MGIC Investment (MTG)

We aren’t fans of MGIC Investment. Its lack of sales growth shows demand is soft, a concerning sign for investors in high-quality stocks.― StockStory Analyst Team

1. News

2. Summary

Why MGIC Investment Is Not Exciting

Founded in 1957 when the modern mortgage insurance industry was in its infancy, MGIC Investment (NYSE:MTG) provides private mortgage insurance that protects lenders when homebuyers default on their loans, enabling borrowers to purchase homes with smaller down payments.

- Net premiums earned contracted by 1.1% annually over the last five years, showing unfavorable market dynamics this cycle

- Sales were flat over the last five years, indicating it’s failed to expand this cycle

- On the bright side, its combined ratio improved by 28.4 percentage points over the last five years as it refined its cost structure

MGIC Investment lacks the business quality we seek. There are more profitable opportunities elsewhere.

Why There Are Better Opportunities Than MGIC Investment

MGIC Investment’s stock price of $26.27 implies a valuation ratio of 1.1x forward P/B. MGIC Investment’s valuation may seem like a bargain, especially when stacked up against other insurance companies. We remind you that you often get what you pay for, though.

Cheap stocks can look like great bargains at first glance, but you often get what you pay for. These mediocre businesses often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. MGIC Investment (MTG) Research Report: Q3 CY2025 Update

Mortgage insurer MGIC Investment (NYSE:MTG) missed Wall Street’s revenue expectations in Q3 CY2025, with sales flat year on year at $304.5 million. Its non-GAAP profit of $0.83 per share was 12.2% above analysts’ consensus estimates.

MGIC Investment (MTG) Q3 CY2025 Highlights:

- Net Premiums Earned: $241.8 million (flat year on year)

- Revenue: $304.5 million vs analyst estimates of $307.6 million (flat year on year, 1% miss)

- Pre-tax Profit: $235.1 million (77.2% margin, 7.6% year-on-year decline)

- Adjusted EPS: $0.83 vs analyst estimates of $0.74 (12.2% beat)

- Book Value per Share: $22.87 (10.7% year-on-year growth)

- Market Capitalization: $6.17 billion

Company Overview

Founded in 1957 when the modern mortgage insurance industry was in its infancy, MGIC Investment (NYSE:MTG) provides private mortgage insurance that protects lenders when homebuyers default on their loans, enabling borrowers to purchase homes with smaller down payments.

MGIC's primary business involves insuring first mortgage loans, typically on owner-occupied single-family homes. When a homebuyer makes a down payment of less than 20%, lenders often require private mortgage insurance (PMI) to mitigate their risk. If a borrower defaults and foreclosure occurs, MGIC pays the lender a predetermined percentage of the loss, helping to make the lender whole.

This insurance plays a crucial role in the housing market by allowing individuals to purchase homes with down payments as low as 3-5% instead of the traditional 20%. For example, a first-time homebuyer with good credit but limited savings might purchase a $300,000 home with just $15,000 down (5%) because MGIC's insurance protects the lender against potential losses on the remaining 15% that would traditionally be required.

The company generates revenue through premium payments, which can be structured as monthly payments, single upfront payments, or a combination. These premiums are typically paid by the borrower as part of their monthly mortgage payment, though sometimes lenders pay the premiums directly.

Beyond its core mortgage insurance, MGIC offers contract underwriting services through a non-insurance subsidiary. This service helps lenders evaluate mortgage applications according to various guidelines, including those established by government-sponsored enterprises (GSEs) like Fannie Mae and Freddie Mac.

MGIC operates throughout all 50 states, the District of Columbia, Puerto Rico, and Guam, with a business model heavily influenced by housing market conditions, interest rates, and mortgage lending regulations. The company's operations are particularly affected by policies of the GSEs, which purchase a significant portion of U.S. mortgages and establish requirements for loans they acquire.

4. Property & Casualty Insurance

Property & Casualty (P&C) insurers protect individuals and businesses against financial loss from damage to property or from legal liability. This is a cyclical industry, and the sector benefits when there is 'hard market', characterized by strong premium rate increases that outpace loss and cost inflation, resulting in robust underwriting margins. The opposite is true in a 'soft market'. Interest rates also matter, as they determine the yields earned on fixed-income portfolios. On the other hand, P&C insurers face a major secular headwind from the increasing frequency and severity of catastrophe losses due to climate change. Furthermore, the liability side of the business is pressured by 'social inflation'—the trend of rising litigation costs and larger jury awards.

MGIC Investment's main competitors include other private mortgage insurers such as Essent Group (NYSE:ESNT), Radian Group (NYSE:RDN), and National Mortgage Insurance (NASDAQ:NMIH), as well as government agencies like the Federal Housing Administration (FHA) that offer mortgage insurance programs.

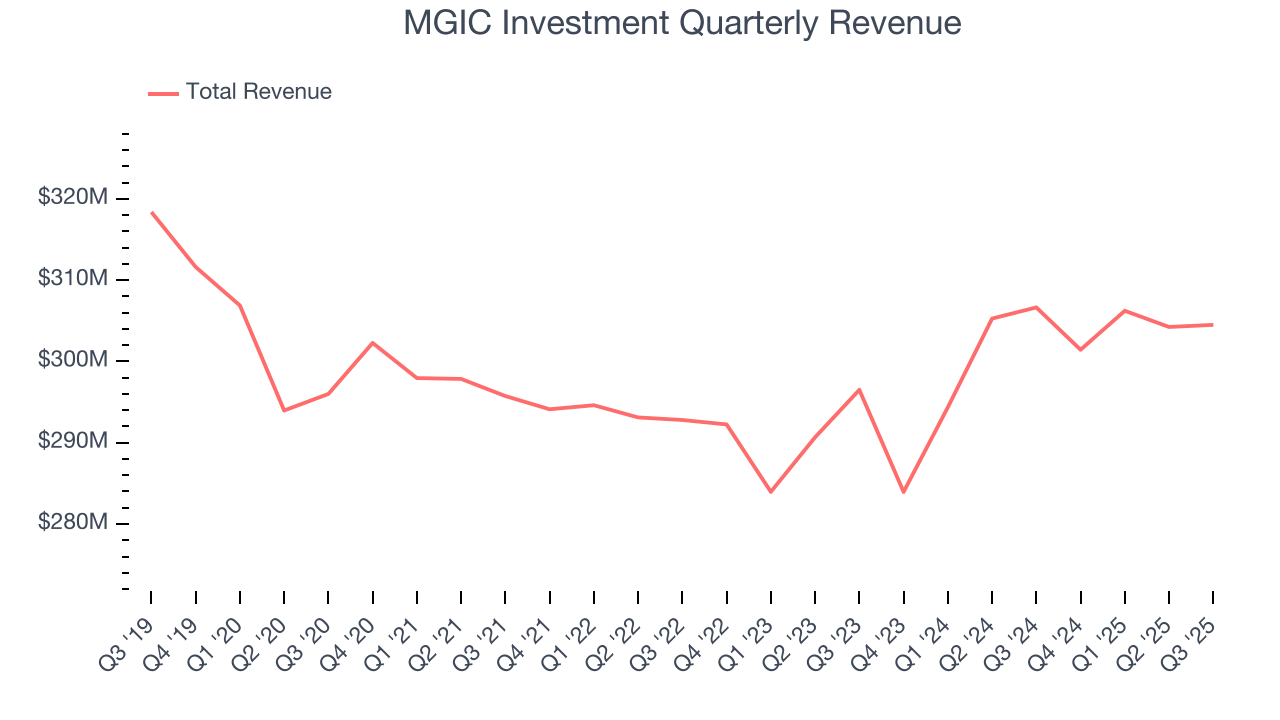

5. Revenue Growth

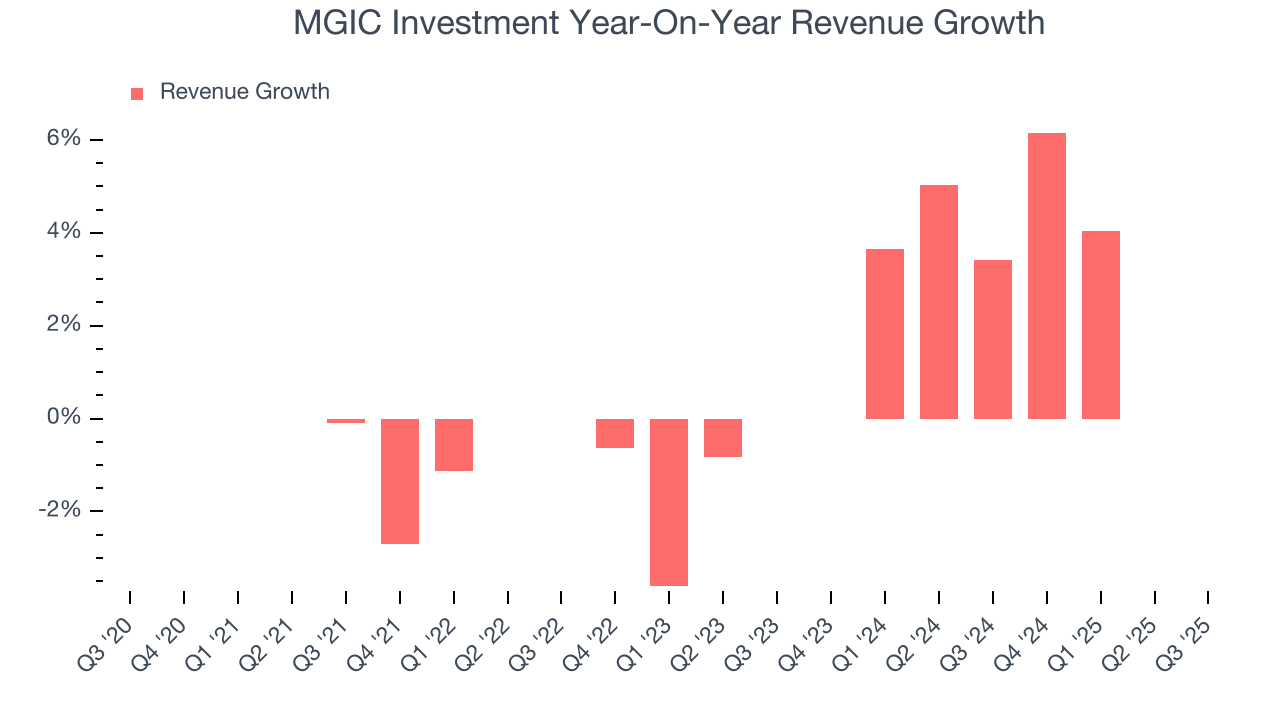

In general, insurance companies earn revenue from three primary sources. The first is the core insurance business itself, often called underwriting and represented in the income statement as premiums earned. The second source is investment income from investing the “float” (premiums collected upfront not yet paid out as claims) in assets such as fixed-income assets and equities. The third is fees from various sources such as policy administration, annuities, or other value-added services. Unfortunately, MGIC Investment struggled to consistently increase demand as its $1.22 billion of revenue for the trailing 12 months was close to its revenue five years ago. This was below our standards and suggests it’s a lower quality business.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. MGIC Investment’s annualized revenue growth of 2.3% over the last two years is above its five-year trend, but we were still disappointed by the results.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, MGIC Investment missed Wall Street’s estimates and reported a rather uninspiring 0.7% year-on-year revenue decline, generating $304.5 million of revenue.

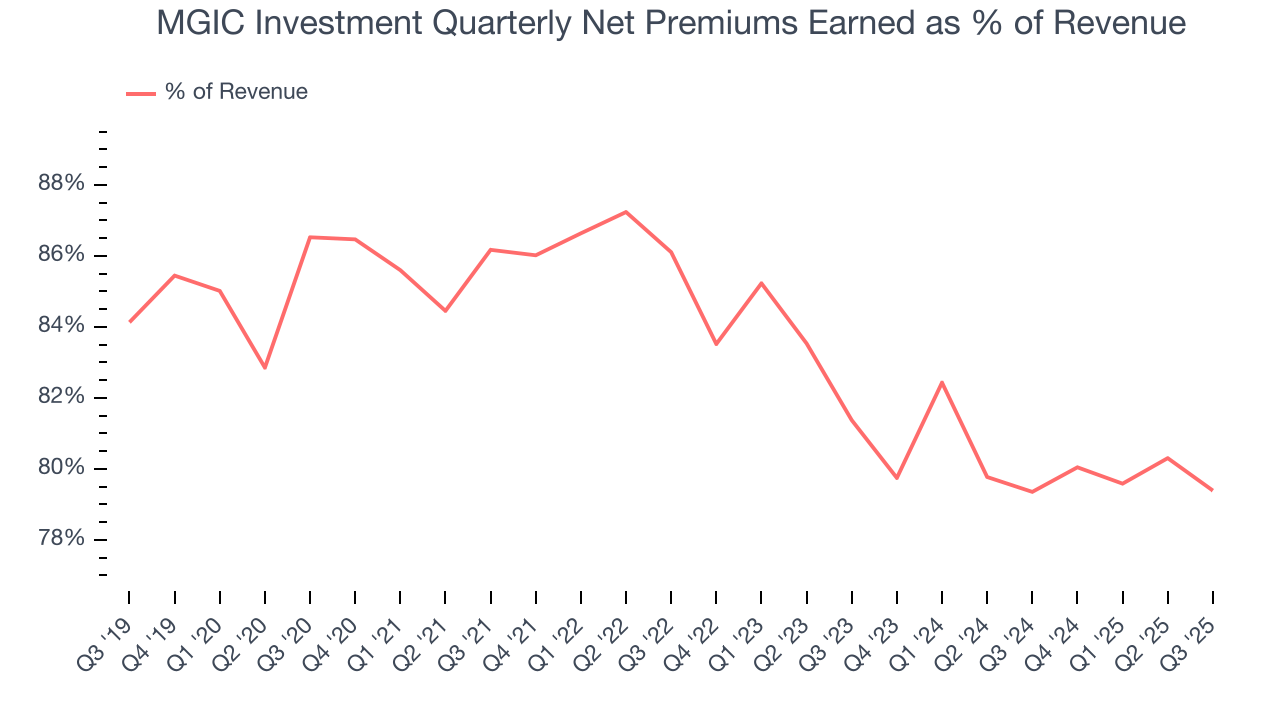

Net premiums earned made up 83.1% of the company’s total revenue during the last five years, meaning MGIC Investment barely relies on non-insurance activities to drive its overall growth.

Our experience and research show the market cares primarily about an insurer’s net premiums earned growth as investment and fee income are considered more susceptible to market volatility and economic cycles.

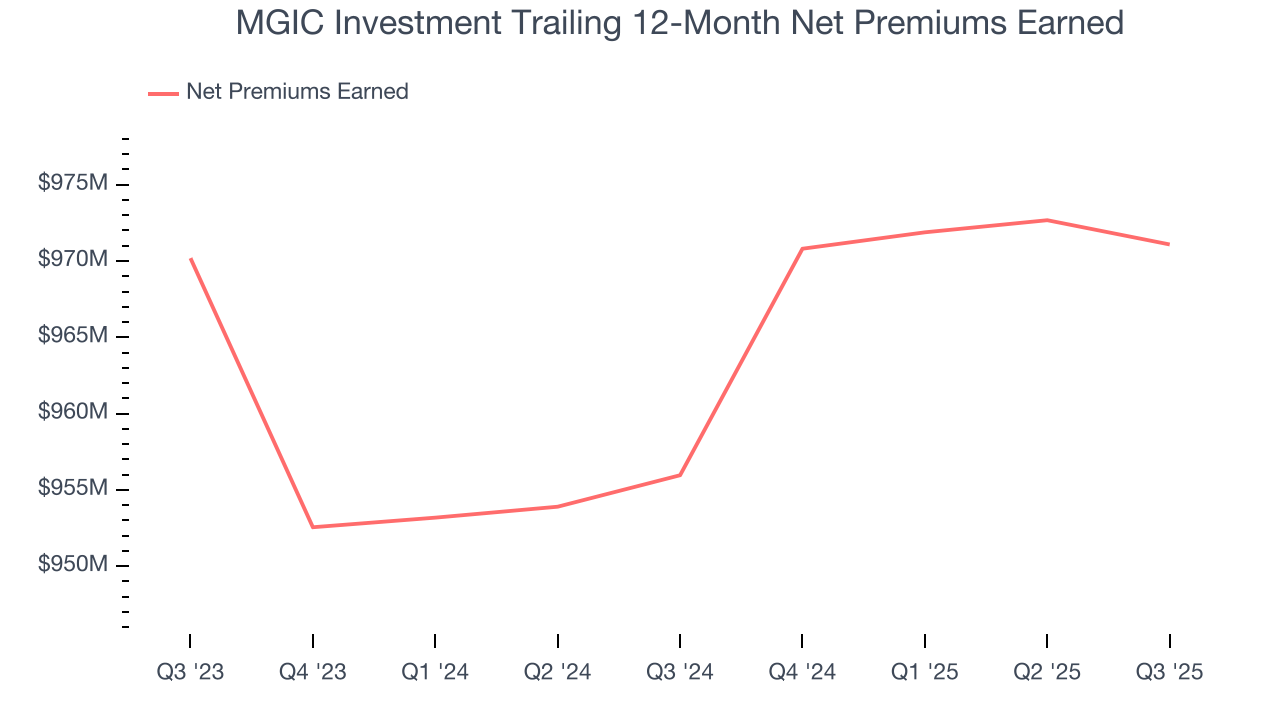

6. Net Premiums Earned

Net premiums earned are net of what’s paid to reinsurers (insurance for insurance companies), which are used by insurers to protect themselves from large losses.

MGIC Investment’s net premiums earned has declined by 1.1% annually over the last five years, much worse than the broader insurance industry. This shows that policy underwriting underperformed its other business lines.

When analyzing MGIC Investment’s net premiums earned over the last two years, we can see a sliver of stabilization as income was flat. Since two-year net premiums earned underperformed total revenue over this period, it’s implied that insurance policies were a detractor of consolidated growth.

MGIC Investment produced $241.8 million of net premiums earned in Q3, flat year on year and short of Wall Street Consensus estimates.

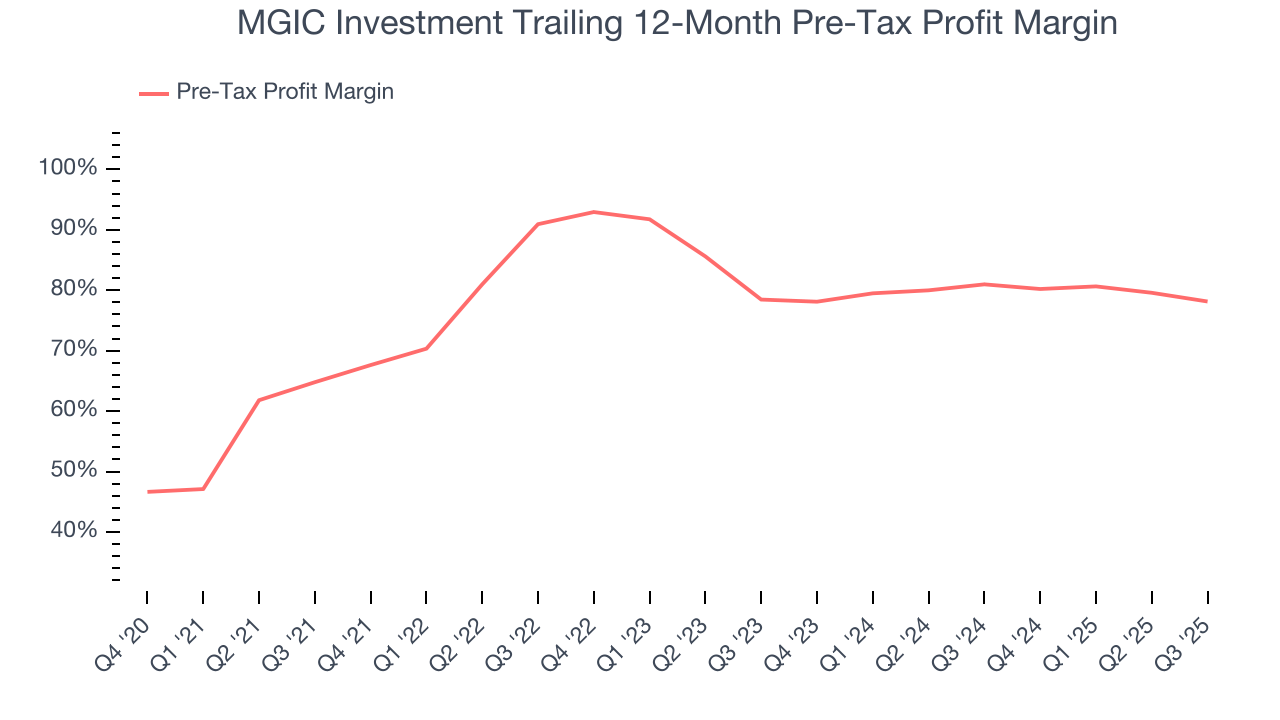

7. Pre-Tax Profit Margin

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For insurance companies, we look at pre-tax profit rather than the operating margin that defines sectors such as consumer, tech, and industrials.

The economics of insurers are driven by their balance sheets, where assets (investing the float + premiums receivable) and liabilities (claims to pay) define the fundamentals. Interest income and expense should therefore be factored into the definition of profit but taxes - which are largely out of a company’s control - should not.

Over the last four years, MGIC Investment’s pre-tax profit margin has fallen by 13.4 percentage points, going from 64.8% to 78.1%. However, fixed cost leverage was muted more recently as the company’s pre-tax profit margin was flat on a two-year basis.

In Q3, MGIC Investment’s pre-tax profit margin was 77.2%. This result was 5.7 percentage points worse than the same quarter last year.

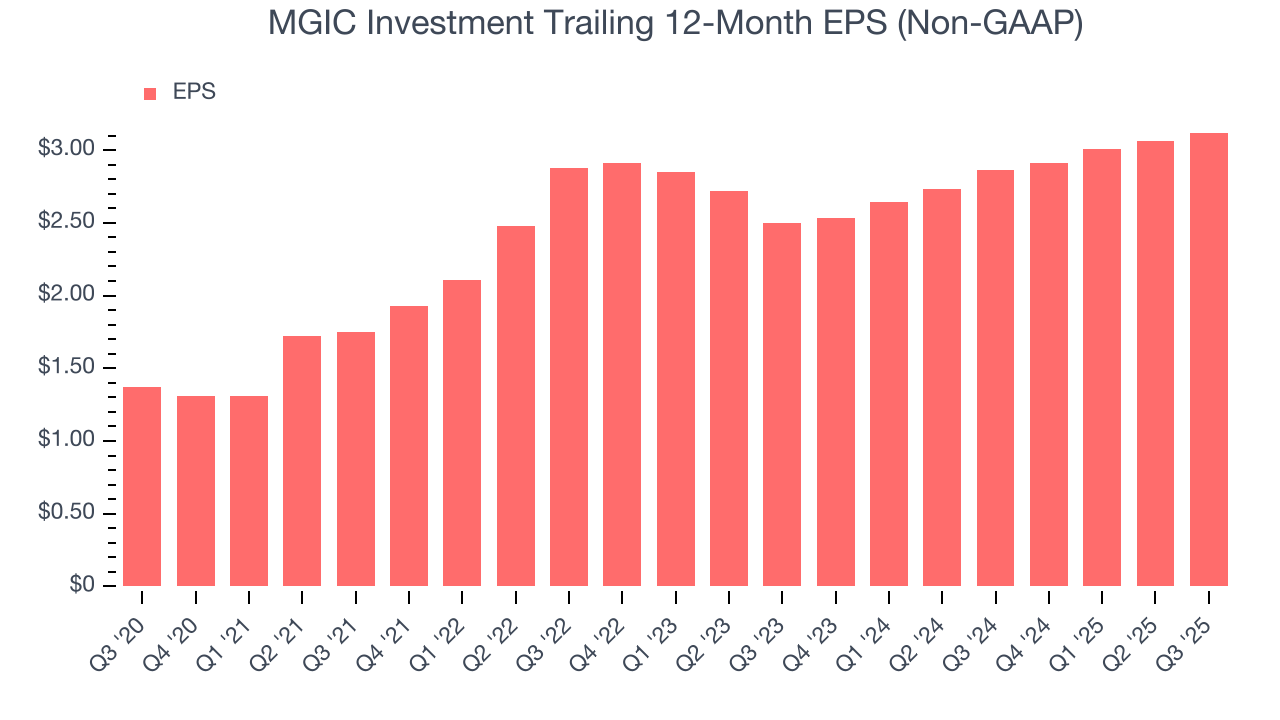

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

MGIC Investment’s EPS grew at a remarkable 17.9% compounded annual growth rate over the last five years, higher than its flat revenue. This tells us management responded to softer demand by adapting its cost structure.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For MGIC Investment, its two-year annual EPS growth of 11.7% was lower than its five-year trend. We hope its growth can accelerate in the future.

In Q3, MGIC Investment reported adjusted EPS of $0.83, up from $0.77 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects MGIC Investment’s full-year EPS of $3.12 to shrink by 2.3%.

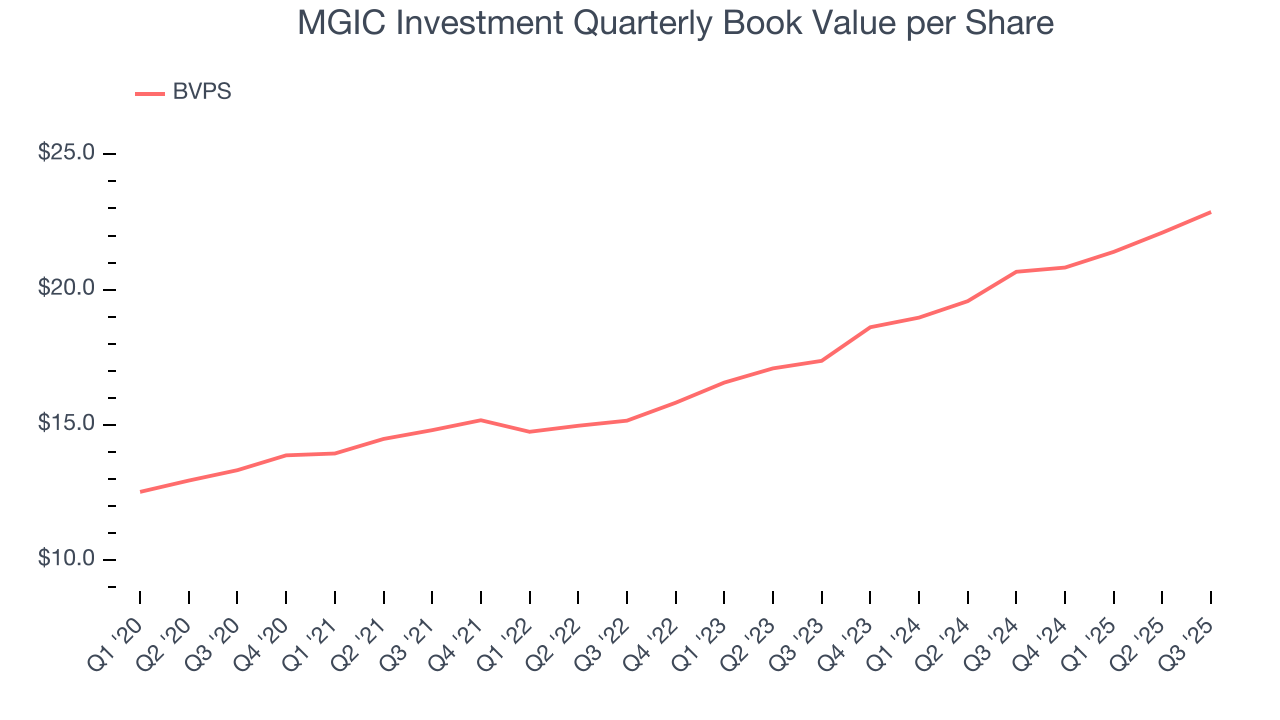

9. Book Value Per Share (BVPS)

Insurance companies are balance sheet businesses, collecting premiums upfront and paying out claims over time. The float–premiums collected but not yet paid out–are invested, creating an asset base supported by a liability structure. Book value per share (BVPS) captures this dynamic by measuring these assets (investment portfolio, cash, reinsurance recoverables) less liabilities (claim reserves, debt, future policy benefits). BVPS is essentially the residual value for shareholders.

We therefore consider BVPS very important to track for insurers and a metric that sheds light on business quality. While other (and more commonly known) per-share metrics like EPS can sometimes be lumpy due to reserve releases or one-time items and can be managed or skewed while still following accounting rules, BVPS reflects long-term capital growth and is harder to manipulate.

MGIC Investment’s BVPS grew at an impressive 11.4% annual clip over the last five years. BVPS growth has also accelerated recently, growing by 14.7% annually over the last two years from $17.37 to $22.87 per share.

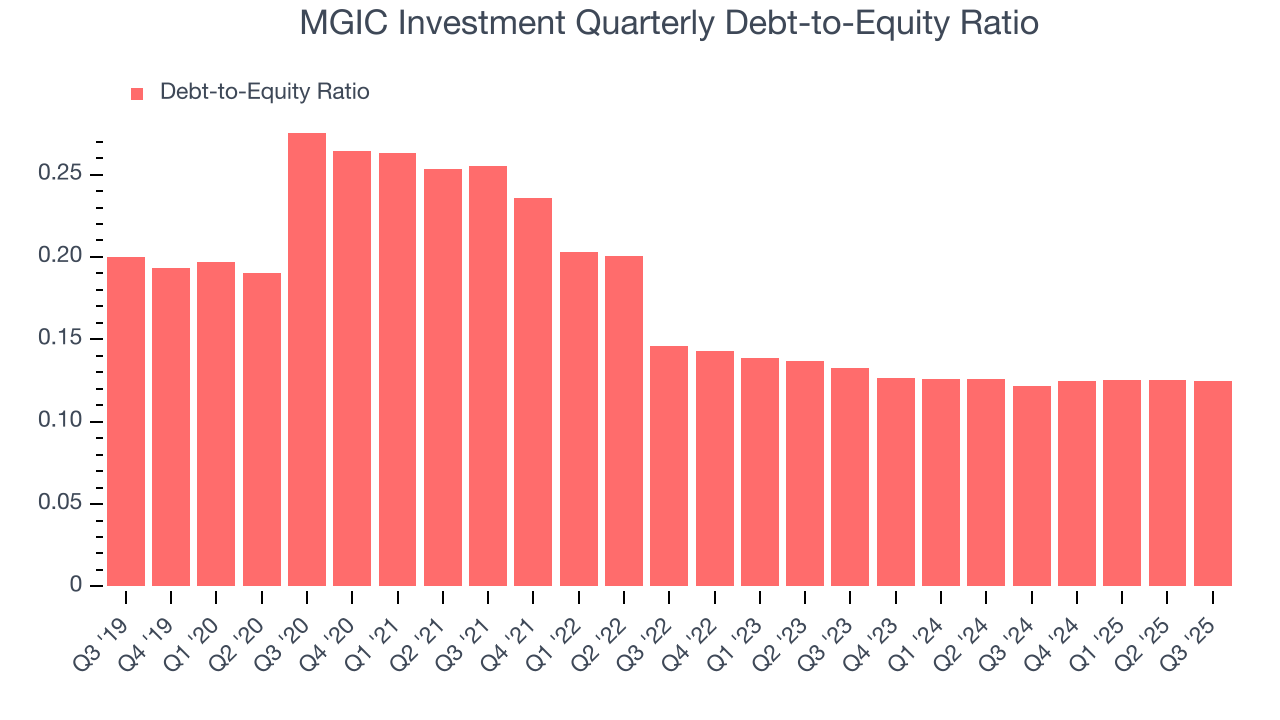

10. Balance Sheet Assessment

The debt-to-equity ratio is a widely used measure to assess a company's balance sheet health. A higher ratio means that a business aggressively financed its growth with debt. This can result in higher earnings (if the borrowed funds are invested profitably) but also increases risk.

If debt levels are too high, there could be difficulties in meeting obligations, especially during economic downturns or periods of rising interest rates if the debt has variable-rate payments.

MGIC Investment currently has $645.8 million of debt and $5.17 billion of shareholder's equity on its balance sheet, and over the past four quarters, has averaged a debt-to-equity ratio of 0.1×. We think this is safe and raises no red flags. In general, we’re comfortable with any ratio below 1.0× for an insurance business. Anything below 0.5× is a bonus.

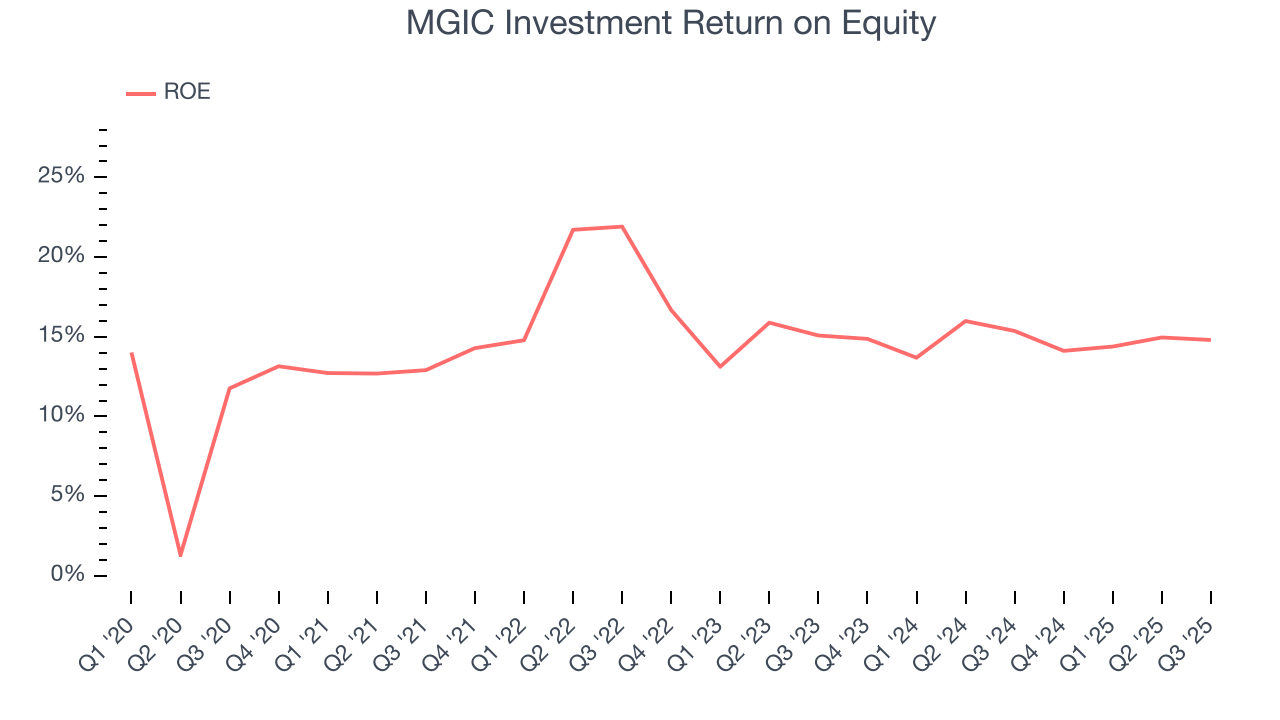

11. Return on Equity

Return on equity (ROE) serves as a comprehensive measure of an insurer's performance, showing how efficiently it converts shareholder capital into profits. Strong ROE performance typically translates to better returns for investors through a combination of earnings retention, share repurchases, and dividend distributions.

Over the last five years, MGIC Investment has averaged an ROE of 15.2%, healthy for a company operating in a sector where the average shakes out around 12.5% and those putting up 20%+ are greatly admired. This is a bright spot for MGIC Investment.

12. Key Takeaways from MGIC Investment’s Q3 Results

It was good to see MGIC Investment beat analysts’ EPS expectations this quarter. On the other hand, its revenue slightly missed. Overall, this print was mixed. The stock remained flat at $26.36 immediately following the results.

13. Is Now The Time To Buy MGIC Investment?

Updated: January 24, 2026 at 11:06 PM EST

Before investing in or passing on MGIC Investment, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

MGIC Investment isn’t a terrible business, but it doesn’t pass our quality test. First off, its revenue growth was weak over the last five years. And while its improving combined ratio shows the business has become more productive, the downside is its projected EPS for the next year is lacking. On top of that, its net premiums earned has declined over the last five years.

MGIC Investment’s P/B ratio based on the next 12 months is 1.1x. While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're fairly confident there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $28.75 on the company (compared to the current share price of $26.27).