PennyMac Mortgage Investment Trust (PMT)

PennyMac Mortgage Investment Trust is in for a bumpy ride. Its low returns on capital and plummeting sales suggest it struggles to generate demand and profits, a red flag.― StockStory Analyst Team

1. News

2. Summary

Why We Think PennyMac Mortgage Investment Trust Will Underperform

Operating as a real estate investment trust since 2009 to maintain tax advantages, PennyMac Mortgage Investment Trust (NYSE:PMT) is a specialty finance company that invests in mortgage-related assets and operates a correspondent lending business.

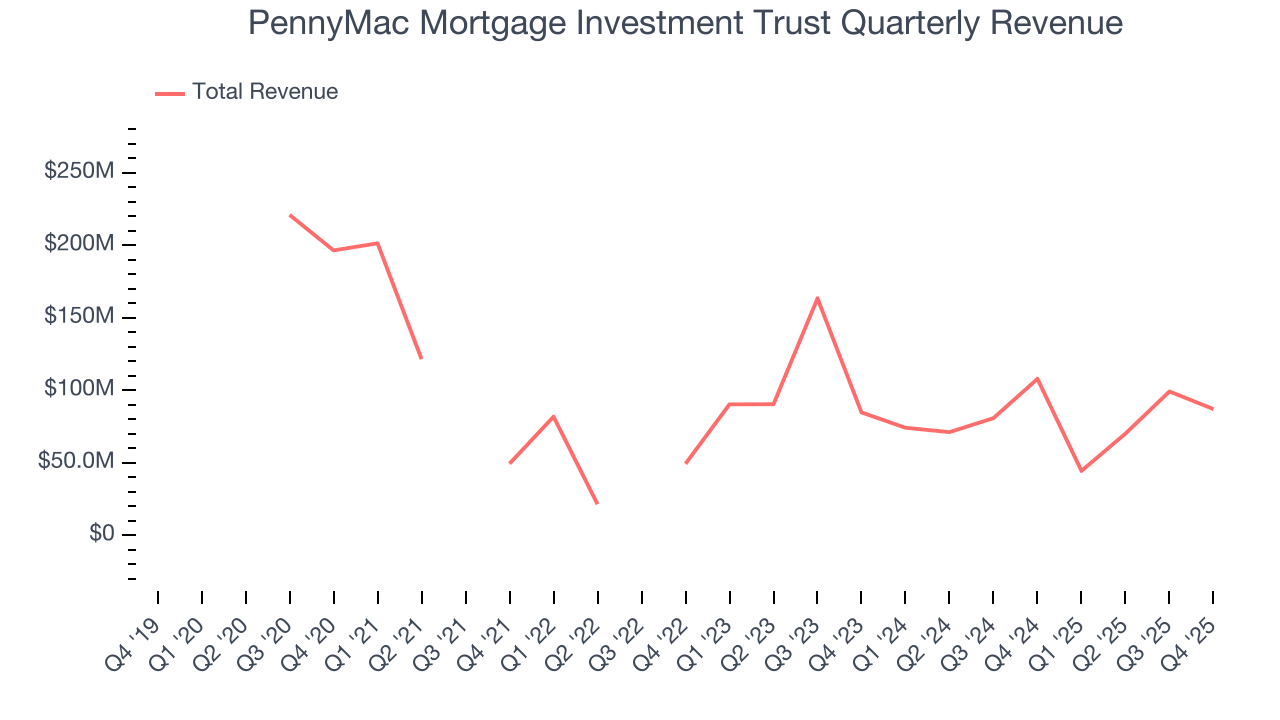

- Sales tumbled by 23.1% annually over the last five years, showing market trends are working against its favor during this cycle

- Sales were less profitable over the last two years as its earnings per share fell by 22% annually, worse than its revenue declines

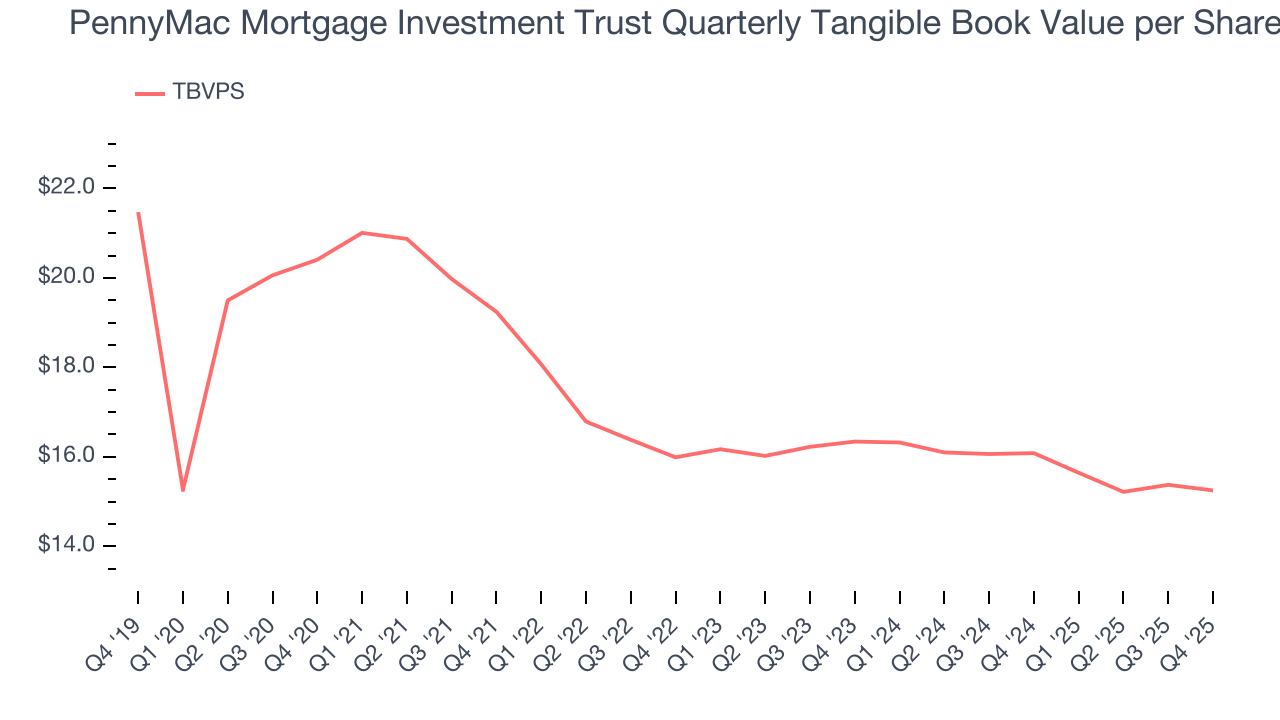

- Loan losses and capital returns have eroded its tangible book value per share this cycle as its tangible book value per share declined by 5.4% annually over the last five years

PennyMac Mortgage Investment Trust falls below our quality standards. We believe there are better opportunities elsewhere.

Why There Are Better Opportunities Than PennyMac Mortgage Investment Trust

At $11.76 per share, PennyMac Mortgage Investment Trust trades at 0.8x forward P/B. This certainly seems like a cheap stock, but we think there are valid reasons why it trades this way.

Our advice is to pay up for elite businesses whose advantages are tailwinds to earnings growth. Don’t get sucked into lower-quality businesses just because they seem like bargains. These mediocre businesses often never achieve a higher multiple as hoped, a phenomenon known as a “value trap”.

3. PennyMac Mortgage Investment Trust (PMT) Research Report: Q4 CY2025 Update

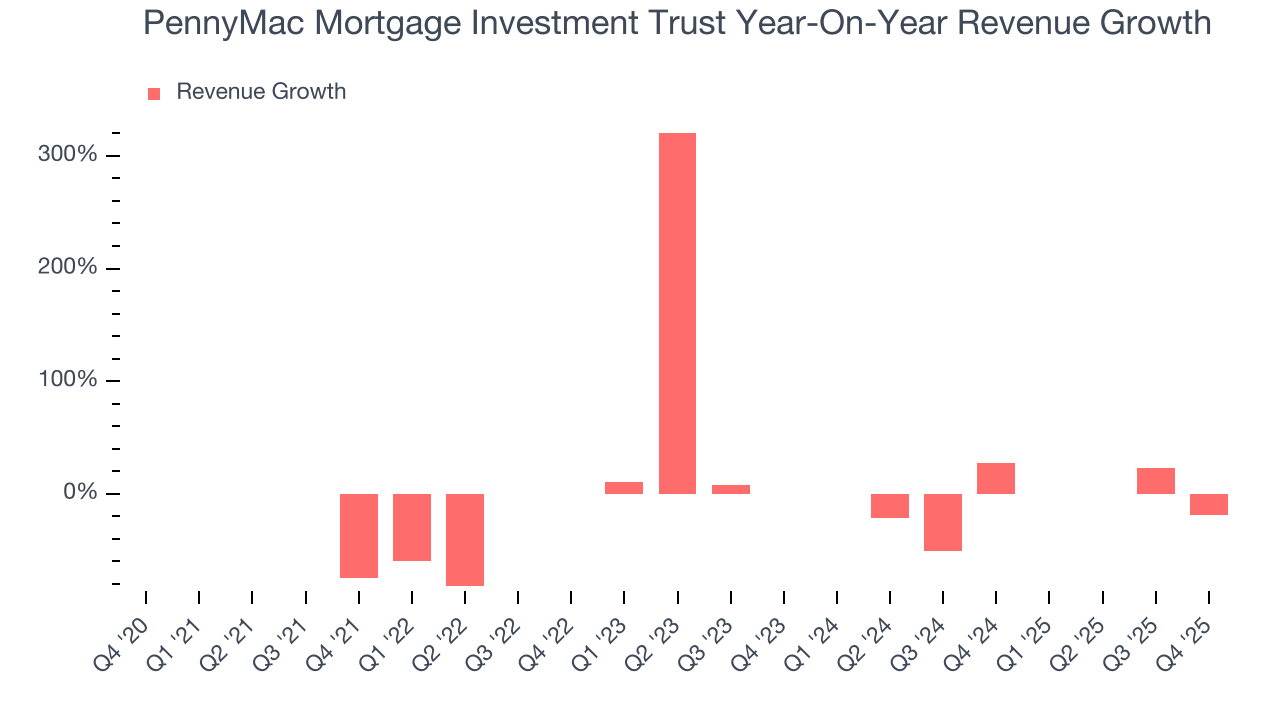

Mortgage REIT PennyMac Mortgage Investment Trust (NYSE:PMT) missed Wall Street’s revenue expectations in Q4 CY2025, with sales falling 19.3% year on year to $87.1 million. Its GAAP profit of $0.48 per share was 20.7% above analysts’ consensus estimates.

PennyMac Mortgage Investment Trust (PMT) Q4 CY2025 Highlights:

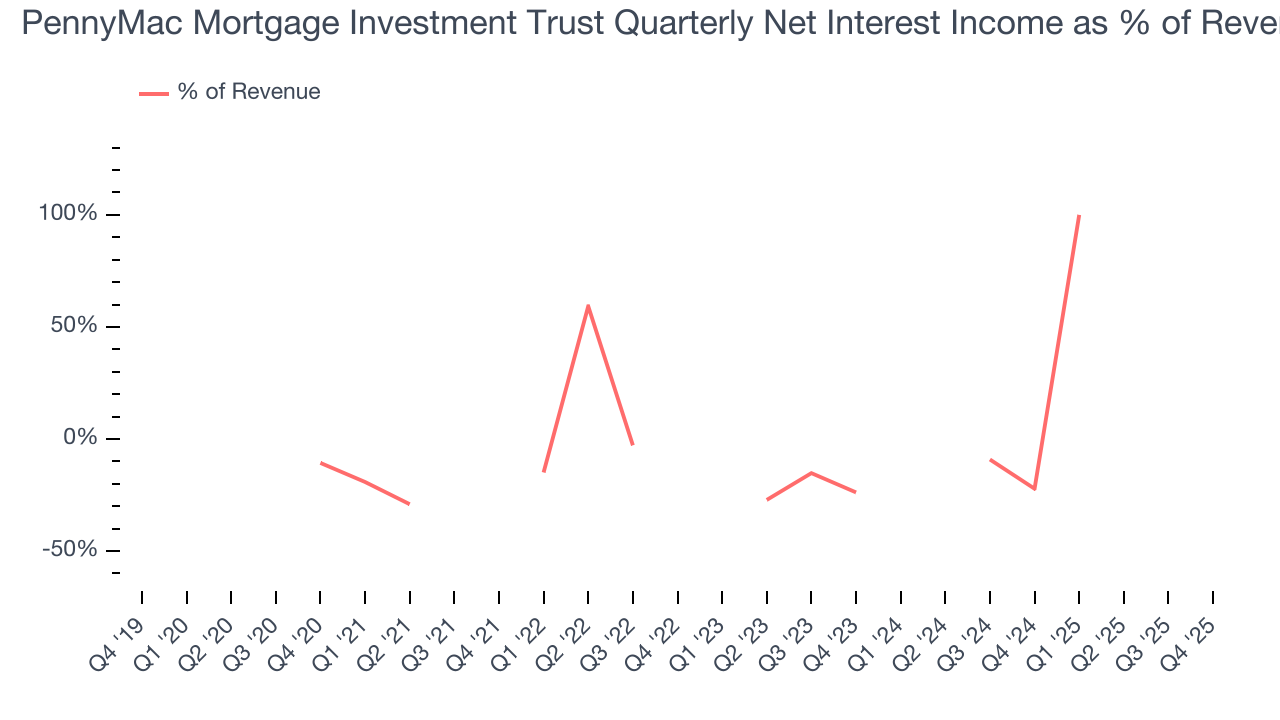

- Net Interest Income: -$6.46 million vs analyst estimates of -$5.85 million

- Revenue: $87.1 million vs analyst estimates of $99.85 million (19.3% year-on-year decline, 12.8% miss)

- Efficiency Ratio: 66% (1,703.3 basis point year-on-year decrease)

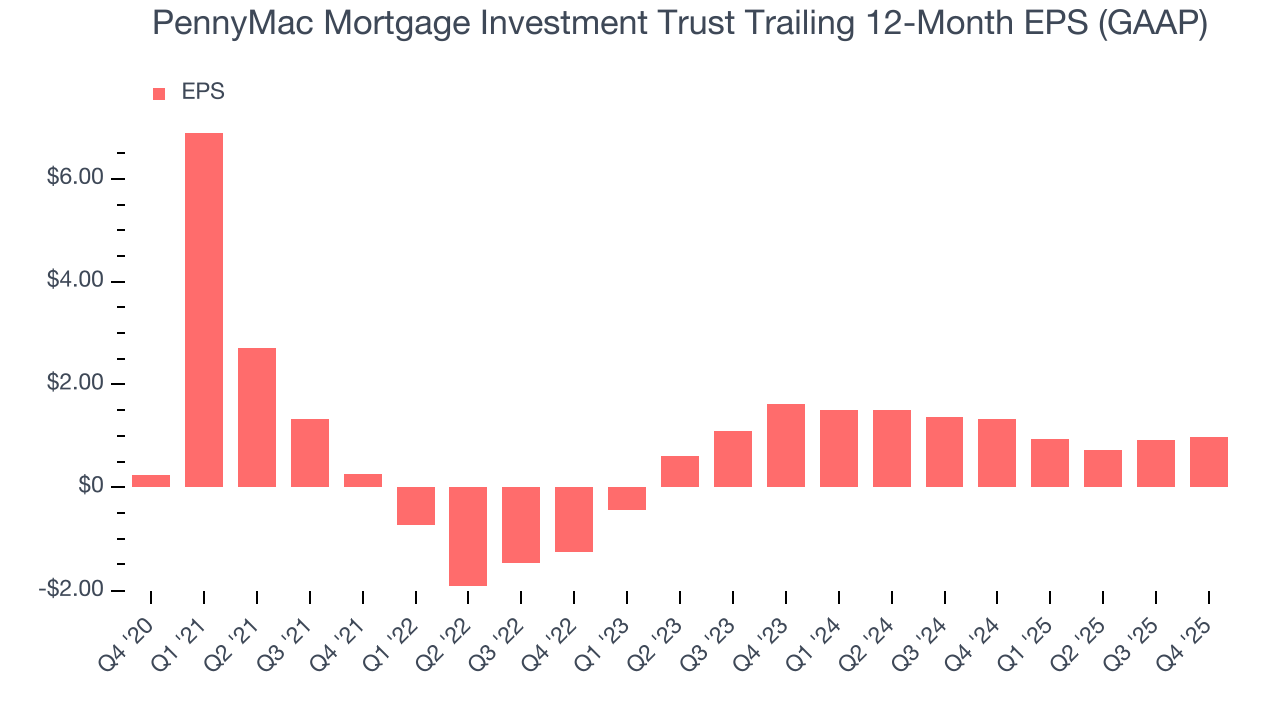

- EPS (GAAP): $0.48 vs analyst estimates of $0.40 (20.7% beat)

- Tangible Book Value per Share: $15.25 vs analyst estimates of $15.15 (5.2% year-on-year decline, 0.7% beat)

- Market Capitalization: $1.17 billion

Company Overview

Operating as a real estate investment trust since 2009 to maintain tax advantages, PennyMac Mortgage Investment Trust (NYSE:PMT) is a specialty finance company that invests in mortgage-related assets and operates a correspondent lending business.

PMT's business model revolves around three main segments. Through its Correspondent Production segment, the company acts as an intermediary between smaller mortgage lenders and the capital markets, purchasing newly originated prime-quality loans and then selling them to government-sponsored entities like Fannie Mae and Freddie Mac or into Ginnie Mae securitizations. This activity generates fee income and creates investment opportunities in mortgage servicing rights (MSRs).

The Interest Rate Sensitive Strategies segment manages investments in MSRs, agency mortgage-backed securities (MBS), and related interest rate hedging activities. MSRs represent the right to collect payments for servicing mortgage loans, generating income streams that typically increase when interest rates rise.

The Credit Sensitive Strategies segment focuses on investments that carry credit risk, including credit risk transfer (CRT) arrangements, subordinate mortgage-backed securities, and distressed loans. CRT investments allow PMT to assume some of the credit risk from government-sponsored entities in exchange for potential returns.

PMT is externally managed by PNMAC Capital Management, a subsidiary of PennyMac Financial Services, Inc. (NYSE:PFSI), which handles investment decisions. Another PFSI subsidiary, PennyMac Loan Services, performs loan production and servicing activities on PMT's behalf. This relationship with PFSI provides operational expertise but creates potential conflicts of interest due to the fee structure.

As a REIT, PMT must distribute at least 90% of its taxable income to shareholders annually to maintain its tax-advantaged status. This structure appeals to income-focused investors seeking dividend yields that often exceed those of traditional stocks.

4. Thrifts & Mortgage Finance

Thrifts & Mortgage Finance institutions operate by accepting deposits and extending loans primarily for residential mortgages, earning revenue through interest rate spreads (difference between lending rates and borrowing costs) and origination fees. The industry benefits from demographic tailwinds as millennials enter prime homebuying age, technological advancements streamlining the loan approval process, and potential interest rate stabilization improving affordability. However, significant headwinds include net interest margin compression during rate volatility, increased competition from fintech disruptors offering digital-first experiences, mounting regulatory compliance costs, and potential housing market corrections that could impact loan portfolios and default rates.

PMT competes with other mortgage REITs including Chimera Investment Corporation (NYSE:CIM), Invesco Mortgage Capital (NYSE:IVR), Rithm Capital (NYSE:RITM), MFA Financial (NYSE:MFA), New York Mortgage Trust (NASDAQ:NYMT), Redwood Trust (NYSE:RWT), and Two Harbors Investment (NYSE:TWO).

5. Sales Growth

Two primary revenue streams drive bank earnings. While net interest income, which is earned by charging higher rates on loans than paid on deposits, forms the foundation, fee-based services across banking, credit, wealth management, and trading operations provide additional income. PennyMac Mortgage Investment Trust struggled to consistently generate demand over the last five years as its revenue dropped at a 23.4% annual rate. This was below our standards and suggests it’s a low quality business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. PennyMac Mortgage Investment Trust’s annualized revenue declines of 16.2% over the last two years suggest its demand continued shrinking.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, PennyMac Mortgage Investment Trust missed Wall Street’s estimates and reported a rather uninspiring 19.3% year-on-year revenue decline, generating $87.1 million of revenue.

Net interest income made up -1.1% of the company’s total revenue during the last five years, meaning PennyMac Mortgage Investment Trust is well diversified and has a variety of income streams driving its overall growth. Nevertheless, net interest income is critical to analyze for banks because they’re considered a higher-quality, more recurring revenue source by investors.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.6. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

PennyMac Mortgage Investment Trust’s EPS grew at an astounding 32.5% compounded annual growth rate over the last five years, higher than its 23.4% annualized revenue declines. However, this alone doesn’t tell us much about its business quality because its efficiency ratio didn’t improve.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For PennyMac Mortgage Investment Trust, its two-year annual EPS declines of 22% mark a reversal from its (seemingly) healthy five-year trend. We hope PennyMac Mortgage Investment Trust can return to earnings growth in the future.

In Q4, PennyMac Mortgage Investment Trust reported EPS of $0.48, up from $0.41 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects PennyMac Mortgage Investment Trust’s full-year EPS of $0.98 to grow 68.6%.

7. Tangible Book Value Per Share (TBVPS)

Banks profit by intermediating between depositors and borrowers, making them fundamentally balance sheet-driven enterprises. Market participants emphasize balance sheet quality and sustained book value growth when evaluating these institutions.

This is why we consider tangible book value per share (TBVPS) the most important metric to track for banks. TBVPS represents the real, liquid net worth per share of a bank, excluding intangible assets that have debatable value upon liquidation. Traditional metrics like EPS are helpful but face distortion from M&A activity and loan loss accounting rules.

PennyMac Mortgage Investment Trust’s TBVPS declined at a 5.7% annual clip over the last five years. On a two-year basis, TBVPS fell at a slower pace, dropping by 3.4% annually from $16.34 to $15.25 per share.

Over the next 12 months, Consensus estimates call for PennyMac Mortgage Investment Trust’s TBVPS to remain flat at roughly $15.16, a disappointing projection.

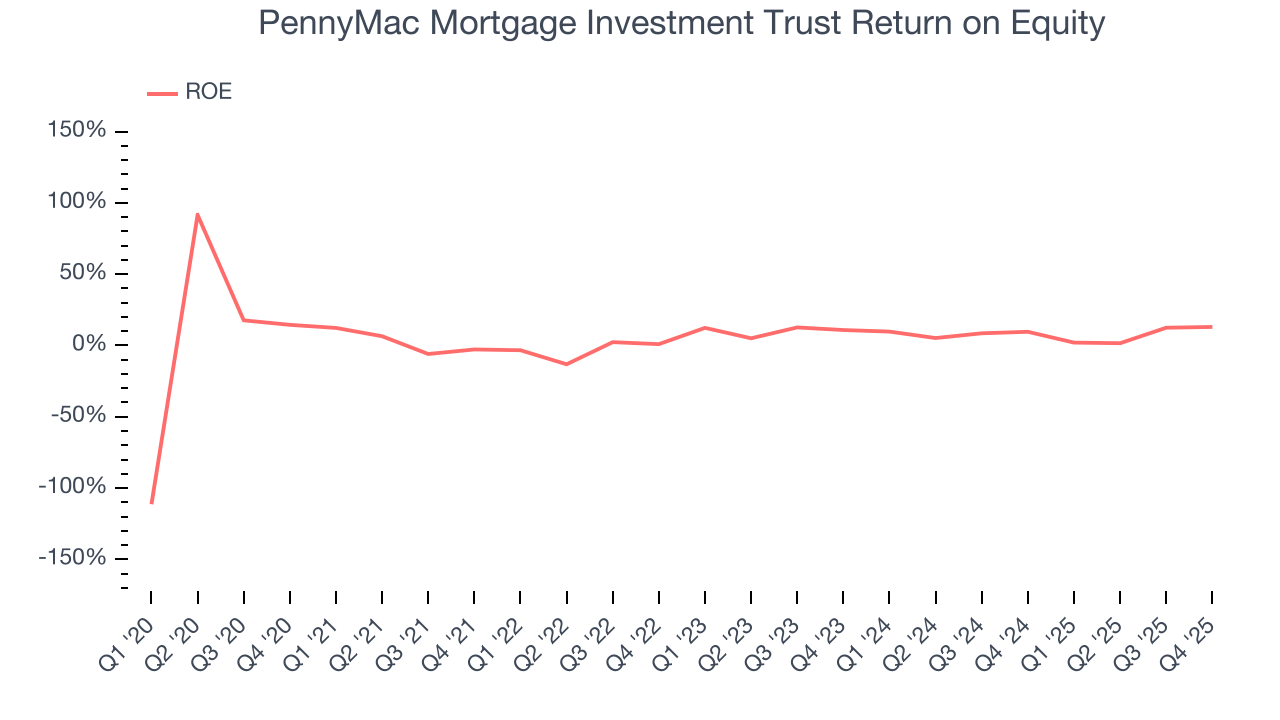

8. Return on Equity

Return on equity (ROE) reveals the profit generated per dollar of shareholder equity, which represents a key source of bank funding. Banks maintaining elevated ROE levels tend to accelerate wealth creation for shareholders via earnings retention, buybacks, and distributions.

Over the last five years, PennyMac Mortgage Investment Trust has averaged an ROE of 5%, uninspiring for a company operating in a sector where the average shakes out around 7.5%.

9. Key Takeaways from PennyMac Mortgage Investment Trust’s Q4 Results

It was good to see PennyMac Mortgage Investment Trust beat analysts’ EPS expectations this quarter. We were also happy its tangible book value per share narrowly outperformed Wall Street’s estimates. On the other hand, its revenue missed and its net interest income fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 1.1% to $13.36 immediately after reporting.

10. Is Now The Time To Buy PennyMac Mortgage Investment Trust?

Updated: March 14, 2026 at 12:46 AM EDT

Before investing in or passing on PennyMac Mortgage Investment Trust, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

PennyMac Mortgage Investment Trust doesn’t pass our quality test. To kick things off, its revenue has declined over the last five years. While its net interest income growth was exceptional over the last five years, the downside is its estimated sales for the next 12 months are weak. On top of that, its TBVPS has declined over the last five years.

PennyMac Mortgage Investment Trust’s P/B ratio based on the next 12 months is 0.8x. While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $13.36 on the company (compared to the current share price of $11.76).