Arbor Realty Trust (ABR)

Arbor Realty Trust is up against the odds. Its revenue and earnings have underwhelmed, suggesting weak business fundamentals.― StockStory Analyst Team

1. News

2. Summary

Why We Think Arbor Realty Trust Will Underperform

With roots dating back to 2003 and a focus on the stability of multifamily housing, Arbor Realty Trust (NYSE:ABR) is a specialized lender that provides financing solutions for multifamily and commercial real estate while also originating and servicing government-backed mortgage loans.

- Customers postponed purchases of its products and services this cycle as its revenue declined by 15.9% annually over the last two years

- Performance over the past two years shows each sale was less profitable as its earnings per share dropped by 31% annually, worse than its revenue

- Loan losses and capital returns have eroded its tangible book value per share this cycle as its tangible book value per share declined by 5.1% annually over the last two years

Arbor Realty Trust doesn’t meet our quality criteria. There are better opportunities in the market.

Why There Are Better Opportunities Than Arbor Realty Trust

Arbor Realty Trust is trading at $7.68 per share, or 0.7x forward P/B. Arbor Realty Trust’s valuation may seem like a great deal, but we think there are valid reasons why it’s so cheap.

Our advice is to pay up for elite businesses whose advantages are tailwinds to earnings growth. Don’t get sucked into lower-quality businesses just because they seem like bargains. These mediocre businesses often never achieve a higher multiple as hoped, a phenomenon known as a “value trap”.

3. Arbor Realty Trust (ABR) Research Report: Q4 CY2025 Update

Real estate investment trust Arbor Realty Trust (NYSE:ABR) reported Q4 CY2025 results topping the market’s revenue expectations, but sales fell by 12.1% year on year to $133.4 million. Its GAAP profit of $0.07 per share was 49.7% below analysts’ consensus estimates.

Arbor Realty Trust (ABR) Q4 CY2025 Highlights:

- Net Interest Income: $55.74 million vs analyst estimates of $53.93 million (32.7% year-on-year decline, 3.4% beat)

- Revenue: $133.4 million vs analyst estimates of $120.9 million (12.1% year-on-year decline, 10.3% beat)

- EPS (GAAP): $0.07 vs analyst expectations of $0.14 (49.7% miss)

- Market Capitalization: $1.42 billion

Company Overview

With roots dating back to 2003 and a focus on the stability of multifamily housing, Arbor Realty Trust (NYSE:ABR) is a specialized lender that provides financing solutions for multifamily and commercial real estate while also originating and servicing government-backed mortgage loans.

Arbor operates through two complementary business segments. Its Structured Business provides short-term bridge loans, mezzanine financing, and preferred equity investments primarily for multifamily properties and single-family rental portfolios. These customized financing solutions typically help borrowers during transition periods—such as when acquiring undervalued properties that need improvements or when waiting for long-term conventional financing. A property developer might use Arbor's bridge loan to quickly purchase and renovate an apartment complex before refinancing with permanent financing.

The company's Agency Business serves as an intermediary between property investors and government-sponsored enterprises like Fannie Mae and Freddie Mac. As an approved lender in various government programs, Arbor originates, sells, and services multifamily mortgage loans across the United States, with a particular focus on smaller balance loans. After selling these loans to government agencies, Arbor typically retains the servicing rights, creating a stable, long-term revenue stream from servicing fees.

Arbor generates revenue through multiple channels: interest income on its loan portfolio, gains from originating and selling agency loans, and ongoing servicing fees. The company's business model is designed to produce consistent earnings through these diversified income streams. Arbor's nationwide presence, with offices across multiple states, allows it to source deals across diverse geographic markets, while its status as a REIT requires it to distribute at least 90% of its taxable income to shareholders annually.

4. Thrifts & Mortgage Finance

Thrifts & Mortgage Finance institutions operate by accepting deposits and extending loans primarily for residential mortgages, earning revenue through interest rate spreads (difference between lending rates and borrowing costs) and origination fees. The industry benefits from demographic tailwinds as millennials enter prime homebuying age, technological advancements streamlining the loan approval process, and potential interest rate stabilization improving affordability. However, significant headwinds include net interest margin compression during rate volatility, increased competition from fintech disruptors offering digital-first experiences, mounting regulatory compliance costs, and potential housing market corrections that could impact loan portfolios and default rates.

Arbor Realty Trust competes with other commercial mortgage REITs such as Blackstone Mortgage Trust (NYSE:BXMT), Starwood Property Trust (NYSE:STWD), and Ready Capital Corporation (NYSE:RC). In its Agency Business, Arbor faces competition from larger financial institutions like Walker & Dunlop (NYSE:WD) and CBRE Group (NYSE:CBRE).

5. Sales Growth

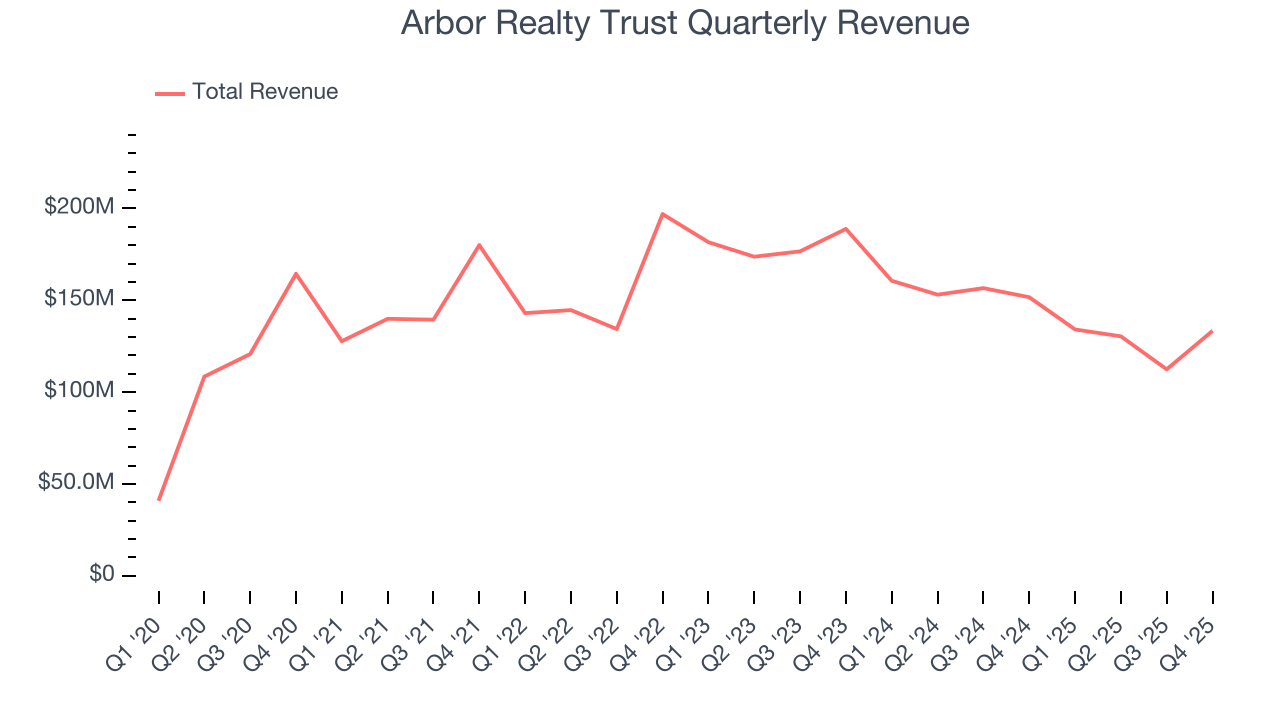

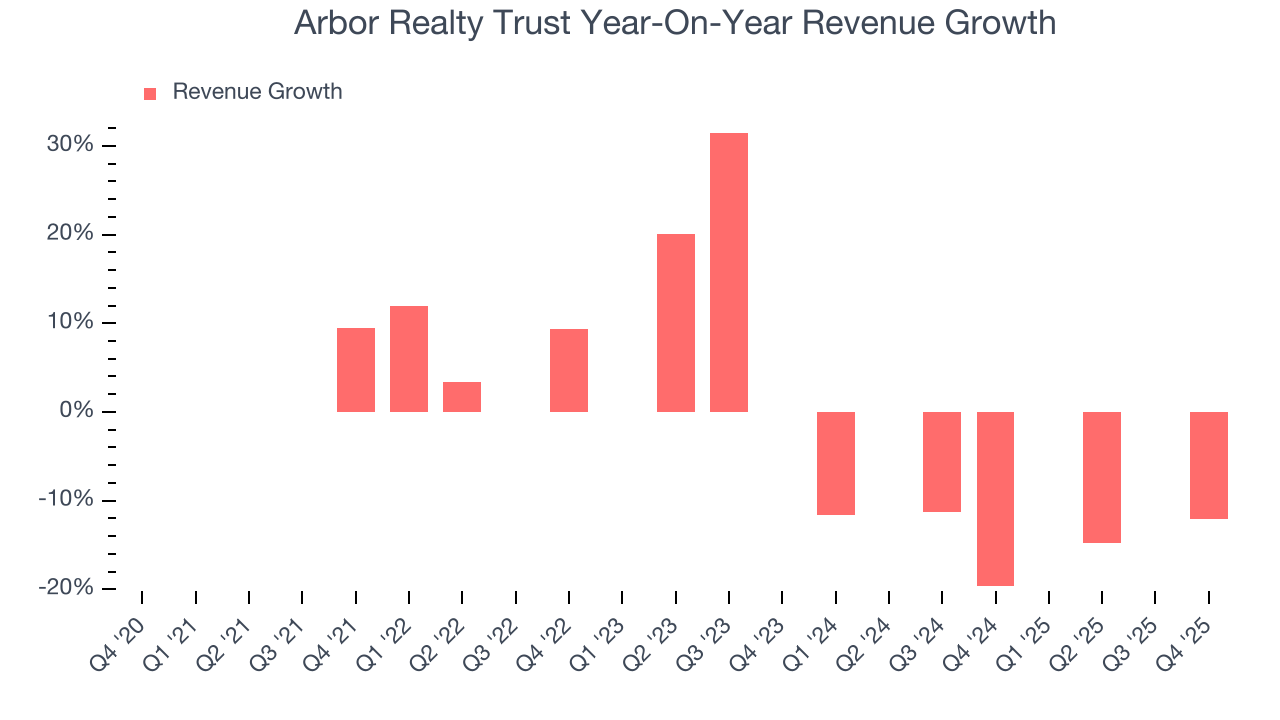

Two primary revenue streams drive bank earnings. While net interest income, which is earned by charging higher rates on loans than paid on deposits, forms the foundation, fee-based services across banking, credit, wealth management, and trading operations provide additional income. Over the last five years, Arbor Realty Trust grew its revenue at a sluggish 3.3% compounded annual growth rate. This fell short of our benchmark for the banking sector and is a poor baseline for our analysis.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Arbor Realty Trust’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 15.9% annually.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Arbor Realty Trust’s revenue fell by 12.1% year on year to $133.4 million but beat Wall Street’s estimates by 10.3%.

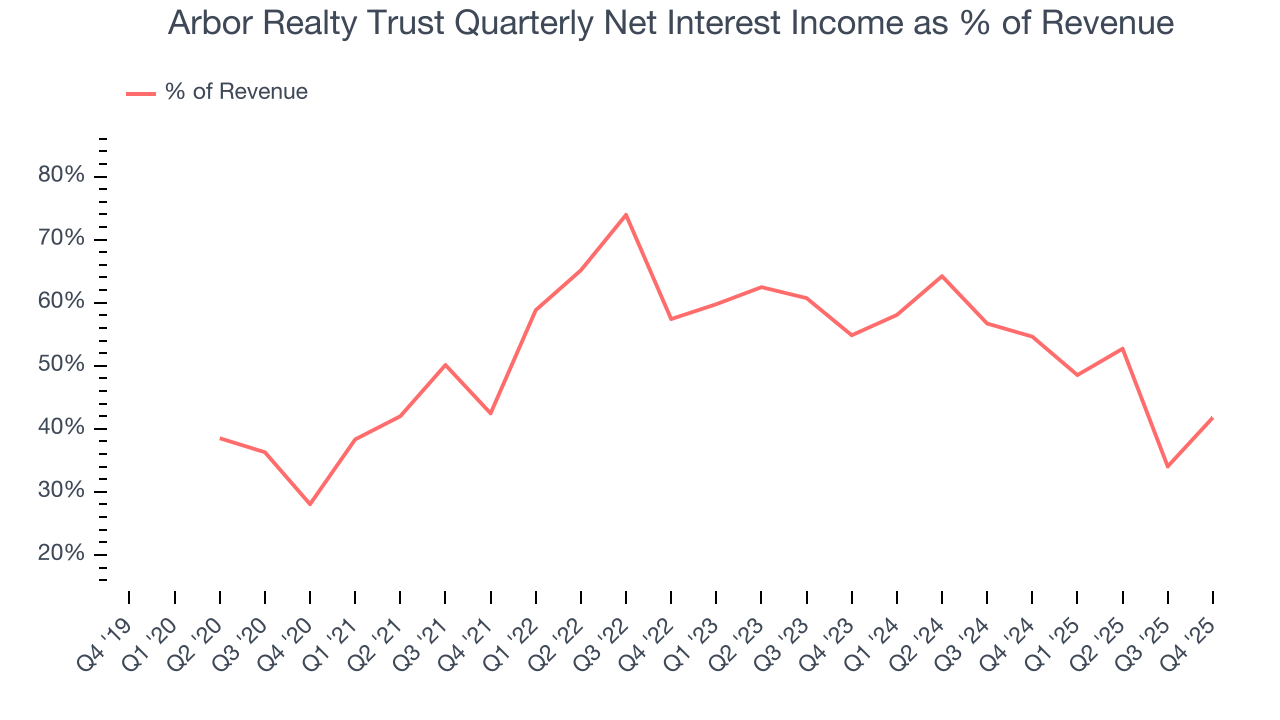

Net interest income made up 53.8% of the company’s total revenue during the last five years, meaning Arbor Realty Trust’s growth drivers strike a balance between lending and non-lending activities.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.Markets consistently prioritize net interest income growth over fee-based revenue, recognizing its superior quality and recurring nature compared to the more unpredictable non-interest income streams.

6. Earnings Per Share

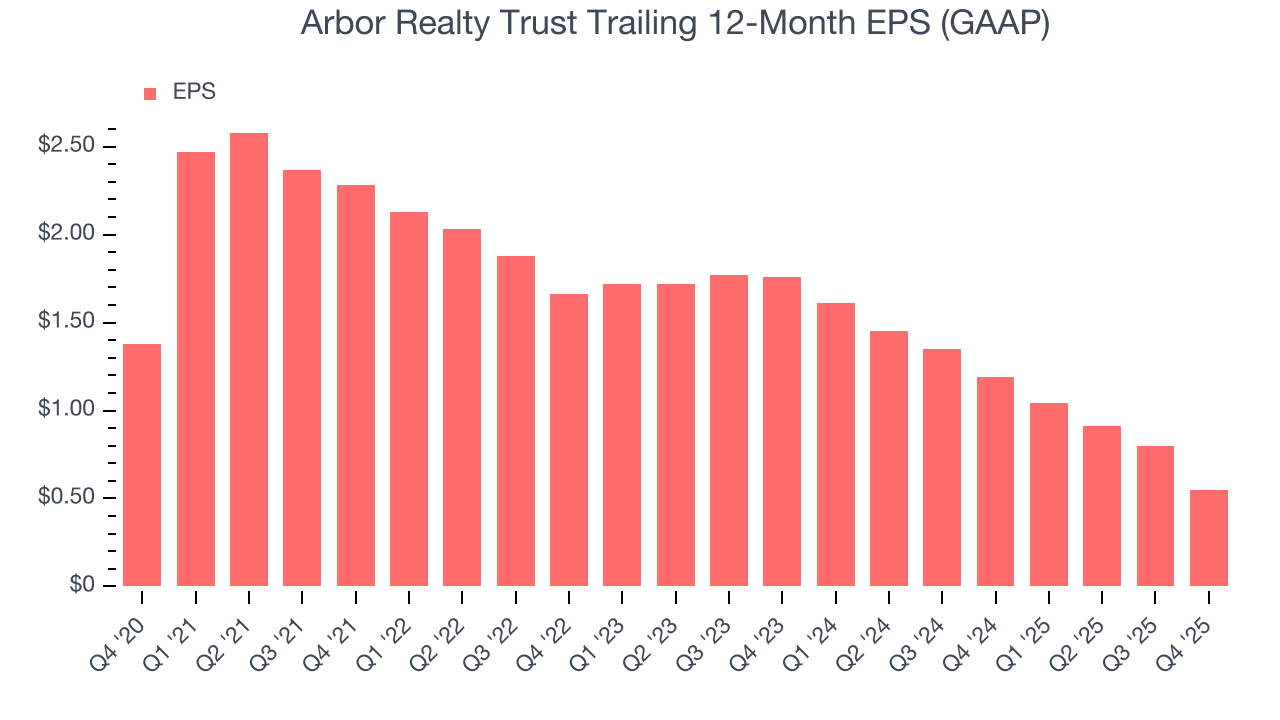

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Arbor Realty Trust, its EPS declined by 16.8% annually over the last five years while its revenue grew by 3.3%. This tells us the company became less profitable on a per-share basis as it expanded.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Arbor Realty Trust, its two-year annual EPS declines of 44.1% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q4, Arbor Realty Trust reported EPS of $0.07, down from $0.32 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Arbor Realty Trust’s full-year EPS of $0.55 to grow 29.5%.

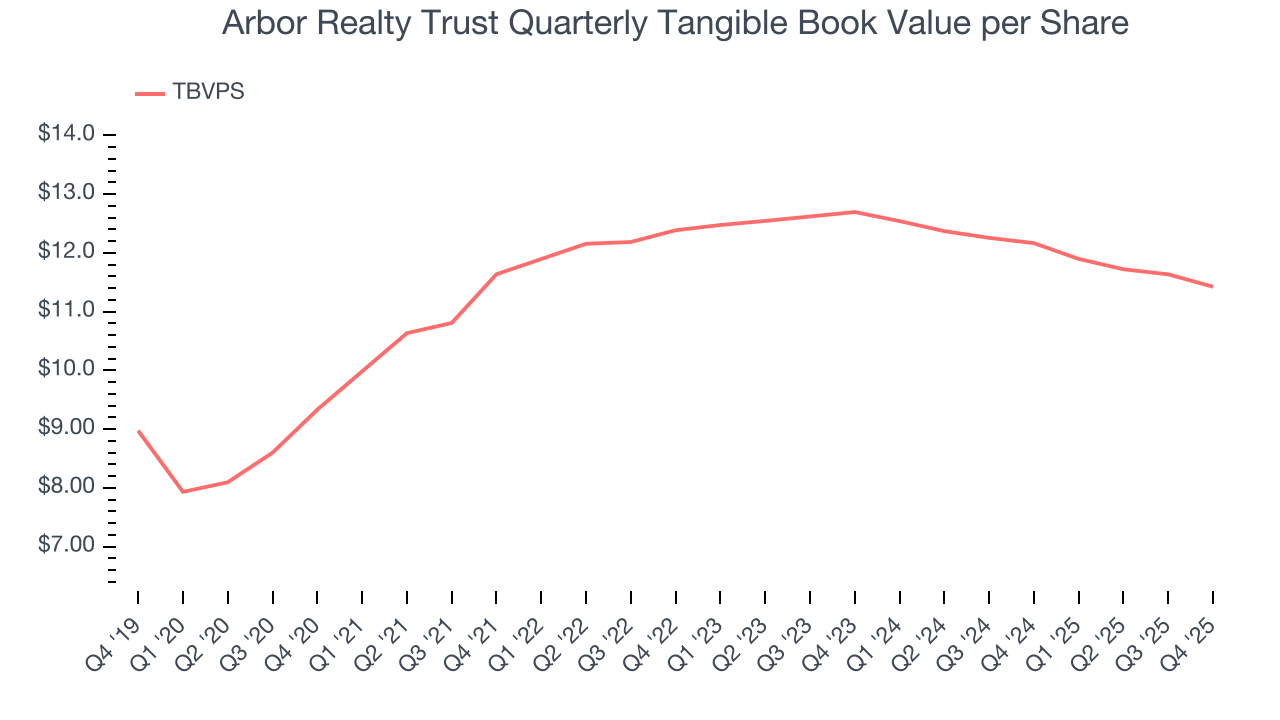

7. Tangible Book Value Per Share (TBVPS)

The balance sheet drives banking profitability since earnings flow from the spread between borrowing and lending rates. As such, valuations for these companies concentrate on capital strength and sustainable equity accumulation potential.

Because of this, tangible book value per share (TBVPS) emerges as the critical performance benchmark. By excluding intangible assets with uncertain liquidation values, this metric captures real, liquid net worth per share. Traditional metrics like EPS are helpful but face distortion from M&A activity and loan loss accounting rules.

Arbor Realty Trust’s TBVPS grew at a mediocre 4.1% annual clip over the last five years. On a two-year basis, however, dynamics have changed as TBVPS dropped by 5.1% annually ($12.69 to $11.42 per share).

Over the next 12 months, Consensus estimates call for Arbor Realty Trust’s TBVPS to shrink by 6.5% to $10.69, a sour projection.

8. Return on Equity

Return on equity, or ROE, tells us how much profit a company generates for each dollar of shareholder equity, a key funding source for banks. Over a long period, banks with high ROE tend to compound shareholder wealth faster through retained earnings, buybacks, and dividends.

Over the last five years, Arbor Realty Trust has averaged an ROE of 12.1%, healthy for a company operating in a sector where the average shakes out around 7.5% and those putting up 15%+ are greatly admired. This is a bright spot for Arbor Realty Trust.

9. Key Takeaways from Arbor Realty Trust’s Q4 Results

We were impressed by how significantly Arbor Realty Trust blew past analysts’ revenue expectations this quarter. We were also glad its net interest income outperformed Wall Street’s estimates. On the other hand, its EPS missed. Overall, this print was mixed. The stock remained flat at $7.27 immediately following the results.

10. Is Now The Time To Buy Arbor Realty Trust?

Updated: March 14, 2026 at 12:55 AM EDT

Before making an investment decision, investors should account for Arbor Realty Trust’s business fundamentals and valuation in addition to what happened in the latest quarter.

We see the value of companies driving economic growth, but in the case of Arbor Realty Trust, we’re out. First off, its revenue growth was weak over the last five years, and analysts expect its demand to deteriorate over the next 12 months. While its above-average ROE suggests its management team has made good investment decisions, the downside is its estimated sales for the next 12 months are weak. On top of that, its projected EPS for the next year is lacking.

Arbor Realty Trust’s P/B ratio based on the next 12 months is 0.7x. While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $8.88 on the company (compared to the current share price of $7.68).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.