Rush Street Interactive (RSI)

We wouldn’t buy Rush Street Interactive. Its underwhelming revenue growth and failure to generate meaningful free cash flow is a concerning trend.― StockStory Analyst Team

1. News

2. Summary

Why We Think Rush Street Interactive Will Underperform

Specializing in online casino gaming and sports betting, Rush Street Interactive (NYSE:RSI) is an operator of digital gaming platforms.

- Operating margin falls short of the industry average, and the smaller profit dollars make it harder to react to unexpected market developments

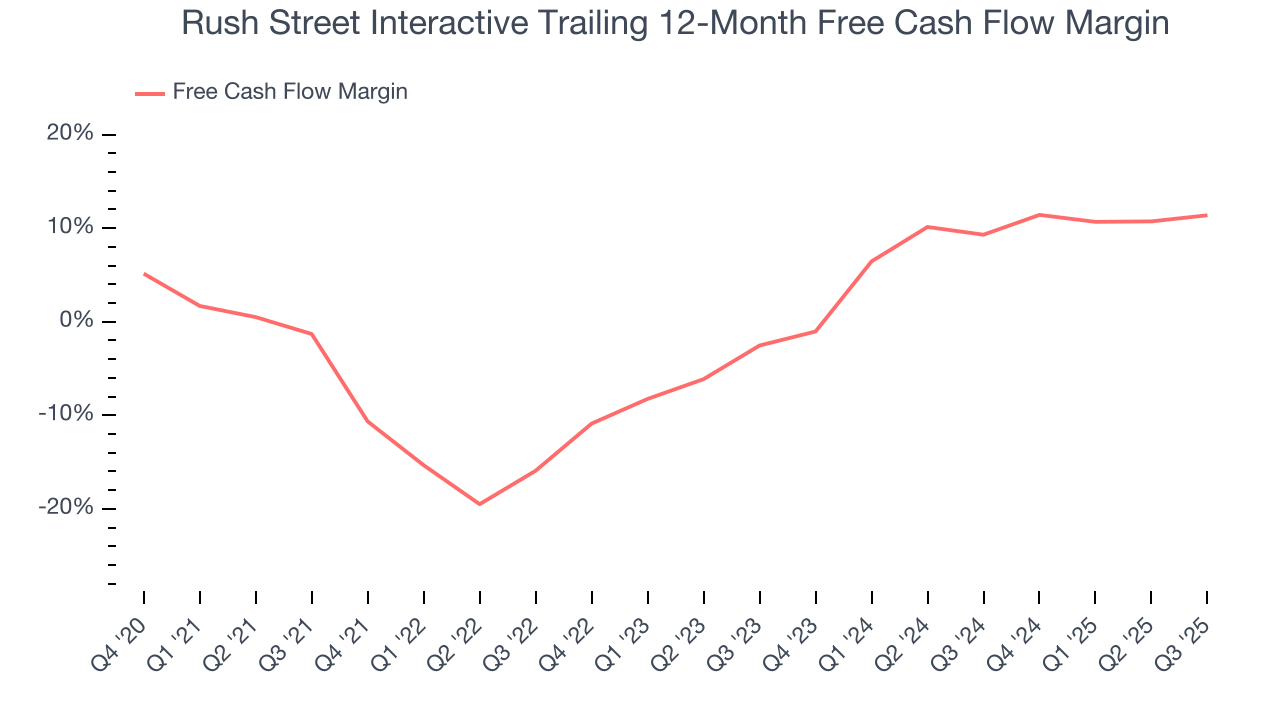

- Ability to fund investments or reward shareholders with increased buybacks or dividends is restricted by its weak free cash flow margin of 13.1% for the last two years

- Lackluster 28.1% annual revenue growth over the last two years indicates the company is losing ground to competitors

Rush Street Interactive fails to meet our quality criteria. We’re hunting for superior stocks elsewhere.

Why There Are Better Opportunities Than Rush Street Interactive

At $19.49 per share, Rush Street Interactive trades at 27.9x forward P/E. This multiple is higher than that of consumer discretionary peers; it’s also rich for the top-line growth of the company. Not a great combination.

There are stocks out there similarly priced with better business quality. We prefer owning these.

3. Rush Street Interactive (RSI) Research Report: Q4 CY2025 Update

Online casino and sports betting company Rush Street Interactive (NYSE:RSI) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 27.8% year on year to $324.9 million. The company’s full-year revenue guidance of $1.4 billion at the midpoint came in 6.2% above analysts’ estimates. Its non-GAAP profit of $0.08 per share was 24.8% below analysts’ consensus estimates.

Rush Street Interactive (RSI) Q4 CY2025 Highlights:

- Revenue: $324.9 million vs analyst estimates of $304.8 million (27.8% year-on-year growth, 6.6% beat)

- Adjusted EPS: $0.08 vs analyst expectations of $0.11 (24.8% miss)

- Adjusted EBITDA: $44.15 million vs analyst estimates of $42.56 million (13.6% margin, 3.7% beat)

- EBITDA guidance for the upcoming financial year 2026 is $220 million at the midpoint, above analyst estimates of $211.9 million

- Operating Margin: 8.8%, up from 4.8% in the same quarter last year

- Market Capitalization: $1.57 billion

Company Overview

Specializing in online casino gaming and sports betting, Rush Street Interactive (NYSE:RSI) is an operator of digital gaming platforms.

Rush Street Interactive recognized the burgeoning demand for mobile gaming and entered the market in 2012 to address the need for high-quality, user-friendly online games.

Today, the company provides a wide array of online casino games and sports betting options through its digital platforms. This lineup includes slot games, table games, and sportsbooks, appealing to both casual and serious players.

Rush Street Interactive generates revenue by acting as "the house" for its real-money gaming customers. In the company's social gaming business, which doesn't use real money, revenue is derived from in-game purchases for virtual currencies that can be used to play games.

4. Consumer Discretionary - Gaming Solutions

The Consumer Discretionary sector, by definition, is made up of companies selling non-essential goods and services. When economic conditions deteriorate or tastes shift, consumers can easily cut back or eliminate these purchases. For long-term investors with five-year holding periods, this creates a structural challenge: the sector is inherently hit-driven, with low switching costs and fickle customers. As a result, only a handful of companies can reliably grow demand and compound earnings over long periods, which is why our bar is high and High Quality ratings are rare.

Gaming solutions companies provide the technology infrastructure behind gambling—slot machines, table game systems, lottery terminals, sports-betting platforms, and back-end software for casinos and online operators. Tailwinds include the ongoing legalization of sports betting across U.S. states and international markets, growing adoption of digital and mobile wagering, and casino operators' demand for data-driven player engagement tools. However, headwinds include stringent and evolving regulatory requirements across jurisdictions, high upfront R&D costs to develop next-generation platforms, and customer concentration risk given the limited number of large casino operators. Increasing competition from in-house technology development by major operators also pressures demand.

Rush Street Interactive competes with established online-first companies like Flutter Entertainment (FanDuel, PokerStars), DraftKings, BetMGM, Bet365, and Fanatics (PointsBet), as well as traditional casino operators that have moved online, including Penn Entertainment (ESPN Bet), Hard Rock Digital, Caesars Entertainment, and Wynn Resorts (WynnBET).

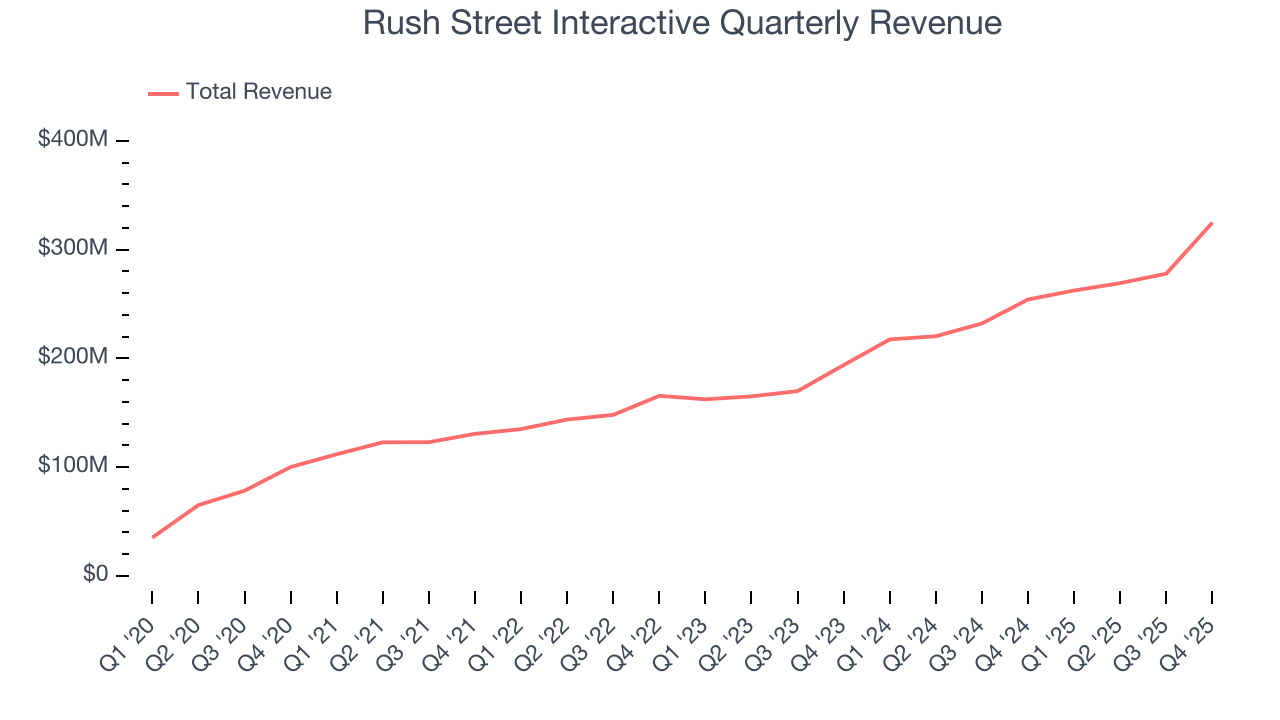

5. Revenue Growth

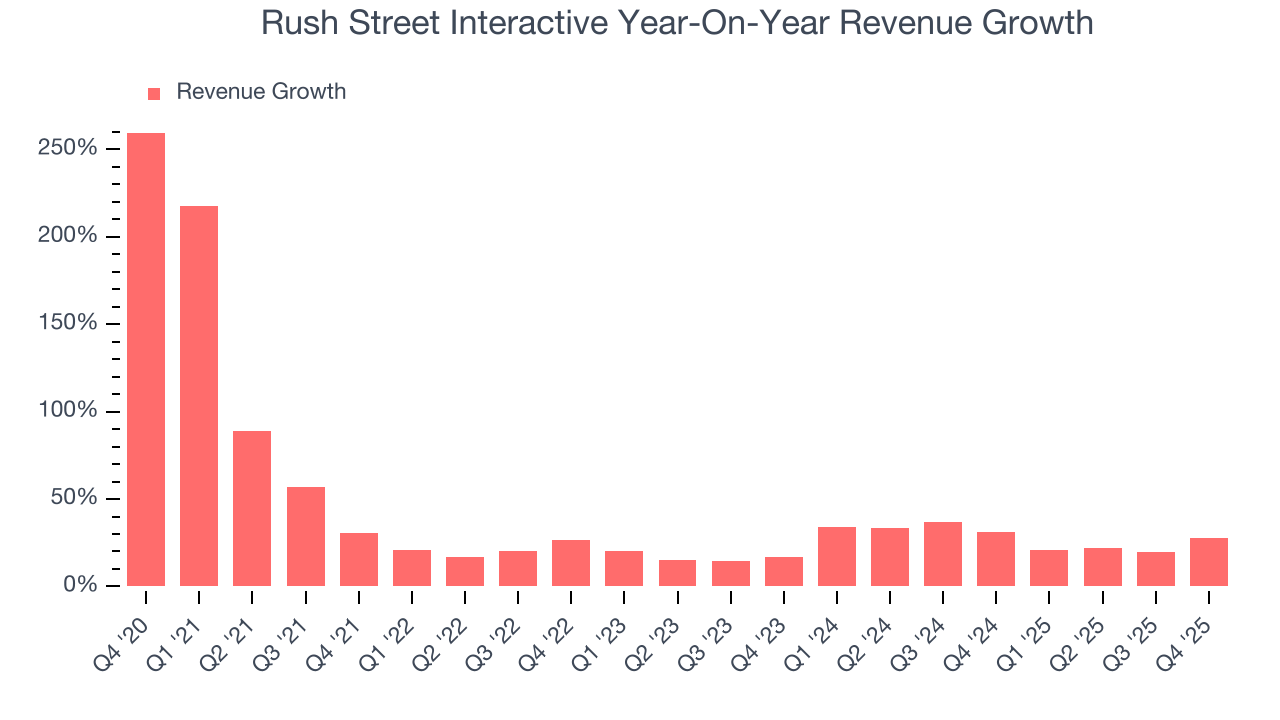

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Rush Street Interactive grew its sales at a 32.4% annual rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the consumer discretionary sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Rush Street Interactive’s recent performance shows its demand has slowed as its annualized revenue growth of 28.1% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

This quarter, Rush Street Interactive reported robust year-on-year revenue growth of 27.8%, and its $324.9 million of revenue topped Wall Street estimates by 6.6%.

Looking ahead, sell-side analysts expect revenue to grow 16.9% over the next 12 months, a deceleration versus the last two years. Despite the slowdown, this projection is noteworthy and suggests the market is baking in success for its products and services.

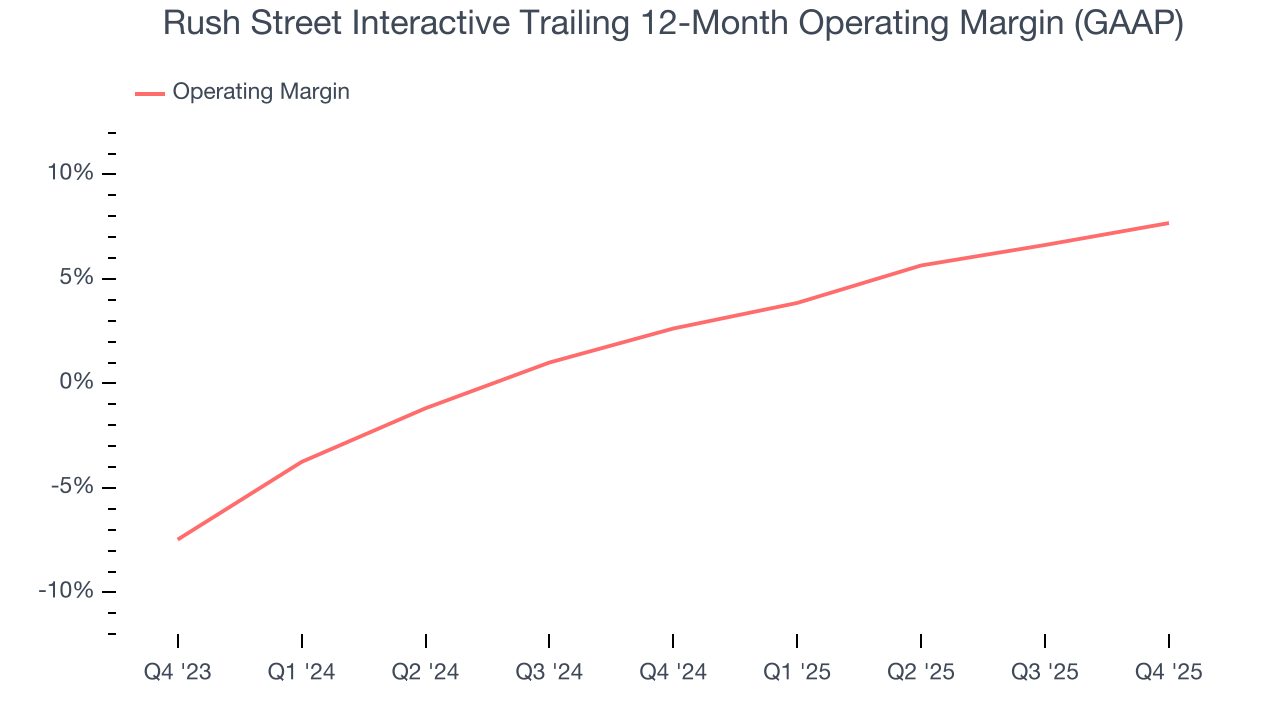

6. Operating Margin

Rush Street Interactive’s operating margin has risen over the last 12 months and averaged 5.4% over the last two years. The company’s higher efficiency is a breath of fresh air, but its suboptimal cost structure means it still sports inadequate profitability for a consumer discretionary business.

This quarter, Rush Street Interactive generated an operating margin profit margin of 8.8%, up 4.1 percentage points year on year. This increase was a welcome development and shows it was more efficient.

7. Earnings Per Share

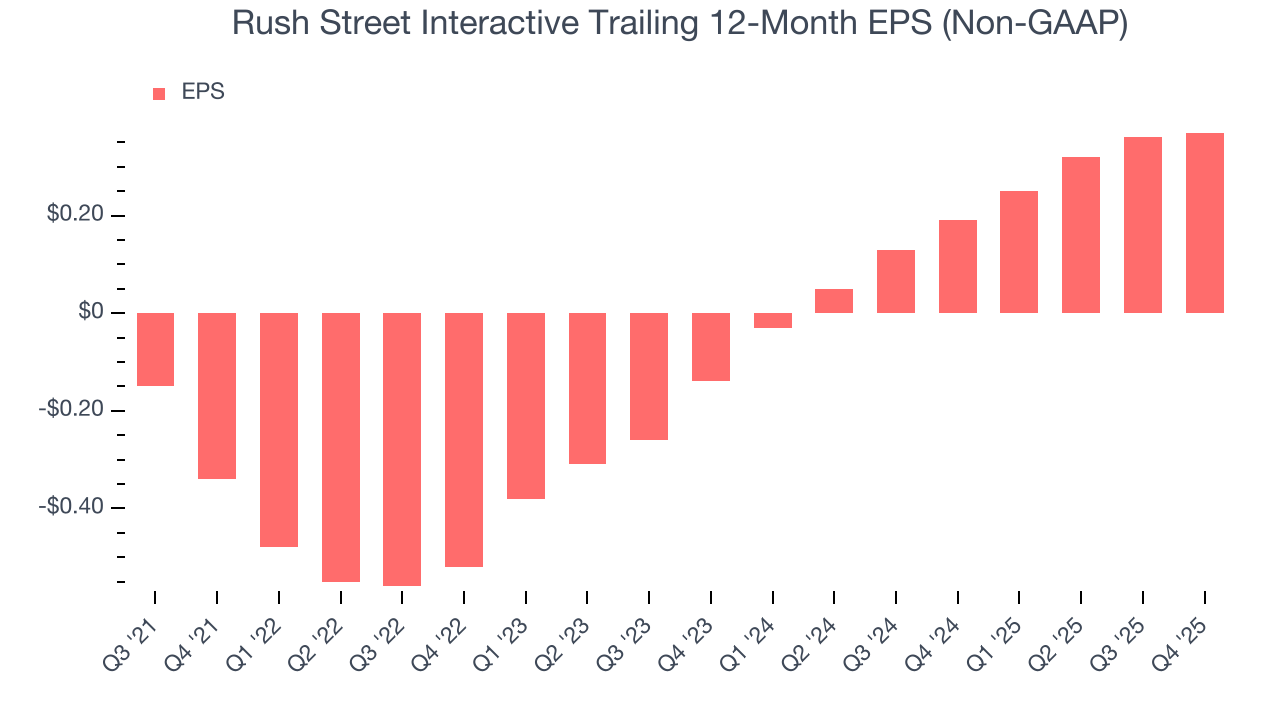

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Rush Street Interactive’s full-year EPS flipped from negative to positive over the last four years. This is encouraging and shows it’s at a critical moment in its life.

In Q4, Rush Street Interactive reported adjusted EPS of $0.08, up from $0.07 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates, but we care more about long-term adjusted EPS growth than short-term movements. Over the next 12 months, Wall Street expects Rush Street Interactive’s full-year EPS of $0.37 to grow 57%.

8. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Rush Street Interactive has shown poor cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 11.6%, lousy for a consumer discretionary business.

9. Balance Sheet Assessment

Businesses that maintain a cash surplus face reduced bankruptcy risk.

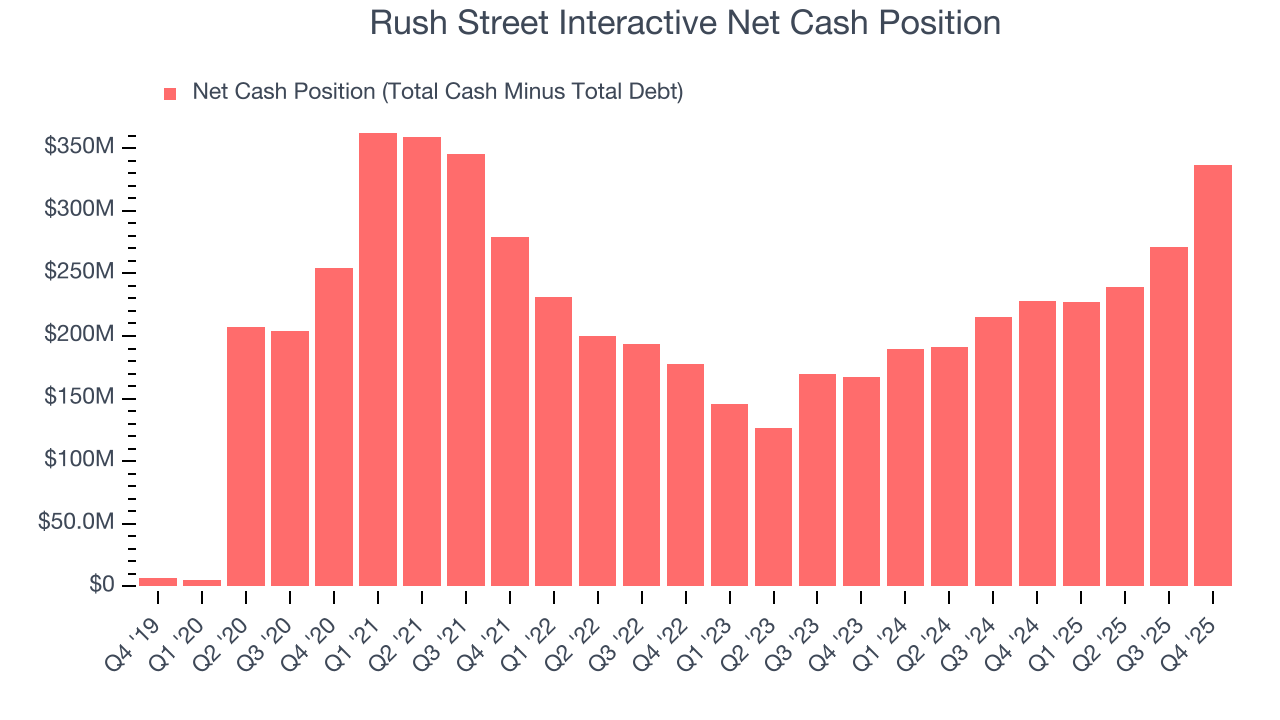

Rush Street Interactive is a profitable, well-capitalized company with $336.3 million of cash and no debt. This position is 20.3% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

10. Key Takeaways from Rush Street Interactive’s Q4 Results

We were impressed by Rush Street Interactive’s optimistic full-year revenue guidance, which blew past analysts’ expectations. We were also glad its revenue outperformed Wall Street’s estimates. On the other hand, its EPS missed. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 2.8% to $17.44 immediately following the results.

11. Is Now The Time To Buy Rush Street Interactive?

Updated: February 17, 2026 at 10:04 PM EST

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Rush Street Interactive.

Rush Street Interactive doesn’t pass our quality test. While its projected EPS for the next year implies the company’s fundamentals will improve, the downside is its Forecasted free cash flow margin suggests the company will ramp up its investments next year. On top of that, its low free cash flow margins give it little breathing room.

Rush Street Interactive’s P/E ratio based on the next 12 months is 27.9x. While this valuation is fair, the upside isn’t great compared to the potential downside. There are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $23.86 on the company (compared to the current share price of $19.49).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.