Procore Technologies (PCOR)

Procore Technologies doesn’t excite us. Its revenue growth has decelerated and its historical operating losses don’t give us confidence in a turnaround.― StockStory Analyst Team

1. News

2. Summary

Why We Think Procore Technologies Will Underperform

With a mission to build software for the people that build the world, Procore Technologies (NYSE:PCOR) provides cloud-based software that enables owners, contractors, and other stakeholders to collaborate and manage construction projects from any device.

- Operating profits and efficiency rose over the last year as it benefited from some fixed cost leverage

- Track record of operating margin losses stem from its decision to pursue growth instead of profits

- One positive is that its software is difficult to replicate at scale and leads to a top-tier gross margin of 79.6%

Procore Technologies doesn’t check our boxes. There are superior opportunities elsewhere.

Why There Are Better Opportunities Than Procore Technologies

Procore Technologies is trading at $54.28 per share, or 5.8x forward price-to-sales. This multiple rich for the business quality. Not a great combination.

We’d rather pay up for companies with elite fundamentals than get a decent price on a poor one. High-quality businesses often have more durable earnings power, helping us sleep well at night.

3. Procore Technologies (PCOR) Research Report: Q4 CY2025 Update

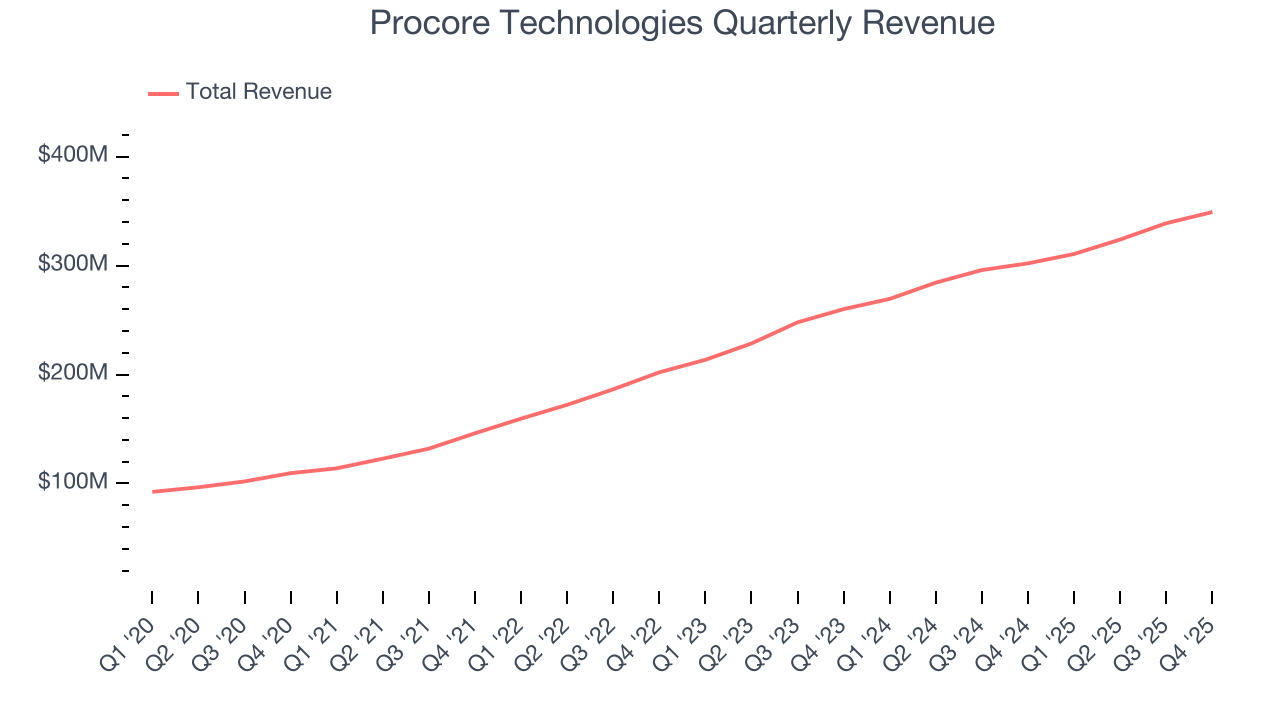

Construction management software provider Procore Technologies (NYSE:PCOR) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 15.6% year on year to $349.1 million. Guidance for next quarter’s revenue was better than expected at $352 million at the midpoint, 0.8% above analysts’ estimates. Its non-GAAP profit of $0.37 per share was 3.8% above analysts’ consensus estimates.

Procore Technologies (PCOR) Q4 CY2025 Highlights:

- Revenue: $349.1 million vs analyst estimates of $340.8 million (15.6% year-on-year growth, 2.4% beat)

- Adjusted EPS: $0.37 vs analyst estimates of $0.36 (3.8% beat)

- Revenue Guidance for Q1 CY2026 is $352 million at the midpoint, roughly in line with what analysts were expecting

- Operating Margin: -12.3%, up from -21.9% in the same quarter last year

- Free Cash Flow Margin: 25.8%, up from 20% in the previous quarter

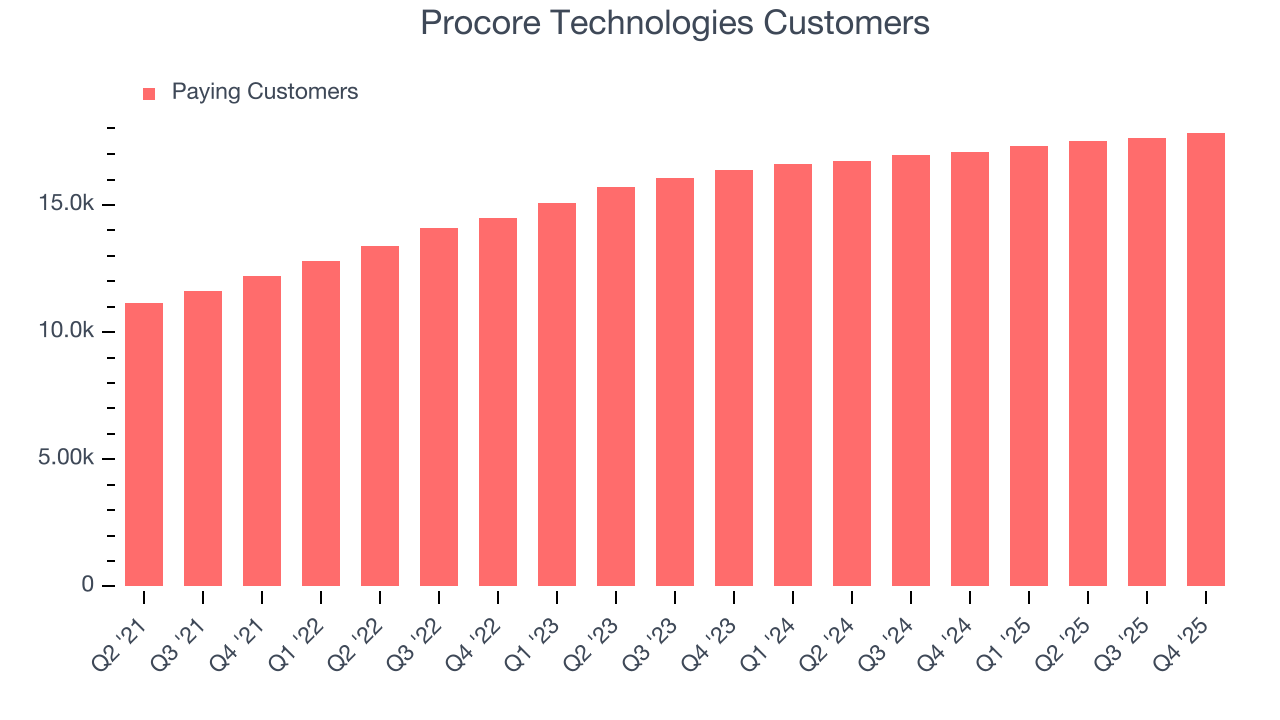

- Customers: 17,850, up from 17,623 in the previous quarter

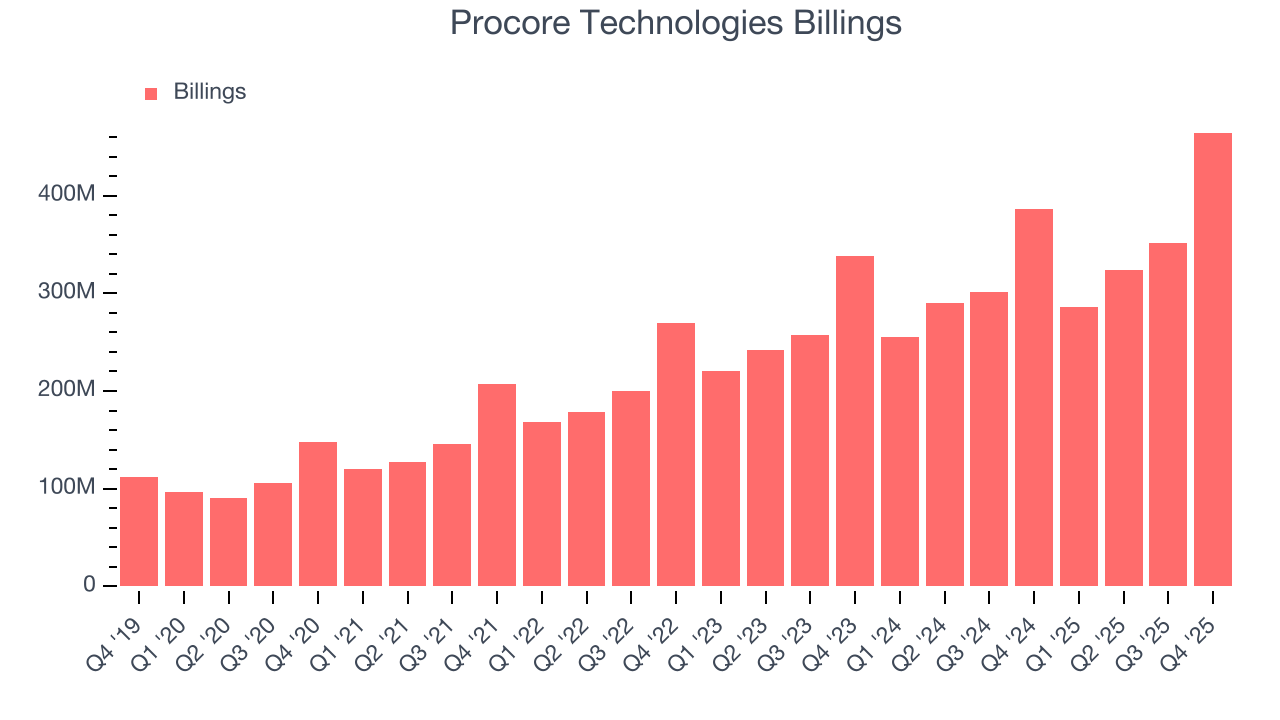

- Billings: $464.5 million at quarter end, up 20.3% year on year

- Market Capitalization: $7.56 billion

Company Overview

With a mission to build software for the people that build the world, Procore Technologies (NYSE:PCOR) provides cloud-based software that enables owners, contractors, and other stakeholders to collaborate and manage construction projects from any device.

Procore's platform serves as the system of record for construction projects, connecting everyone involved through five integrated product categories: Preconstruction, Project Execution, Workforce Management, Financial Management, and Construction Intelligence. The platform allows users to manage critical tasks including bidding, scheduling, quality control, safety compliance, labor tracking, and budget monitoring—all accessible from offices or jobsites via computers, smartphones, and tablets.

What distinguishes Procore is its unlimited user model, which allows customers to invite all project participants to collaborate without per-user fees. This approach facilitates widespread adoption across project teams and creates network effects as collaborators often become paying customers to manage their own portfolios. The platform also features an extensive App Marketplace with over 500 third-party integrations, enabling customers to connect Procore with accounting software, document management systems, and other specialized tools.

For example, a general contractor might use Procore to share updated blueprints with specialty contractors, track labor hours against budget in real-time, document safety issues with photos, and generate financial reports for the project owner—all while maintaining a complete digital record of the project. Procore monetizes its offerings through subscriptions, with pricing typically based on the number of products and the annual construction volume managed on the platform rather than charging per user.

4. Design Software

The demand for rich, interactive 2D, 3D, VR and AR experiences is growing, and while the ubiquitous metaverse might still be more of a buzzword than a real thing, what is real is the demand for the tools to create these experiences, whether they are games, 3D tours or interactive movies.

Procore's main competitors include Autodesk Construction Cloud (NASDAQ:ADSK), Oracle Construction and Engineering (NYSE:ORCL), Trimble (NASDAQ:TRMB), and privately-held companies like Fieldwire, PlanGrid (acquired by Autodesk), and Buildertrend.

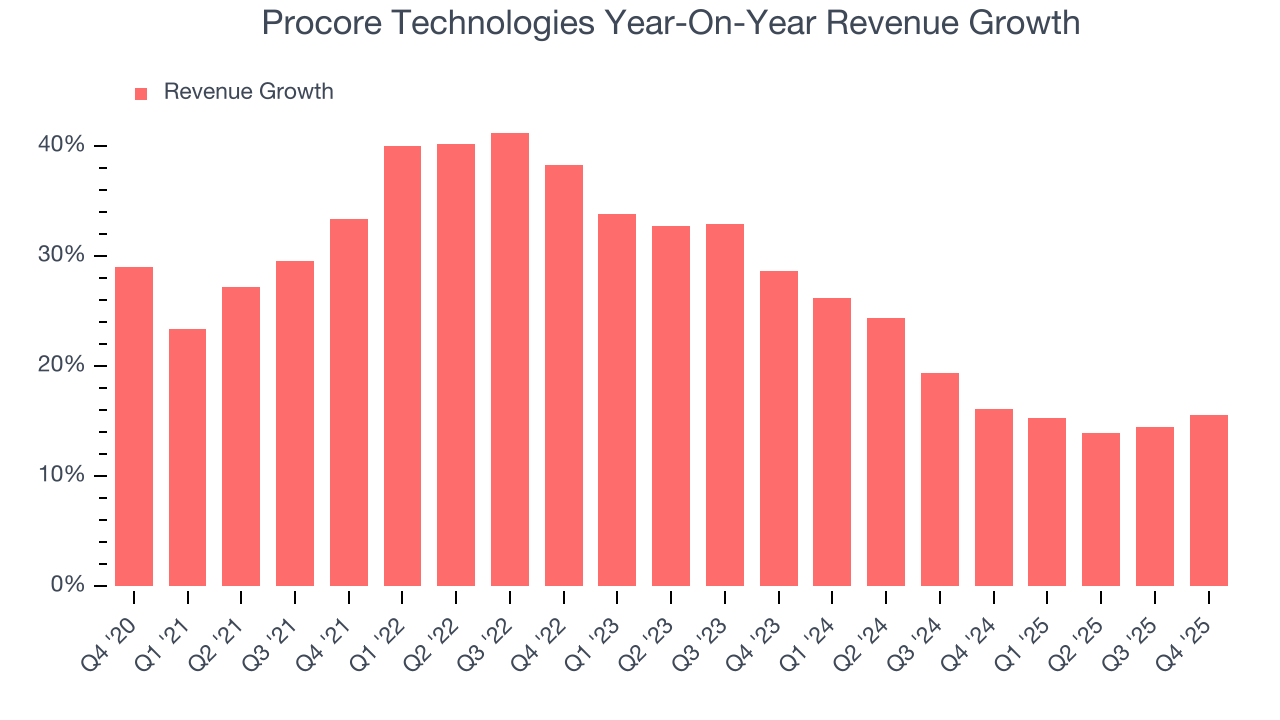

5. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Procore Technologies grew its sales at an impressive 27% compounded annual growth rate. Its growth beat the average software company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within software, a half-decade historical view may miss recent innovations or disruptive industry trends. Procore Technologies’s annualized revenue growth of 18% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Procore Technologies reported year-on-year revenue growth of 15.6%, and its $349.1 million of revenue exceeded Wall Street’s estimates by 2.4%. Company management is currently guiding for a 13.3% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 11.1% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and indicates its products and services will see some demand headwinds.

6. Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Procore Technologies’s billings punched in at $464.5 million in Q4, and over the last four quarters, its growth slightly outpaced the sector as it averaged 15.1% year-on-year increases. This performance aligned with its total sales growth and shows the company is successfully converting sales into cash. Its growth also enhances liquidity and provides a solid foundation for future investments.

7. Customer Base

Procore Technologies reported 17,850 customers at the end of the quarter, a sequential increase of 227. That’s a little better than last quarter and quite a bit above the typical growth we’ve seen over the previous year. Shareholders should take this as an indication that Procore Technologies’s go-to-market strategy is working well.

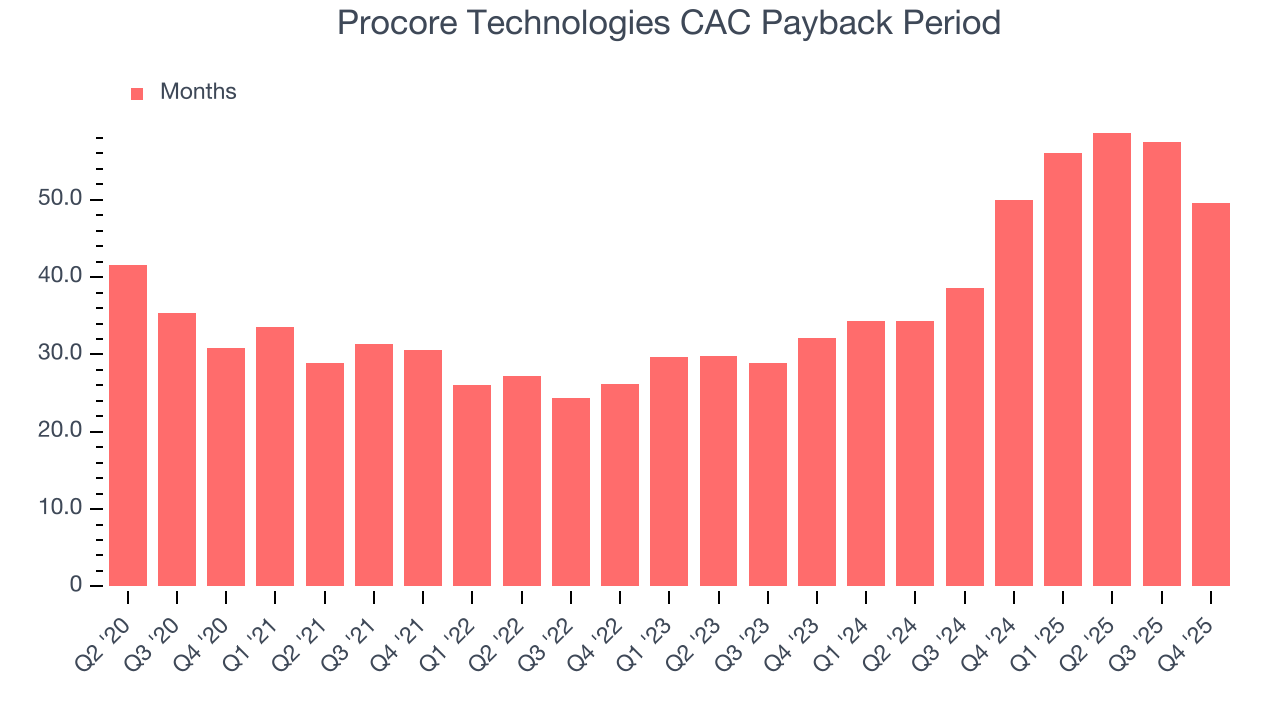

8. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

Procore Technologies does a decent job acquiring new customers, and its CAC payback period checked in at 49.6 months this quarter. The company’s relatively fast recovery of its customer acquisition costs gives it the option to accelerate growth by increasing its sales and marketing investments.

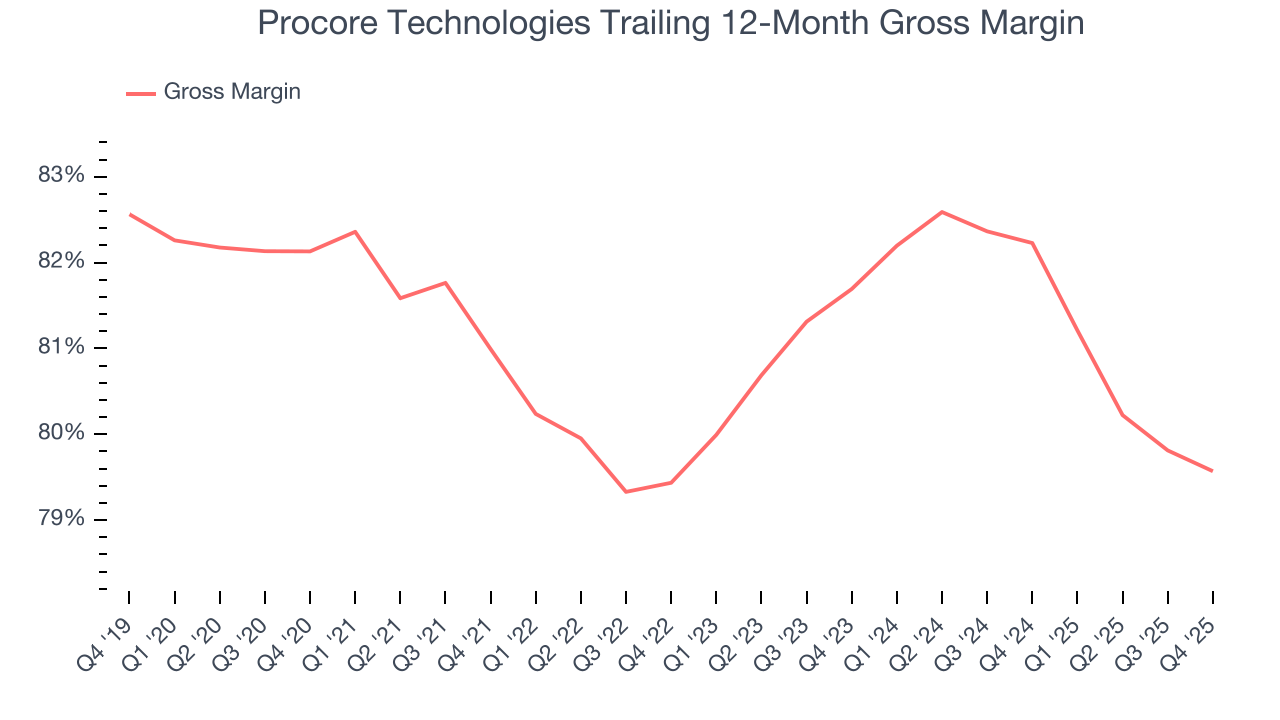

9. Gross Margin & Pricing Power

For software companies like Procore Technologies, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

Procore Technologies’s robust unit economics are better than the broader software industry, an output of its asset-lite business model and pricing power. They also enable the company to fund large investments in new products and sales during periods of rapid growth to achieve outsized profits at scale. As you can see below, it averaged an excellent 79.6% gross margin over the last year. That means Procore Technologies only paid its providers $20.43 for every $100 in revenue.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. Procore Technologies has seen gross margins decline by 2.1 percentage points over the last 2 year, which is among the worst in the software space.

Procore Technologies’s gross profit margin came in at 80.1% this quarter , marking a 1.1 percentage point decrease from 81.2% in the same quarter last year. Procore Technologies’s full-year margin has also been trending down over the past 12 months, decreasing by 2.7 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to lower prices and higher input costs.

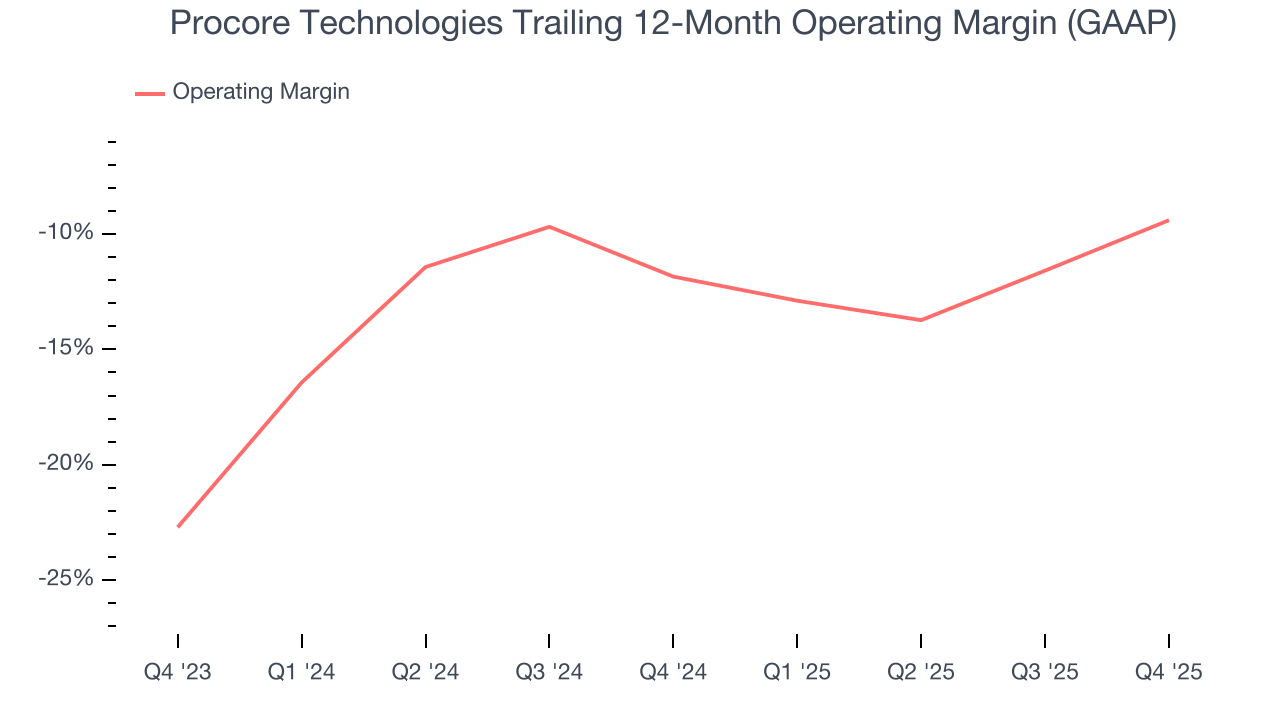

10. Operating Margin

Procore Technologies’s expensive cost structure has contributed to an average operating margin of negative 9.4% over the last year. Unprofitable, high-growth software companies require extra attention because they spend heaps of money to capture market share. As seen in its fast historical revenue growth, this strategy seems to have worked so far, but it’s unclear what would happen if Procore Technologies reeled back its investments. Wall Street seems to think it will face some obstacles, and we tend to agree.

Over the last two years, Procore Technologies’s expanding sales gave it operating leverage as its margin rose by 2.4 percentage points. Still, it will take much more for the company to reach long-term profitability.

This quarter, Procore Technologies generated a negative 12.3% operating margin.

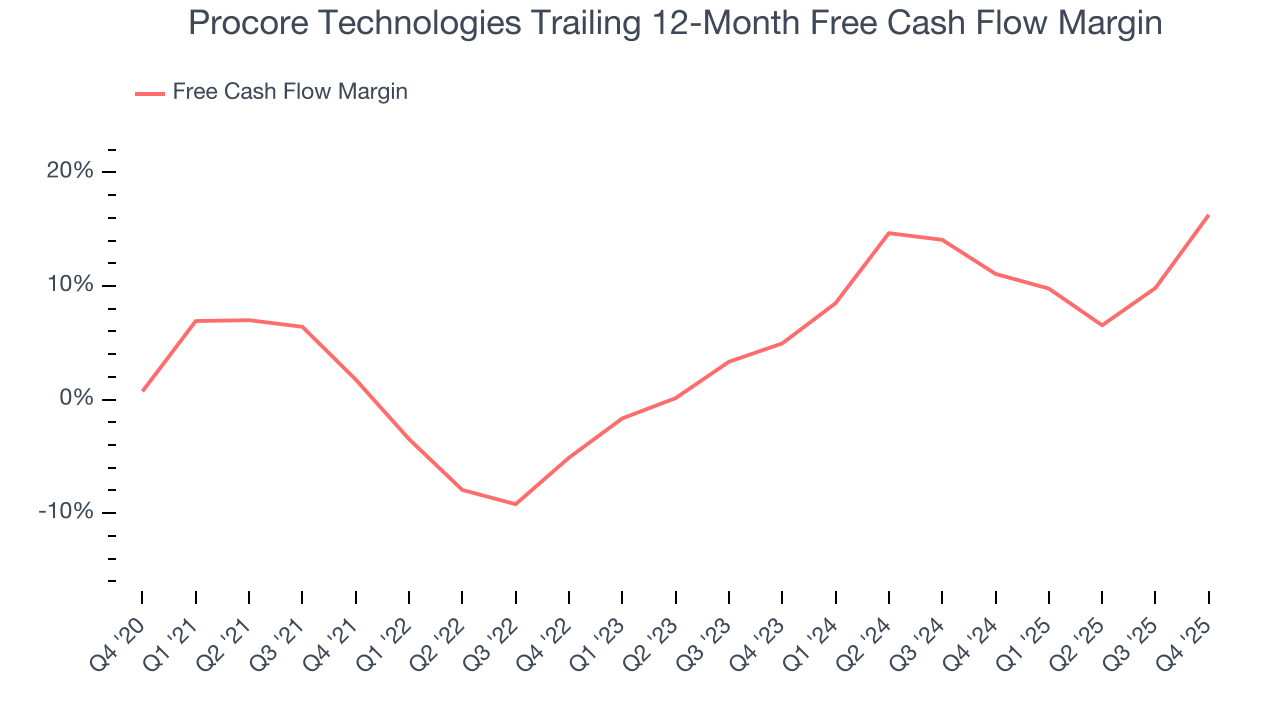

11. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Procore Technologies has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 16.3% over the last year, slightly better than the broader software sector.

Procore Technologies’s free cash flow clocked in at $90.08 million in Q4, equivalent to a 25.8% margin. This result was good as its margin was 25.7 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, causing temporary swings. Long-term trends trump fluctuations.

Over the next year, analysts predict Procore Technologies’s cash conversion will slightly improve. Their consensus estimates imply its free cash flow margin of 16.3% for the last 12 months will increase to 16.9%, it options for capital deployment (investments, share buybacks, etc.).

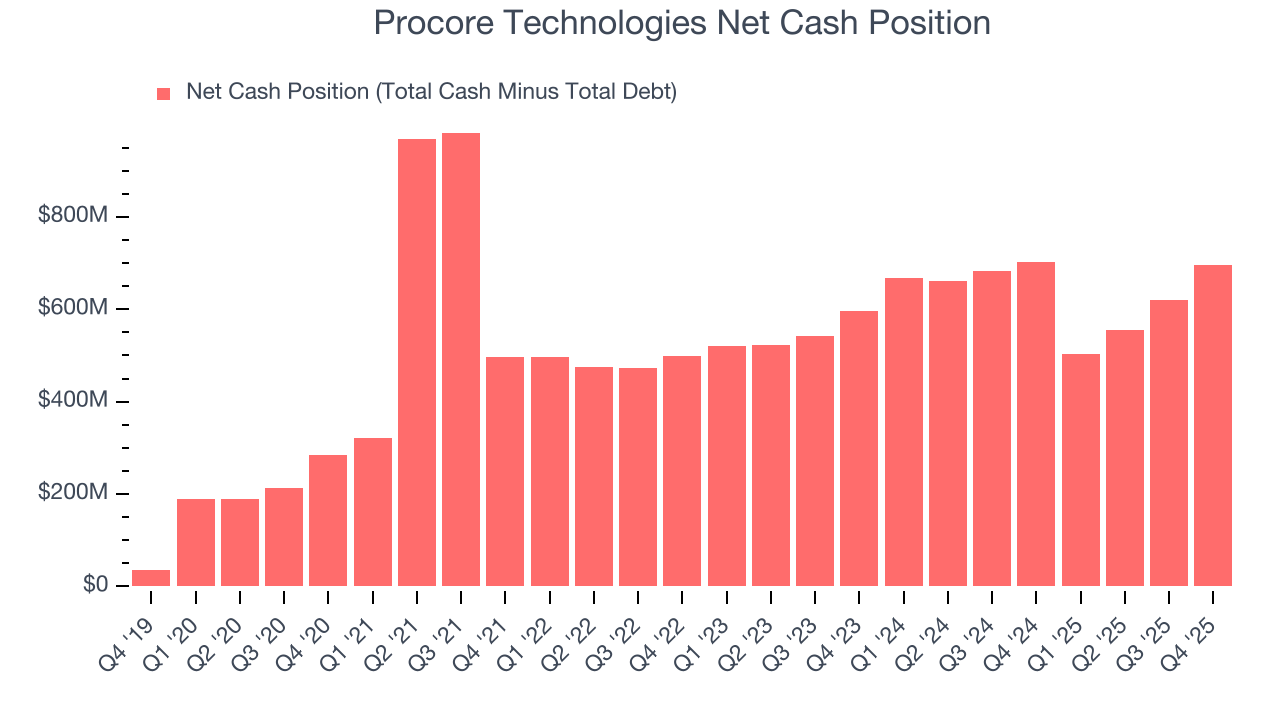

12. Balance Sheet Assessment

One of the best ways to mitigate bankruptcy risk is to hold more cash than debt.

Procore Technologies is a well-capitalized company with $768.5 million of cash and $72.41 million of debt on its balance sheet. This $696.1 million net cash position is 8.6% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

13. Key Takeaways from Procore Technologies’s Q4 Results

We were impressed by how significantly Procore Technologies blew past analysts’ billings expectations this quarter. We were also glad its customer growth accelerated. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 10.5% to $52.91 immediately after reporting.

14. Is Now The Time To Buy Procore Technologies?

Updated: March 28, 2026 at 10:31 PM EDT

When considering an investment in Procore Technologies, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

Procore Technologies isn’t a terrible business, but it doesn’t pass our bar. Although its revenue growth was strong over the last five years, it’s expected to deteriorate over the next 12 months and its expanding operating margin shows it’s becoming more efficient at building and selling its software. And while the company’s admirable gross margin indicates excellent unit economics, the downside is its operating margins reveal poor profitability compared to other software companies.

Procore Technologies’s price-to-sales ratio based on the next 12 months is 5.8x. Beauty is in the eye of the beholder, but we don’t really see a big opportunity at the moment. We're fairly confident there are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $72.56 on the company (compared to the current share price of $54.28).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.