Trane Technologies (TT)

We see solid potential in Trane Technologies. Its combination of extraordinary growth and robust profitability makes it a beloved asset.― StockStory Analyst Team

1. News

2. Summary

Why We Like Trane Technologies

With low-pressure heating systems as its first product, Trane (NYSE:TT) designs, manufactures, and sells HVAC and refrigeration systems, the former to commercial and residential building customers and the latter to commercial truck manufacturers.

- Earnings per share grew by 21.6% annually over the last five years and trumped its peers

- ROIC punches in at 24.3%, illustrating management’s expertise in identifying profitable investments, and its returns are climbing as it finds even more attractive growth opportunities

- Excellent operating margin highlights the strength of its business model, and it turbocharged its profits by achieving some fixed cost leverage

We have an affinity for Trane Technologies. The price seems fair in light of its quality, so this could be a good time to invest in some shares.

Why Is Now The Time To Buy Trane Technologies?

At $385.75 per share, Trane Technologies trades at 27.5x forward P/E. Valuation is above that of many industrials companies, but we think the price is justified given its business fundamentals.

Entry price certainly impacts returns, but over a long-term, multi-year period, business quality matters much more than where you buy a stock.

3. Trane Technologies (TT) Research Report: Q4 CY2025 Update

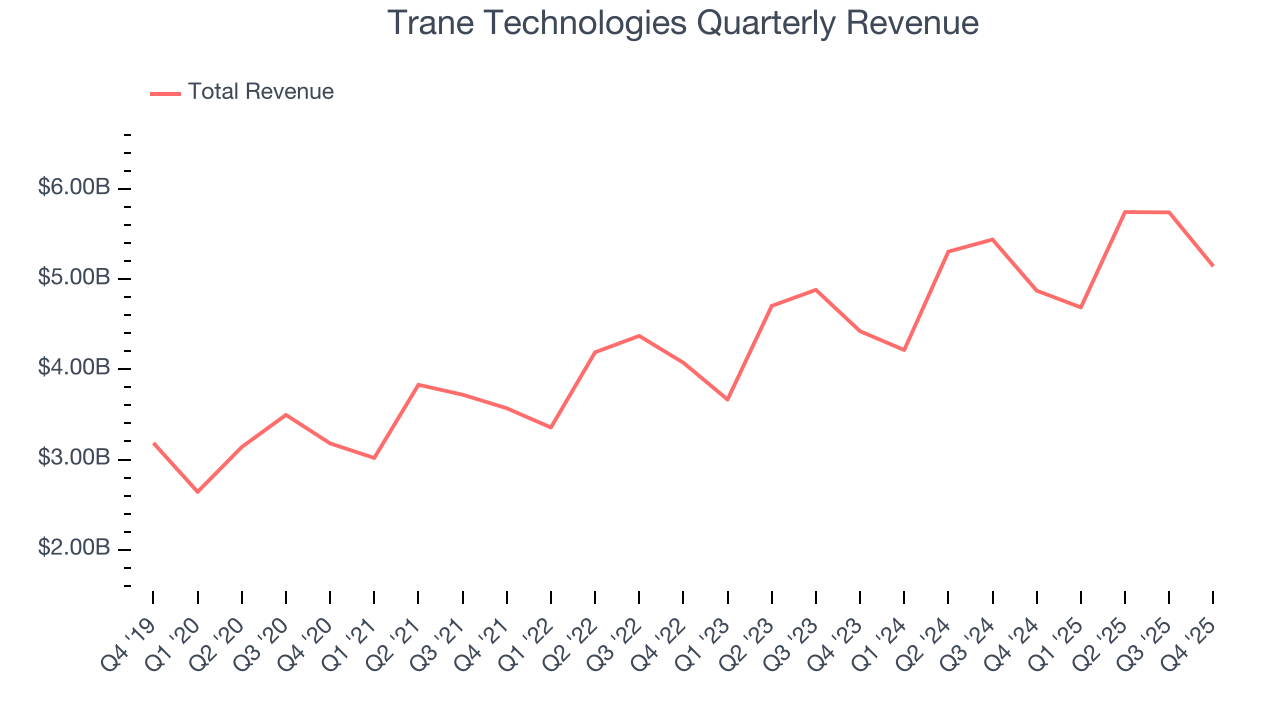

HVAC company Trane (NYSE:TT) reported revenue ahead of Wall Streets expectations in Q4 CY2025, with sales up 5.5% year on year to $5.14 billion. Its non-GAAP profit of $2.86 per share was 1.6% above analysts’ consensus estimates.

Trane Technologies (TT) Q4 CY2025 Highlights:

- Revenue: $5.14 billion vs analyst estimates of $5.11 billion (5.5% year-on-year growth, 0.8% beat)

- Adjusted EPS: $2.86 vs analyst estimates of $2.81 (1.6% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $14.75 at the midpoint, in line with analyst estimates

- Operating Margin: 15.9%, in line with the same quarter last year

- Free Cash Flow Margin: 20.1%, up from 15.9% in the same quarter last year

- Backlog: $7.8 billion at quarter end

- Market Capitalization: $87.41 billion

Company Overview

With low-pressure heating systems as its first product, Trane (NYSE:TT) designs, manufactures, and sells HVAC and refrigeration systems, the former to commercial and residential building customers and the latter to commercial truck manufacturers.

The company traces its origins back to the late 1800s as a family plumbing business. Trane as we know it today was later incorporated in 1913 after that first product and subsequently continued to launch products, like Turbovac, a type of water chiller that fundamentally altered the industry’s approach to large-building air conditioning systems.

Today's product portfolio includes air conditioners, furnaces, heat pumps, and thermal energy storage solutions. In addition to reliability of its products and systems, Trane also aims to facilitate energy efficiency for its customers, which is an increasingly important area of focus in fast-growing end markets like datacenters.

Trane's customers include commercial building owners and operators, industrial facilities such as production plants, and retailers such as grocery stores. Over the years, the company has increased its revenue from services such as repair, maintenance, and energy management programs. This gives Trane a growing base of steadier, recurring revenues that are less subject to macro swings.

4. HVAC and Water Systems

Many HVAC and water systems companies sell essential, non-discretionary infrastructure for buildings. Since the useful lives of these water heaters and vents are fairly standard, these companies have a portion of predictable replacement revenue. In the last decade, trends in energy efficiency and clean water are driving innovation that is leading to incremental demand. On the other hand, new installations for these companies are at the whim of residential and commercial construction volumes, which tend to be cyclical and can be impacted heavily by economic factors such as interest rates.

Competitors in the commercial HVAC space include Carrier Global (NYSE:CARR), Lennox International (NYSE:LII), and Japanese company Daikin (TSE:6367), which also owns the Goodman brand.

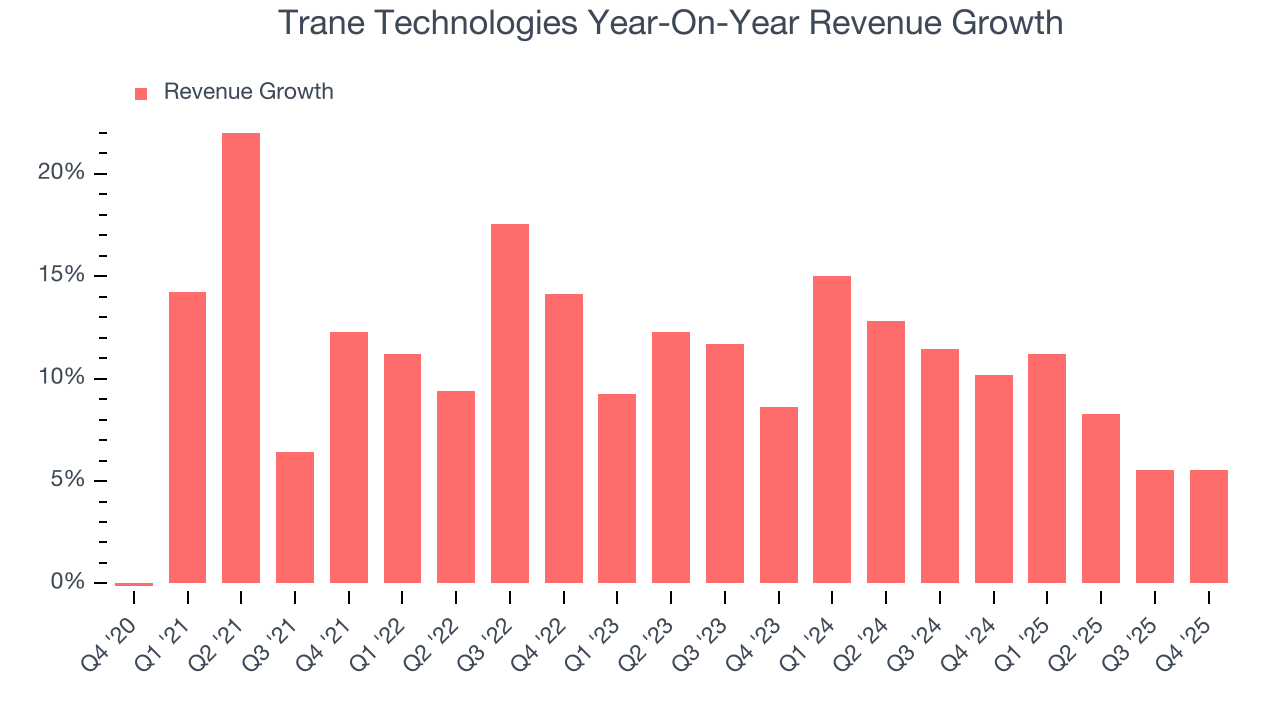

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Trane Technologies grew its sales at an impressive 11.4% compounded annual growth rate. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Trane Technologies’s annualized revenue growth of 9.8% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Trane Technologies reported year-on-year revenue growth of 5.5%, and its $5.14 billion of revenue exceeded Wall Street’s estimates by 0.8%.

Looking ahead, sell-side analysts expect revenue to grow 7.2% over the next 12 months, a slight deceleration versus the last two years. This projection is underwhelming and indicates its products and services will see some demand headwinds. At least the company is tracking well in other measures of financial health.

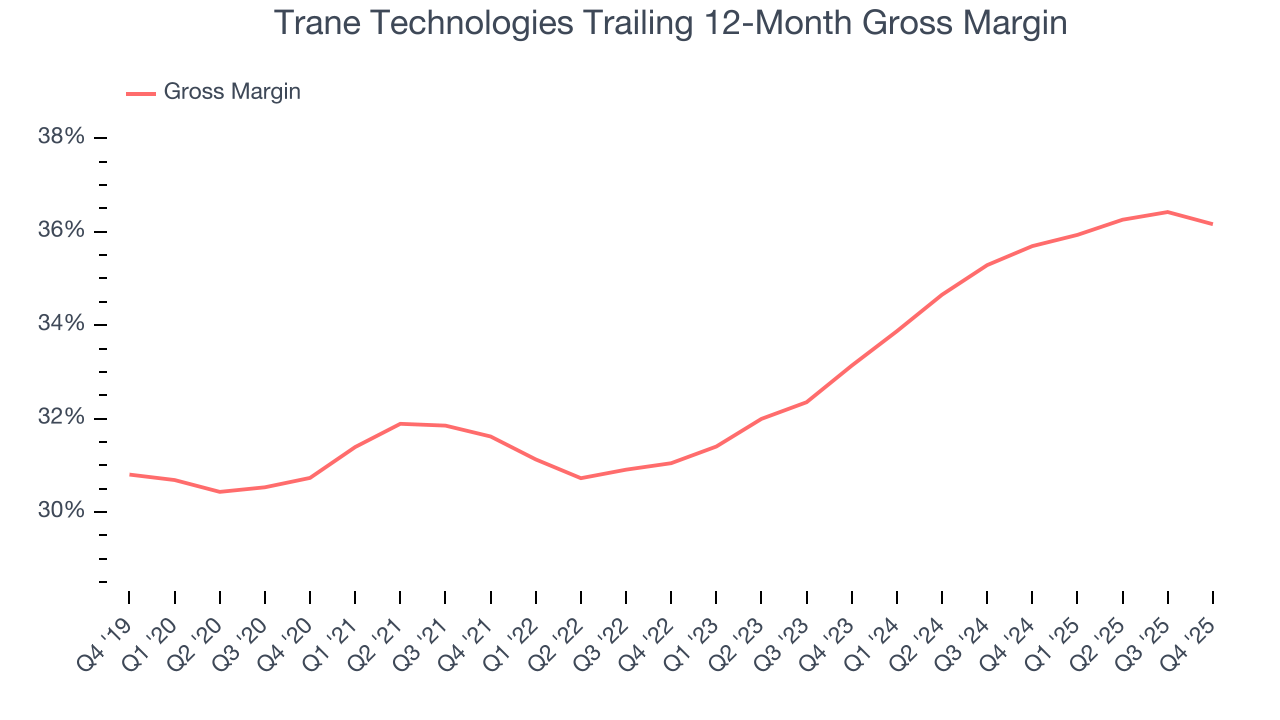

6. Gross Margin & Pricing Power

Gross profit margin is a critical metric to track because it sheds light on its pricing power, complexity of products, and ability to procure raw materials, equipment, and labor.

Trane Technologies’s gross margin is good compared to other industrials businesses and signals it sells differentiated products, not commodities. As you can see below, it averaged an impressive 33.8% gross margin over the last five years. Said differently, Trane Technologies paid its suppliers $66.19 for every $100 in revenue.

This quarter, Trane Technologies’s gross profit margin was 34.1%, marking a 1 percentage point decrease from 35.1% in the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

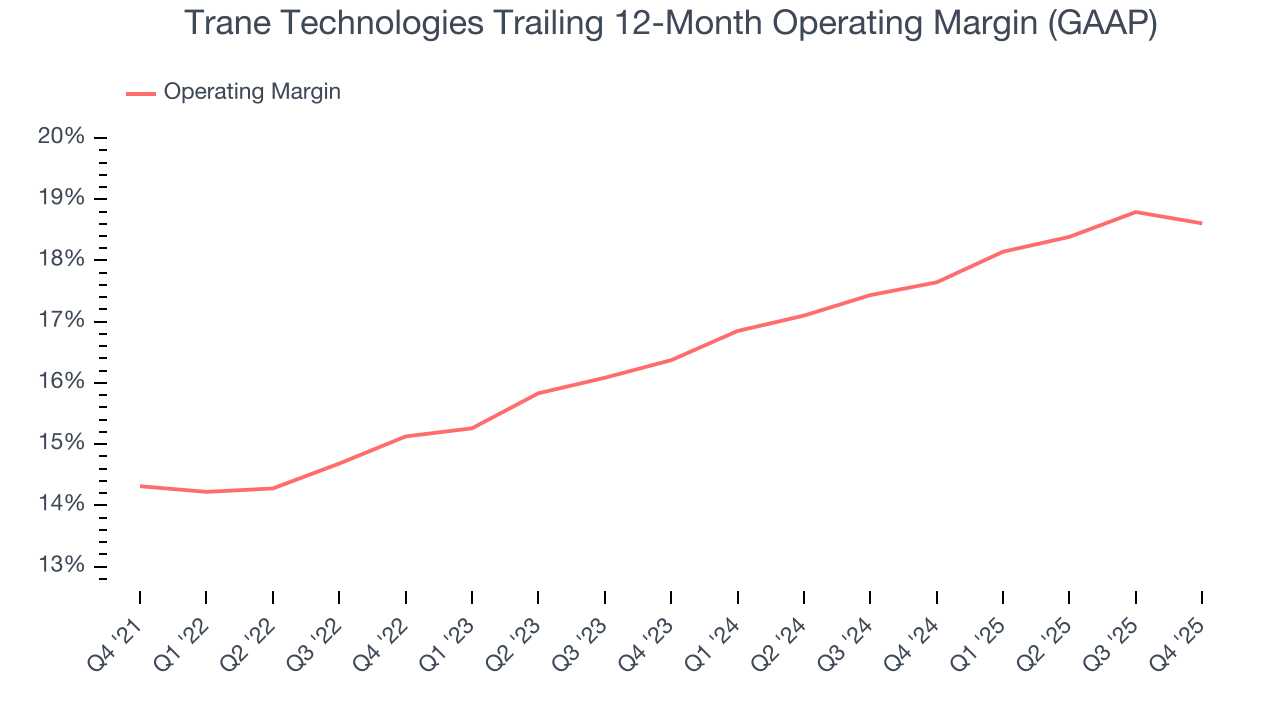

7. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Trane Technologies has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 16.6%. This result isn’t too surprising as its gross margin gives it a favorable starting point.

Looking at the trend in its profitability, Trane Technologies’s operating margin rose by 4.3 percentage points over the last five years, as its sales growth gave it operating leverage.

This quarter, Trane Technologies generated an operating margin profit margin of 15.9%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

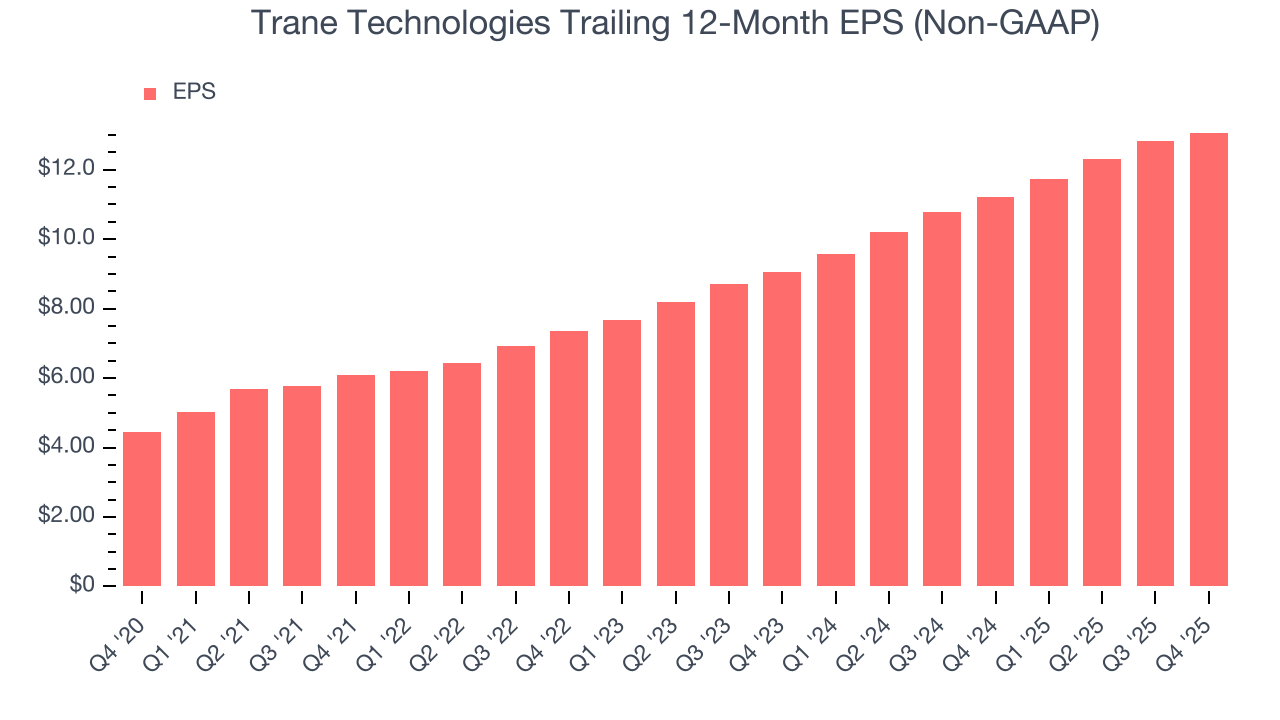

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Trane Technologies’s EPS grew at an astounding 24% compounded annual growth rate over the last five years, higher than its 11.4% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

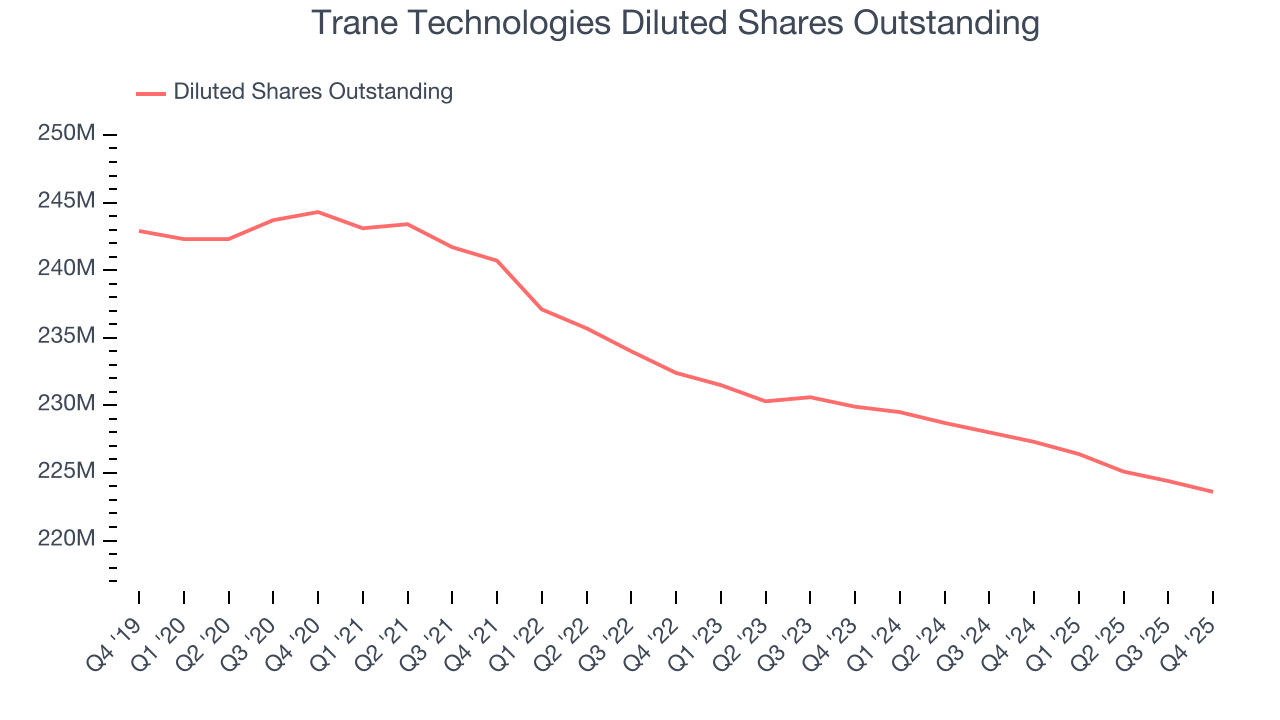

We can take a deeper look into Trane Technologies’s earnings quality to better understand the drivers of its performance. As we mentioned earlier, Trane Technologies’s operating margin was flat this quarter but expanded by 4.3 percentage points over the last five years. On top of that, its share count shrank by 8.5%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Trane Technologies, its two-year annual EPS growth of 20.2% was lower than its five-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q4, Trane Technologies reported adjusted EPS of $2.86, up from $2.61 in the same quarter last year. This print beat analysts’ estimates by 1.6%. Over the next 12 months, Wall Street expects Trane Technologies’s full-year EPS of $13.07 to grow 13.1%.

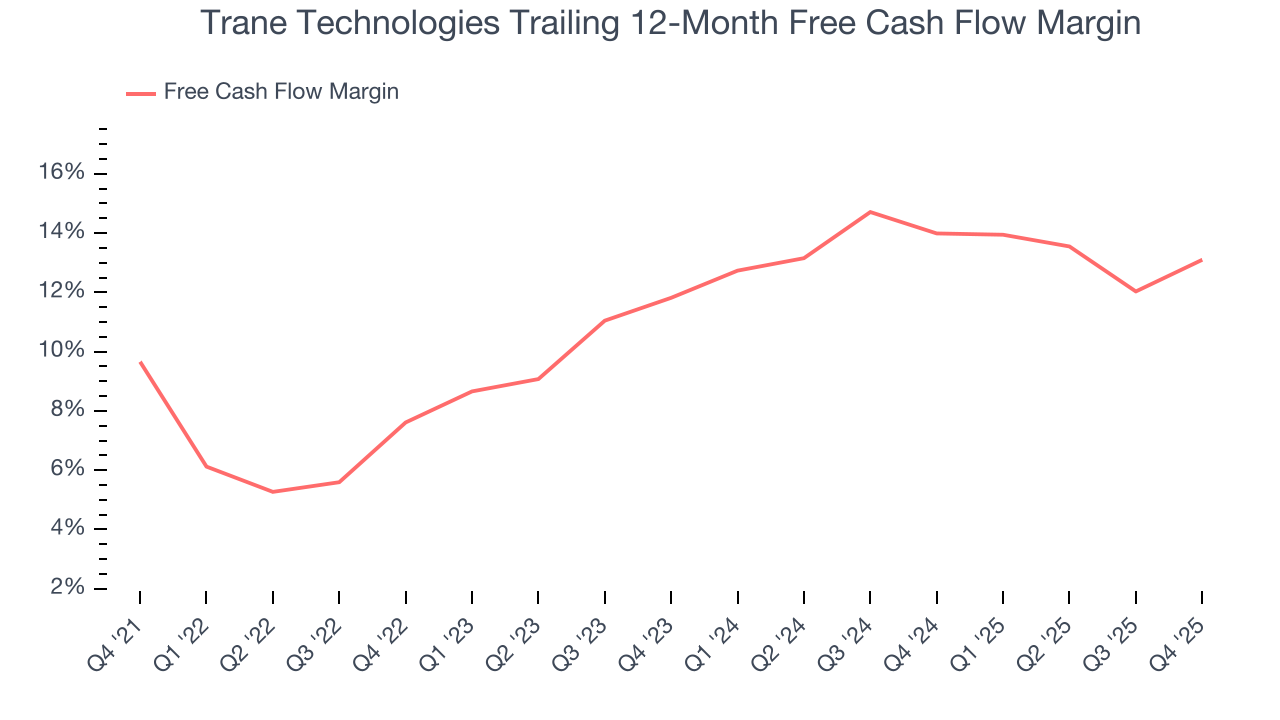

9. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Trane Technologies has shown robust cash profitability, enabling it to comfortably ride out cyclical downturns while investing in plenty of new offerings and returning capital to investors. The company’s free cash flow margin averaged 11.5% over the last five years, quite impressive for an industrials business.

Taking a step back, we can see that Trane Technologies’s margin expanded by 3.4 percentage points during that time. This is encouraging because it gives the company more optionality.

Trane Technologies’s free cash flow clocked in at $1.03 billion in Q4, equivalent to a 20.1% margin. This result was good as its margin was 4.2 percentage points higher than in the same quarter last year, building on its favorable historical trend.

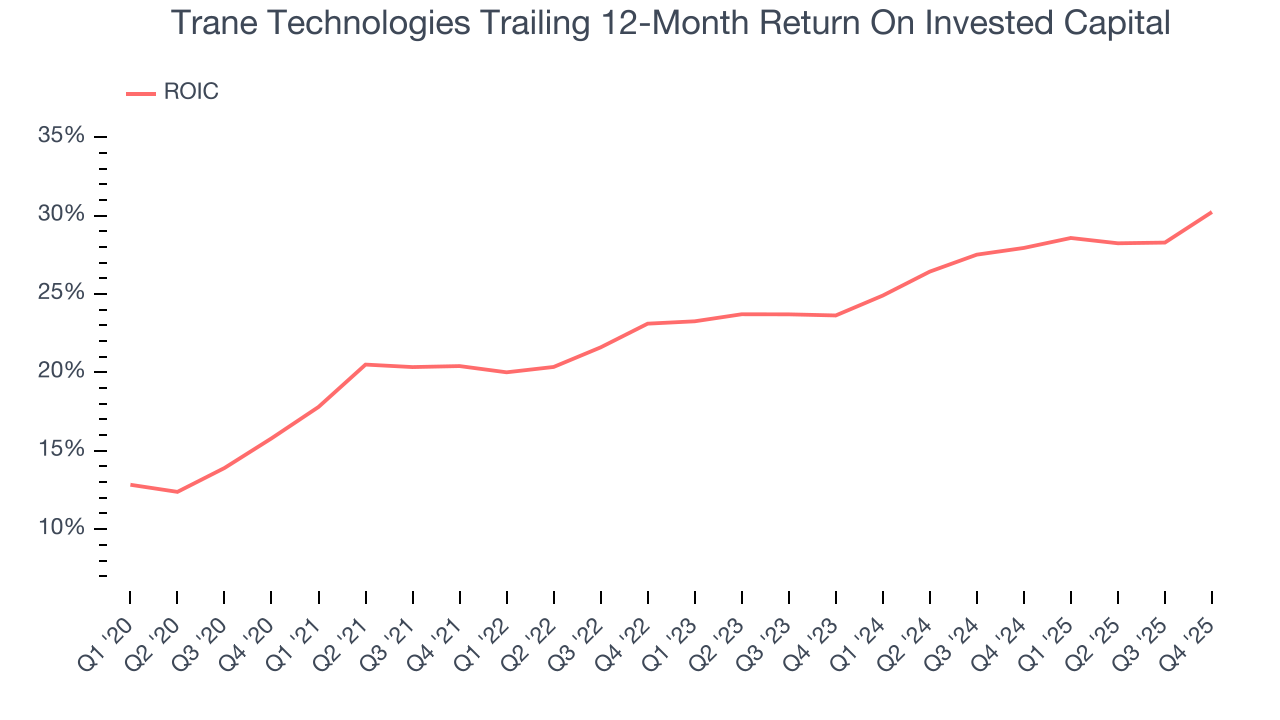

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Trane Technologies’s five-year average ROIC was 25.1%, placing it among the best industrials companies. This illustrates its management team’s ability to invest in highly profitable ventures and produce tangible results for shareholders.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Fortunately, Trane Technologies’s has increased over the last few years. This is a great sign when paired with its already strong returns. It could suggest its competitive advantage or profitable growth opportunities are expanding.

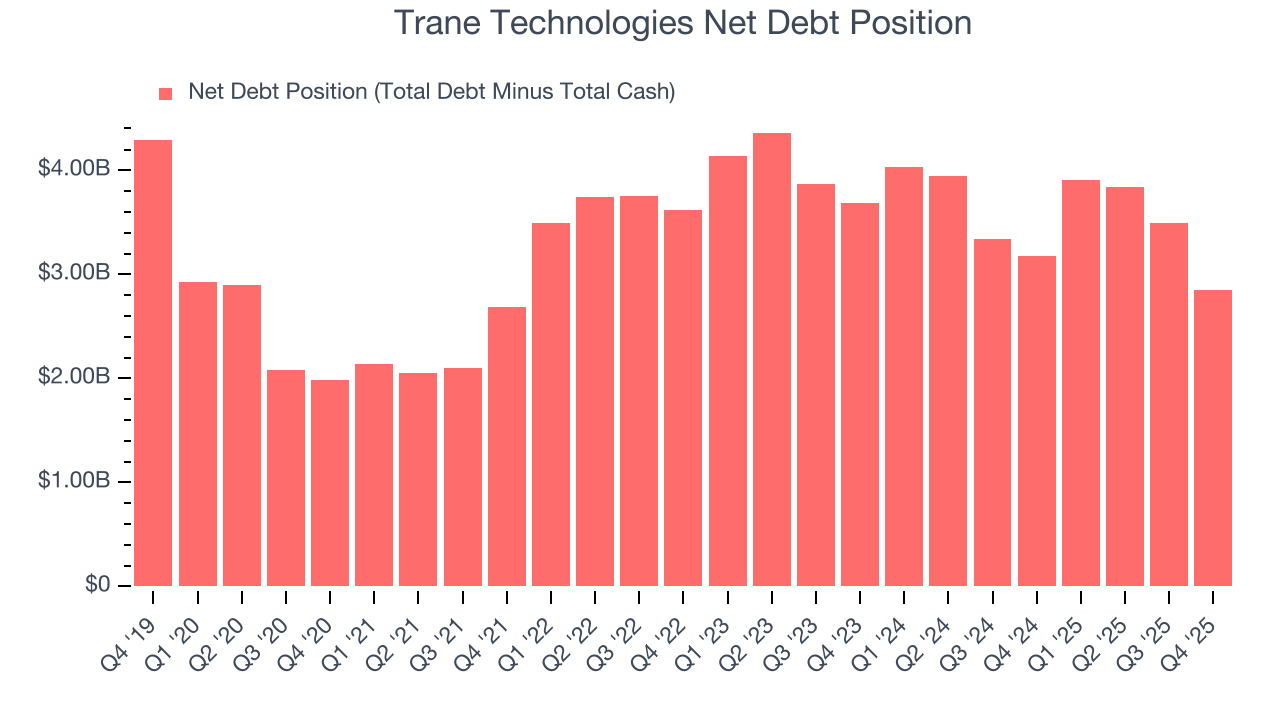

11. Balance Sheet Assessment

Trane Technologies reported $1.76 billion of cash and $4.62 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $4.28 billion of EBITDA over the last 12 months, we view Trane Technologies’s 0.7× net-debt-to-EBITDA ratio as safe. We also see its $222.2 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Trane Technologies’s Q4 Results

It was good to see Trane Technologies narrowly top analysts’ revenue expectations this quarter. EPS also beat, but EPS guidance for the upcoming fiscal year was just in line. Overall, we still think this quarter was decent. The stock remained flat at $397.50 immediately after reporting.

13. Is Now The Time To Buy Trane Technologies?

Updated: January 29, 2026 at 6:35 AM EST

Are you wondering whether to buy Trane Technologies or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

There are multiple reasons why we think Trane Technologies is an elite industrials company. First of all, the company’s revenue growth was impressive over the last five years. On top of that, its astounding EPS growth over the last five years shows its profits are trickling down to shareholders, and its stellar ROIC suggests it has been a well-run company historically.

Trane Technologies’s P/E ratio based on the next 12 months is 26.7x. Analyzing the industrials landscape today, Trane Technologies’s positive attributes shine bright. We think it’s one of the best businesses in our coverage and like the stock at this price.

Wall Street analysts have a consensus one-year price target of $476.52 on the company (compared to the current share price of $397.50), implying they see 19.9% upside in buying Trane Technologies in the short term.