Synchrony Financial (SYF)

Not many stocks excite us like Synchrony Financial. Its eye-popping 32.5% annualized EPS growth over the last five years has significantly outpaced its peers.― StockStory Analyst Team

1. News

2. Summary

Why We Like Synchrony Financial

Powering over 73 million active accounts and partnerships with major brands like Amazon, PayPal, and Lowe's, Synchrony Financial (NYSE:SYF) provides credit cards, installment loans, and banking products through partnerships with retailers, healthcare providers, and digital platforms.

- Performance over the past five years shows its incremental sales were extremely profitable, as its annual earnings per share growth of 32.5% outpaced its revenue gains

- Annual tangible book value per share growth of 20.8% over the last two years was superb and indicates its capital strength increased during this cycle

- ROE punches in at 23.1%, illustrating management’s expertise in identifying profitable investments

Synchrony Financial is at the top of our list. The price looks fair based on its quality, and we think now is the time to buy.

Why Is Now The Time To Buy Synchrony Financial?

Synchrony Financial is trading at $77.25 per share, or 8.4x forward P/E. The stock’s multiple sure seems like a bargain relative to its business quality and fundamentals.

Our eyes light up when companies with elite fundamentals trade at bargain prices because shareholders can benefit from both earnings growth and a positive re-rating - a powerful one-two punch.

3. Synchrony Financial (SYF) Research Report: Q4 CY2025 Update

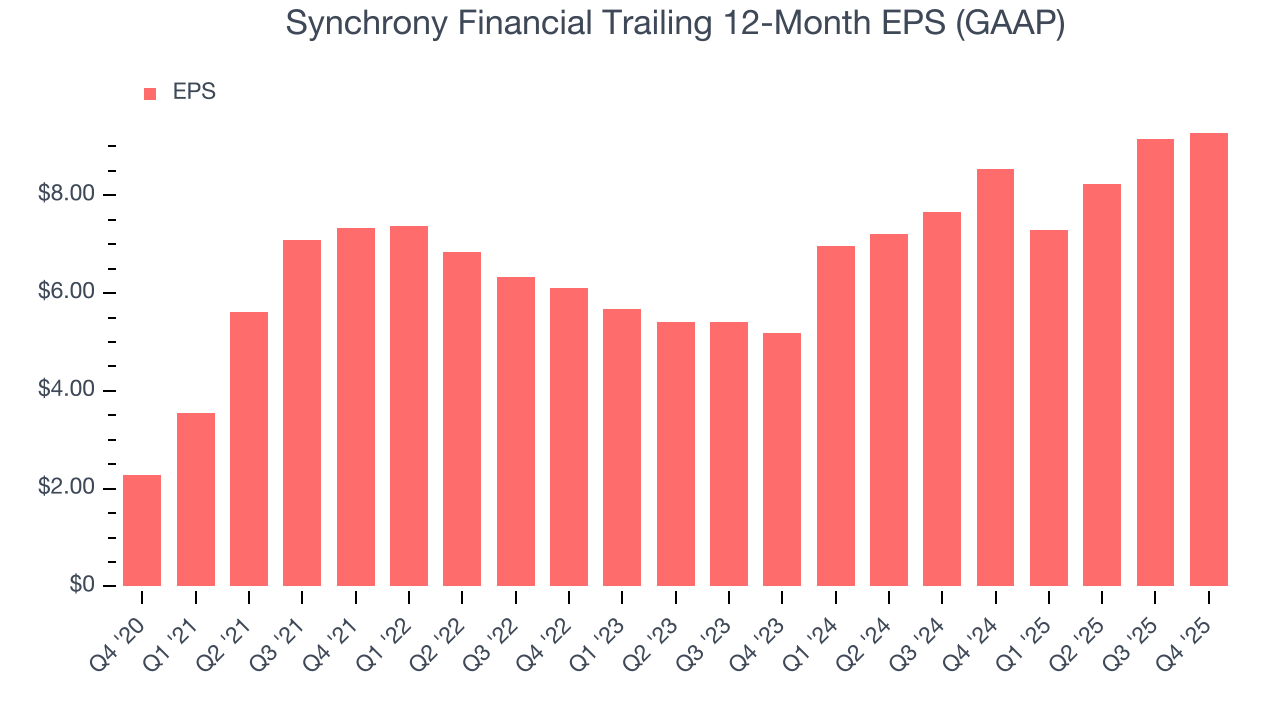

Consumer financial services company Synchrony Financial (NYSE:SYF) missed Wall Street’s revenue expectations in Q4 CY2025, with sales flat year on year at $3.79 billion. Its GAAP profit of $2.04 per share was in line with analysts’ consensus estimates.

Synchrony Financial (SYF) Q4 CY2025 Highlights:

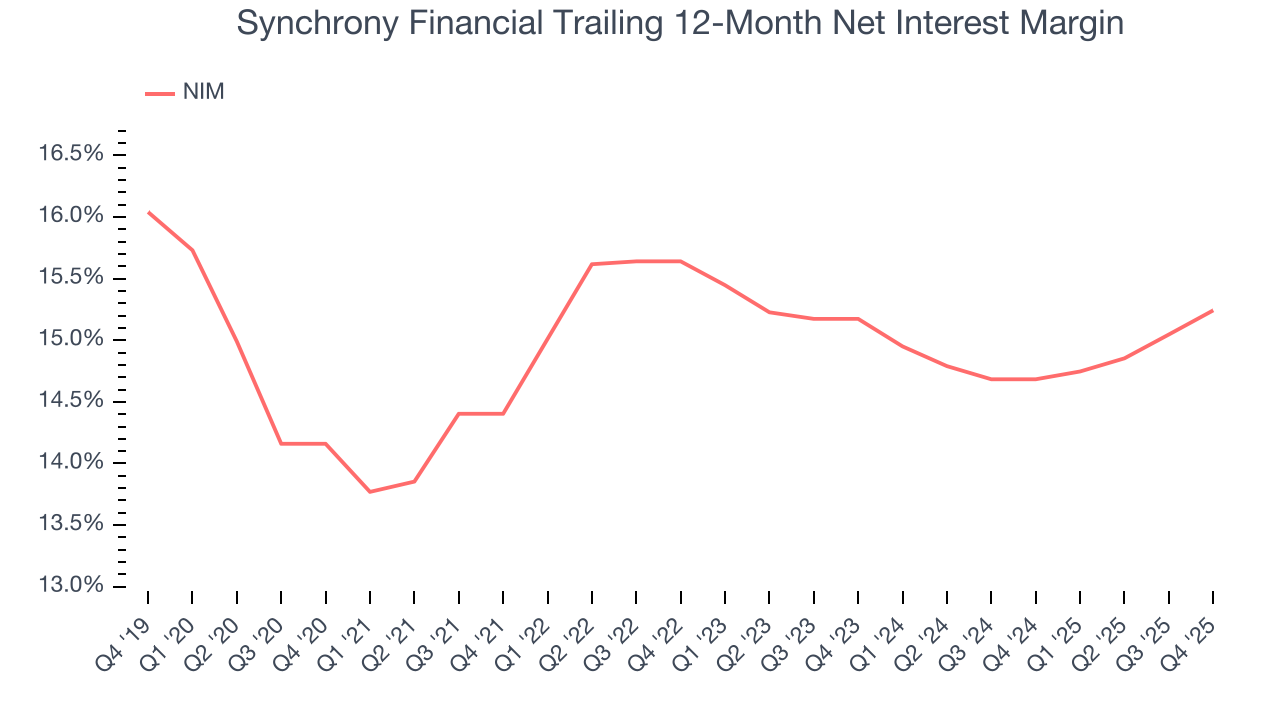

- Net Interest Margin: 15.8% vs analyst estimates of 15.6% (18.2 basis point beat)

- Revenue: $3.79 billion vs analyst estimates of $3.85 billion (flat year on year, 1.5% miss)

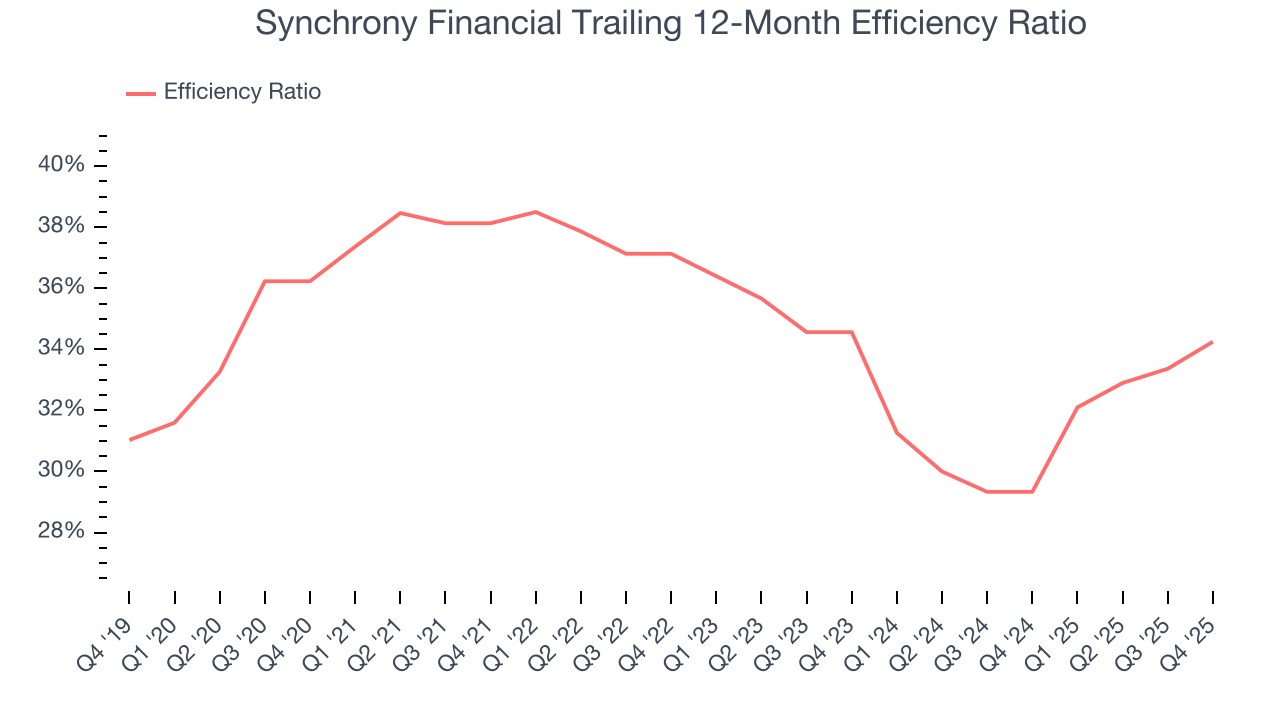

- Efficiency Ratio: 36.9% vs analyst estimates of 32.8% (411.2 basis point miss)

- EPS (GAAP): $2.04 vs analyst estimates of $2.05 (in line)

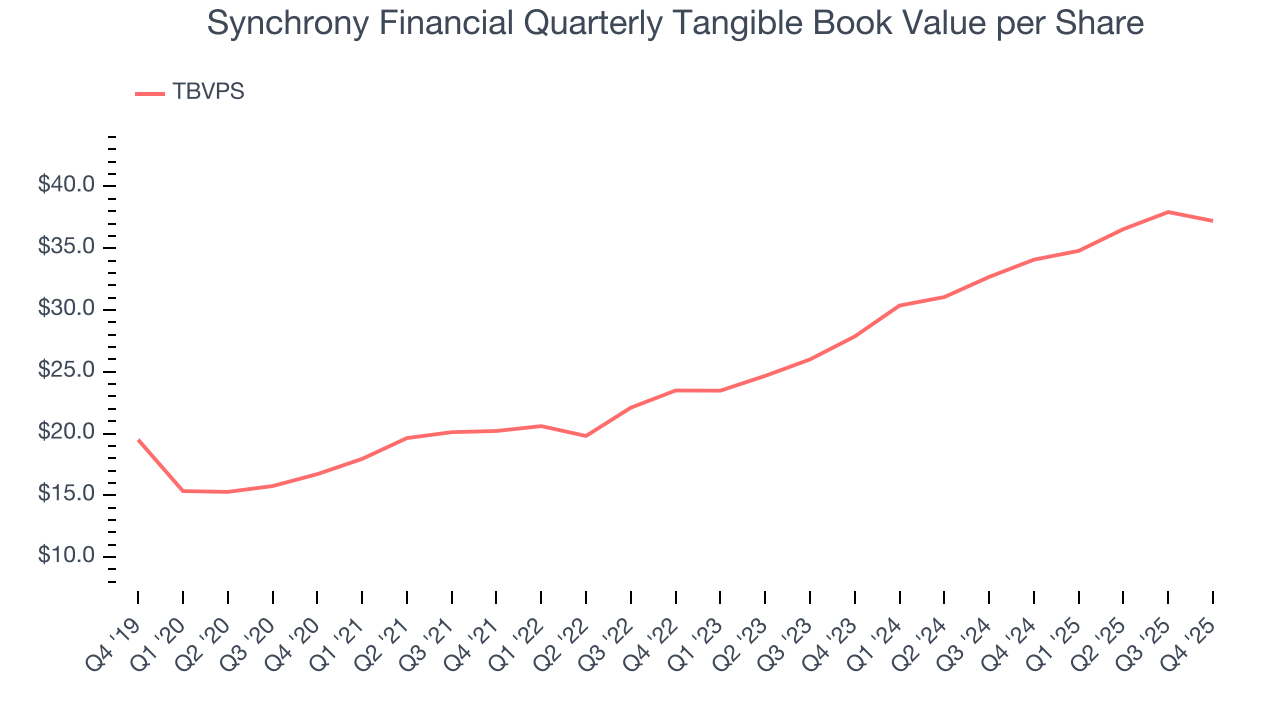

- Tangible Book Value per Share: $37.21 vs analyst estimates of $39.01 (9.2% year-on-year growth, 4.6% miss)

- Market Capitalization: $27.92 billion

Company Overview

Powering over 73 million active accounts and partnerships with major brands like Amazon, PayPal, and Lowe's, Synchrony Financial (NYSE:SYF) provides credit cards, installment loans, and banking products through partnerships with retailers, healthcare providers, and digital platforms.

Synchrony operates through five sales platforms: Home & Auto, Digital, Diversified & Value, Health & Wellness, and Lifestyle. Each platform serves specific industry segments, allowing Synchrony to tailor its credit solutions to particular consumer needs. The company's credit products include private label credit cards that can only be used at specific retailers, dual cards that function as both private label and general purpose credit cards, and installment loans for larger purchases.

The company's business model revolves around establishing long-term partnerships with retailers and service providers. These partners—which include major brands like Lowe's, Amazon, PayPal, Sam's Club, and Walgreens—promote Synchrony's credit products because they help increase sales and strengthen customer loyalty. When consumers use Synchrony's credit products, the company earns interest income from the balances carried on these accounts, as well as fees. For dual cards used outside partner networks, Synchrony also earns interchange fees.

Synchrony's CareCredit platform represents a significant specialized offering, providing healthcare financing through a network of over 270,000 provider locations. This allows patients to finance medical procedures, dental work, veterinary care, and other health-related expenses that may not be fully covered by insurance.

The company also operates a direct banking business, offering FDIC-insured deposit products including certificates of deposit, IRAs, money market accounts, and savings accounts. These deposits provide a stable, low-cost funding source for Synchrony's lending activities. The online banking platform allows Synchrony to expand its deposit base without relying on traditional branch networks.

Synchrony invests heavily in digital capabilities, with approximately 58% of consumer revolving credit applications processed through digital channels. The company's technology infrastructure enables seamless integration with partner systems, allowing for instant credit decisions at the point of sale, both in-store and online.

4. Credit Card

Credit card companies facilitate electronic payments and extend revolving credit to consumers. Growth comes from increasing digital payment adoption, cross-border transaction growth, and value-added services for cardholders and merchants. Challenges include regulatory scrutiny of fees and practices, competition from alternative payment methods, and potential credit losses during economic downturns.

Synchrony's primary competitors include major financial institutions that offer similar credit products, such as American Express, Bread Financial, Capital One, JPMorgan Chase, Citibank, TD Bank, and Wells Fargo. In the direct banking space, Synchrony competes for deposits with traditional banks and online-focused institutions like Ally Financial, Marcus by Goldman Sachs, and Discover.

5. Revenue Growth

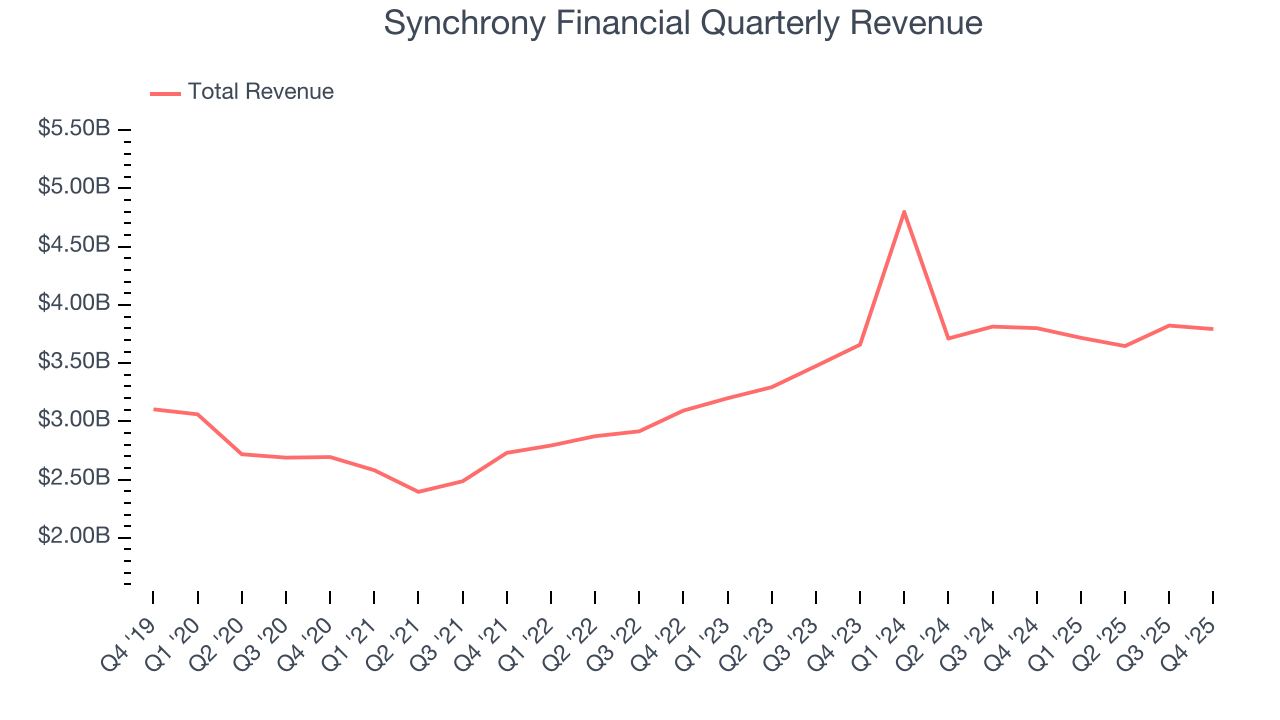

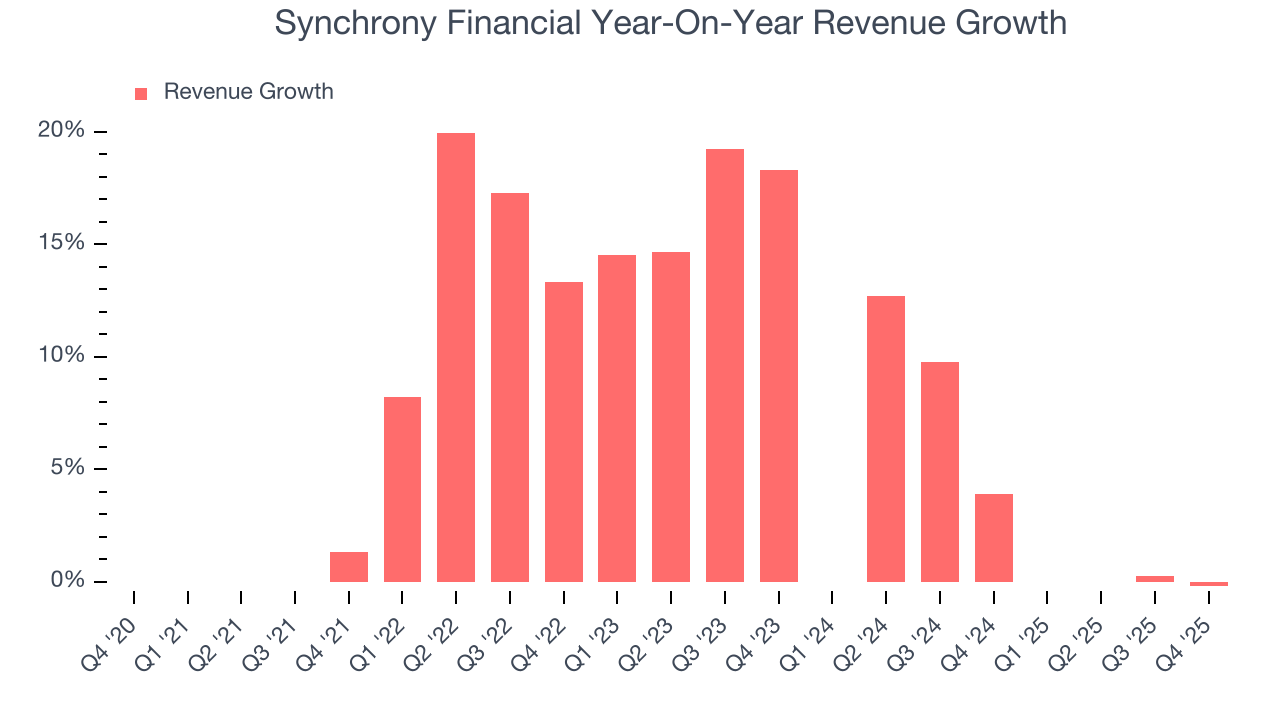

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years. Unfortunately, Synchrony Financial’s 6.1% annualized revenue growth over the last five years was mediocre. This wasn’t a great result compared to the rest of the financials sector, but there are still things to like about Synchrony Financial.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Synchrony Financial’s recent performance shows its demand has slowed as its annualized revenue growth of 4.9% over the last two years was below its five-year trend.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Synchrony Financial missed Wall Street’s estimates and reported a rather uninspiring 0.2% year-on-year revenue decline, generating $3.79 billion of revenue.

6. Net Interest Margin

The net interest margin (NIM) is a key profitability indicator that measures the difference between what a financial institution earns on its loans and what it pays on its deposits. This metric measures how efficiently one can generate income from its core lending activities.

Synchrony Financial’s net interest margin has increased by 108.3 and 6.9 basis points (100 basis points = 1 percentage point) over the last five and two years, respectively. Although the longer-term number is reassuring, the two-year change was worse than the financials industry. The firm’s NIM for the trailing 12 months was 15.2%.

7. Efficiency Ratio

Topline growth is certainly important, but the overall profitability of this growth matters for the bottom line. For Credit Card companies, we look at efficiency ratio, which is non-interest expense (salaries, rent, IT, marketing, excluding interest paid out to depositors) as a percentage of total revenue.

Investors place greater emphasis on efficiency ratio movements than absolute values, understanding that expense structures reflect revenue mix variations. Lower ratios represent better operational performance since they show lenders generating more revenue per dollar of expense.

Over the last five years, Synchrony Financial’s efficiency ratio has swelled by 2 percentage points, going from 38.1% to 34.3%. However, fixed cost leverage was muted more recently as the company’s efficiency ratio was flat on a two-year basis.

In Q4, Synchrony Financial’s efficiency ratio was 36.9%, falling short of analysts’ expectations by 411.2 basis points (100 basis points = 1 percentage point).

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Synchrony Financial’s EPS grew at an astounding 32.5% compounded annual growth rate over the last five years, higher than its 6.1% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Synchrony Financial, its two-year annual EPS growth of 33.9% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q4, Synchrony Financial reported EPS of $2.04, up from $1.91 in the same quarter last year. This print was close to analysts’ estimates. Over the next 12 months, Wall Street expects Synchrony Financial’s full-year EPS of $9.28 to grow 1.5%.

9. Tangible Book Value Per Share (TBVPS)

Financial firms are valued based on their balance sheet strength and ability to compound book value across diverse business lines.

This explains why tangible book value per share (TBVPS) is a premier metric for the sector. TBVPS provides concrete per-share net worth that investors can trust when evaluating companies with complex, multi-faceted business models. Other (and more commonly known) per-share metrics like EPS can sometimes be murky due to the complexity of multiple business lines, M&A activity, or accounting rules that vary across different financial services segments.

Synchrony Financial’s TBVPS grew at an excellent 17.4% annual clip over the last five years. TBVPS growth has recently decelerated a bit to 15.6% annual growth over the last two years (from $27.86 to $37.21 per share).

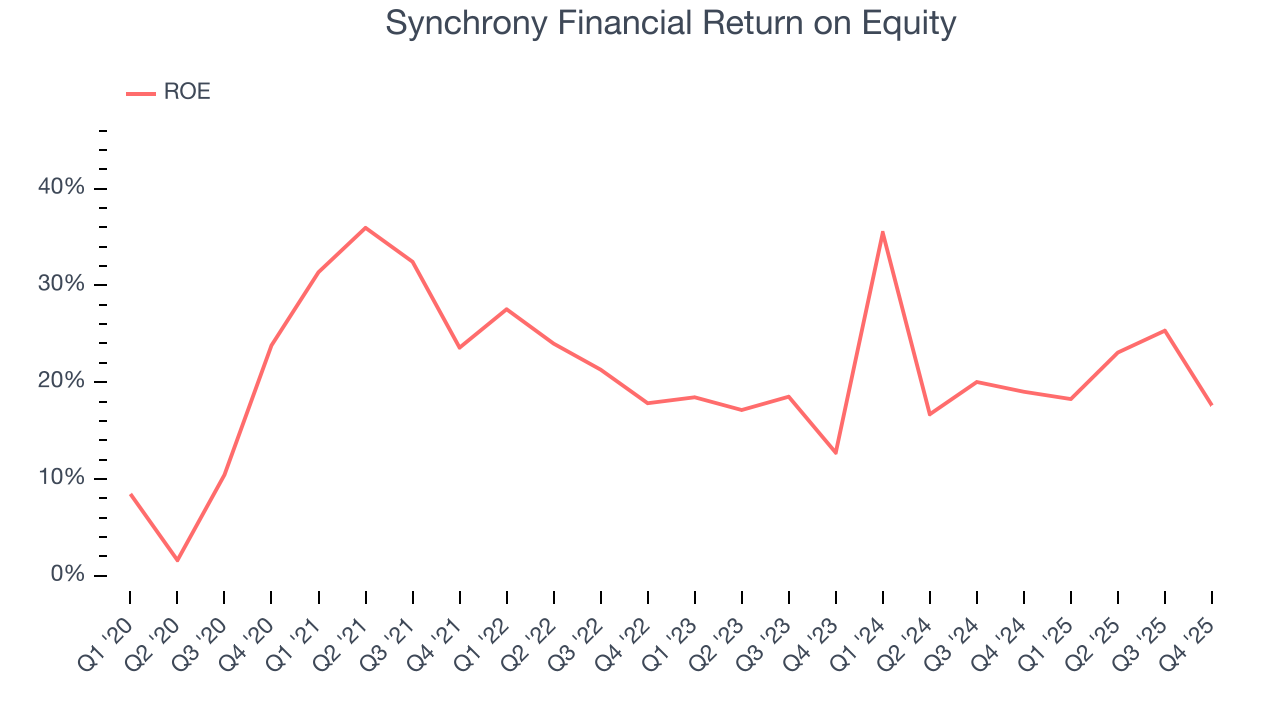

10. Return on Equity

Return on equity, or ROE, quantifies bank profitability relative to shareholder equity - an essential capital source for these institutions. Over extended periods, superior ROE performance drives faster shareholder wealth compounding through reinvestment, share repurchases, and dividend growth.

Over the last five years, Synchrony Financial has averaged an ROE of 22.8%, exceptional for a company operating in a sector where the average shakes out around 10% and those putting up 25%+ are greatly admired. This shows Synchrony Financial has a strong competitive moat.

11. Balance Sheet Assessment

The debt-to-equity ratio is a widely used measure to assess a company's balance sheet health. A higher ratio means that a business aggressively financed its growth with debt. This can result in higher earnings (if the borrowed funds are invested profitably) but also increases risk.

If debt levels are too high, there could be difficulties in meeting obligations, especially during economic downturns or periods of rising interest rates if the debt has variable-rate payments.

Synchrony Financial has no debt, so leverage is not an issue here.

12. Key Takeaways from Synchrony Financial’s Q4 Results

We were impressed by how significantly Synchrony Financial blew past analysts’ net interest margin expectations this quarter. On the other hand, its revenue slightly missed and efficiency ratio came in below expectations (lower is better). Overall, this was a weaker quarter. The stock traded down 2% to $75.99 immediately following the results.

13. Is Now The Time To Buy Synchrony Financial?

Updated: January 27, 2026 at 6:27 AM EST

When considering an investment in Synchrony Financial, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

There are multiple reasons why we think Synchrony Financial is an elite financials company. Although its revenue growth was mediocre over the last five years with analysts expecting growth to slow even further from here, its astounding EPS growth over the last five years shows its profits are trickling down to shareholders. On top of that, Synchrony Financial’s expanding net interest margin shows its loan book is becoming more profitable.

Synchrony Financial’s P/E ratio based on the next 12 months is 8.2x. Looking at the financials space today, Synchrony Financial’s qualities as one of the best businesses really stand out, and we’re pounding the table at this bargain price.

Wall Street analysts have a consensus one-year price target of $92.61 on the company (compared to the current share price of $75.99), implying they see 21.9% upside in buying Synchrony Financial in the short term.