Oracle (ORCL)

Oracle doesn’t excite us. Its poor revenue growth shows demand is soft and its cash burn makes us question its business model.― StockStory Analyst Team

1. News

2. Summary

Why We Think Oracle Will Underperform

Starting as a database company in 1977 and now powering mission-critical systems across the globe, Oracle (NYSE:ORCL) provides enterprise software and hardware products and services that help businesses manage their information technology needs.

- Cash burn makes us question whether it can achieve sustainable long-term growth

- Operating margin was unchanged over the last year, suggesting it failed to gain leverage on its fixed costs

- Limited cash reserves may force the company to seek unfavorable financing terms that could dilute shareholders

Oracle falls below our quality standards. We’d rather invest in businesses with stronger moats.

Why There Are Better Opportunities Than Oracle

At $154.33 per share, Oracle trades at 5.6x forward price-to-sales. This multiple is high given its weaker fundamentals.

It’s better to pay up for high-quality businesses with strong long-term earnings potential rather than to buy lower-quality companies with open questions and big downside risks.

3. Oracle (ORCL) Research Report: Q1 CY2026 Update

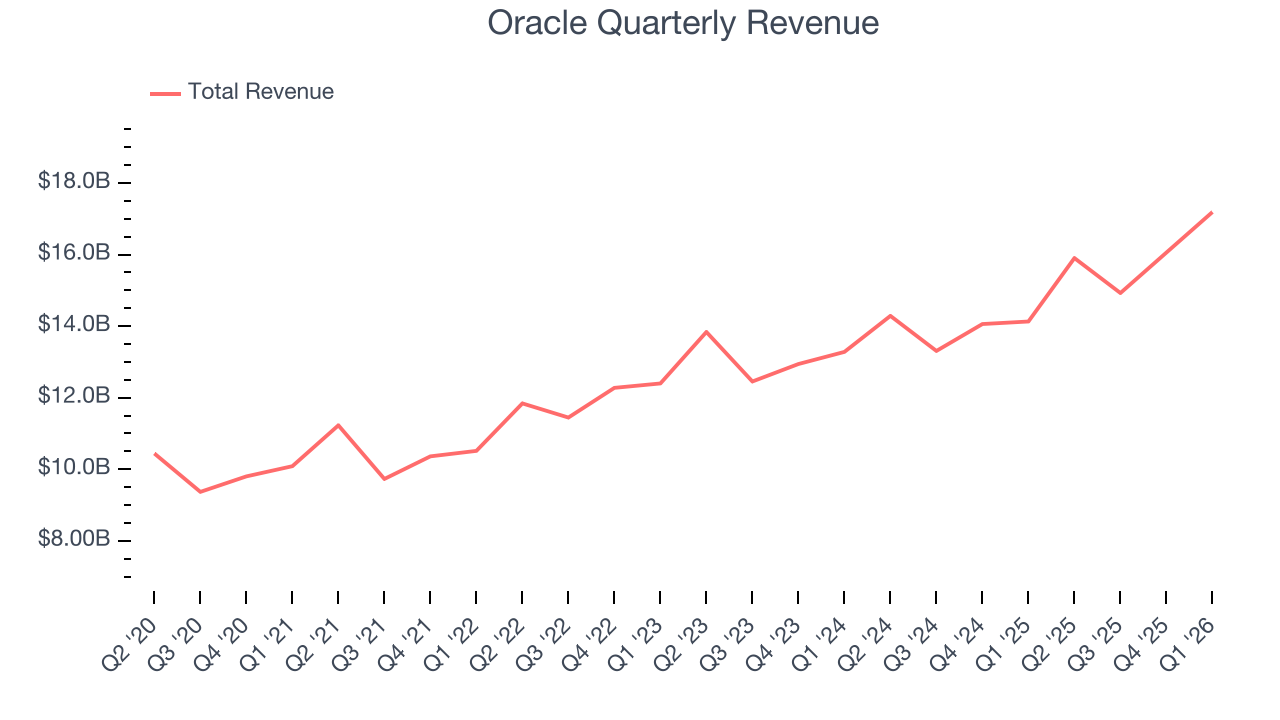

Enterprise software giant Oracle (NYSE:ORCL) beat Wall Street’s revenue expectations in Q1 CY2026, with sales up 21.7% year on year to $17.19 billion. The company expects next quarter’s revenue to be around $19.08 billion, close to analysts’ estimates. Its non-GAAP profit of $1.79 per share was 5.7% above analysts’ consensus estimates.

Oracle (ORCL) Q1 CY2026 Highlights:

- Revenue: $17.19 billion vs analyst estimates of $16.93 billion (21.7% year-on-year growth, 1.5% beat)

- Adjusted EPS: $1.79 vs analyst estimates of $1.69 (5.7% beat)

- Adjusted Operating Income: $7.38 billion vs analyst estimates of $7.20 billion (42.9% margin, 2.4% beat)

- Revenue Guidance for Q2 CY2026 is $19.08 billion at the midpoint, roughly in line with what analysts were expecting

- Adjusted EPS guidance for Q2 CY2026 is $1.98 at the midpoint, above analyst estimates of $1.92

- Operating Margin: 31.8%, in line with the same quarter last year

- Free Cash Flow was -$24.74 billion compared to -$9.97 billion in the previous quarter

- Billings: $16.97 billion at quarter end, up 24.1% year on year

- Market Capitalization: $435.6 billion

Company Overview

Starting as a database company in 1977 and now powering mission-critical systems across the globe, Oracle (NYSE:ORCL) provides enterprise software and hardware products and services that help businesses manage their information technology needs.

Oracle organizes its business into three main segments: cloud and license, hardware, and services. The cloud and license segment is its largest, offering both cloud-based subscription services and traditional software licenses with support. This includes database management systems, middleware, and enterprise applications like ERP, HCM, and SCM that help organizations run their operations.

Oracle Cloud Infrastructure (OCI) is the company's cloud computing platform, designed to compete with Amazon Web Services, Microsoft Azure, and Google Cloud. It includes computing, storage, networking, and database services, with Oracle's Autonomous Database as a flagship offering that uses machine learning to automate routine database administration tasks.

A typical Oracle customer might be a large financial institution using Oracle Fusion Cloud ERP to manage its financial operations, Oracle Database to store customer information, and Oracle Exadata hardware to power its data center. The bank would pay Oracle through subscription fees for cloud services, license fees for software, support fees for maintenance, and possibly consulting fees for implementation services.

The company has been transitioning its business model from traditional on-premise software licenses to cloud subscriptions, allowing customers flexibility in deployment options – public cloud, hybrid cloud, or on-premise. Oracle generates revenue through initial license sales or subscription fees, ongoing support contracts, hardware sales, and professional services. With operations spanning 175 countries, Oracle serves businesses across all major industries, government agencies, and educational institutions.

4. Data Infrastructure

Generating insights from system level data is an increasing priority for most businesses, but to do so requires connecting and analyzing piles of data stored and siloed in separate databases. This is the demand driver for cloud based data infrastructure software providers, who can more readily integrate, distribute and process information vs. legacy on-premise software providers.

Oracle competes with major technology providers including Microsoft (NASDAQ:MSFT), Amazon Web Services (NASDAQ:AMZN), Google Cloud (NASDAQ:GOOGL), IBM (NYSE:IBM), and SAP (NYSE:SAP) in enterprise software and cloud services. In healthcare IT, following its Cerner acquisition, Oracle also competes with Epic Systems, Allscripts (NASDAQ:MDRX), and athenahealth.

5. Revenue Growth

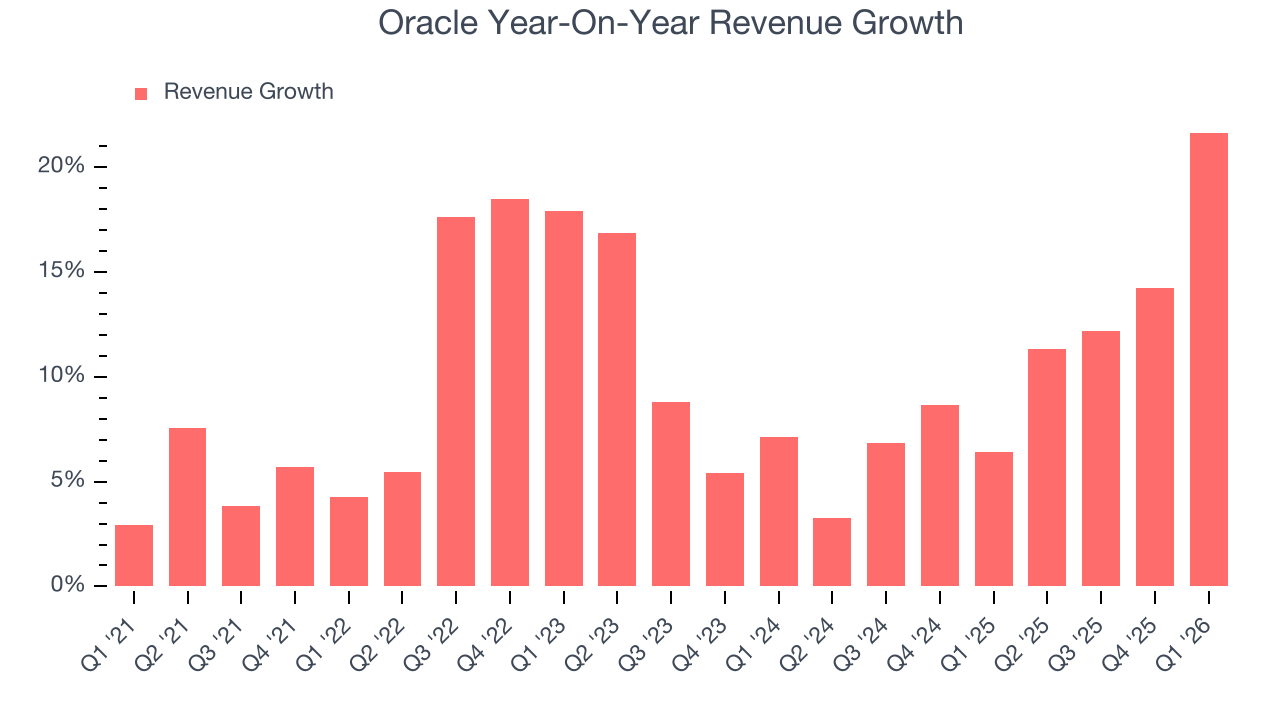

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Oracle grew its sales at a 10.1% compounded annual growth rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the software sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. Oracle’s annualized revenue growth of 10.5% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

This quarter, Oracle reported robust year-on-year revenue growth of 21.7%, and its $17.19 billion of revenue topped Wall Street estimates by 1.5%. Company management is currently guiding for a 20% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 25.7% over the next 12 months, an improvement versus the last two years. This projection is eye-popping for a company of its scale and implies its newer products and services will spur better top-line performance.

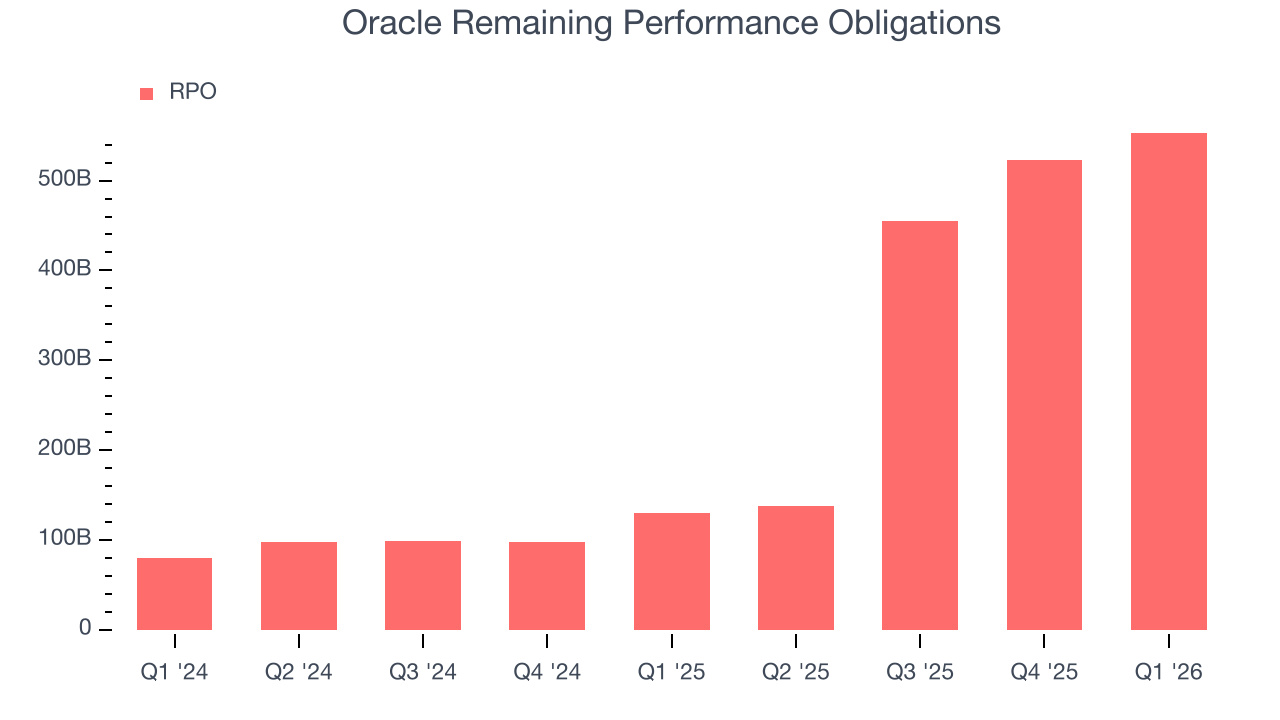

6. Remaining Performance Obligations

In addition to reported revenue, it is useful to analyze RPO, or remaining performance obligations, for Oracle because it shows the value of contracted services to be delivered in the future. It therefore gives visibility into future revenue.

Oracle’s RPO punched in at $553 billion in Q1, and over the last four quarters, its growth was fantastic as it averaged 291% year-on-year increases. This alternate topline metric grew faster than total sales, which likely means contracted services not yet delivered are growing faster than services already delivered (the criteria for revenue recognition). That could be a good sign for future revenue growth.

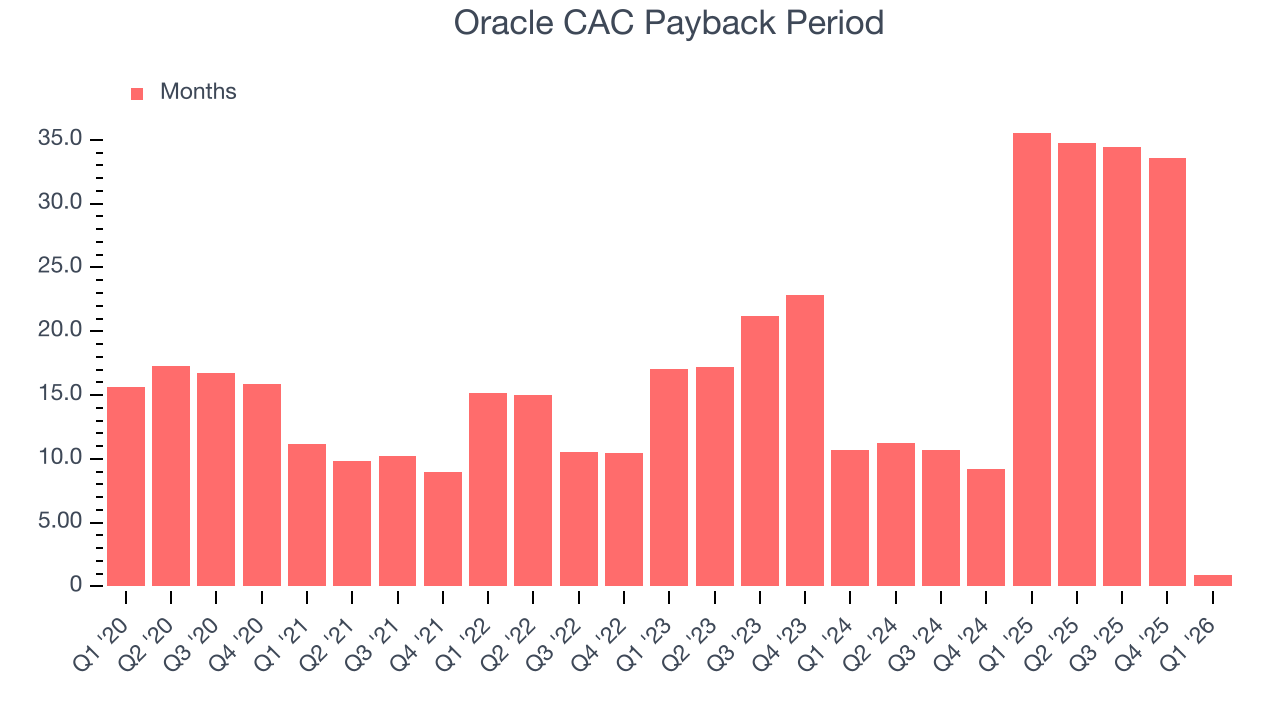

7. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

Oracle is extremely efficient at acquiring new customers, and its CAC payback period checked in at 0.9 months this quarter. The company’s rapid recovery of its customer acquisition costs indicates it has a highly differentiated product offering and a strong brand reputation due to its scale. These dynamics give Oracle more resources to pursue new product initiatives while maintaining the flexibility to increase its sales and marketing investments.

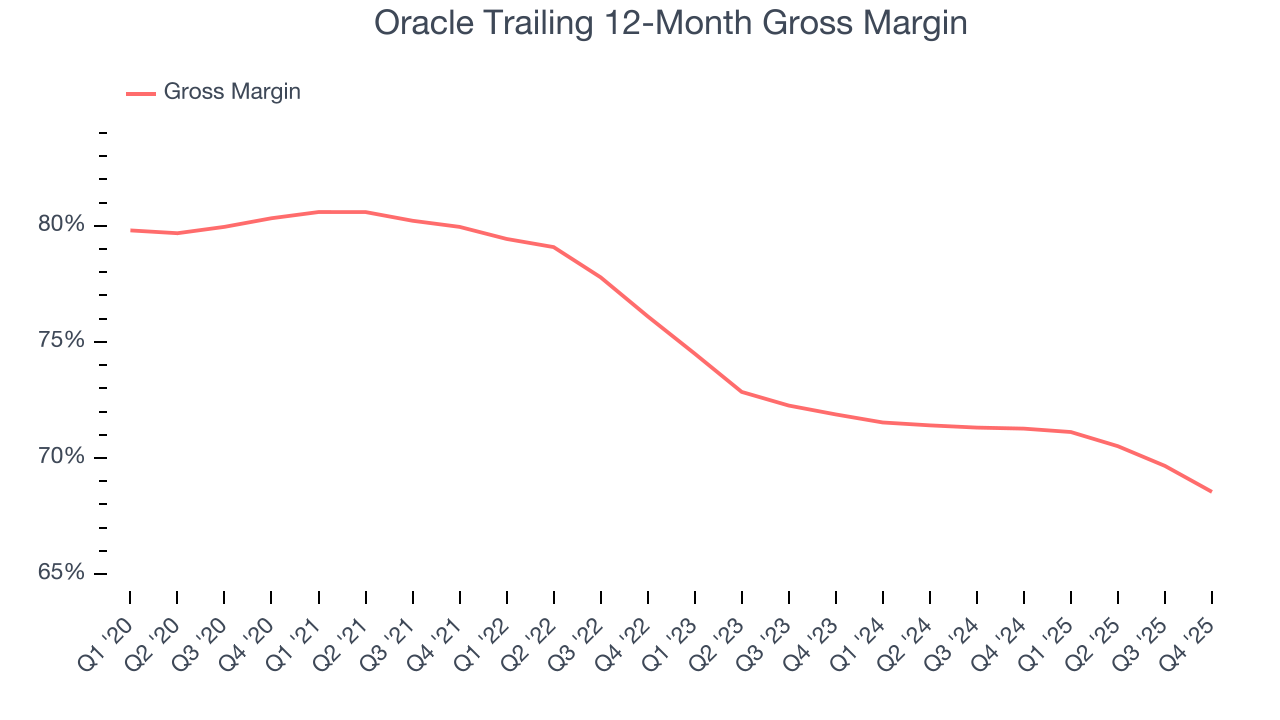

8. Gross Margin & Pricing Power

For software companies like Oracle, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

Oracle’s gross margin is worse than the software industry average, giving it less room than its competitors to hire new talent that can expand its products and services. As you can see below, it averaged a 68% gross margin over the last year. Said differently, Oracle had to pay a chunky $31.99 to its service providers for every $100 in revenue.

9. Operating Margin

While many software businesses point investors to their adjusted profits, which exclude stock-based compensation (SBC), we prefer GAAP operating margin because SBC is a legitimate expense used to attract and retain talent. This metric shows how much revenue remains after accounting for all core expenses – everything from the cost of goods sold to sales and R&D.

Oracle has been a well-oiled machine over the last year. It demonstrated elite profitability for a software business, boasting an average operating margin of 30.6%. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Looking at the trend in its profitability, Oracle’s operating margin might fluctuated slightly but has generally stayed the same over the last two years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Oracle generated an operating margin profit margin of 31.8%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

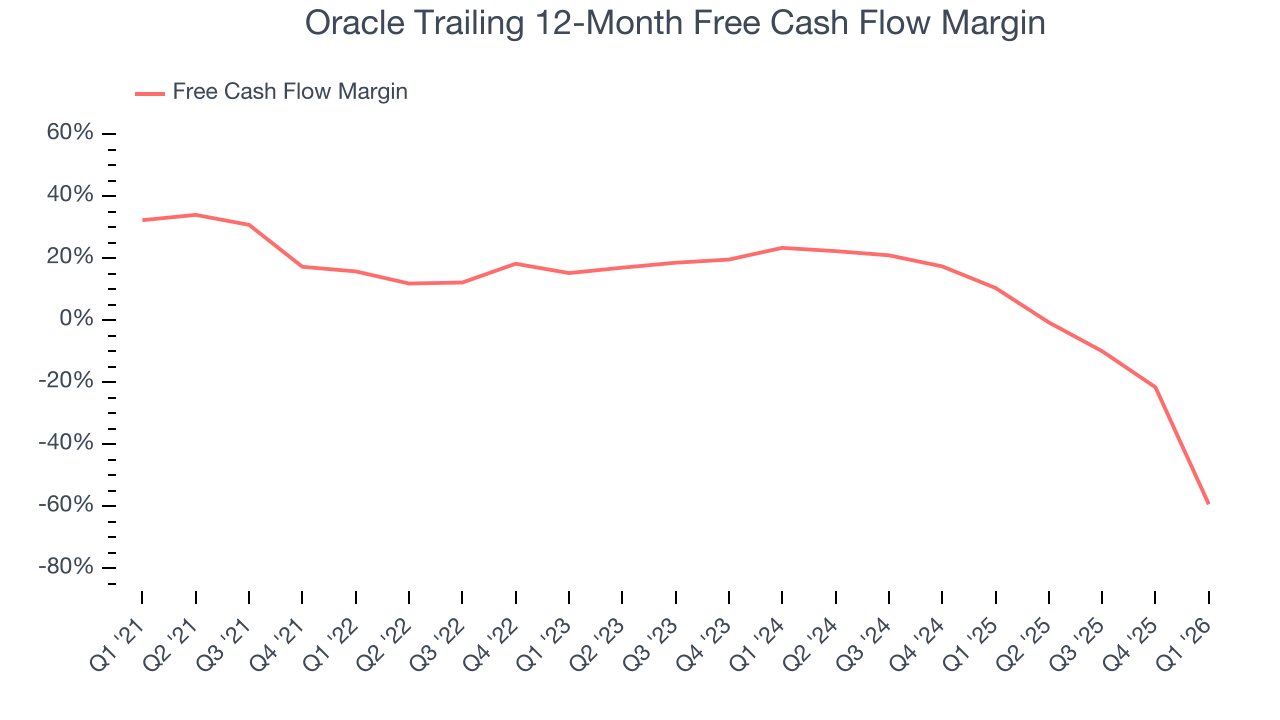

10. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Oracle’s demanding reinvestments have drained its resources over the last year, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 59.3%, meaning it lit $59.28 of cash on fire for every $100 in revenue. This is a stark contrast from its operating margin, and its investments (i.e., stocking inventory, building new facilities) are the primary culprit.

Oracle burned through $24.74 billion of cash in Q1, equivalent to a negative 144% margin. The company’s cash burn increased meaningfully year on year while its cash conversion fell 144.4 percentage points. This relationship shows Oracle’s management team spent more cash this quarter but was less efficient at generating sales with that cash.

Over the next year, analysts predict Oracle will continue burning cash, albeit to a lesser extent. Their consensus estimates imply its free cash flow margin of negative 59.3% for the last 12 months will increase to negative 23.7%.

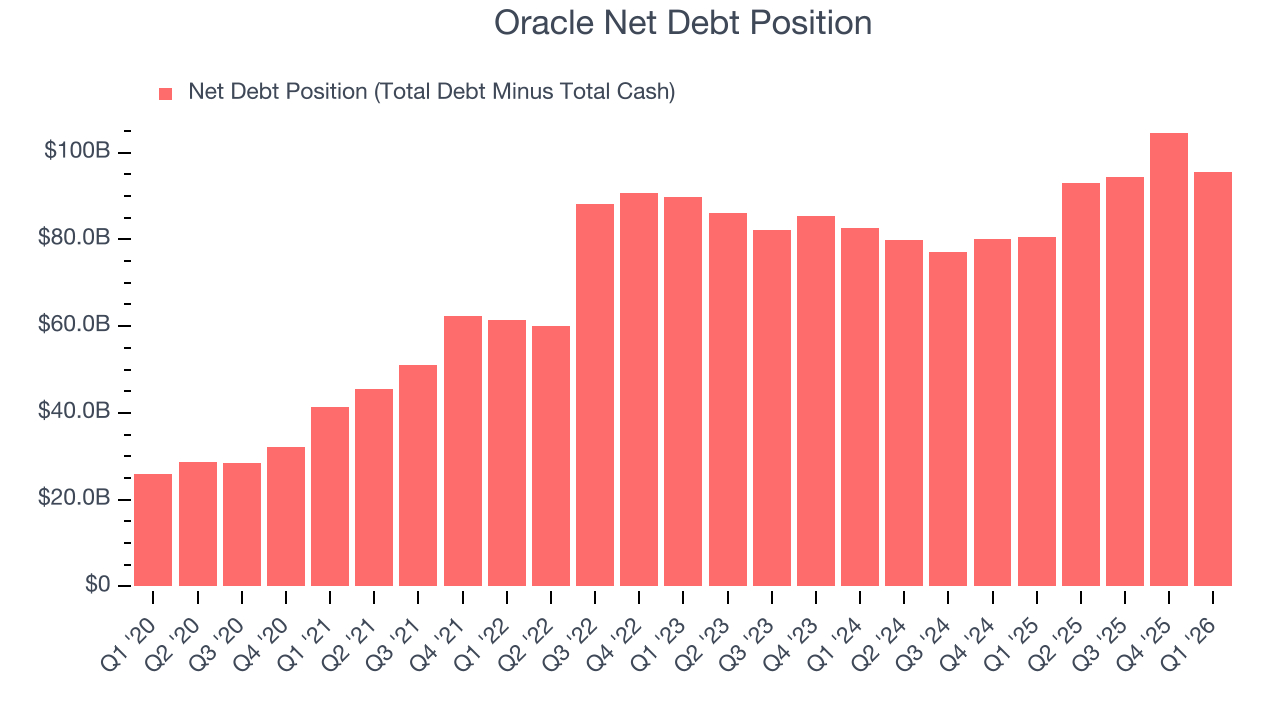

11. Balance Sheet Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

Oracle burned through $24.74 billion of cash over the last year, and its $134.6 billion of debt exceeds the $39.13 billion of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

Unless the Oracle’s fundamentals change quickly, it might find itself in a position where it must raise capital from investors to continue operating. Whether that would be favorable is unclear because dilution is a headwind for shareholder returns.

We remain cautious of Oracle until it generates consistent free cash flow or any of its announced financing plans materialize on its balance sheet.

12. Key Takeaways from Oracle’s Q1 Results

We enjoyed seeing Oracle beat analysts’ billings expectations this quarter. We were also glad its EPS guidance for next quarter exceeded Wall Street’s estimates. On the other hand, its revenue guidance for next quarter was in line. Overall, this print had some key positives. The stock traded up 8.2% to $162.39 immediately after reporting.

13. Is Now The Time To Buy Oracle?

Updated: March 14, 2026 at 1:02 AM EDT

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

Oracle’s business quality ultimately falls short of our standards. First off, its revenue growth was uninspiring over the last five years. While its efficient sales strategy allows it to target and onboard new users at scale, the downside is its operating margin hasn't moved over the last year. On top of that, its growth is coming at the cost of significant cash burn.

Oracle’s price-to-sales ratio based on the next 12 months is 5.6x. Investors with a higher risk tolerance might like the company, but we don’t really see a big opportunity at the moment. We're fairly confident there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $248.60 on the company (compared to the current share price of $154.33).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.