PennyMac Financial Services (PFSI)

We’re wary of PennyMac Financial Services. Its declining sales show demand has evaporated, a red flag for investors seeking high-quality stocks.― StockStory Analyst Team

1. News

2. Summary

Why PennyMac Financial Services Is Not Exciting

Founded during the 2008 financial crisis to help address the mortgage market meltdown, PennyMac Financial Services (NYSE:PFSI) is a specialty financial services company that originates, services, and manages investments related to residential mortgage loans in the United States.

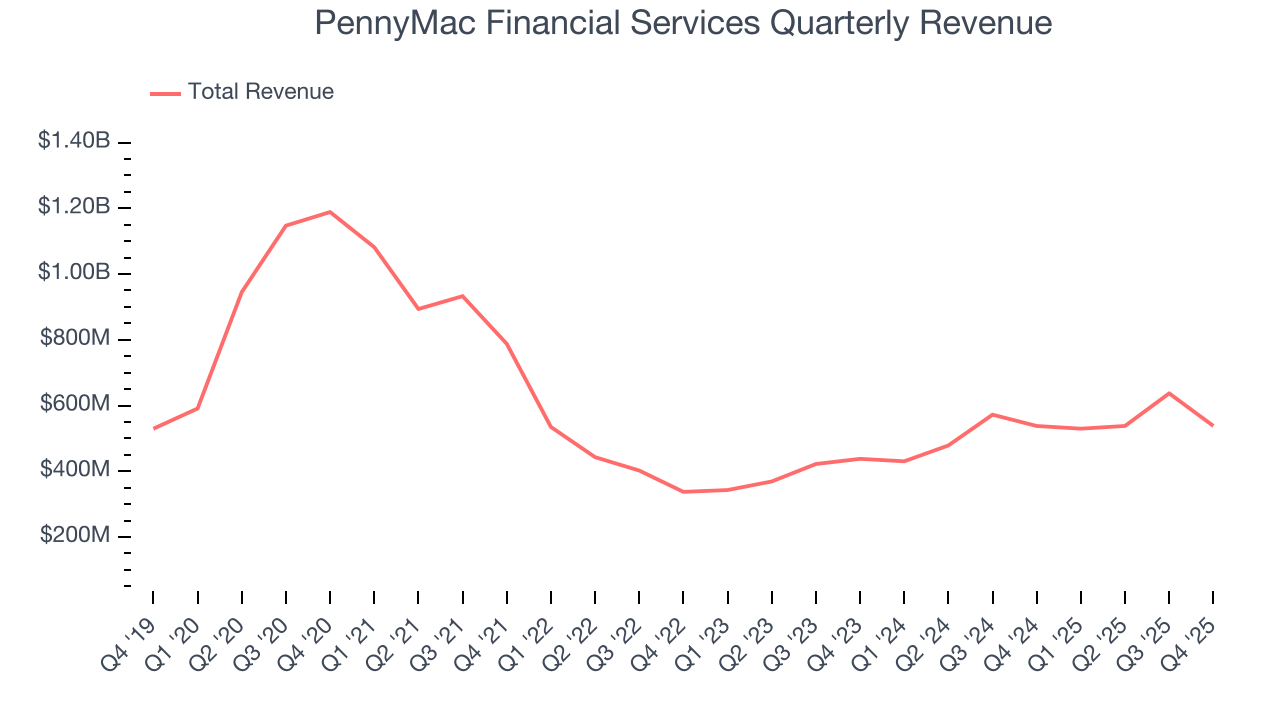

- Sales tumbled by 10.4% annually over the last five years, showing market trends are working against its favor during this cycle

- Earnings per share have contracted by 10% annually over the last five years, a headwind for returns as stock prices often echo long-term EPS performance

- A positive is that its exciting net interest income outlook for the upcoming 12 months calls for 86.2% growth, an acceleration from its five-year trend

PennyMac Financial Services doesn’t live up to our standards. There are more promising alternatives.

Why There Are Better Opportunities Than PennyMac Financial Services

PennyMac Financial Services is trading at $87.25 per share, or 0.9x forward P/B. This multiple is cheaper than most banking peers, but we think this is justified.

Cheap stocks can look like great bargains at first glance, but you often get what you pay for. These mediocre businesses often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. PennyMac Financial Services (PFSI) Research Report: Q4 CY2025 Update

Mortgage banking company PennyMac Financial Services (NYSE:PFSI) missed Wall Street’s revenue expectations in Q4 CY2025, with sales flat year on year at $538 million. Its GAAP profit of $1.97 per share was 39.6% below analysts’ consensus estimates.

PennyMac Financial Services (PFSI) Q4 CY2025 Highlights:

- Revenue: $538 million vs analyst estimates of $640.5 million (flat year on year, 16% miss)

- EPS (GAAP): $1.97 vs analyst expectations of $3.26 (39.6% miss)

- Market Capitalization: $7.64 billion

Company Overview

Founded during the 2008 financial crisis to help address the mortgage market meltdown, PennyMac Financial Services (NYSE:PFSI) is a specialty financial services company that originates, services, and manages investments related to residential mortgage loans in the United States.

PennyMac operates through three main business segments: Production, Servicing, and Investment Management. The Production segment sources new mortgage loans through correspondent production (purchasing loans from other lenders), consumer direct lending (originating loans directly with borrowers online and via call centers), and broker direct lending (working with mortgage brokers).

In its correspondent channel, PennyMac purchases loans that meet specific investor guidelines, particularly those insured or guaranteed by government agencies like FHA, VA, and USDA. These loans are typically pooled into mortgage-backed securities guaranteed by Ginnie Mae and sold to institutional investors. The company earns revenue through loan origination fees, interest income during the holding period, gains on sales, and by retaining the mortgage servicing rights.

The Servicing segment handles loan administration activities including collecting payments, managing escrow accounts for taxes and insurance, assisting borrowers with inquiries, and managing delinquencies and foreclosures when necessary. PennyMac services loans both as the owner of mortgage servicing rights and as a subservicer for PennyMac Mortgage Investment Trust (PMT), a publicly traded mortgage REIT that the company manages.

Through its investment management subsidiary, PNMAC Capital Management, PennyMac earns management fees based on PMT's net assets and potential incentive compensation tied to investment performance. This relationship creates a symbiotic business model where PennyMac Financial Services provides operational expertise while PMT supplies investment capital for mortgage-related assets.

4. Thrifts & Mortgage Finance

Thrifts & Mortgage Finance institutions operate by accepting deposits and extending loans primarily for residential mortgages, earning revenue through interest rate spreads (difference between lending rates and borrowing costs) and origination fees. The industry benefits from demographic tailwinds as millennials enter prime homebuying age, technological advancements streamlining the loan approval process, and potential interest rate stabilization improving affordability. However, significant headwinds include net interest margin compression during rate volatility, increased competition from fintech disruptors offering digital-first experiences, mounting regulatory compliance costs, and potential housing market corrections that could impact loan portfolios and default rates.

PennyMac Financial Services competes with large financial institutions and other independent mortgage producers and servicers, including Rocket Mortgage (NYSE:RKT), Mr. Cooper Group (NASDAQ:COOP), and United Wholesale Mortgage (NYSE:UWMC), as well as the cash windows of government-sponsored enterprises Fannie Mae and Freddie Mac.

5. Sales Growth

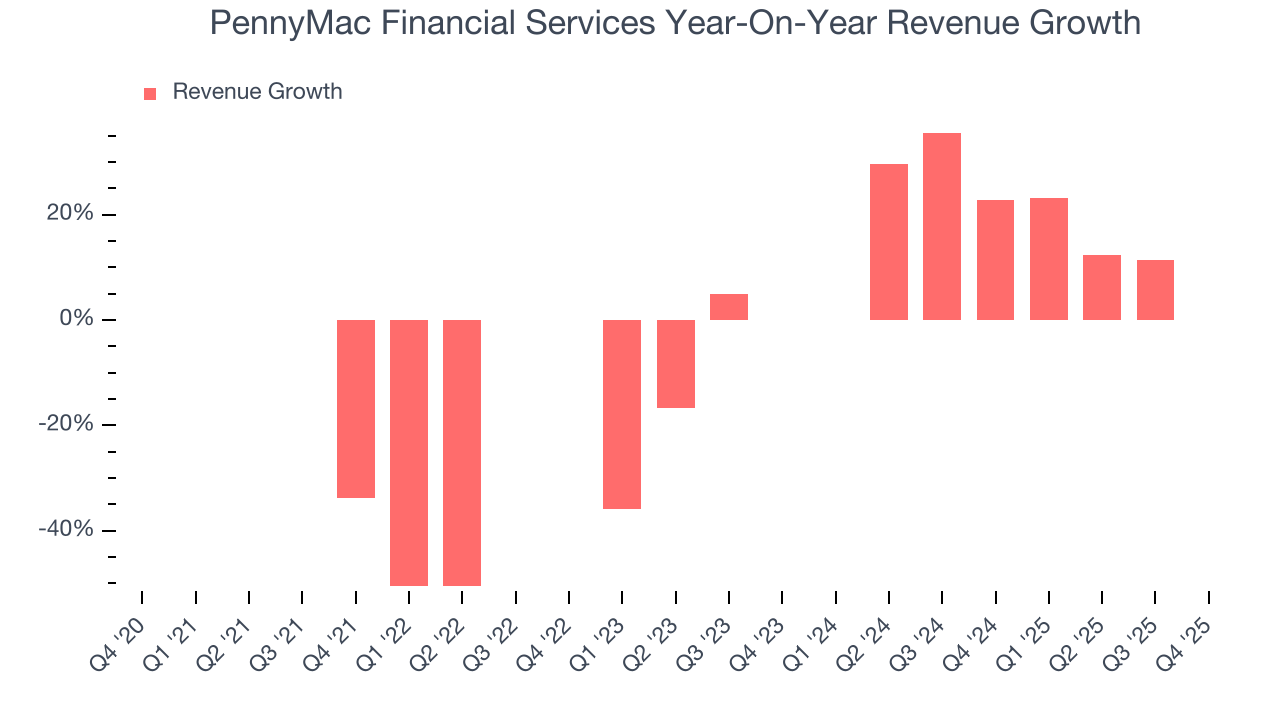

Net interest income and and fee-based revenue are the two pillars supporting bank earnings. The former captures profit from the gap between lending rates and deposit costs, while the latter encompasses charges for banking services, credit products, wealth management, and trading activities. PennyMac Financial Services’s demand was weak over the last five years as its revenue fell at a 10.3% annual rate. This wasn’t a great result and is a rough starting point for our analysis.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. PennyMac Financial Services’s annualized revenue growth of 19.4% over the last two years is above its five-year trend, suggesting its demand recently accelerated.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, PennyMac Financial Services’s $538 million of revenue was flat year on year, falling short of Wall Street’s estimates.

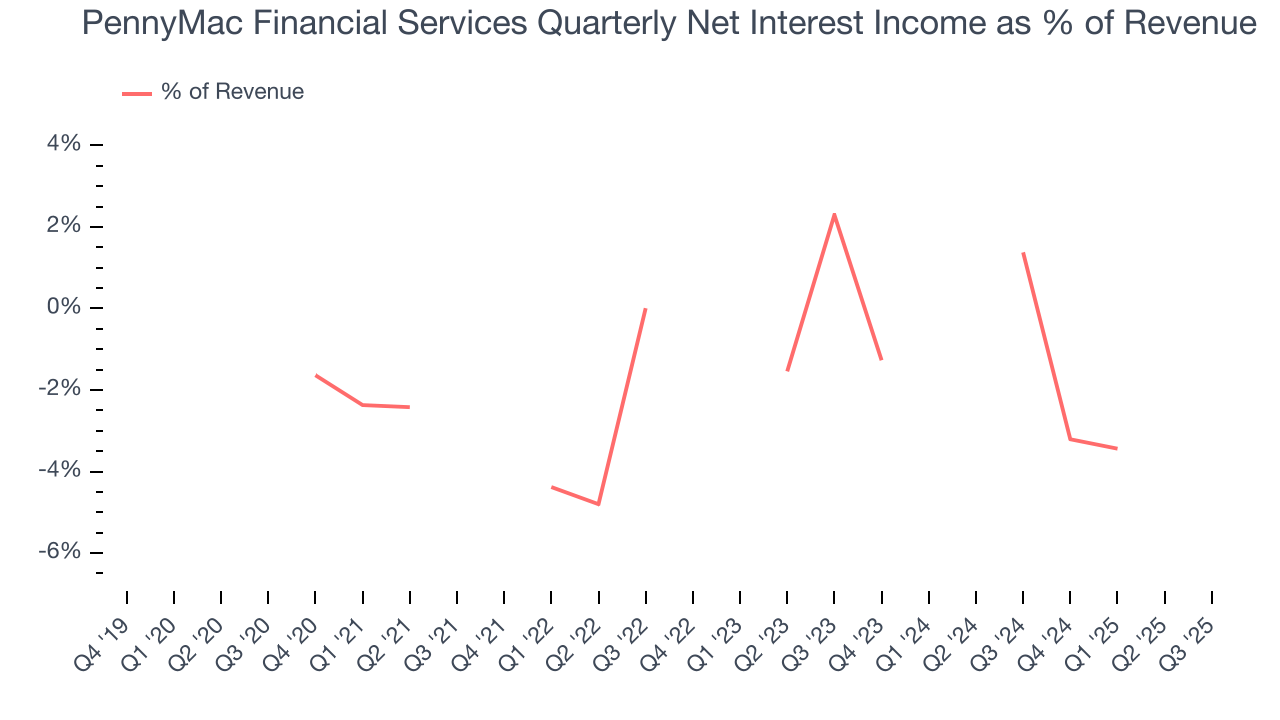

Net interest income made up -1.7% of the company’s total revenue during the last five years, meaning PennyMac Financial Services is well diversified and has a variety of income streams driving its overall growth. Nevertheless, net interest income is critical to analyze for banks because they’re considered a higher-quality, more recurring revenue source by investors.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.6. Earnings Per Share

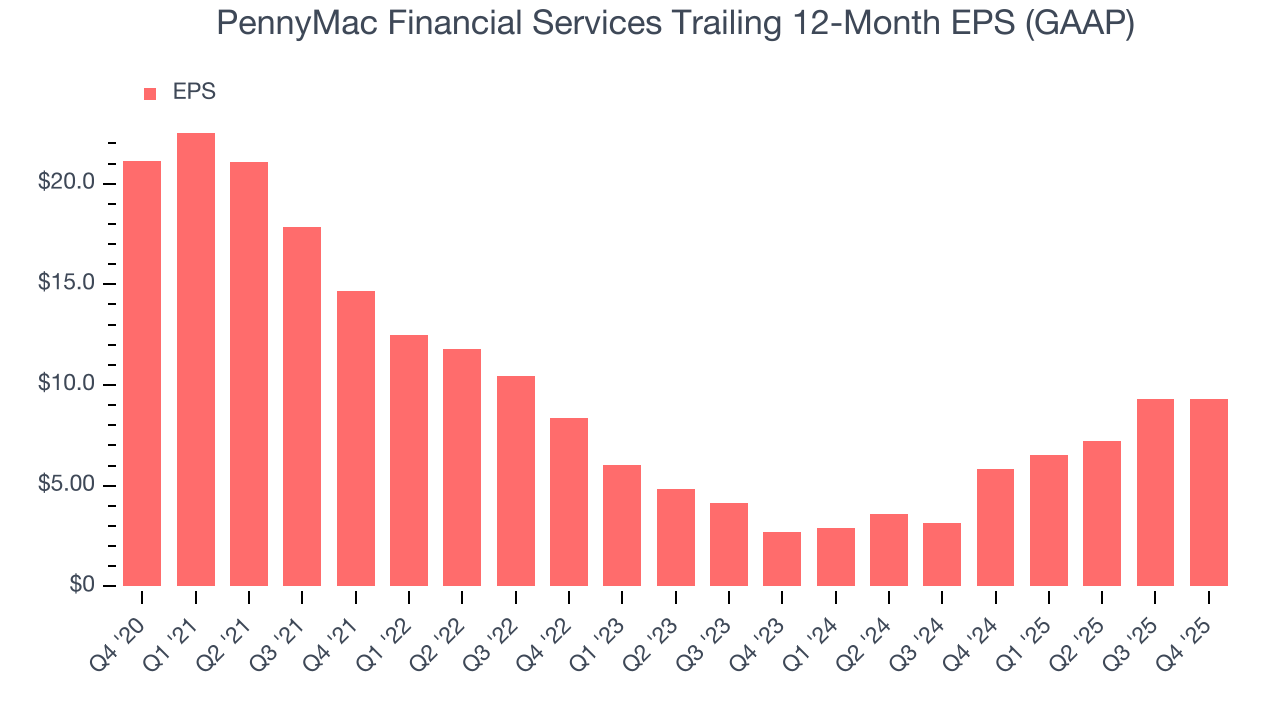

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for PennyMac Financial Services, its EPS declined by 15.1% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For PennyMac Financial Services, its two-year annual EPS growth of 85.2% was higher than its five-year trend. This acceleration made it one of the faster-growing banking companies in recent history.

In Q4, PennyMac Financial Services reported EPS of $1.97, up from $1.95 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates. Over the next 12 months, Wall Street expects PennyMac Financial Services’s full-year EPS of $9.31 to grow 64.1%.

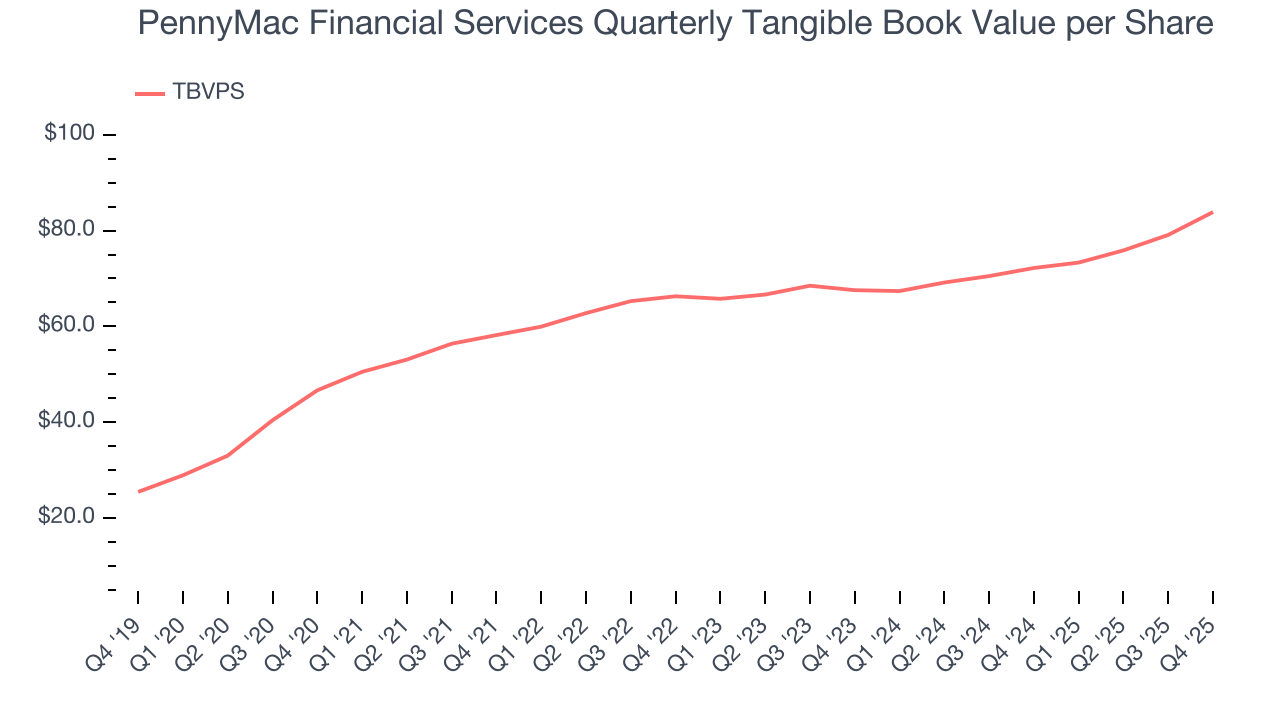

7. Tangible Book Value Per Share (TBVPS)

The balance sheet drives banking profitability since earnings flow from the spread between borrowing and lending rates. As such, valuations for these companies concentrate on capital strength and sustainable equity accumulation potential.

When analyzing banks, tangible book value per share (TBVPS) takes precedence over many other metrics. This measure isolates genuine per-share value by removing intangible assets of debatable liquidation worth. Traditional metrics like EPS are helpful but face distortion from M&A activity and loan loss accounting rules.

PennyMac Financial Services’s TBVPS grew at an incredible 12.4% annual clip over the last five years. TBVPS growth has recently decelerated a bit to 11.4% annual growth over the last two years (from $67.56 to $83.87 per share).

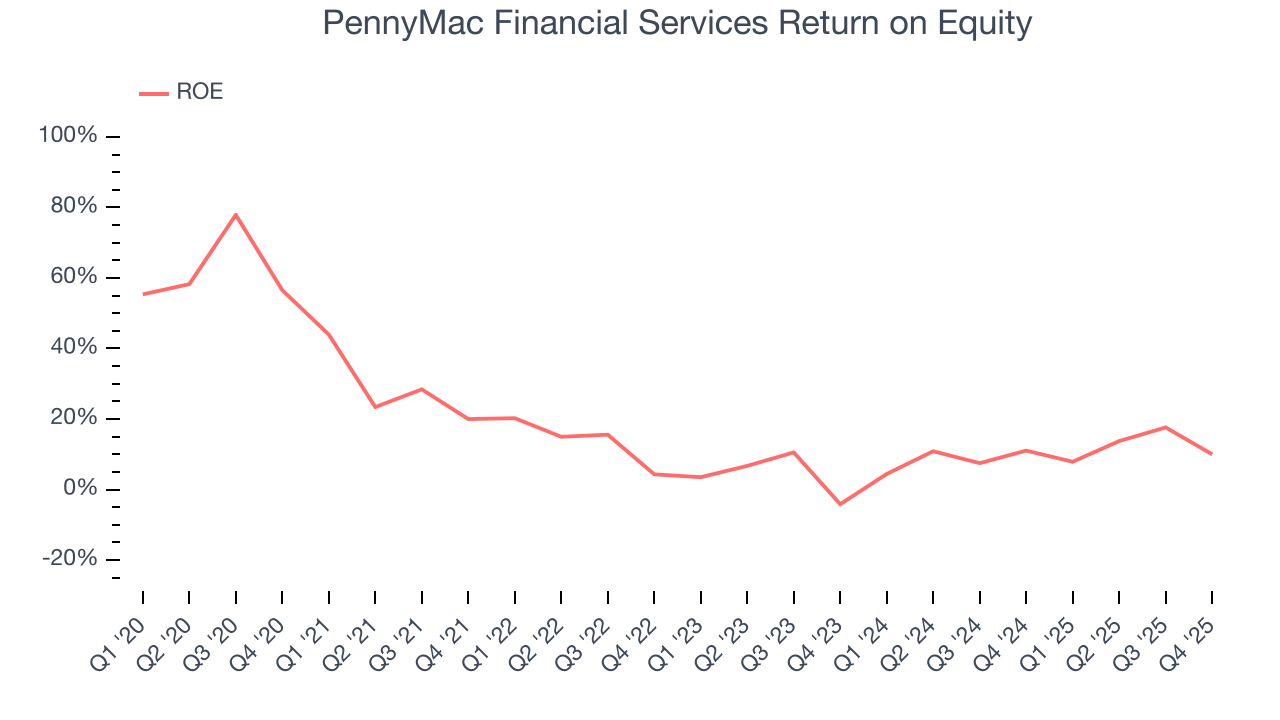

8. Return on Equity

Return on equity (ROE) reveals the profit generated per dollar of shareholder equity, which represents a key source of bank funding. Banks maintaining elevated ROE levels tend to accelerate wealth creation for shareholders via earnings retention, buybacks, and distributions.

Over the last five years, PennyMac Financial Services has averaged an ROE of 13.5%, healthy for a company operating in a sector where the average shakes out around 7.5% and those putting up 15%+ are greatly admired. This is a bright spot for PennyMac Financial Services.

9. Key Takeaways from PennyMac Financial Services’s Q4 Results

We struggled to find many positives in these results. Its revenue missed and its EPS fell short of Wall Street’s estimates, and these shortfalls were huge. Overall, this was a softer quarter. The stock traded down 22.5% to $116 immediately after reporting.

10. Is Now The Time To Buy PennyMac Financial Services?

Updated: March 19, 2026 at 1:04 AM EDT

Before investing in or passing on PennyMac Financial Services, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

PennyMac Financial Services isn’t a terrible business, but it doesn’t pass our quality test. For starters, its revenue has declined over the last five years. While its estimated net interest income growth for the next 12 months is great, the downside is its projected EPS for the next year is lacking. On top of that, its declining EPS over the last five years makes it a less attractive asset to the public markets.

PennyMac Financial Services’s P/B ratio based on the next 12 months is 0.9x. This valuation multiple is fair, but we don’t have much faith in the company. We're pretty confident there are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $137.17 on the company (compared to the current share price of $87.25).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.