Rush Street Interactive (RSI)

Rush Street Interactive faces an uphill battle. Its underwhelming revenue growth and failure to generate meaningful free cash flow is a concerning trend.― StockStory Analyst Team

1. News

2. Summary

Why We Think Rush Street Interactive Will Underperform

Specializing in online casino gaming and sports betting, Rush Street Interactive (NYSE:RSI) is an operator of digital gaming platforms.

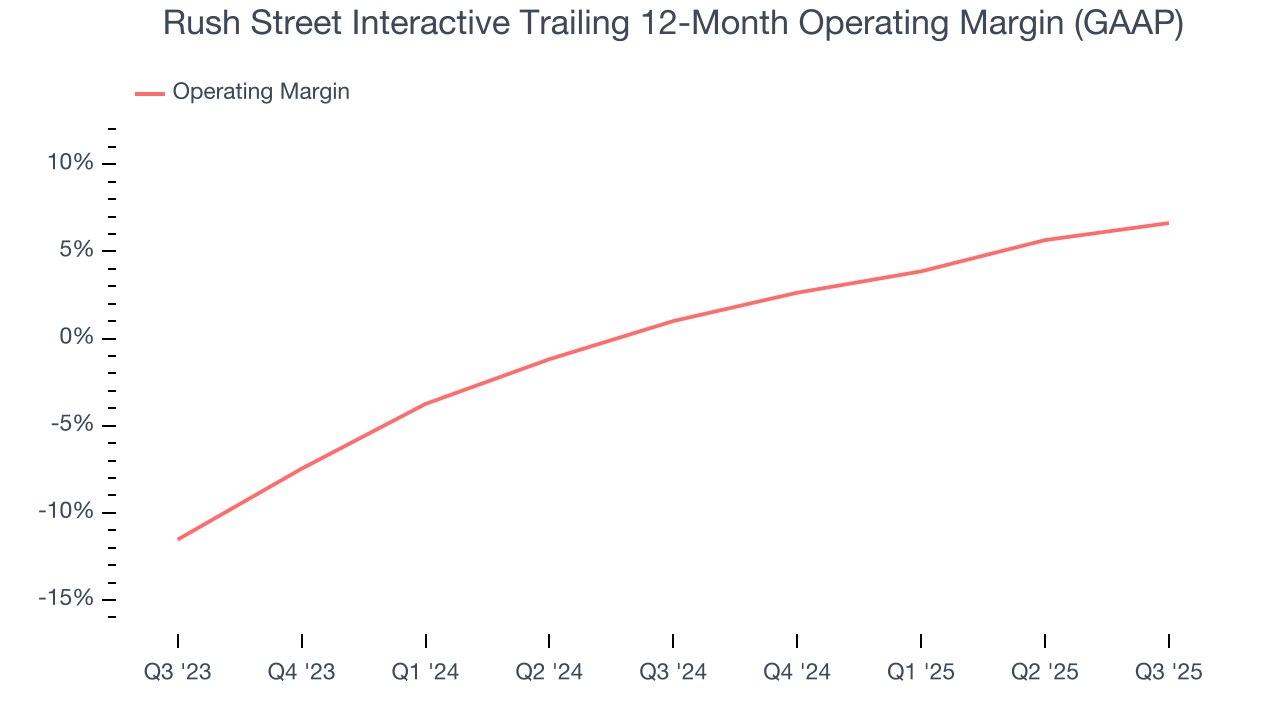

- Operating margin falls short of the industry average, and the smaller profit dollars make it harder to react to unexpected market developments

- Low free cash flow margin gives it little breathing room, constraining its ability to self-fund growth or return capital to shareholders

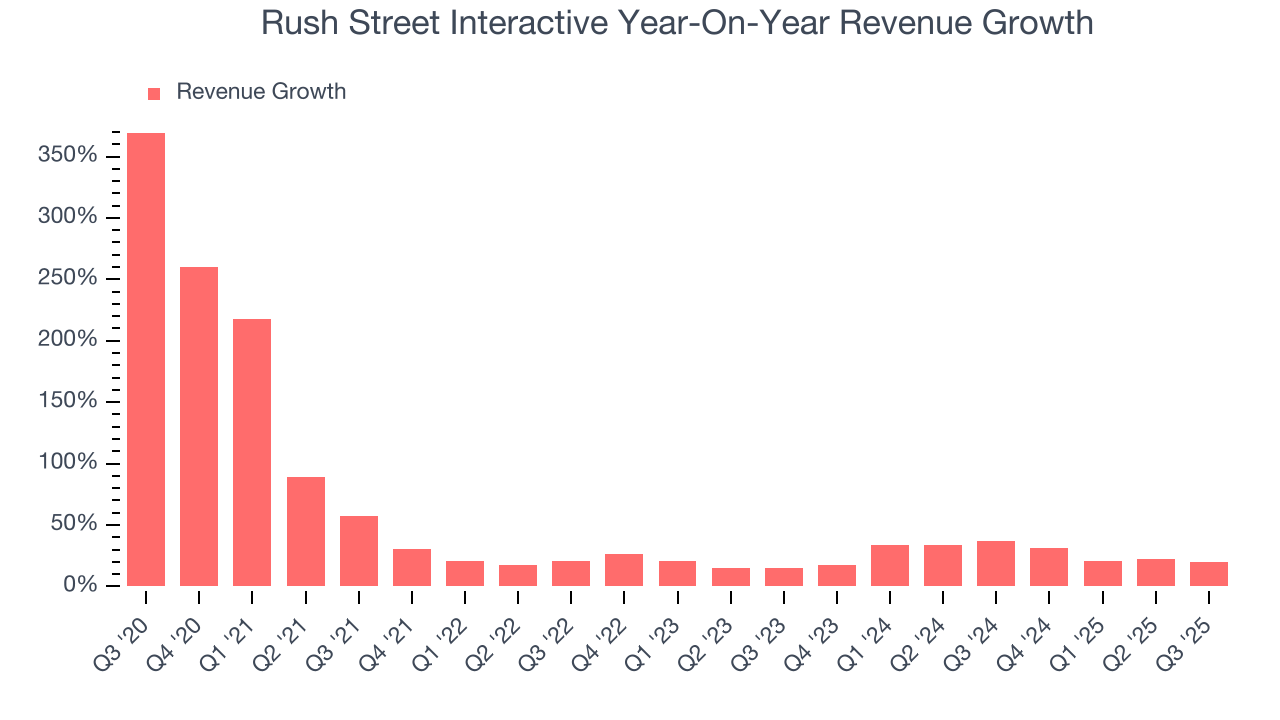

- Annual revenue growth of 26.7% over the last two years was below our standards for the consumer discretionary sector

Rush Street Interactive’s quality is insufficient. There are more promising prospects in the market.

Why There Are Better Opportunities Than Rush Street Interactive

Rush Street Interactive’s stock price of $17.05 implies a valuation ratio of 34.4x forward P/E. Not only is Rush Street Interactive’s multiple richer than most consumer discretionary peers, but it’s also expensive for its revenue characteristics.

We’d rather invest in similarly-priced but higher-quality companies with more reliable earnings growth.

3. Rush Street Interactive (RSI) Research Report: Q3 CY2025 Update

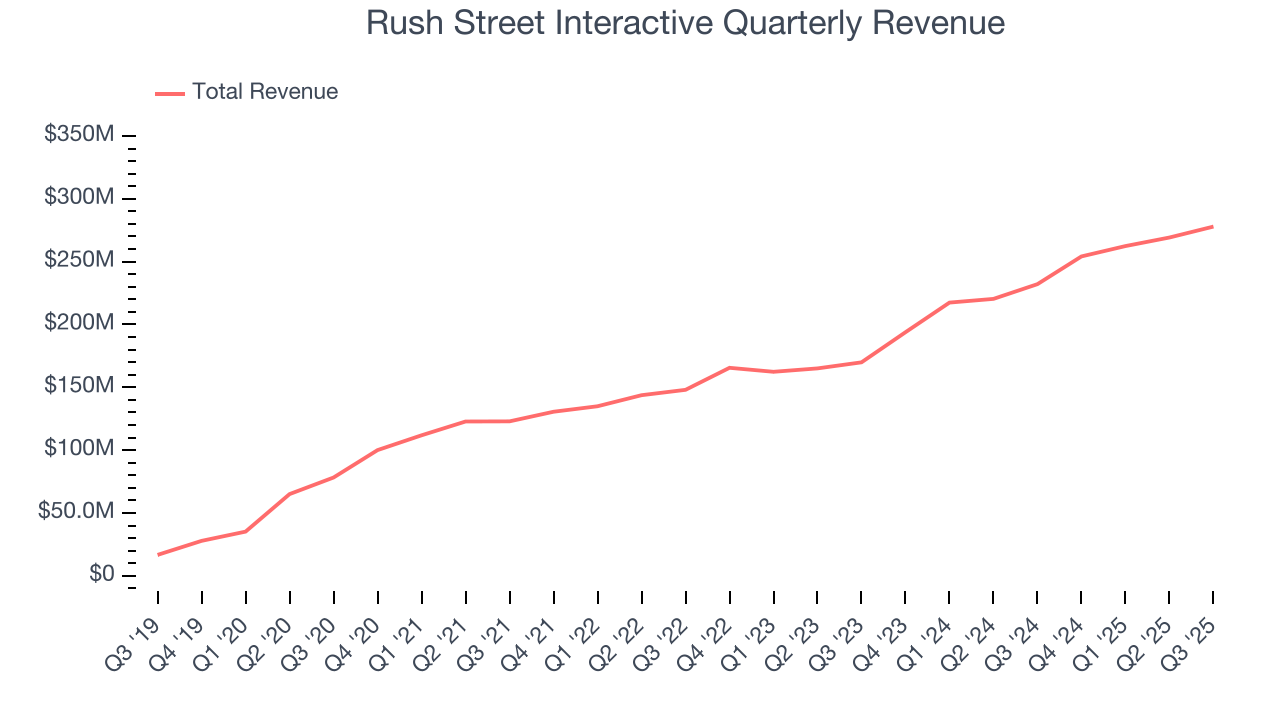

Online casino and sports betting company Rush Street Interactive (NYSE:RSI) announced better-than-expected revenue in Q3 CY2025, with sales up 19.7% year on year to $277.9 million. The company’s full-year revenue guidance of $1.11 billion at the midpoint came in 1.3% above analysts’ estimates. Its non-GAAP profit of $0.09 per share was 24.5% above analysts’ consensus estimates.

Rush Street Interactive (RSI) Q3 CY2025 Highlights:

- Revenue: $277.9 million vs analyst estimates of $266.4 million (19.7% year-on-year growth, 4.3% beat)

- Adjusted EPS: $0.09 vs analyst estimates of $0.07 (24.5% beat)

- Adjusted EBITDA: $36.04 million vs analyst estimates of $31.74 million (13% margin, 13.5% beat)

- The company lifted its revenue guidance for the full year to $1.11 billion at the midpoint from $1.08 billion, a 3.3% increase

- EBITDA guidance for the full year is $150 million at the midpoint, above analyst estimates of $145.6 million

- Operating Margin: 7%, up from 2.8% in the same quarter last year

- Market Capitalization: $1.78 billion

Company Overview

Specializing in online casino gaming and sports betting, Rush Street Interactive (NYSE:RSI) is an operator of digital gaming platforms.

Rush Street Interactive recognized the burgeoning demand for mobile gaming and entered the market in 2012 to address the need for high-quality, user-friendly online games.

Today, the company provides a wide array of online casino games and sports betting options through its digital platforms. This lineup includes slot games, table games, and sportsbooks, appealing to both casual and serious players.

Rush Street Interactive generates revenue by acting as "the house" for its real-money gaming customers. In the company's social gaming business, which doesn't use real money, revenue is derived from in-game purchases for virtual currencies that can be used to play games.

4. Gaming Solutions

Gaming solution companies operate in a dynamic and evolving market, and the digital transformation of the gaming industry presents significant opportunities for innovation and growth, whether it be immersive slot machine terminals or mobile sports betting. However, the gaming solution industry is not without its challenges. Regulatory compliance is a crucial consideration as companies must navigate a complex and often fragmented regulatory landscape across different jurisdictions. Changes in regulations can impact product offerings, operational practices, and market access, requiring companies to maintain flexibility and adaptability in their business strategies. Additionally, the competitive nature of the industry necessitates continuous investment in research and development to stay ahead of competitors and meet evolving consumer demands.

Rush Street Interactive competes with established online-first companies like Flutter Entertainment (FanDuel, PokerStars), DraftKings, BetMGM, Bet365, and Fanatics (PointsBet), as well as traditional casino operators that have moved online, including Penn Entertainment (ESPN Bet), Hard Rock Digital, Caesars Entertainment, and Wynn Resorts (WynnBET).

5. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Thankfully, Rush Street Interactive’s 38.8% annualized revenue growth over the last five years was incredible. Its growth beat the average consumer discretionary company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Rush Street Interactive’s annualized revenue growth of 26.7% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Rush Street Interactive reported year-on-year revenue growth of 19.7%, and its $277.9 million of revenue exceeded Wall Street’s estimates by 4.3%.

Looking ahead, sell-side analysts expect revenue to grow 13.9% over the next 12 months, a deceleration versus the last two years. Still, this projection is above the sector average and implies the market is baking in some success for its newer products and services.

6. Operating Margin

Rush Street Interactive’s operating margin has been trending up over the last 12 months and averaged 4.1% over the last two years. The company’s higher efficiency is a breath of fresh air, but its suboptimal cost structure means it still sports lousy profitability for a consumer discretionary business.

This quarter, Rush Street Interactive generated an operating margin profit margin of 7%, up 4.2 percentage points year on year. This increase was a welcome development and shows it was more efficient.

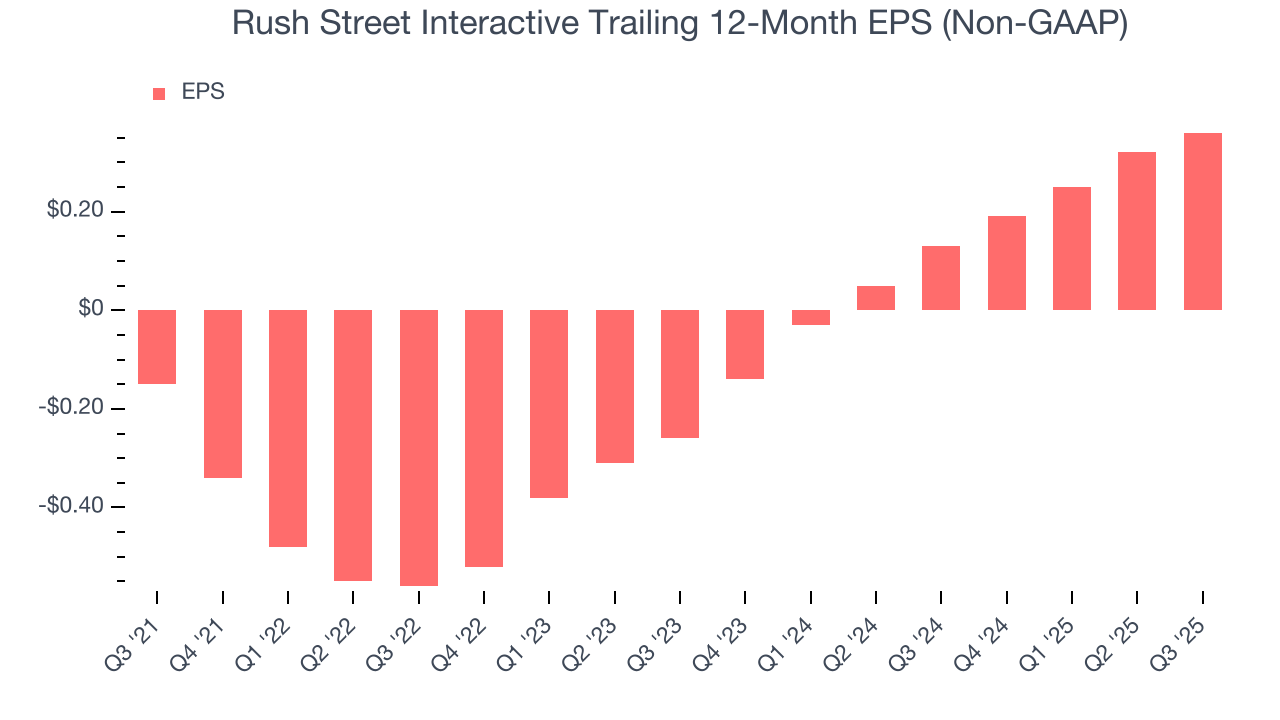

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Rush Street Interactive’s full-year EPS flipped from negative to positive over the last four years. This is encouraging and shows it’s at a critical moment in its life.

In Q3, Rush Street Interactive reported adjusted EPS of $0.09, up from $0.05 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Rush Street Interactive’s full-year EPS of $0.36 to grow 29.2%.

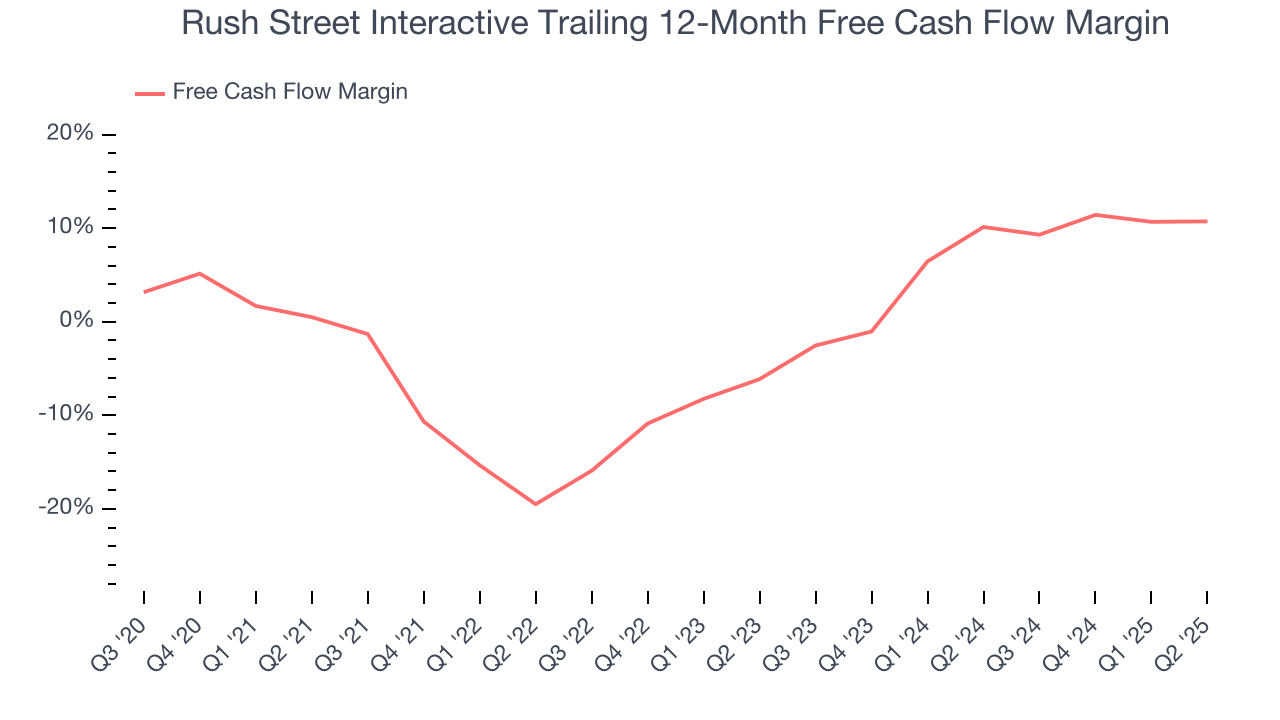

8. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Rush Street Interactive has shown mediocre cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 9.7%, subpar for a consumer discretionary business.

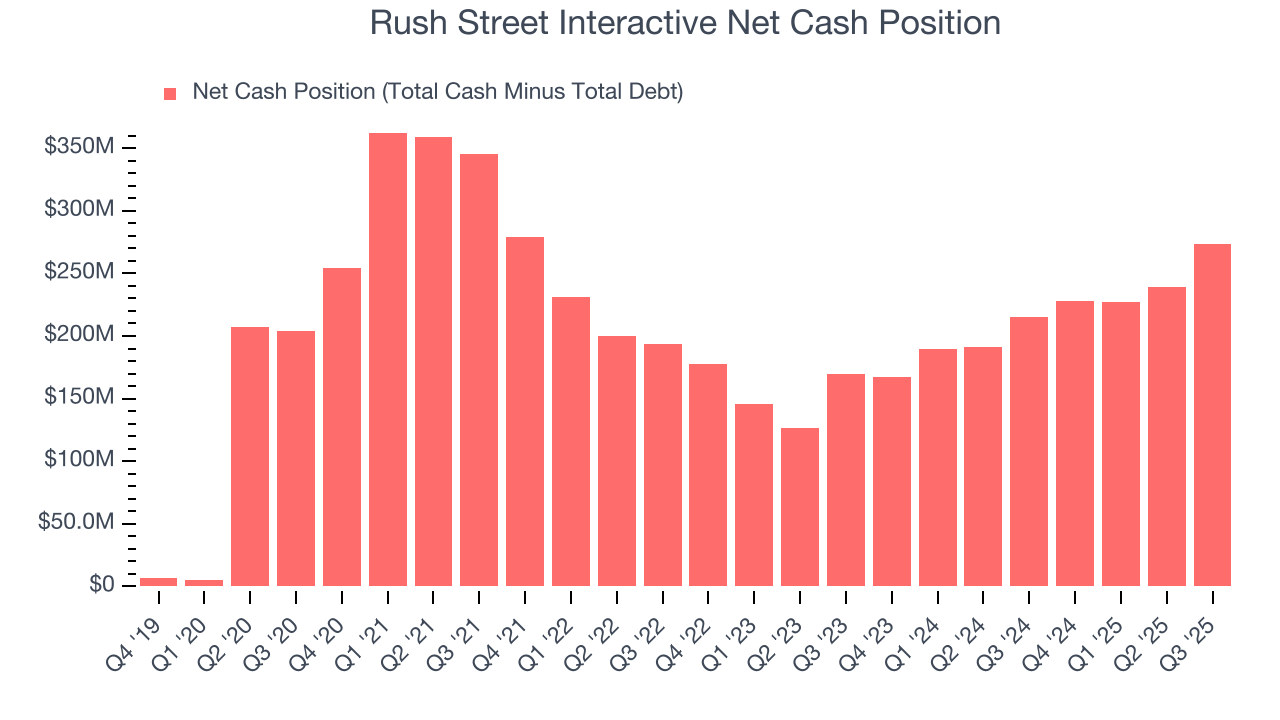

9. Balance Sheet Assessment

Businesses that maintain a cash surplus face reduced bankruptcy risk.

Rush Street Interactive is a profitable, well-capitalized company with $273.5 million of cash and no debt. This position is 16.9% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

10. Key Takeaways from Rush Street Interactive’s Q3 Results

It was good to see Rush Street Interactive beat analysts’ revenue and EPS expectations this quarter. We were also glad its full-year revenue guidance was raised. Overall, we think this was a solid quarter with some key areas of upside. The stock remained flat at $18.18 immediately after reporting.

11. Is Now The Time To Buy Rush Street Interactive?

Updated: January 21, 2026 at 10:04 PM EST

Before making an investment decision, investors should account for Rush Street Interactive’s business fundamentals and valuation in addition to what happened in the latest quarter.

Rush Street Interactive doesn’t pass our quality test. To kick things off, its revenue growth was mediocre over the last five years, and analysts expect its demand to deteriorate over the next 12 months. And while its projected EPS for the next year implies the company will continue generating shareholder value, the downside is its Forecasted free cash flow margin for next year suggests the company will fail to improve its cash conversion. On top of that, its low free cash flow margins give it little breathing room.

Rush Street Interactive’s P/E ratio based on the next 12 months is 36.5x. At this valuation, there’s a lot of good news priced in - you can find more timely opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $23.29 on the company (compared to the current share price of $18.07).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.