PennyMac Financial Services (PFSI)

PennyMac Financial Services doesn’t impress us. Its declining sales show demand has evaporated, a red flag for investors seeking high-quality stocks.― StockStory Analyst Team

1. News

2. Summary

Why PennyMac Financial Services Is Not Exciting

Founded during the 2008 financial crisis to help address the mortgage market meltdown, PennyMac Financial Services (NYSE:PFSI) is a specialty financial services company that originates, services, and manages investments related to residential mortgage loans in the United States.

- Products and services are facing significant end-market challenges during this cycle as sales have declined by 6.9% annually over the last five years

- Falling earnings per share over the last five years has some investors worried as stock prices ultimately follow EPS over the long term

- On the plus side, its projected net interest income growth of 72.5% for the next 12 months is above its five-year trend, pointing to accelerating demand

PennyMac Financial Services’s quality doesn’t meet our bar. More profitable opportunities exist elsewhere.

Why There Are Better Opportunities Than PennyMac Financial Services

PennyMac Financial Services’s stock price of $150.83 implies a valuation ratio of 1.8x forward P/B. Not only is PennyMac Financial Services’s multiple richer than most banking peers, but it’s also expensive for its revenue characteristics.

There are stocks out there similarly priced with better business quality. We prefer owning these.

3. PennyMac Financial Services (PFSI) Research Report: Q3 CY2025 Update

Mortgage banking company PennyMac Financial Services (NYSE:PFSI) reported Q3 CY2025 results exceeding the market’s revenue expectations, with sales up 10.6% year on year to $632.9 million. Its GAAP profit of $3.37 per share was 14.6% above analysts’ consensus estimates.

PennyMac Financial Services (PFSI) Q3 CY2025 Highlights:

- Revenue: $632.9 million vs analyst estimates of $575.7 million (10.6% year-on-year growth, 9.9% beat)

- EPS (GAAP): $3.37 vs analyst estimates of $2.94 (14.6% beat)

- Market Capitalization: $6.28 billion

Company Overview

Founded during the 2008 financial crisis to help address the mortgage market meltdown, PennyMac Financial Services (NYSE:PFSI) is a specialty financial services company that originates, services, and manages investments related to residential mortgage loans in the United States.

PennyMac operates through three main business segments: Production, Servicing, and Investment Management. The Production segment sources new mortgage loans through correspondent production (purchasing loans from other lenders), consumer direct lending (originating loans directly with borrowers online and via call centers), and broker direct lending (working with mortgage brokers).

In its correspondent channel, PennyMac purchases loans that meet specific investor guidelines, particularly those insured or guaranteed by government agencies like FHA, VA, and USDA. These loans are typically pooled into mortgage-backed securities guaranteed by Ginnie Mae and sold to institutional investors. The company earns revenue through loan origination fees, interest income during the holding period, gains on sales, and by retaining the mortgage servicing rights.

The Servicing segment handles loan administration activities including collecting payments, managing escrow accounts for taxes and insurance, assisting borrowers with inquiries, and managing delinquencies and foreclosures when necessary. PennyMac services loans both as the owner of mortgage servicing rights and as a subservicer for PennyMac Mortgage Investment Trust (PMT), a publicly traded mortgage REIT that the company manages.

Through its investment management subsidiary, PNMAC Capital Management, PennyMac earns management fees based on PMT's net assets and potential incentive compensation tied to investment performance. This relationship creates a symbiotic business model where PennyMac Financial Services provides operational expertise while PMT supplies investment capital for mortgage-related assets.

4. Thrifts & Mortgage Finance

Thrifts & Mortgage Finance institutions operate by accepting deposits and extending loans primarily for residential mortgages, earning revenue through interest rate spreads (difference between lending rates and borrowing costs) and origination fees. The industry benefits from demographic tailwinds as millennials enter prime homebuying age, technological advancements streamlining the loan approval process, and potential interest rate stabilization improving affordability. However, significant headwinds include net interest margin compression during rate volatility, increased competition from fintech disruptors offering digital-first experiences, mounting regulatory compliance costs, and potential housing market corrections that could impact loan portfolios and default rates.

PennyMac Financial Services competes with large financial institutions and other independent mortgage producers and servicers, including Rocket Mortgage (NYSE:RKT), Mr. Cooper Group (NASDAQ:COOP), and United Wholesale Mortgage (NYSE:UWMC), as well as the cash windows of government-sponsored enterprises Fannie Mae and Freddie Mac.

5. Sales Growth

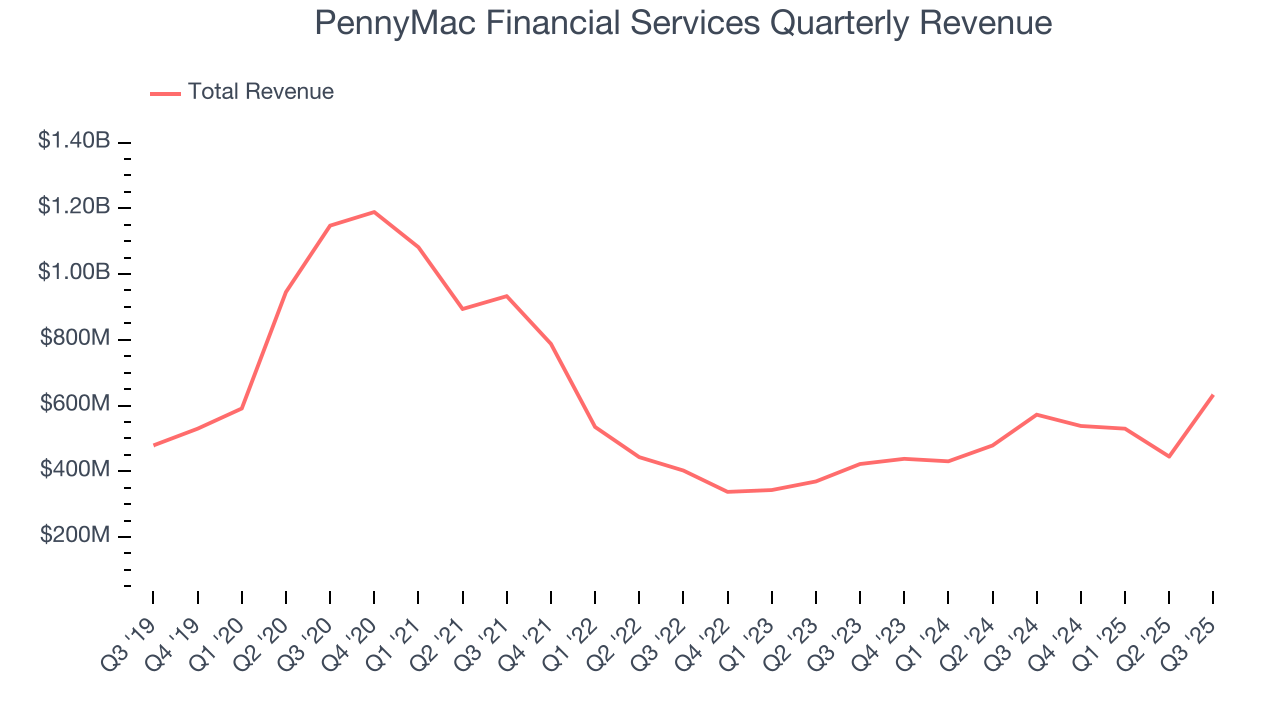

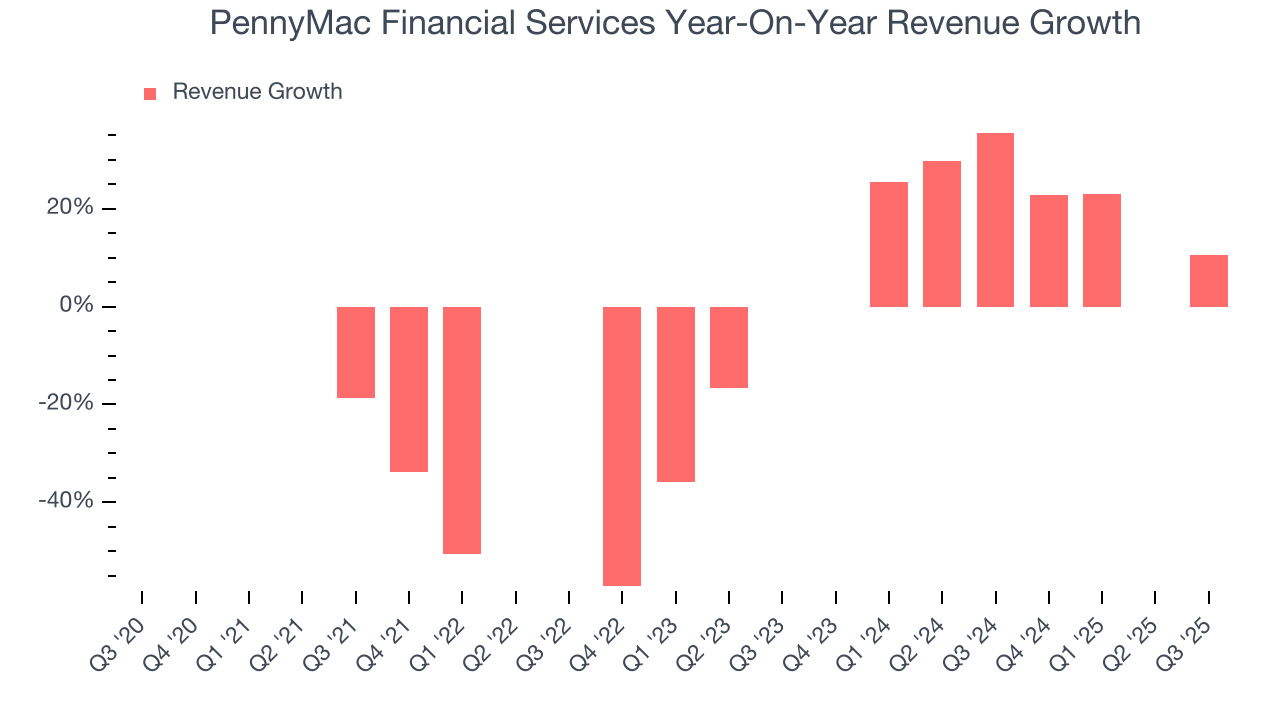

In general, banks make money from two primary sources. The first is net interest income, which is interest earned on loans, mortgages, and investments in securities minus interest paid out on deposits. The second source is non-interest income, which can come from bank account, credit card, wealth management, investing banking, and trading fees. PennyMac Financial Services’s demand was weak over the last five years as its revenue fell at a 7.8% annual rate. This wasn’t a great result, but there are still things to like about PennyMac Financial Services.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. PennyMac Financial Services’s annualized revenue growth of 20.7% over the last two years is above its five-year trend, suggesting its demand recently accelerated.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, PennyMac Financial Services reported year-on-year revenue growth of 10.6%, and its $632.9 million of revenue exceeded Wall Street’s estimates by 9.9%.

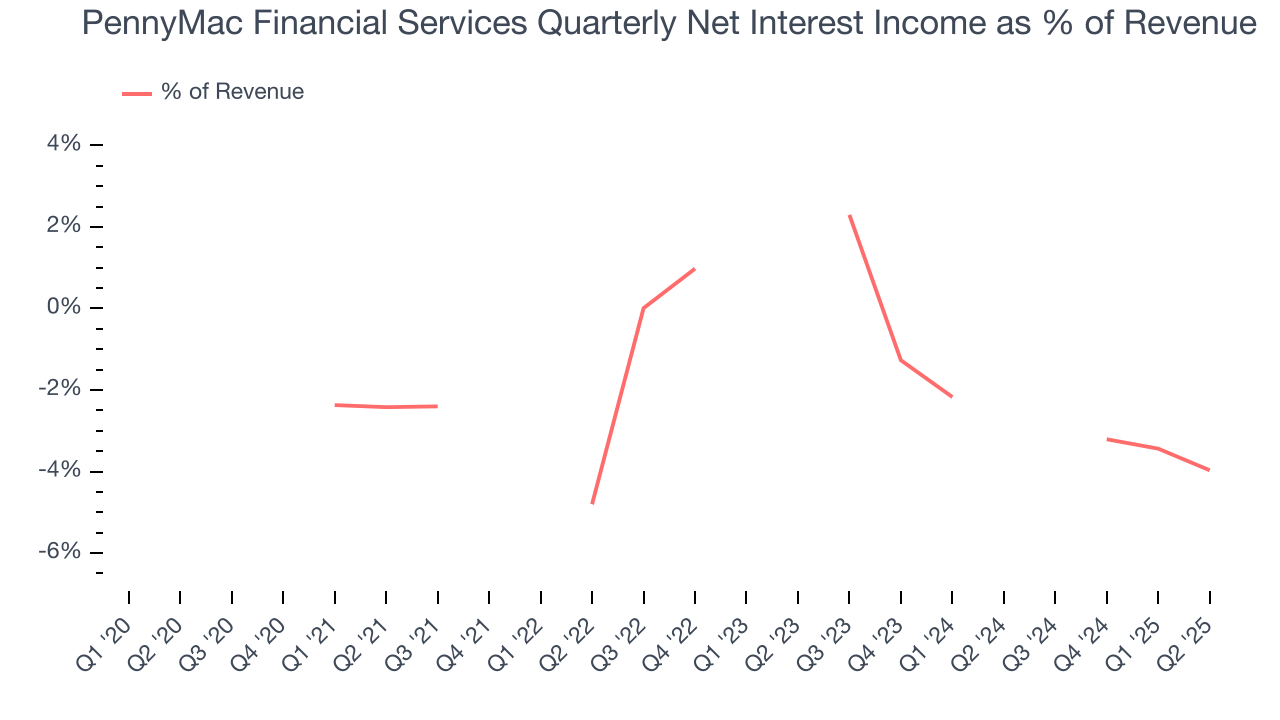

Net interest income made up -1.8% of the company’s total revenue during the last five years, meaning PennyMac Financial Services is well diversified and has a variety of income streams driving its overall growth. Nevertheless, net interest income is critical to analyze for banks because they’re considered a higher-quality, more recurring revenue source by investors.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.6. Earnings Per Share

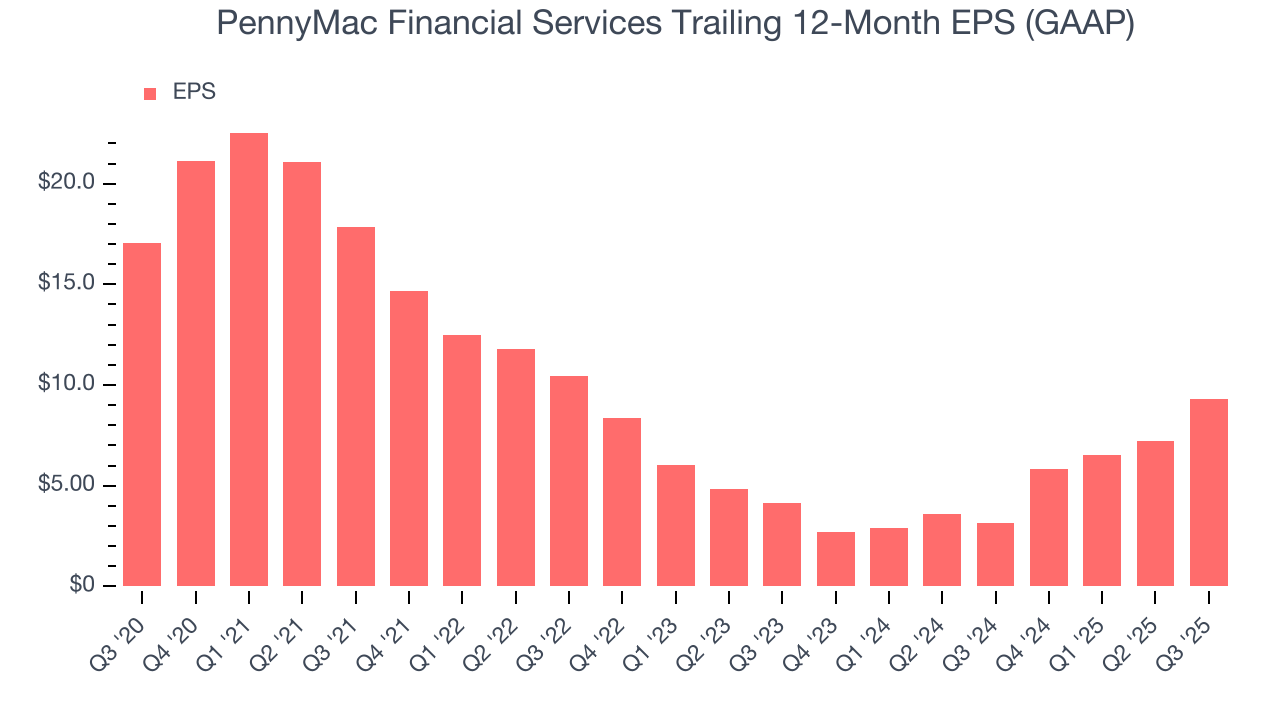

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for PennyMac Financial Services, its EPS declined by 11.4% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For PennyMac Financial Services, its two-year annual EPS growth of 49.4% was higher than its five-year trend. This acceleration made it one of the faster-growing banking companies in recent history.

In Q3, PennyMac Financial Services reported EPS of $3.37, up from $1.30 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects PennyMac Financial Services’s full-year EPS of $9.29 to grow 51.2%.

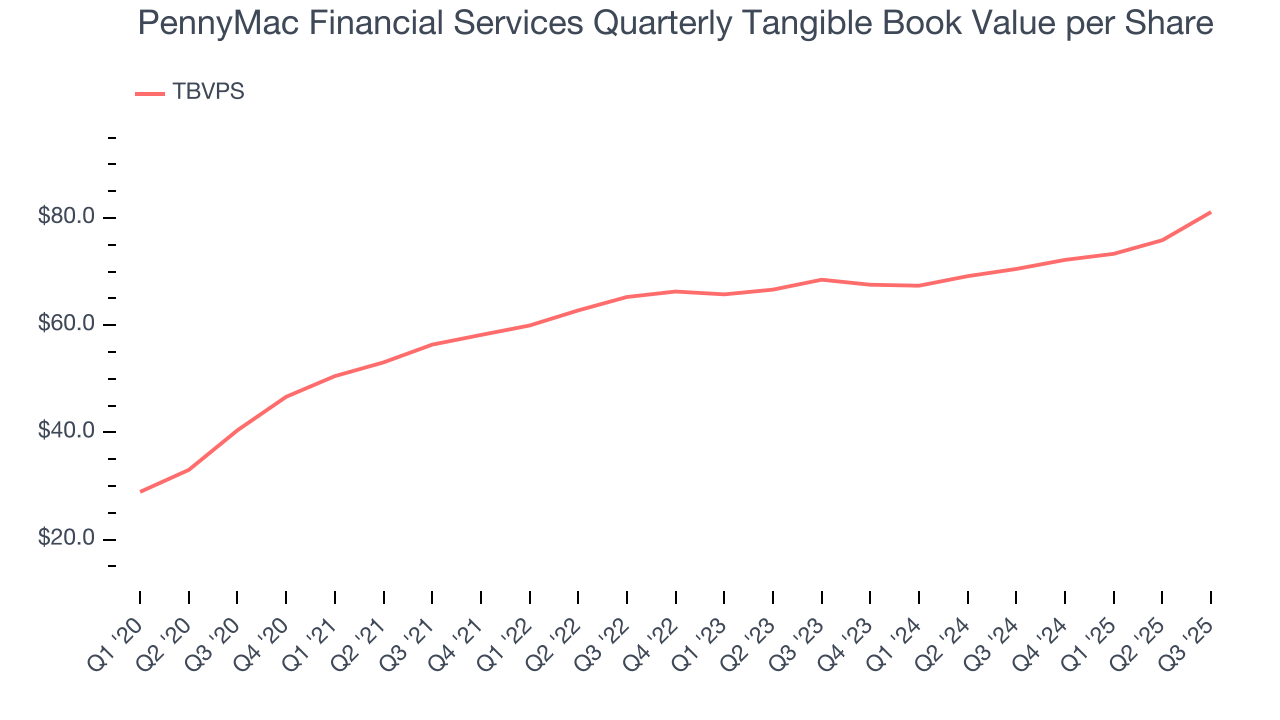

7. Tangible Book Value Per Share (TBVPS)

Banks profit by intermediating between depositors and borrowers, making them fundamentally balance sheet-driven enterprises. Market participants emphasize balance sheet quality and sustained book value growth when evaluating these institutions.

This explains why tangible book value per share (TBVPS) stands as the premier banking metric. TBVPS strips away questionable intangible assets, revealing concrete per-share net worth that investors can trust. Traditional metrics like EPS are helpful but face distortion from M&A activity and loan loss accounting rules.

PennyMac Financial Services’s TBVPS grew at an incredible 15% annual clip over the last five years. However, TBVPS growth has recently decelerated to 8.8% annual growth over the last two years (from $68.49 to $81.12 per share).

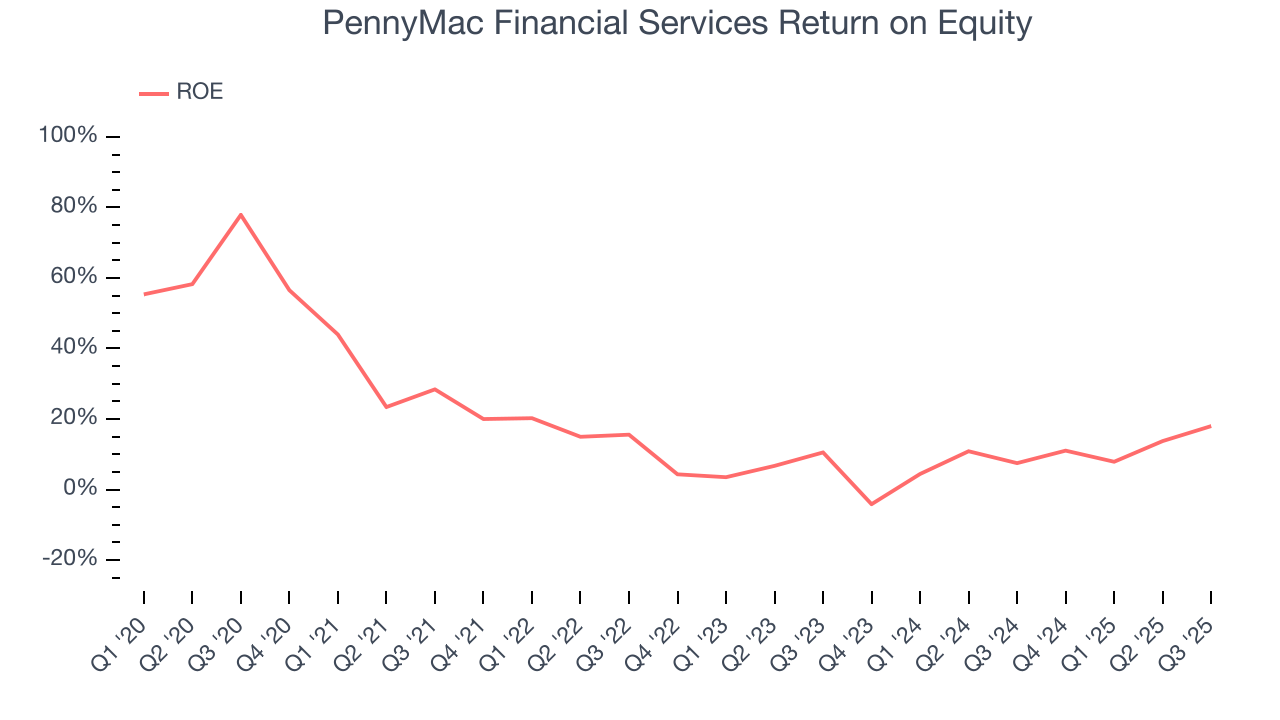

8. Return on Equity

Return on equity (ROE) reveals the profit generated per dollar of shareholder equity, which represents a key source of bank funding. Banks maintaining elevated ROE levels tend to accelerate wealth creation for shareholders via earnings retention, buybacks, and distributions.

Over the last five years, PennyMac Financial Services has averaged an ROE of 15.9%, exceptional for a company operating in a sector where the average shakes out around 7.5% and those putting up 15%+ are greatly admired. This shows PennyMac Financial Services has a strong competitive moat.

9. Key Takeaways from PennyMac Financial Services’s Q3 Results

We were impressed by how significantly PennyMac Financial Services blew past analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Zooming out, we think this was a good print with some key areas of upside. The stock remained flat at $120.96 immediately after reporting.

10. Is Now The Time To Buy PennyMac Financial Services?

Updated: January 24, 2026 at 11:46 PM EST

Are you wondering whether to buy PennyMac Financial Services or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

When it comes to PennyMac Financial Services’s business quality, there are some positives, but it ultimately falls short. Although its revenue has declined over the last five years, its growth over the next 12 months is expected to be higher. And while PennyMac Financial Services’s declining EPS over the last five years makes it a less attractive asset to the public markets, its estimated net interest income growth for the next 12 months is great.

PennyMac Financial Services’s P/B ratio based on the next 12 months is 1.8x. This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're fairly confident there are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $154.75 on the company (compared to the current share price of $150.83).