Primerica (PRI)

Primerica is intriguing. Its superb 27.7% ROE illustrates its skill in making high-return investments.― StockStory Analyst Team

1. News

2. Summary

Why Primerica Is Interesting

With a sales force of over 140,000 licensed representatives operating on an independent contractor model, Primerica (NYSE:PRI) provides term life insurance, investment products, and other financial services to middle-income households in the United States and Canada.

- Industry-leading 27.7% return on equity demonstrates management’s skill in finding high-return investments

- Pre-tax profit margin improvement of 6.8 percentage points over the last five years demonstrates its ability to scale efficiently

- On the flip side, its estimated book value per share growth of 7.5% for the next 12 months implies profitability will slow from its two-year trend

Primerica has some noteworthy aspects. This company is certainly worth watching.

Why Should You Watch Primerica

At $246.21 per share, Primerica trades at 3x forward P/B. The market certainly has elevated expectations given its relatively high multiple, which could cause short-term volatility if there is a hiccup in company performance or even that of its peers.

Primerica can improve its fundamentals over time by putting up good numbers quarter after quarter, year after year. Once that happens, we’ll be happy to recommend the stock.

3. Primerica (PRI) Research Report: Q4 CY2025 Update

Financial services company Primerica (NYSE:PRI) announced better-than-expected revenue in Q4 CY2025, with sales up 8% year on year to $853.7 million. Its non-GAAP profit of $6.13 per share was 8% above analysts’ consensus estimates.

Primerica (PRI) Q4 CY2025 Highlights:

- Net Premiums Earned: $445.9 million vs analyst estimates of $455.7 million (1.3% year-on-year growth, 2.2% miss)

- Revenue: $853.7 million vs analyst estimates of $846.8 million (8% year-on-year growth, 0.8% beat)

- Pre-tax Profit: $247.1 million (28.9% margin)

- Adjusted EPS: $6.13 vs analyst estimates of $5.68 (8% beat)

- Market Capitalization: $8.46 billion

Company Overview

With a sales force of over 140,000 licensed representatives operating on an independent contractor model, Primerica (NYSE:PRI) provides term life insurance, investment products, and other financial services to middle-income households in the United States and Canada.

Primerica's business model centers on transforming individuals into part-time financial representatives who primarily sell to their personal networks. The company targets households earning between $30,000 and $130,000 annually, a demographic often underserved by traditional financial advisors who typically focus on wealthier clients. This approach allows Primerica to reach millions of middle-income families through person-to-person connections.

The company's product lineup is designed to address basic financial needs. Its term life insurance policies offer straightforward death benefits without investment components, with coverage periods ranging from 10 to 35 years. On the investment side, Primerica representatives help clients build retirement savings through mutual funds, managed investments, annuities, and employer-sponsored retirement plans.

In 2021, Primerica expanded into the senior health insurance market by acquiring e-TeleQuote, which sells Medicare Advantage and Medicare Supplement plans to eligible beneficiaries. Unlike Primerica's core business, e-TeleQuote employs full-time licensed health insurance agents who enroll seniors in plans from major carriers like UnitedHealthcare and Humana.

Primerica's representatives earn commissions on initial sales and ongoing trails based on client asset values. The company attracts representatives by offering a business opportunity with low entry costs, allowing individuals to supplement their income without leaving their current jobs. This entrepreneurial pitch helps Primerica continuously recruit new representatives to replace those who leave, maintaining its distribution network across the United States and Canada.

4. Life Insurance

Life insurance companies collect premiums from policyholders in exchange for providing a future death benefit or retirement income stream. Interest rates matter for the sector (and make it cyclical), with higher rates allowing insurers to reinvest their fixed-income portfolios at more attractive yields and vice versa. Additionally, favorable demographic shifts, such as an aging population, are driving strong demand for retirement products while AI and data analytics offer significant opportunities to improve underwriting accuracy and operational efficiency. Conversely, the industry faces headwinds from persistent competition from agile insurtechs that threaten traditional distribution models.

Primerica competes with traditional life insurance companies like Northwestern Mutual and New York Life, discount brokerages such as Charles Schwab (NYSE:SCHW) and Fidelity, and other financial services firms targeting middle-income consumers including Edward Jones and Ameriprise Financial (NYSE:AMP).

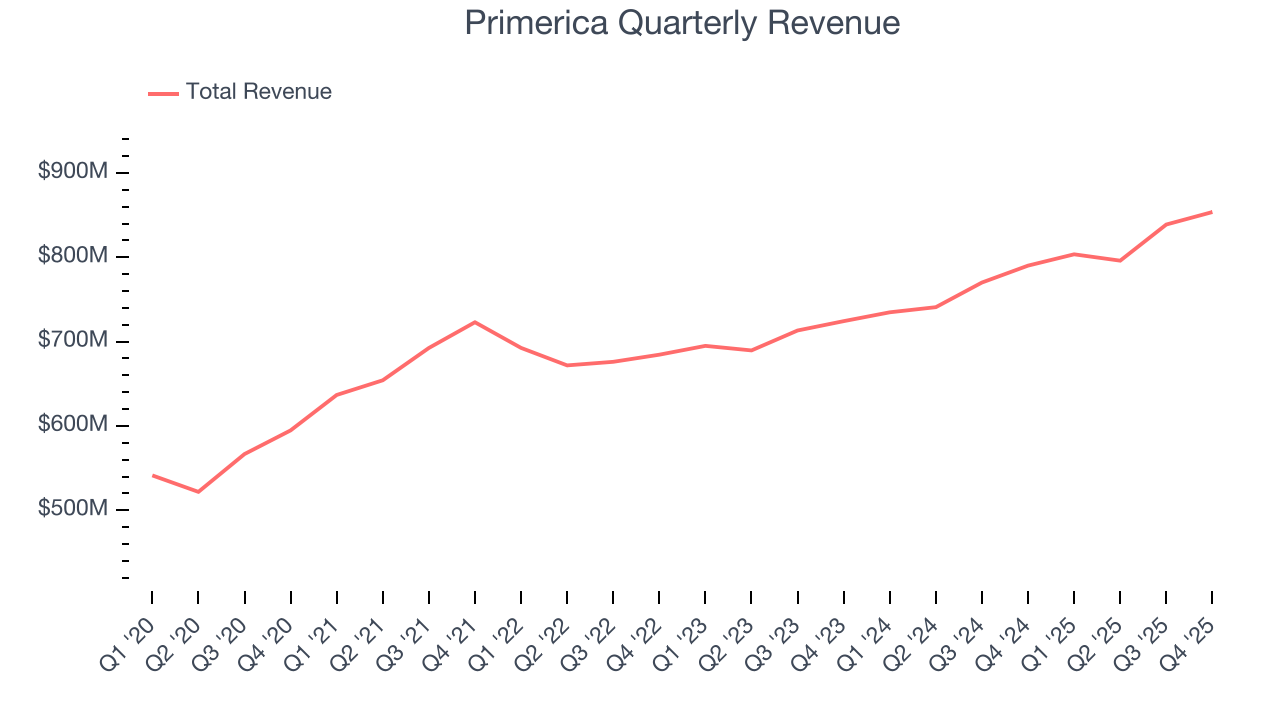

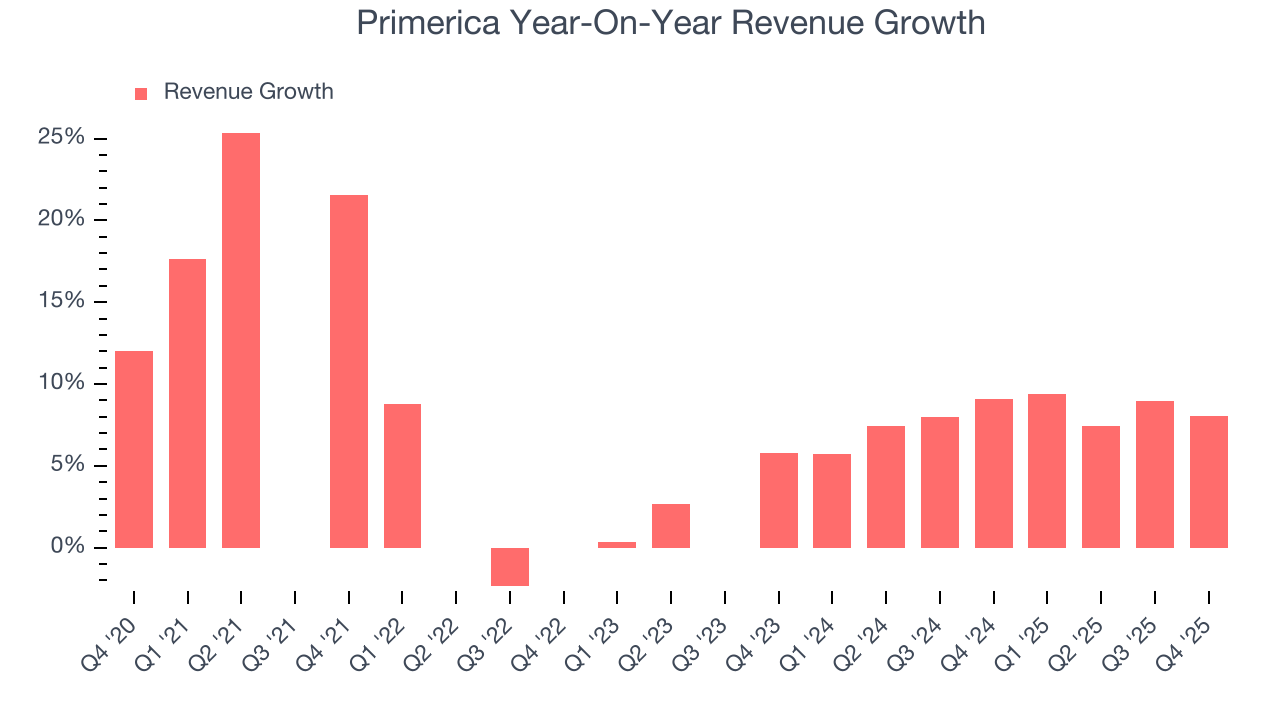

5. Revenue Growth

Insurance companies generate revenue three ways. The first is the core insurance business itself, represented in the income statement as premiums earned. The second source is investment income from investing the “float” (premiums collected but not yet paid out as claims) in assets such as fixed-income assets and equities. The third is fees from policy administration, annuities, and other value-added services. Luckily, Primerica’s revenue grew at a decent 8.2% compounded annual growth rate over the last five years. Its growth was slightly above the average insurance company and shows its offerings resonate with customers.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Primerica’s annualized revenue growth of 8% over the last two years aligns with its five-year trend, suggesting its demand was stable.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Primerica reported year-on-year revenue growth of 8%, and its $853.7 million of revenue exceeded Wall Street’s estimates by 0.8%.

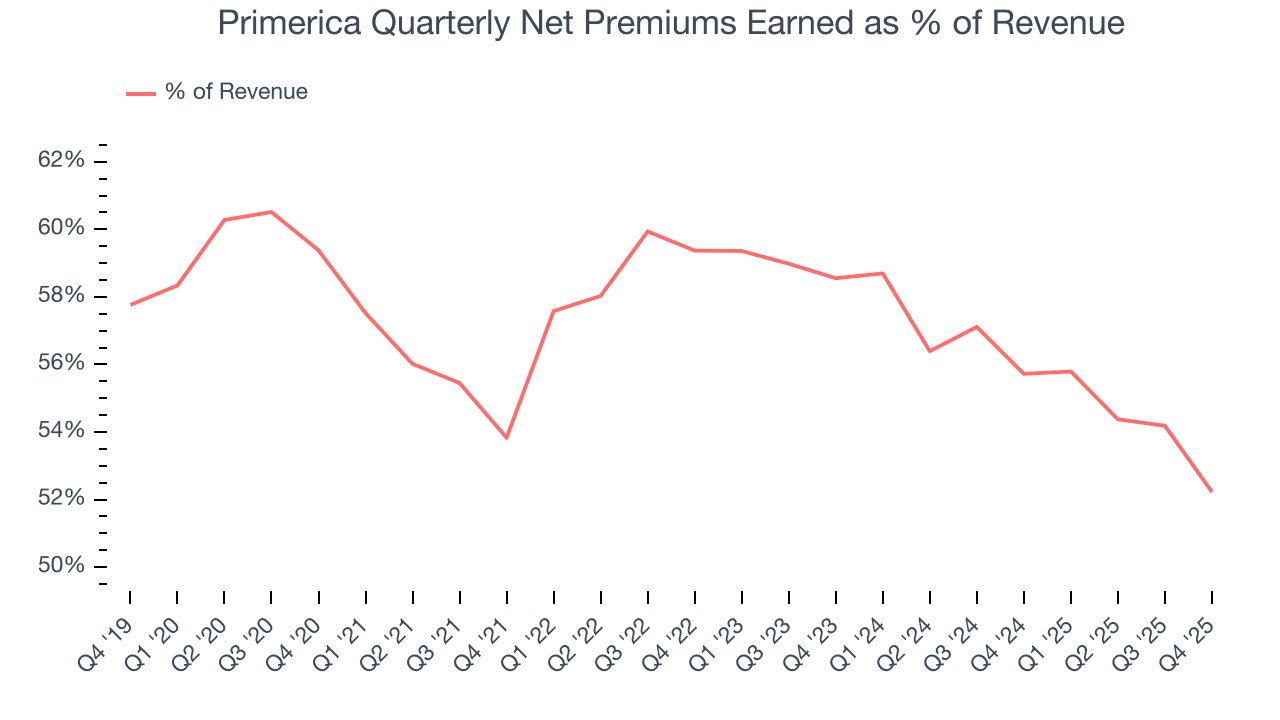

Net premiums earned made up 56.7% of the company’s total revenue during the last five years, meaning Primerica’s growth drivers strike a balance between insurance and non-insurance activities.

Markets consistently prioritize net premiums earned growth over investment and fee income, recognizing its superior quality as a core indicator of the company’s underwriting success and market penetration.

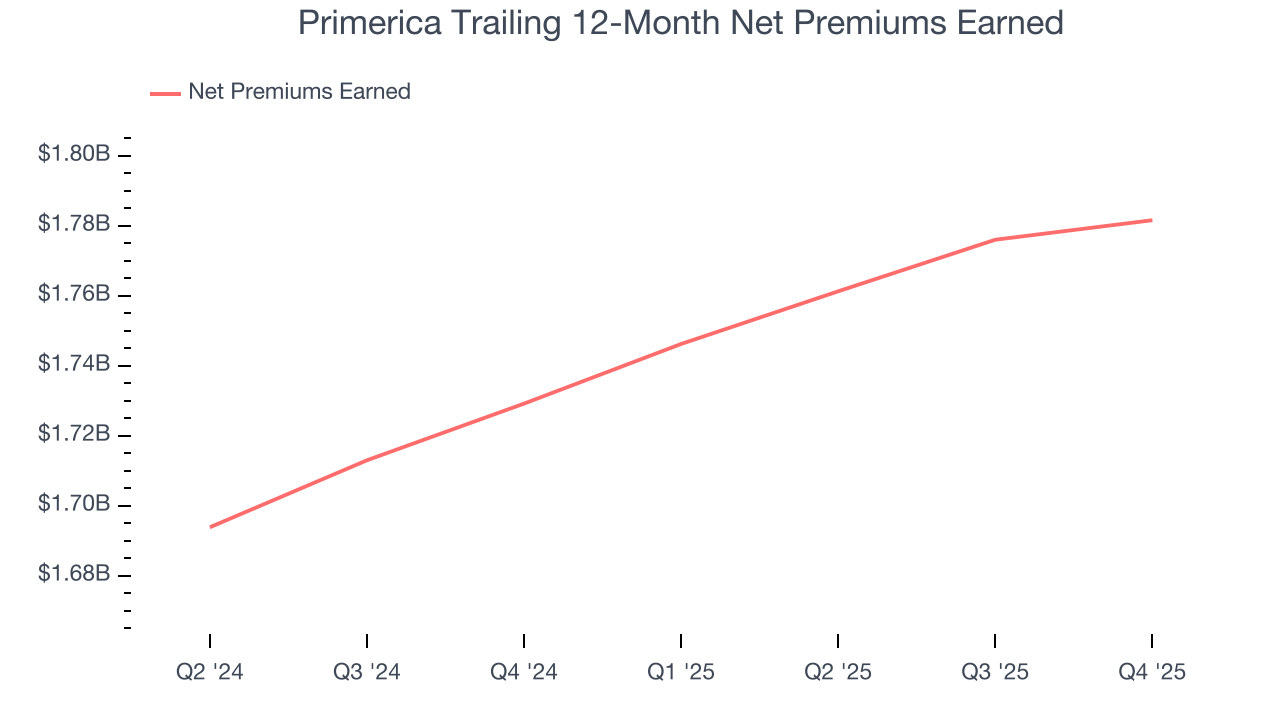

6. Net Premiums Earned

When insurers sell policies, they protect themselves from extremely large losses or an outsized accumulation of losses with reinsurance (insurance for insurance companies). Net premiums earned are:

- Gross premiums - what’s ceded to reinsurers as a risk mitigation and transfer strategy

Primerica’s net premiums earned has grown at a 6.1% annualized rate over the last five years, slightly worse than the broader insurance industry and slower than its total revenue.

When analyzing Primerica’s net premiums earned over the last two years, we can see that growth decelerated to 3.6% annually. Since two-year net premiums earned grew slower than total revenue over this period, it’s implied that other line items such as investment income grew at a faster rate. While these additional streams certainly contribute to the bottom line, their impact can vary. Some firms have shown greater success and long-term consistency in investing their float compared to peers. However, sharp fluctuations in the fixed income and equity markets can significantly affect short-term performance.

This quarter, Primerica’s net premiums earned was $445.9 million, up 1.3% year on year. But this wasn’t enough juice to meet Wall Street Consensus estimates.

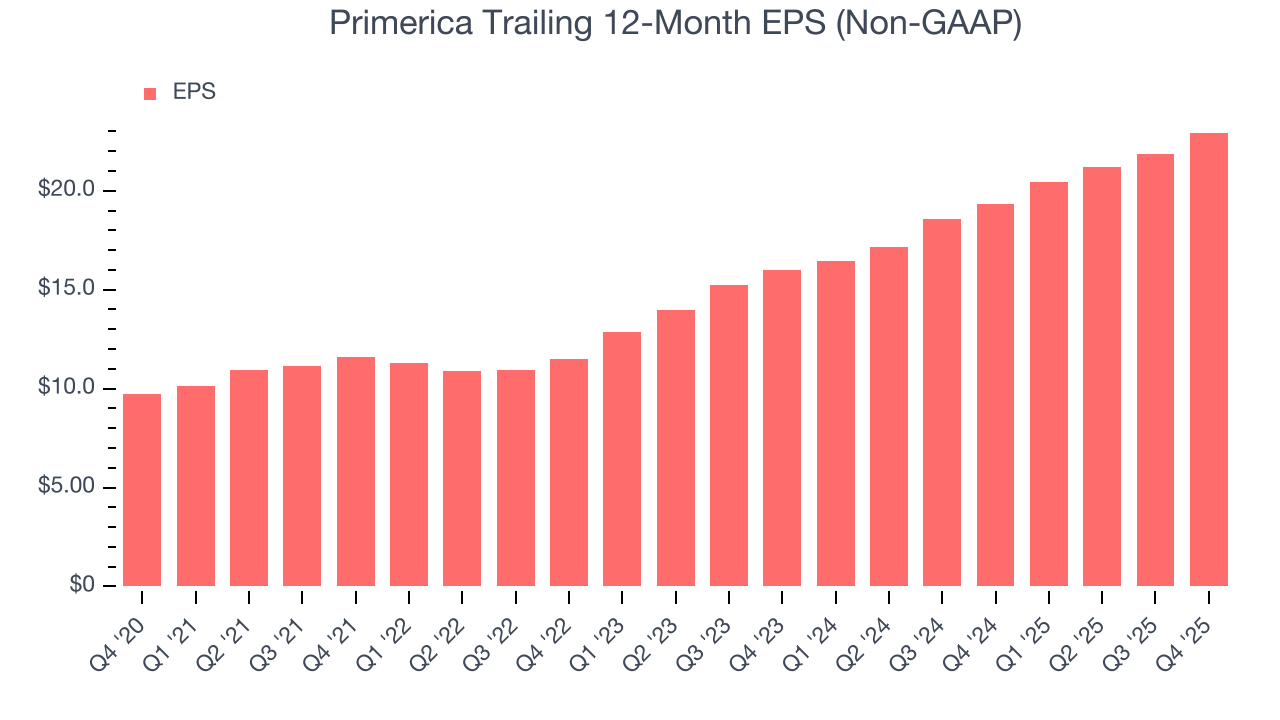

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Primerica’s EPS grew at a remarkable 18.7% compounded annual growth rate over the last five years, higher than its 8.2% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

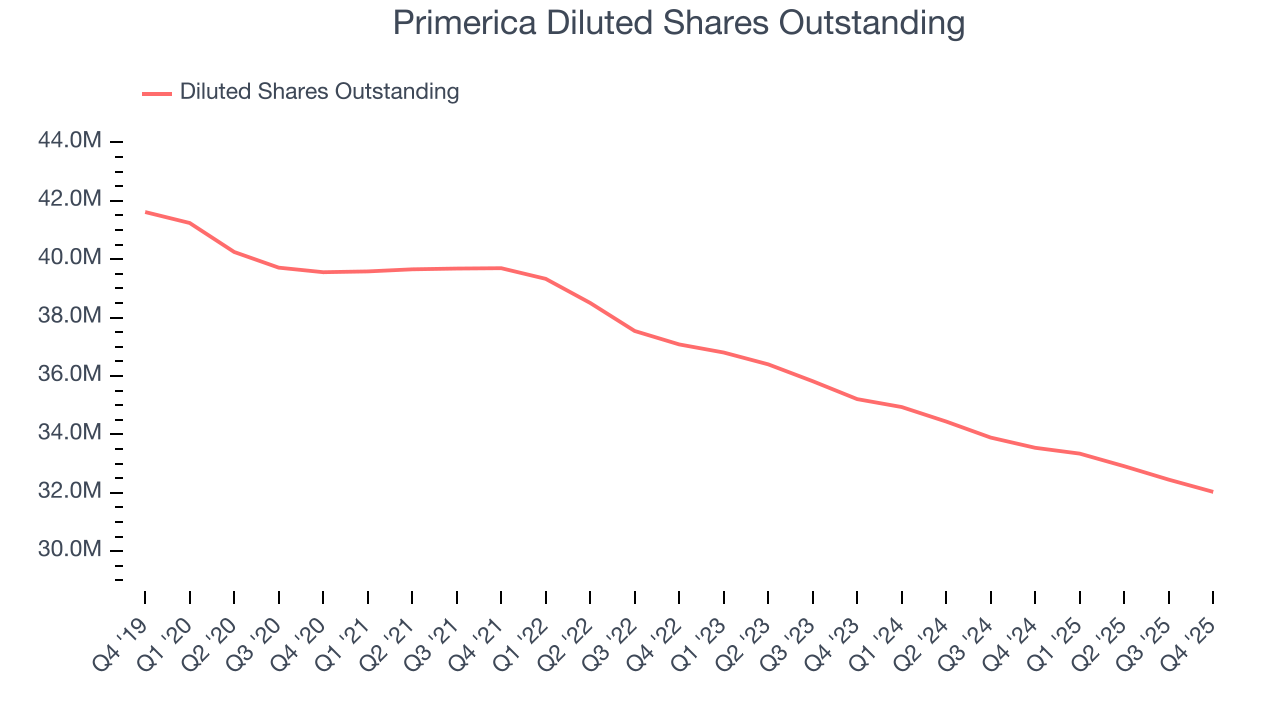

Diving into the nuances of Primerica’s earnings can give us a better understanding of its performance. As we mentioned earlier, Primerica’s pre-tax profit margin expanded by 6.8 percentage points over the last five years. On top of that, its share count shrank by 19%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Primerica, its two-year annual EPS growth of 19.7% is similar to its five-year trend, implying stable earnings.

In Q4, Primerica reported adjusted EPS of $6.13, up from $5.03 in the same quarter last year. This print beat analysts’ estimates by 8%. Over the next 12 months, Wall Street expects Primerica’s full-year EPS of $22.94 to grow 3.5%.

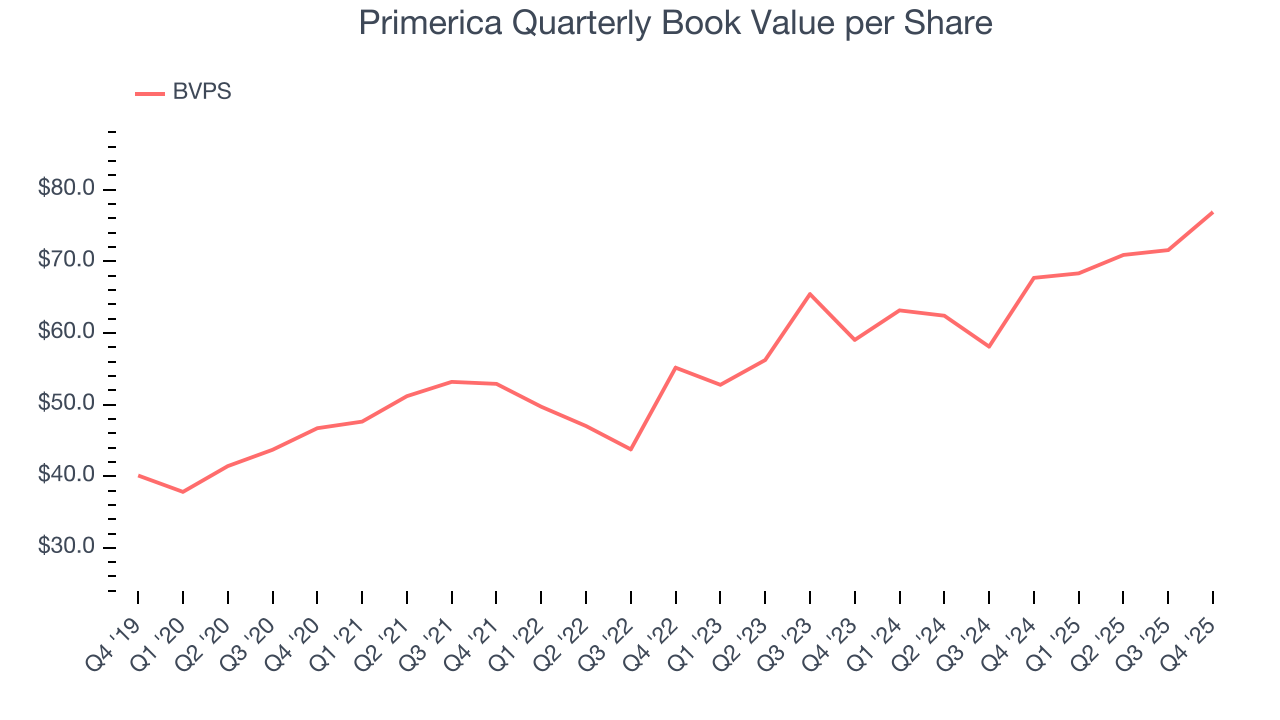

8. Book Value Per Share (BVPS)

Insurance companies are balance sheet businesses, collecting premiums upfront and paying out claims over time. The float–premiums collected but not yet paid out–are invested, creating an asset base supported by a liability structure. Book value per share (BVPS) captures this dynamic by measuring these assets (investment portfolio, cash, reinsurance recoverables) less liabilities (claim reserves, debt, future policy benefits). BVPS is essentially the residual value for shareholders.

We therefore consider BVPS very important to track for insurers and a metric that sheds light on business quality. While other (and more commonly known) per-share metrics like EPS can sometimes be lumpy due to reserve releases or one-time items and can be managed or skewed while still following accounting rules, BVPS reflects long-term capital growth and is harder to manipulate.

Primerica’s BVPS grew at a solid 10.5% annual clip over the last five years. BVPS growth has also accelerated recently, growing by 14.1% annually over the last two years from $59.03 to $76.89 per share.

Over the next 12 months, Consensus estimates call for Primerica’s BVPS to grow by 4.3% to $72.96, lousy growth rate.

9. Balance Sheet Assessment

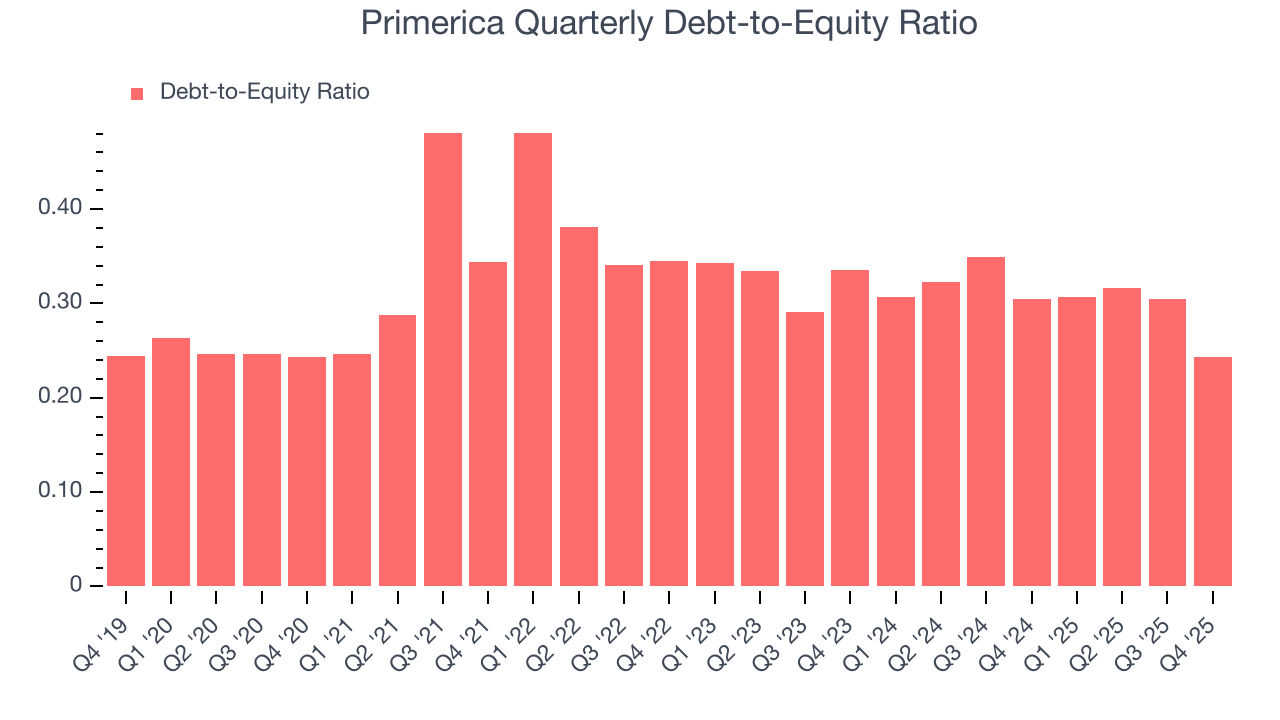

The debt-to-equity ratio is a widely used measure to assess a company's balance sheet health. A higher ratio means that a business aggressively financed its growth with debt. This can result in higher earnings (if the borrowed funds are invested profitably) but also increases risk.

If debt levels are too high, there could be difficulties in meeting obligations, especially during economic downturns or periods of rising interest rates if the debt has variable-rate payments.

Primerica currently has $595.3 million of debt and $2.45 billion of shareholder's equity on its balance sheet, and over the past four quarters, has averaged a debt-to-equity ratio of 0.3×. We think this is safe and raises no red flags. In general, we’re comfortable with any ratio below 1.0× for an insurance business. Anything below 0.5× is a bonus.

10. Return on Equity

Return on equity, or ROE, represents the ultimate measure of an insurer's effectiveness, quantifying how well it transforms shareholder investments into profits. Over the long term, insurance companies with robust ROE metrics typically deliver superior shareholder returns through a balanced approach to capital management.

Over the last five years, Primerica has averaged an ROE of 27.7%, exceptional for a company operating in a sector where the average shakes out around 12.5% and those putting up 20%+ are greatly admired. This shows Primerica has a strong competitive moat.

11. Key Takeaways from Primerica’s Q4 Results

It was good to see Primerica narrowly top analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its net premiums earned missed. Overall, this was a weaker quarter. The stock traded up 1.9% to $258.23 immediately following the results.

12. Is Now The Time To Buy Primerica?

Updated: March 30, 2026 at 12:06 AM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Primerica.

There are a lot of things to like about Primerica. To kick things off, its revenue growth was decent over the last five years. And while its projected EPS for the next year is lacking, its stellar ROE suggests it has been a well-run company historically. On top of that, its expanding pre-tax profit margin shows the business has become more efficient.

Primerica’s P/B ratio based on the next 12 months is 3x. This valuation tells us it’s a bit of a market darling with a lot of good news priced in. Primerica is a good one to add to your watchlist - there are companies featuring superior fundamentals at the moment.

Wall Street analysts have a consensus one-year price target of $289.43 on the company (compared to the current share price of $246.21).