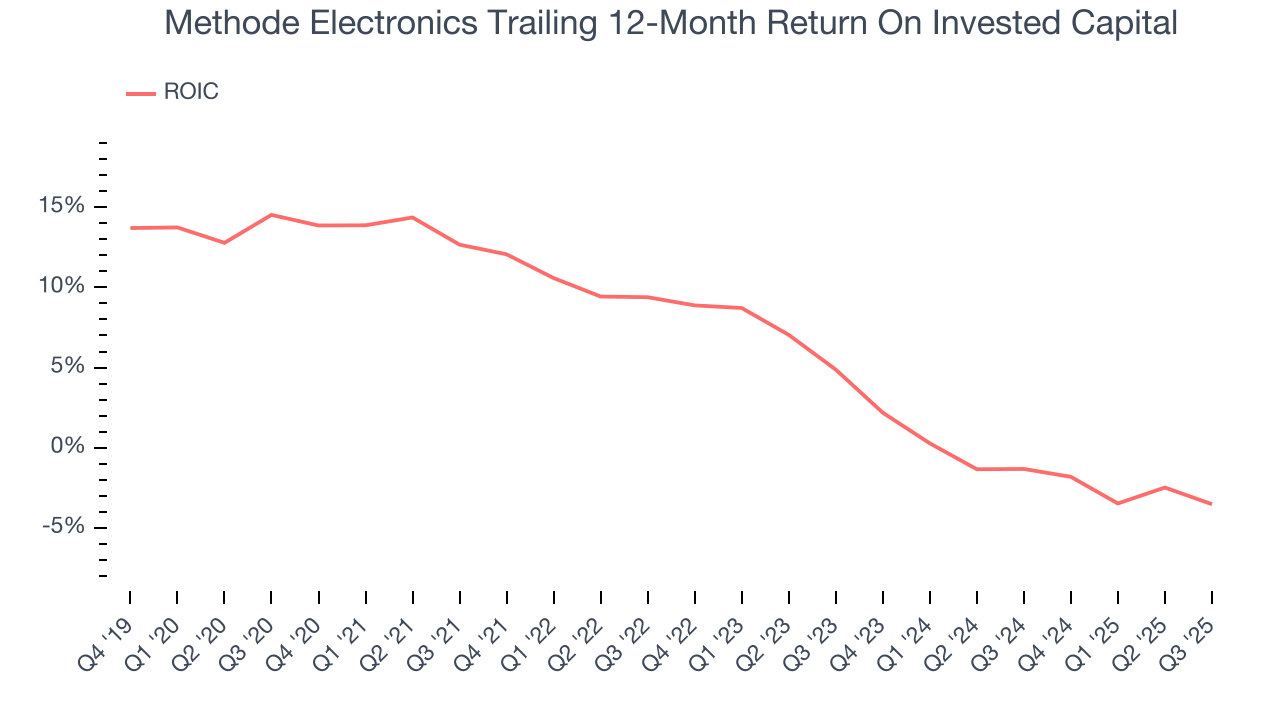

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Methode Electronics historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 4.4%, lower than the typical cost of capital (how much it costs to raise money) for industrials companies.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Methode Electronics’s ROIC has unfortunately decreased significantly. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

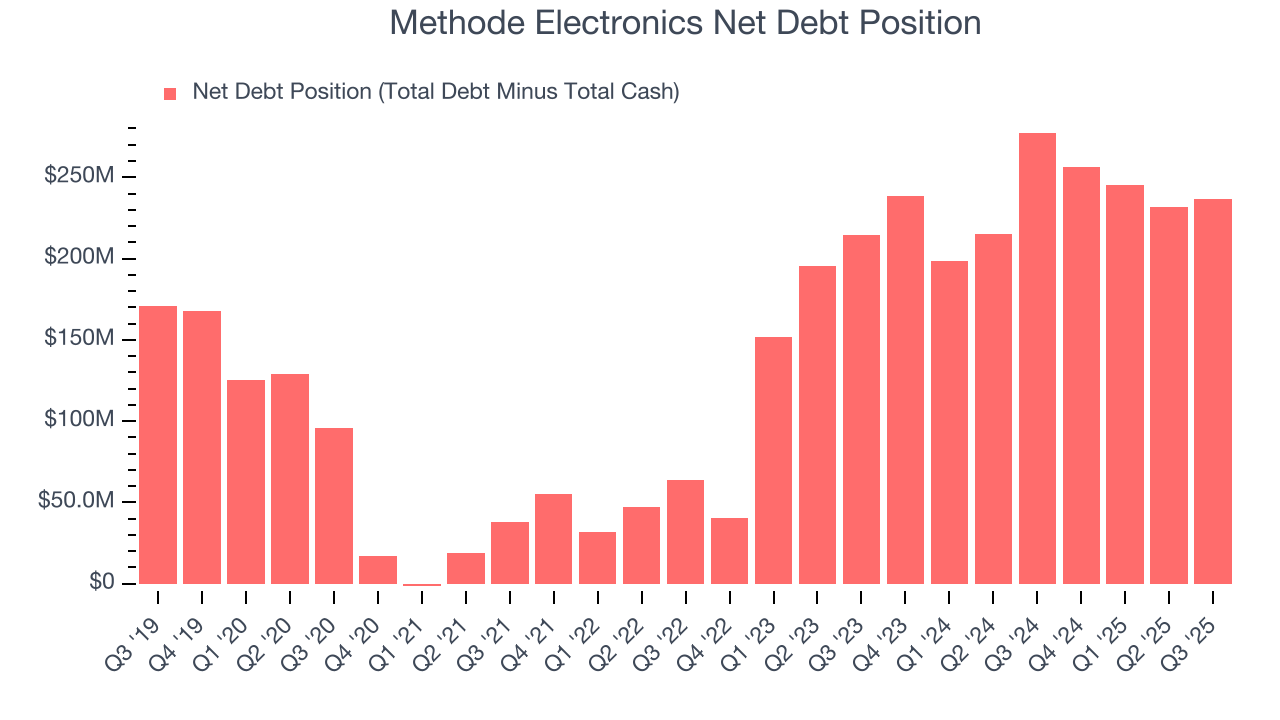

11. Balance Sheet Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

Methode Electronics’s $355.4 million of debt exceeds the $118.5 million of cash on its balance sheet. Furthermore, its 6× net-debt-to-EBITDA ratio (based on its EBITDA of $38.5 million over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. Methode Electronics could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope Methode Electronics can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

12. Key Takeaways from Methode Electronics’s Q3 Results

We were impressed by how significantly Methode Electronics blew past analysts’ EBITDA expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a good print with some key areas of upside. The market seemed to be hoping for more, and the stock traded down 6.2% to $8.15 immediately following the results.

13. Is Now The Time To Buy Methode Electronics?

Updated: January 24, 2026 at 10:21 PM EST

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

Methode Electronics falls short of our quality standards. First off, its revenue growth was weak over the last five years, and analysts don’t see anything changing over the next 12 months. And while its projected EPS for the next year implies the company’s fundamentals will improve, the downside is its diminishing returns show management's prior bets haven't worked out. On top of that, its relatively low ROIC suggests management has struggled to find compelling investment opportunities.

Methode Electronics’s P/E ratio based on the next 12 months is 126.3x. This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $9.25 on the company (compared to the current share price of $7.30).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.