Rocket Companies (RKT)

Rocket Companies piques our interest. Its revenue and EPS are projected to skyrocket next year, an optimistic sign for its share price.― StockStory Analyst Team

1. News

2. Summary

Why Rocket Companies Is Interesting

Born in Detroit during the 1980s and evolving into a tech-driven financial powerhouse, Rocket Companies (NYSE:RKT) is a fintech company that provides digital mortgage lending, real estate services, and personal finance solutions through its technology platform.

- Notable projected net interest income growth of 35.5% for the next 12 months hints at market share gains

- Notable projected tangible book value per share growth of 427% for the next 12 months hints at strong capital generation

- On the flip side, its customers postponed purchases of its products and services this cycle as its revenue declined by 16.7% annually over the last five years

Rocket Companies almost passes our quality test. We’d wait until its quality rises or its price falls.

Why Should You Watch Rocket Companies

Rocket Companies is trading at $17.69 per share, or 2.8x forward P/B. The rich valuation multiple means there is a lot of good news priced into the stock; short-term price swings could result if anything bursts that bubble.

Rocket Companies could improve its business quality by stringing together a few solid quarters. We’d be more open to buying the stock when that time comes.

3. Rocket Companies (RKT) Research Report: Q4 CY2025 Update

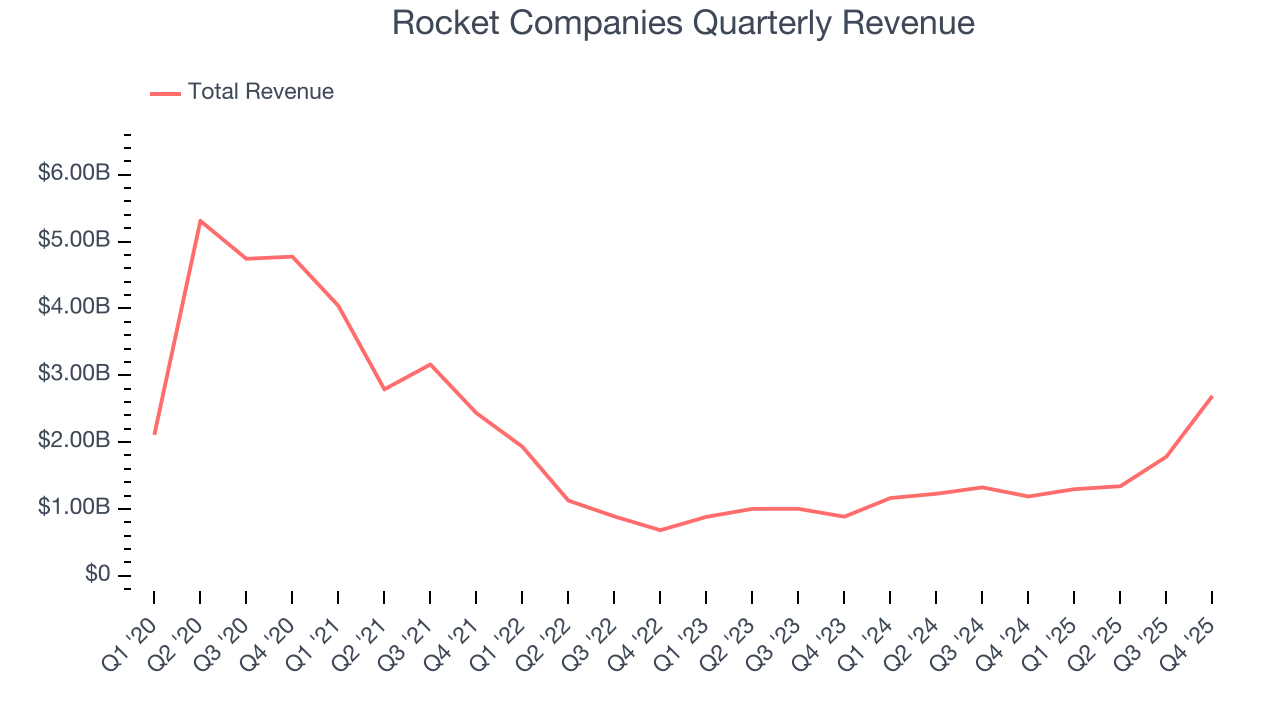

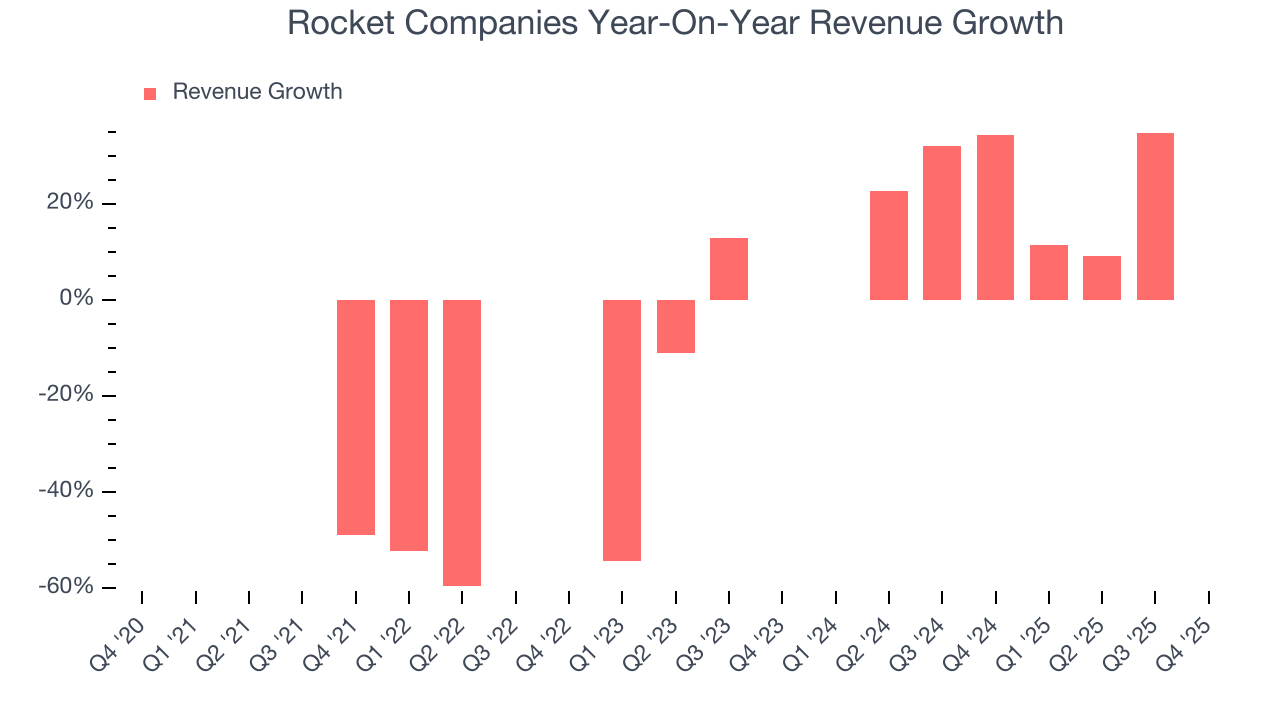

Fintech mortgage provider Rocket Companies (NYSE:RKT) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 127% year on year to $2.69 billion. On top of that, next quarter’s revenue guidance ($2.7 billion at the midpoint) was surprisingly good and 15.9% above what analysts were expecting. Its non-GAAP profit of $0.11 per share was 26.7% above analysts’ consensus estimates.

Rocket Companies (RKT) Q4 CY2025 Highlights:

- Net Interest Income: $29 million vs analyst estimates of $36.54 million

- Revenue: $2.69 billion vs analyst estimates of $2.21 billion (127% year-on-year growth, 21.7% beat)

- Adjusted EPS: $0.11 vs analyst estimates of $0.09 (26.7% beat)

- Revenue Guidance for Q1 CY2026 is $2.7 billion at the midpoint, above analyst estimates of $2.33 billion

- Market Capitalization: $48.8 billion

Company Overview

Born in Detroit during the 1980s and evolving into a tech-driven financial powerhouse, Rocket Companies (NYSE:RKT) is a fintech company that provides digital mortgage lending, real estate services, and personal finance solutions through its technology platform.

The company operates through several interconnected businesses centered around homeownership and financial services. Its flagship business, Rocket Mortgage, offers a digital mortgage application and approval process that allows clients to apply, upload documents, e-sign, and manage their loans through a mobile app or website. Rocket Mortgage functions both as a loan originator and servicer, maintaining relationships with clients throughout the life of their loans.

Rocket's ecosystem extends beyond mortgages to include Rocket Homes, a real estate search platform with agent referral services; Rocket Money, a personal finance app for budget management and subscription tracking; Rocket Loans, which provides personal loans; and Amrock, which handles title insurance, property valuation, and settlement services. This integrated approach allows clients to navigate the entire homebuying process within the Rocket platform.

The company generates revenue primarily by originating mortgage loans that it sells to government-backed entities like Fannie Mae and Freddie Mac or other investors in the secondary mortgage market. Rocket operates through both direct-to-consumer channels and partner networks, including relationships with mortgage brokers and financial institutions.

Rocket has heavily invested in artificial intelligence and data analytics, leveraging its vast data assets (10 petabytes) to automate processes and enhance client experiences. For instance, a homebuyer might use Rocket Homes to find a property, connect with a real estate agent, secure mortgage pre-approval through Rocket Mortgage, and close the transaction with Amrock's services—all within the same technology ecosystem.

4. Thrifts & Mortgage Finance

Thrifts & Mortgage Finance institutions operate by accepting deposits and extending loans primarily for residential mortgages, earning revenue through interest rate spreads (difference between lending rates and borrowing costs) and origination fees. The industry benefits from demographic tailwinds as millennials enter prime homebuying age, technological advancements streamlining the loan approval process, and potential interest rate stabilization improving affordability. However, significant headwinds include net interest margin compression during rate volatility, increased competition from fintech disruptors offering digital-first experiences, mounting regulatory compliance costs, and potential housing market corrections that could impact loan portfolios and default rates.

Rocket Companies competes with traditional mortgage lenders like Wells Fargo (NYSE:WFC) and Bank of America (NYSE:BAC), as well as digital-first mortgage providers such as UWM Holdings (NYSE:UWMC), loanDepot (NYSE:LDI), and PennyMac Financial Services (NYSE:PFSI).

5. Sales Growth

From lending activities to service fees, most banks build their revenue model around two income sources. Interest rate spreads between loans and deposits create the first stream, with the second coming from charges on everything from basic bank accounts to complex investment banking transactions. Rocket Companies’s demand was weak over the last five years as its revenue fell at a 15.9% annual rate. This wasn’t a great result, but there are still things to like about Rocket Companies.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Rocket Companies’s annualized revenue growth of 37.3% over the last two years is above its five-year trend, suggesting its demand recently accelerated.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Rocket Companies reported magnificent year-on-year revenue growth of 127%, and its $2.69 billion of revenue beat Wall Street’s estimates by 21.7%. Company management is currently guiding for a 108% year-on-year increase in sales next quarter.

6. Earnings Per Share

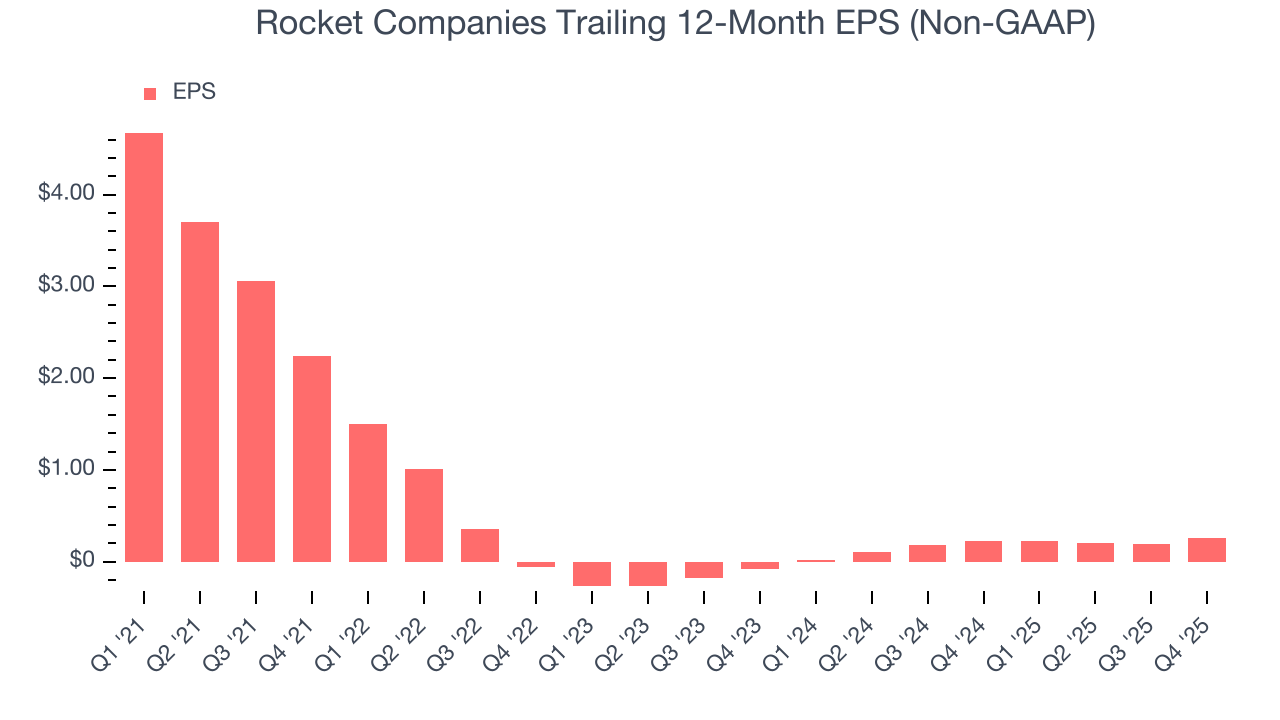

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Rocket Companies, its EPS declined by 43.4% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Rocket Companies, its two-year annual EPS growth of 129% was higher than its five-year trend. This acceleration made it one of the faster-growing banking companies in recent history.

In Q4, Rocket Companies reported adjusted EPS of $0.11, up from $0.04 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Rocket Companies’s full-year EPS of $0.26 to grow 217%.

7. Return on Equity

Return on equity, or ROE, tells us how much profit a company generates for each dollar of shareholder equity, a key funding source for banks. Over a long period, banks with high ROE tend to compound shareholder wealth faster through retained earnings, buybacks, and dividends.

Over the last five years, Rocket Companies has averaged an ROE of 16.5%, excellent for a company operating in a sector where the average shakes out around 7.5% and those putting up 15%+ are greatly admired. This shows Rocket Companies has a strong competitive moat.

8. Key Takeaways from Rocket Companies’s Q4 Results

It was good to see Rocket Companies beat analysts’ EPS expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. On the other hand, its net interest income missed. Overall, we think this was a solid quarter with some key areas of upside. The stock traded up 9.1% to $19.21 immediately after reporting.

9. Is Now The Time To Buy Rocket Companies?

Updated: February 26, 2026 at 4:15 PM EST

Before investing in or passing on Rocket Companies, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

Rocket Companies is a fine business. Although its revenue has declined over the last five years, its growth over the next 12 months is expected to be higher. And while Rocket Companies’s declining EPS over the last five years makes it a less attractive asset to the public markets, its estimated net interest income growth for the next 12 months is great. On top of that, its projected EPS for the next year implies the company’s fundamentals will improve.

Rocket Companies’s P/B ratio based on the next 12 months is 2.7x. At this valuation, there’s a lot of good news priced in. Add this one to your watchlist and come back to it later.

Wall Street analysts have a consensus one-year price target of $21.57 on the company (compared to the current share price of $19.21).