Magnachip (MX)

We wouldn’t recommend Magnachip. Its falling revenue and negative returns on capital suggest it’s destroying value as demand fizzles out.― StockStory Analyst Team

1. News

2. Summary

Why We Think Magnachip Will Underperform

With its technology found in common consumer electronics such as TVs and smartphones, Magnachip Semiconductor (NYSE:MX) is a provider of analog and mixed-signal semiconductors.

- Products and services are facing significant end-market challenges during this cycle as sales have declined by 18.8% annually over the last five years

- Falling earnings per share over the last five years has some investors worried as stock prices ultimately follow EPS over the long term

- Unfavorable liquidity position could lead to additional equity financing that dilutes shareholders

Magnachip’s quality is lacking. We’d rather invest in businesses with stronger moats.

Why There Are Better Opportunities Than Magnachip

Magnachip’s stock price of $2.88 implies a valuation ratio of 0.5x forward price-to-sales. The market typically values companies like Magnachip based on their anticipated profits for the next 12 months, but it expects the business to lose money. We also think the upside isn’t great compared to the potential downside here - there are more exciting stocks to buy.

We’d rather pay up for companies with elite fundamentals than get a decent price on a poor one. High-quality businesses often have more durable earnings power, helping us sleep well at night.

3. Magnachip (MX) Research Report: Q4 CY2025 Update

Semiconductor manufacturer Magnachip Semiconductor (NYSE:MX) met Wall Street’s revenue expectations in Q4 CY2025, but sales fell by 35.6% year on year to $40.57 million. The company expects next quarter’s revenue to be around $46 million, coming in 1.1% above analysts’ estimates. Its non-GAAP loss of $0.08 per share was 75% above analysts’ consensus estimates.

Magnachip (MX) Q4 CY2025 Highlights:

- Revenue: $40.57 million vs analyst estimates of $40.5 million (35.6% year-on-year decline, in line)

- Adjusted EPS: -$0.08 vs analyst estimates of -$0.32 (75% beat)

- Adjusted EBITDA: -$8.86 million (-21.8% margin, 236% year-on-year decline)

- Revenue Guidance for Q1 CY2026 is $46 million at the midpoint, above analyst estimates of $45.5 million

- Operating Margin: -30.7%, down from -14.4% in the same quarter last year

- Free Cash Flow was -$4.82 million, down from $4.43 million in the same quarter last year

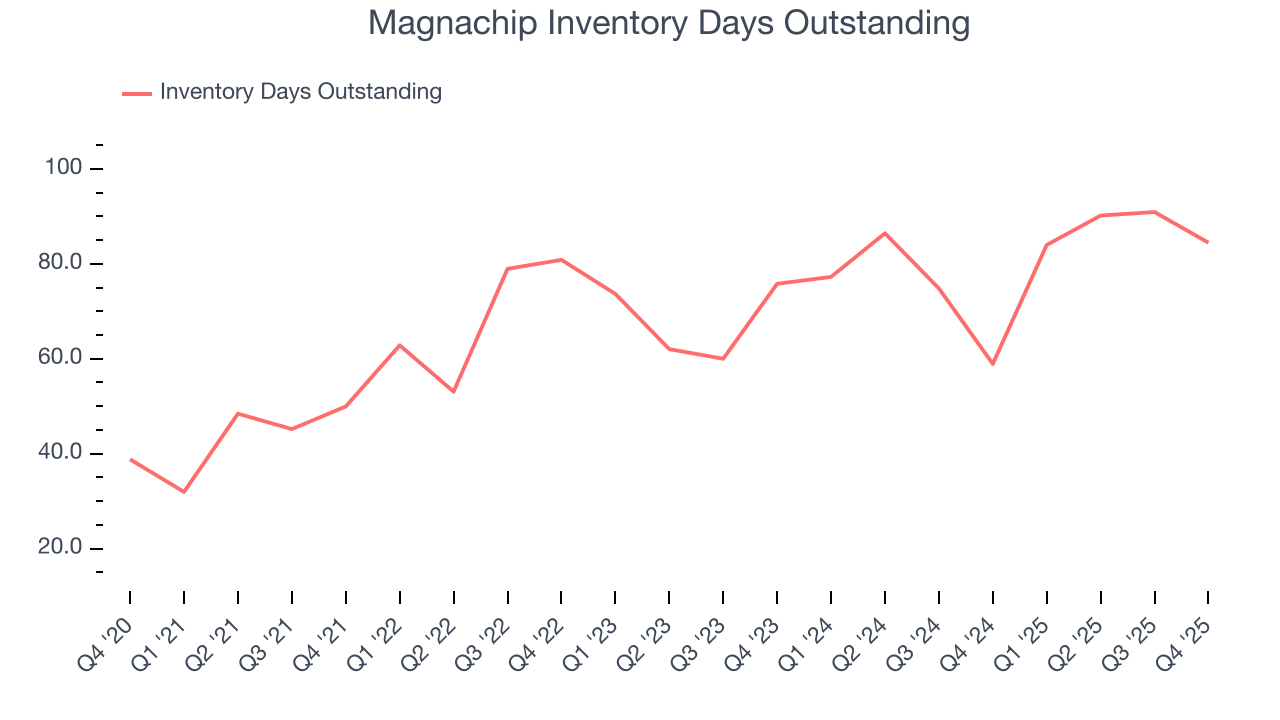

- Inventory Days Outstanding: 84, down from 91 in the previous quarter

- Market Capitalization: $97.87 million

Company Overview

With its technology found in common consumer electronics such as TVs and smartphones, Magnachip Semiconductor (NYSE:MX) is a provider of analog and mixed-signal semiconductors.

Magnachip is headquartered in South Korea and was founded in 2004 after Hynix Semiconductor’s non-memory business was separated from the parent company. Magnachip went public in 2011.

Magnachip’s product portfolio is divided into two segments: Display Solutions and Power Solutions. The company’s Display Solutions technology delivers defined analog voltages and currents that activate pixels on displays. One example is Magnachip’s display drivers, which are chips that serve as interfaces between microprocessors and LCD screens in smartphones. Another example is timing controllers, which are chips that receive and convert image data on screens.

Magnachip’s Power Solutions technology allows for power consumption regulation and efficiency in devices. Examples include various transistors, which enable low standby power consumption in consumer electronics such as laptops so as not to drain the battery when in sleep or standby modes. Driver and regulator technologies in Power Solutions also aid in the heat dissipation needed for many consumer electronics such as tablets to prevent them from getting too hot.

Magnachip’s customers are largely consumer, computing, and industrial electronics OEMs (original equipment manufacturers). The company manufactures most of its Display Solutions products at external foundries, while Power Solutions products are manufactured through a combination of both in-house manufacturing and external foundries.

Competitors offering analog and mixed-signal semiconductors for display and power management include Diodes (NASDAQ:DIOD), Infineon Technologies (XTRA:IFX), and Novatek Microelectronics (TWSE:3034).

4. Revenue Growth

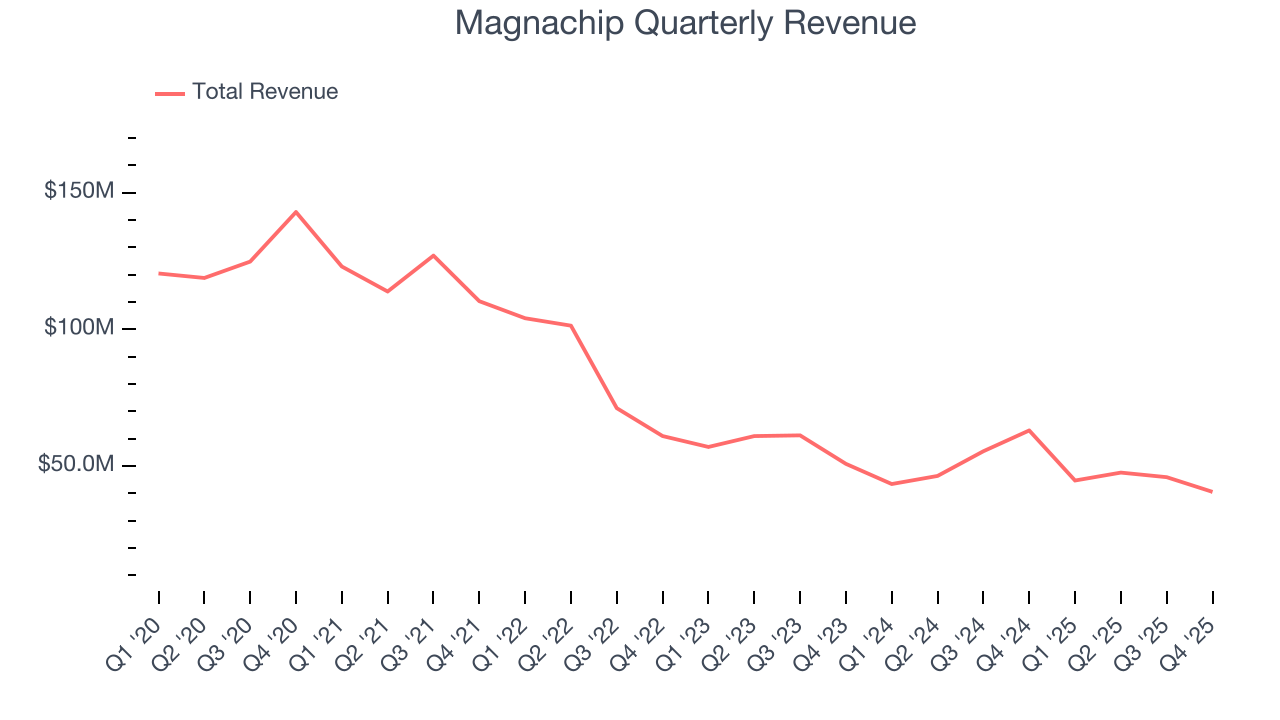

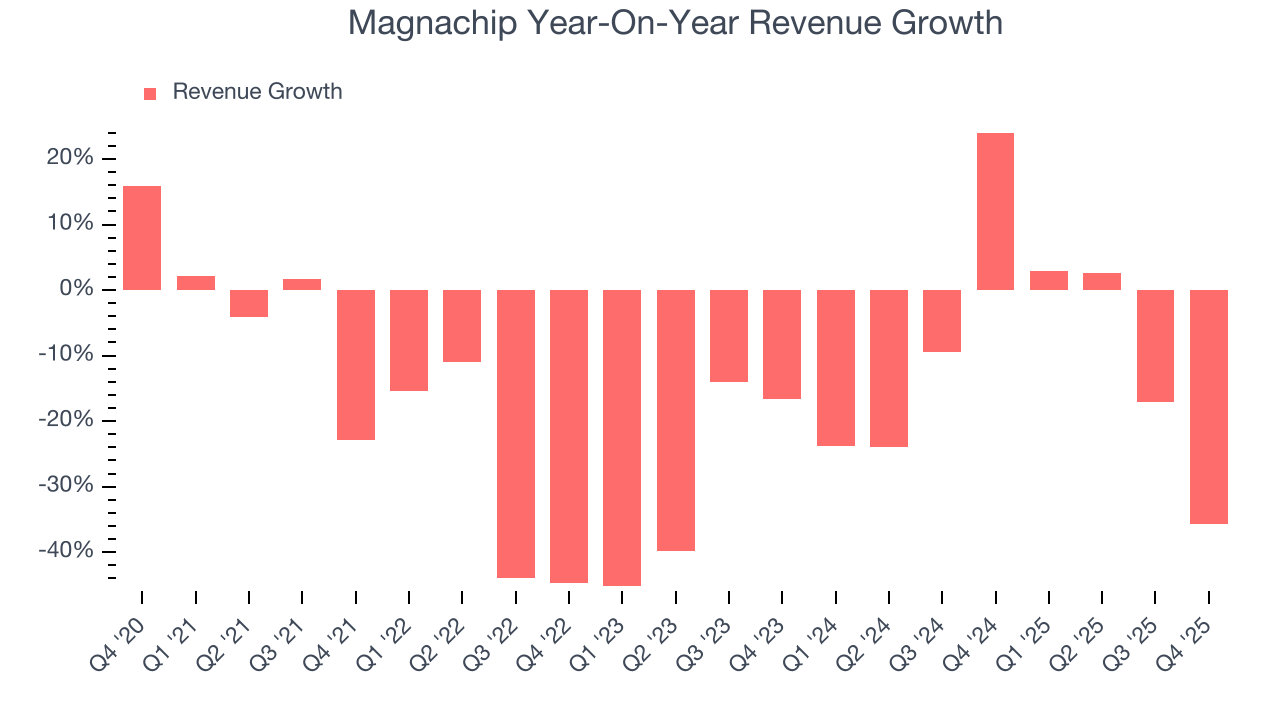

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years. Magnachip struggled to consistently generate demand over the last five years as its sales dropped at a 18.8% annual rate. This wasn’t a great result and is a sign of poor business quality. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

Long-term growth is the most important, but short-term results matter for semiconductors because the rapid pace of technological innovation (Moore's Law) could make yesterday's hit product obsolete today. Magnachip’s annualized revenue declines of 11.8% over the last two years suggest its demand continued shrinking.

This quarter, Magnachip reported a rather uninspiring 35.6% year-on-year revenue decline to $40.57 million of revenue, in line with Wall Street’s estimates. Despite meeting estimates, the drop in sales could mean that the current downcycle is deepening. Company management is currently guiding for a 2.9% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to decline by 3.6% over the next 12 months. Although this projection is better than its two-year trend, it’s tough to feel optimistic about a company facing demand difficulties.

5. Product Demand & Outstanding Inventory

Days Inventory Outstanding (DIO) is an important metric for chipmakers, as it reflects a business’ capital intensity and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise, the company may have to downsize production.

This quarter, Magnachip’s DIO came in at 84, which is 16 days above its five-year average. These numbers suggest that despite the recent decrease, the company’s inventory levels are higher than what we’ve seen in the past.

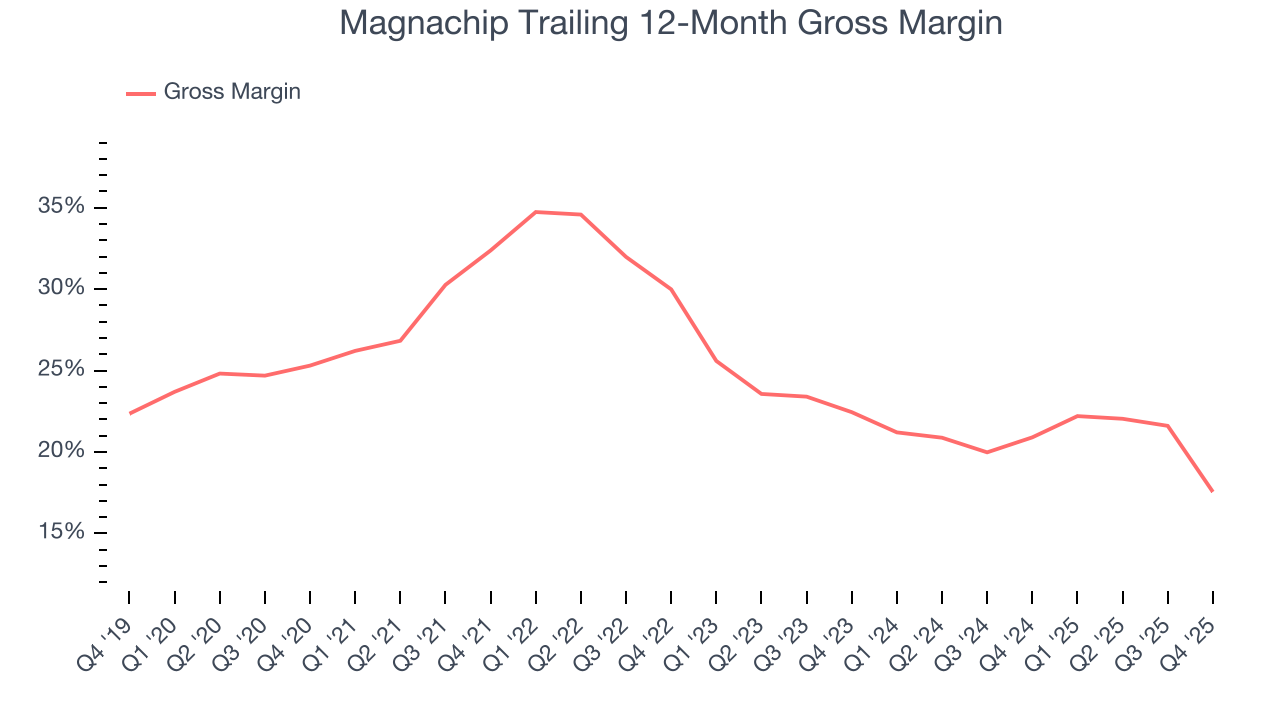

6. Gross Margin & Pricing Power

Gross profit margin is a key metric to track because it shows how much money a semiconductor company gets to keep after paying for its raw materials, manufacturing, and other input costs.

Magnachip’s gross margin is one of the worst in the semiconductor industry, signaling it operates in a competitive market and lacks pricing power. As you can see below, it averaged a 19.4% gross margin over the last two years. That means Magnachip paid its suppliers a lot of money ($80.65 for every $100 in revenue) to run its business.

Magnachip produced a 9.3% gross profit margin in Q4 , marking a 15.9 percentage point decrease from 25.2% in the same quarter last year. Magnachip’s full-year margin has also been trending down over the past 12 months, decreasing by 3.3 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to lower prices and higher input costs (such as raw materials and manufacturing expenses).

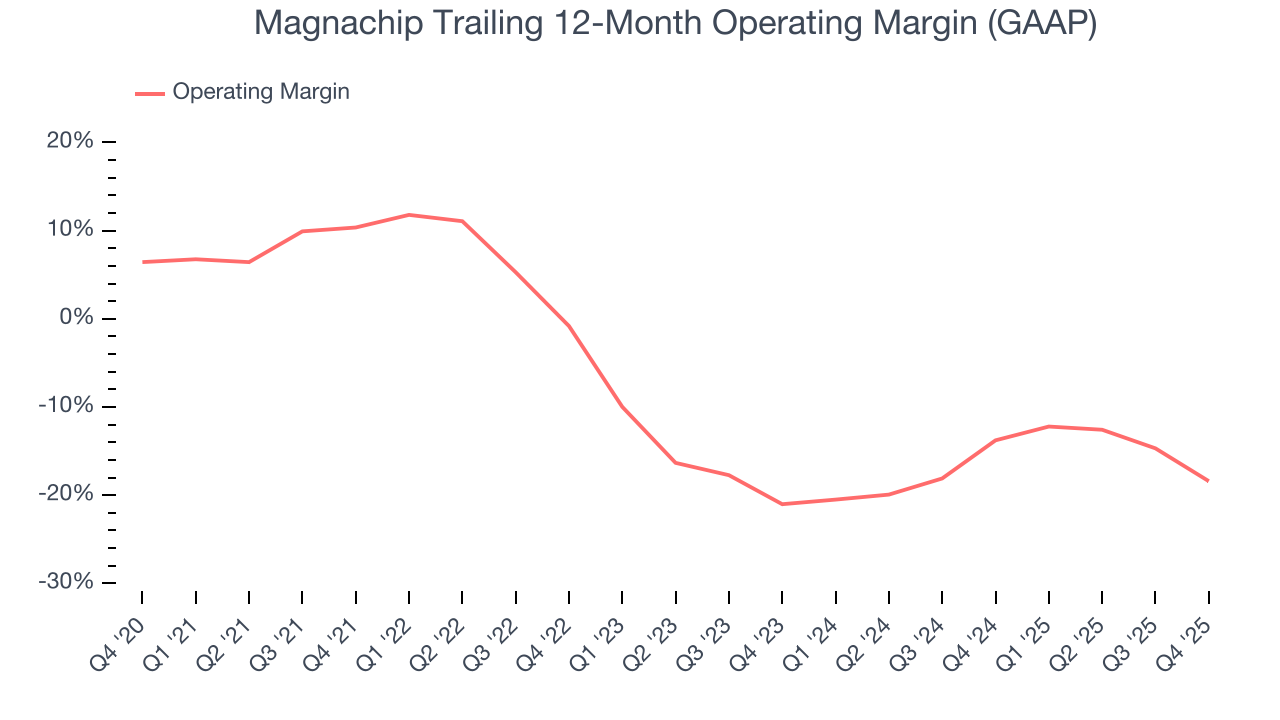

7. Operating Margin

Magnachip’s high expenses have contributed to an average operating margin of negative 15.9% over the last two years. Unprofitable semiconductor companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

Analyzing the trend in its profitability, Magnachip’s operating margin decreased by 28.8 percentage points over the last five years. Magnachip’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

Magnachip’s operating margin was negative 30.7% this quarter. The company's consistent lack of profits raise a flag.

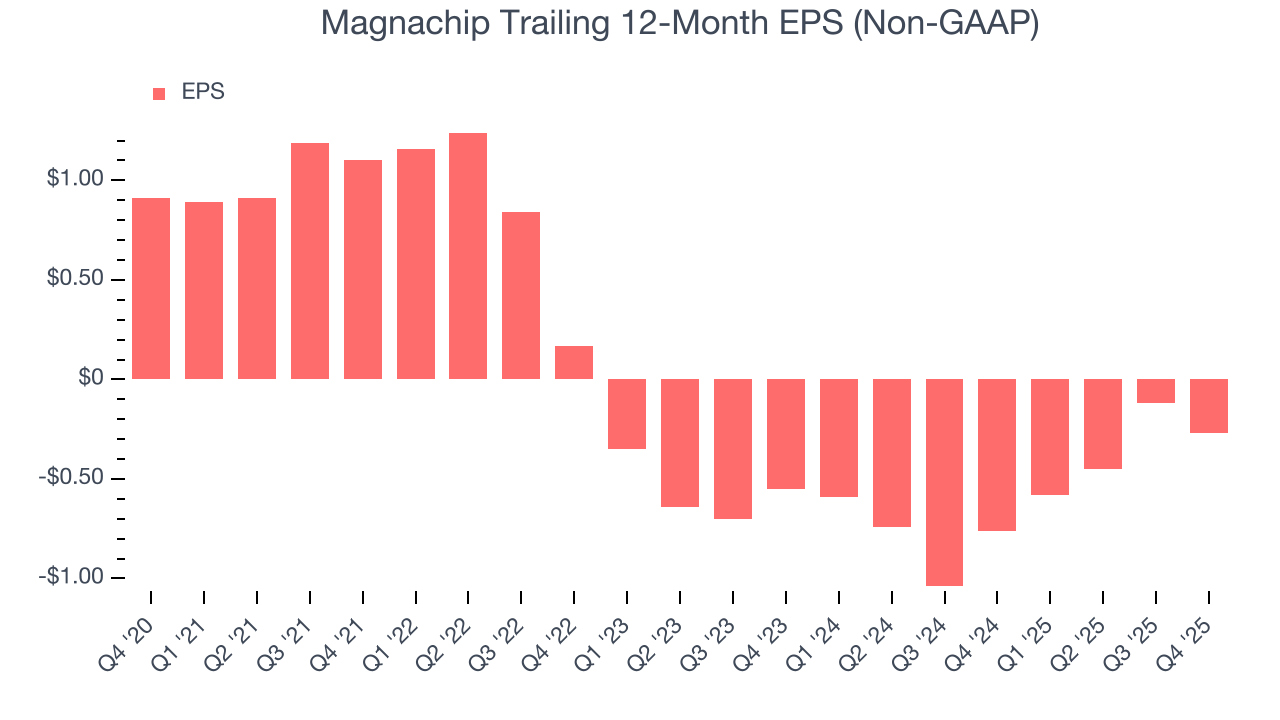

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Magnachip, its EPS and revenue declined by 18.1% and 18.8% annually over the last five years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Magnachip’s low margin of safety could leave its stock price susceptible to large downswings.

In Q4, Magnachip reported adjusted EPS of negative $0.08, down from $0.07 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Magnachip to perform poorly. Analysts forecast its full-year EPS of negative $0.27 will tumble to negative $0.94.

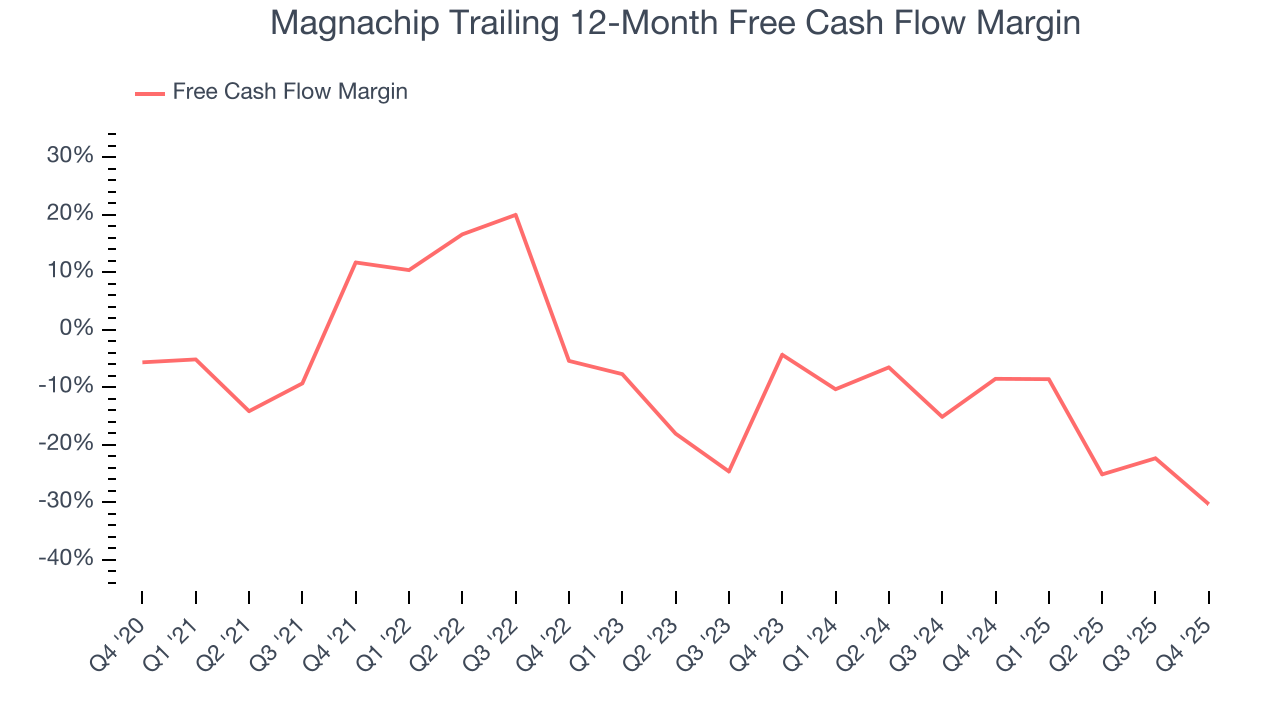

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Magnachip’s demanding reinvestments have drained its resources over the last two years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 18.6%, meaning it lit $18.58 of cash on fire for every $100 in revenue.

Taking a step back, we can see that Magnachip’s margin dropped by 42 percentage points over the last five years. Almost any movement in the wrong direction is undesirable because it is already burning cash. If the trend continues, it could signal it’s becoming a more capital-intensive business.

Magnachip burned through $4.82 million of cash in Q4, equivalent to a negative 11.9% margin. The company’s cash flow turned negative after being positive in the same quarter last year, but it’s still above its two-year average. We wouldn’t read too much into this quarter’s decline because investment needs can be seasonal, leading to short-term swings. Long-term trends are more important.

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Magnachip’s five-year average ROIC was negative 4.6%, meaning management lost money while trying to expand the business. Its returns were among the worst in the semiconductor sector.

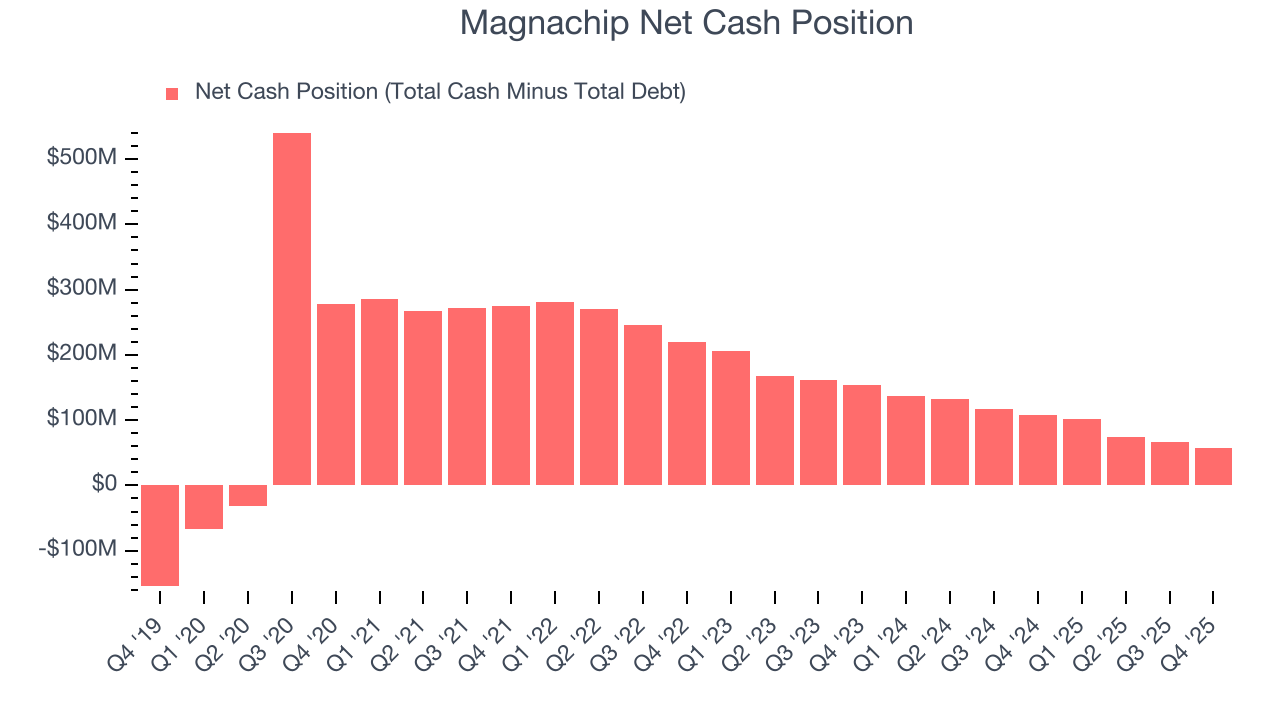

11. Balance Sheet Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

Magnachip burned through $54.2 million of cash over the last year. With $103.8 million of cash on its balance sheet, the company has around 23 months of runway left (assuming its $46.72 million of debt isn’t due right away).

Unless the Magnachip’s fundamentals change quickly, it might find itself in a position where it must raise capital from investors to continue operating. Whether that would be favorable is unclear because dilution is a headwind for shareholder returns.

We remain cautious of Magnachip until it generates consistent free cash flow or any of its announced financing plans materialize on its balance sheet.

12. Key Takeaways from Magnachip’s Q4 Results

It was good to see Magnachip beat analysts’ EPS expectations this quarter. We were also glad its inventory levels shrunk. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 9.9% to $2.95 immediately after reporting.

13. Is Now The Time To Buy Magnachip?

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Magnachip.

Magnachip falls short of our quality standards. First off, its revenue has declined over the last five years. On top of that, Magnachip’s relatively low ROIC suggests management has struggled to find compelling investment opportunities, and its projected EPS for the next year is lacking.

Magnachip’s forward price-to-sales ratio is 0.6x. The market typically values companies like Magnachip based on their anticipated profits for the next 12 months, but it expects the business to lose money. We also think the upside isn’t great compared to the potential downside here - there are more exciting stocks to buy.

Wall Street analysts have a consensus one-year price target of $4 on the company (compared to the current share price of $2.95).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.