United Natural Foods (UNFI)

United Natural Foods faces an uphill battle. Its sales have underperformed and its low returns on capital show it has few growth opportunities.― StockStory Analyst Team

1. News

2. Summary

Why We Think United Natural Foods Will Underperform

With a vast network of 55 distribution centers spanning approximately 30 million square feet of warehouse space, United Natural Foods (NYSE:UNFI) is North America's premier grocery wholesaler distributing natural, organic, and conventional products to over 30,000 retail locations across the US and Canada.

- Gross margin of 13.4% is an output of its commoditized products

- Earnings per share fell by 29.3% annually over the last three years while its revenue grew, showing its incremental sales were much less profitable

- 5× net-debt-to-EBITDA ratio makes lenders less willing to extend additional capital, potentially necessitating dilutive equity offerings

United Natural Foods doesn’t meet our quality criteria. We see more lucrative opportunities elsewhere.

Why There Are Better Opportunities Than United Natural Foods

At $40.50 per share, United Natural Foods trades at 13.2x forward P/E. Yes, this valuation multiple is lower than that of other consumer staples peers, but we’ll remind you that you often get what you pay for.

Cheap stocks can look like great bargains at first glance, but you often get what you pay for. These mediocre businesses often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. United Natural Foods (UNFI) Research Report: Q4 CY2025 Update

Food distribution company United Natural Foods (NYSE:UNFI) fell short of the market’s revenue expectations in Q4 CY2025, with sales falling 2.6% year on year to $7.95 billion. The company’s full-year revenue guidance of $31.2 billion at the midpoint came in 2.3% below analysts’ estimates. Its non-GAAP profit of $0.62 per share was 22.7% above analysts’ consensus estimates.

United Natural Foods (UNFI) Q4 CY2025 Highlights:

- Revenue: $7.95 billion vs analyst estimates of $8.11 billion (2.6% year-on-year decline, 2% miss)

- Adjusted EPS: $0.62 vs analyst estimates of $0.51 (22.7% beat)

- Adjusted EBITDA: $179 million vs analyst estimates of $167.2 million (2.3% margin, 7% beat)

- The company dropped its revenue guidance for the full year to $31.2 billion at the midpoint from $31.8 billion, a 1.9% decrease

- EBITDA guidance for the full year is $695 million at the midpoint, above analyst estimates of $674.6 million

- Operating Margin: 0.7%, in line with the same quarter last year

- Free Cash Flow Margin: 3.1%, similar to the same quarter last year

- Market Capitalization: $2.37 billion

Company Overview

With a vast network of 55 distribution centers spanning approximately 30 million square feet of warehouse space, United Natural Foods (NYSE:UNFI) is North America's premier grocery wholesaler distributing natural, organic, and conventional products to over 30,000 retail locations across the US and Canada.

UNFI serves as a critical link in the food supply chain, offering approximately 230,000 products across diverse categories including grocery items, perishables, frozen foods, wellness products, and bulk goods. The company operates through three segments: Natural (distributing organic and specialty items), Conventional (handling mainstream grocery products), and Retail (operating 75 Cub Foods and Shoppers grocery stores).

Beyond distribution, UNFI provides retailers with an array of services to enhance their competitiveness, including shelf management, store design, electronic payment processing, marketing programs, and data analytics. The company also maintains a portfolio of private label brands such as ESSENTIAL EVERYDAY, WILD HARVEST, and WOODSTOCK, offering customers national brand equivalent products at competitive prices.

UNFI's sophisticated logistics network employs advanced technology including radio-frequency devices, automated order selection, and transportation management systems that optimize delivery routes. The company also operates Marketplace by UNFI, a business-to-business digital platform connecting emerging brands with retailers. Through its Woodstock Farms Manufacturing subsidiary, UNFI produces nuts, dried fruits, seeds, and other natural snacks in its organic-certified facility in New Jersey.

4. Perishable Food

The perishable food industry is diverse, encompassing large-scale producers and distributors to specialty and artisanal brands. These companies sell produce, dairy products, meats, and baked goods and have become integral to serving modern American consumers who prioritize freshness, quality, and nutritional value. Investing in perishable food stocks presents both opportunities and challenges. While the perishable nature of products can introduce risks related to supply chain management and shelf life, it also creates a constant demand driven by the necessity for fresh food. Companies that can efficiently manage inventory, distribution, and quality control are well-positioned to thrive in this competitive market. Navigating the perishable food industry requires adherence to strict food safety standards, regulations, and labeling requirements.

UNFI competes with other major food distributors including Sysco Corporation (NYSE:SYY), Performance Food Group (NYSE:PFGC), C&S Wholesale Grocers (privately held), and KeHE Distributors (privately held), which also serve various segments of the grocery retail industry.

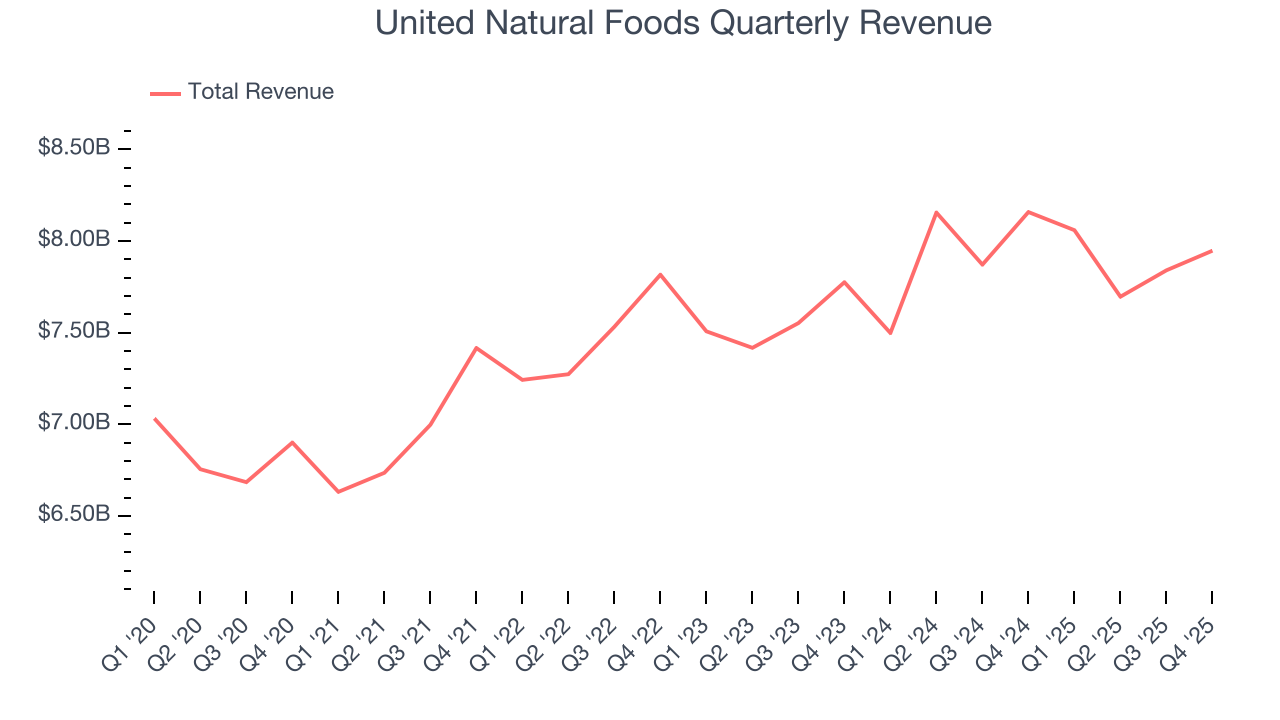

5. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $31.54 billion in revenue over the past 12 months, United Natural Foods is one of the most widely recognized consumer staples companies. Its influence over consumers gives it negotiating leverage with distributors, enabling it to pick and choose where it sells its products (a luxury many don’t have). However, its scale is a double-edged sword because it’s harder to find incremental growth when your existing brands have penetrated most of the market. For United Natural Foods to boost its sales, it likely needs to adjust its prices, launch new offerings, or lean into foreign markets.

As you can see below, United Natural Foods’s 1.8% annualized revenue growth over the last three years was sluggish. This shows it failed to generate demand in any major way and is a rough starting point for our analysis.

This quarter, United Natural Foods missed Wall Street’s estimates and reported a rather uninspiring 2.6% year-on-year revenue decline, generating $7.95 billion of revenue.

Looking ahead, sell-side analysts expect revenue to grow 1.9% over the next 12 months, similar to its three-year rate. This projection doesn't excite us and indicates its newer products will not lead to better top-line performance yet.

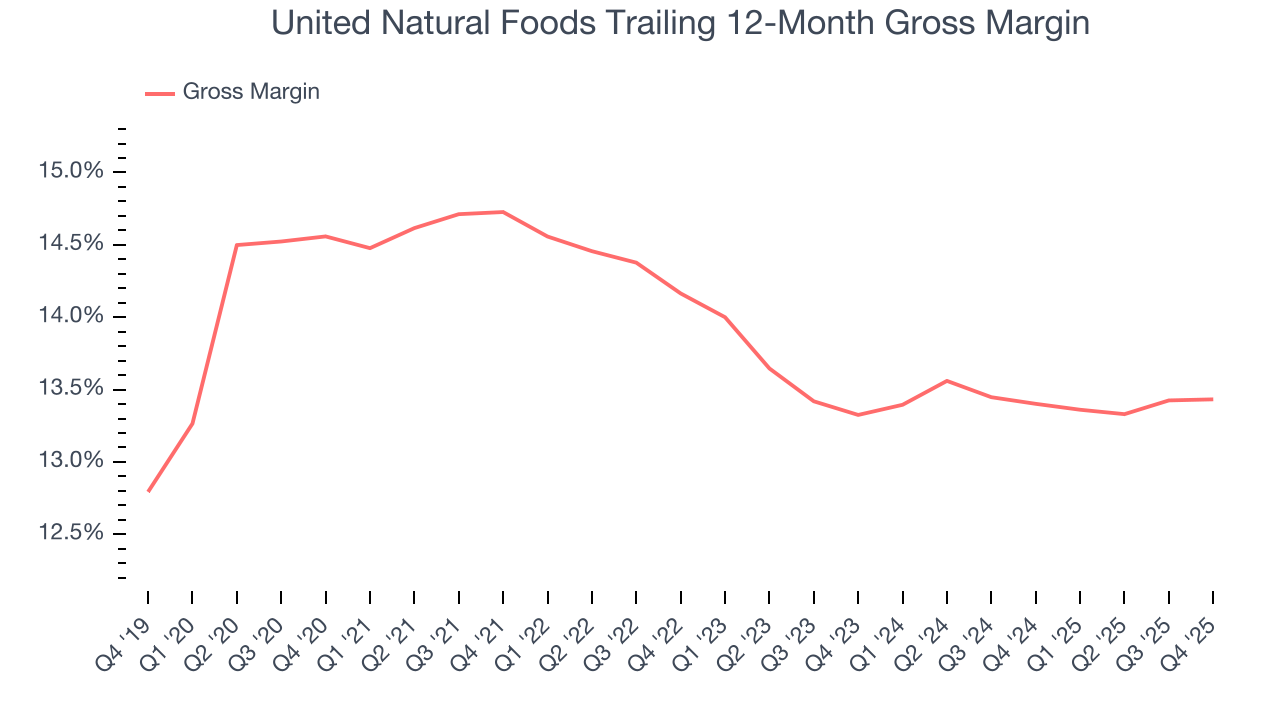

6. Gross Margin & Pricing Power

United Natural Foods has bad unit economics for a consumer staples company, signaling it operates in a competitive market and lacks pricing power because its products can be substituted. As you can see below, it averaged a 13.4% gross margin over the last two years. That means United Natural Foods paid its suppliers a lot of money ($86.58 for every $100 in revenue) to run its business.

This quarter, United Natural Foods’s gross profit margin was 13.2%, in line with the same quarter last year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

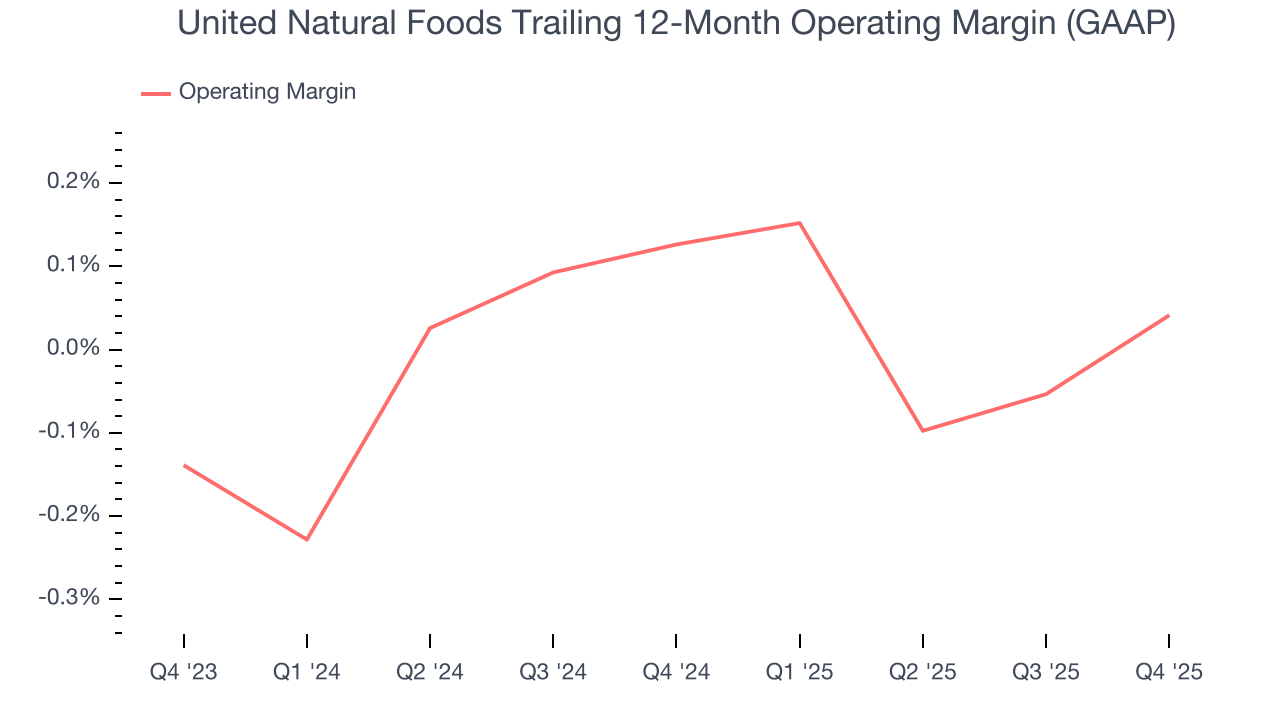

7. Operating Margin

United Natural Foods’s operating margin has more or less stayed the same over the last 12 months . The company broke even over the last two years, lousy for a consumer staples business. Its large expense base , inefficient cost structure, and low gross margin were the main culprits behind this performance.

Looking at the trend in its profitability, United Natural Foods’s operating margin might fluctuated slightly but has generally stayed the same over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q4, United Natural Foods’s breakeven margin was 0.7%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

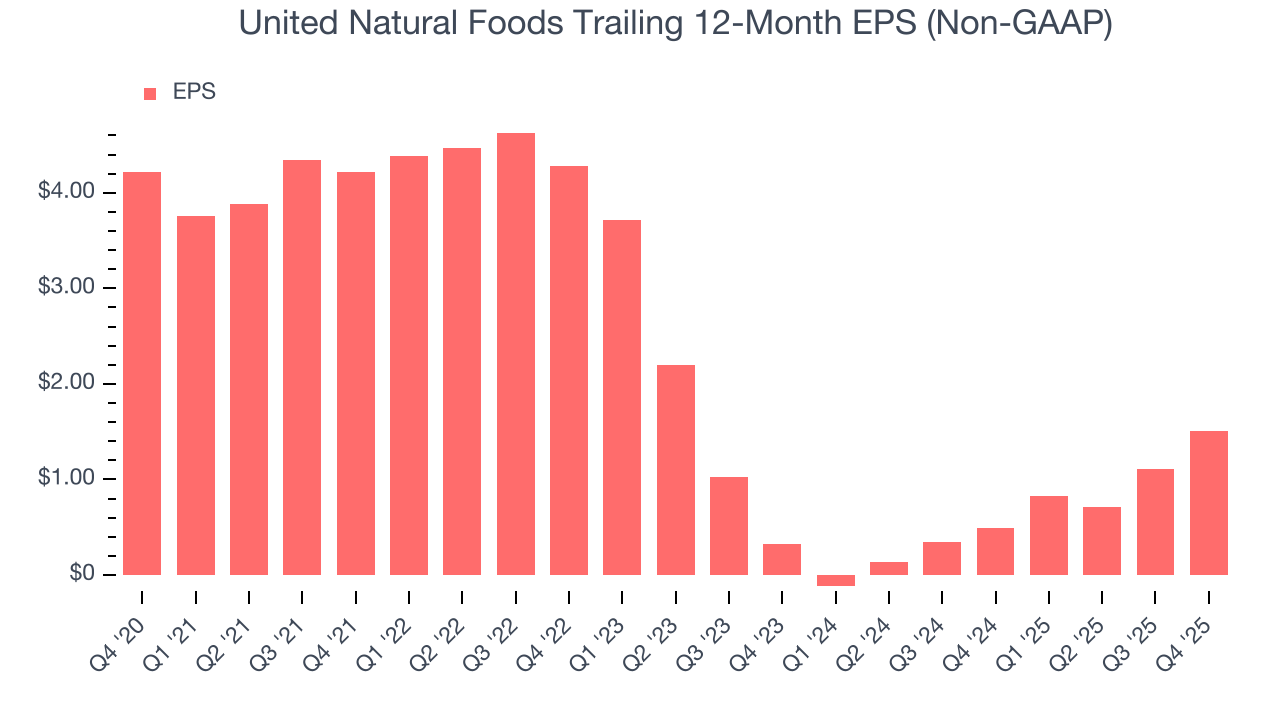

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for United Natural Foods, its EPS declined by 29.3% annually over the last three years while its revenue grew by 1.8%. However, its operating margin didn’t change during this time, telling us that non-fundamental factors such as interest and taxes affected its ultimate earnings.

In Q4, United Natural Foods reported adjusted EPS of $0.62, up from $0.22 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects United Natural Foods’s full-year EPS of $1.51 to grow 56.9%.

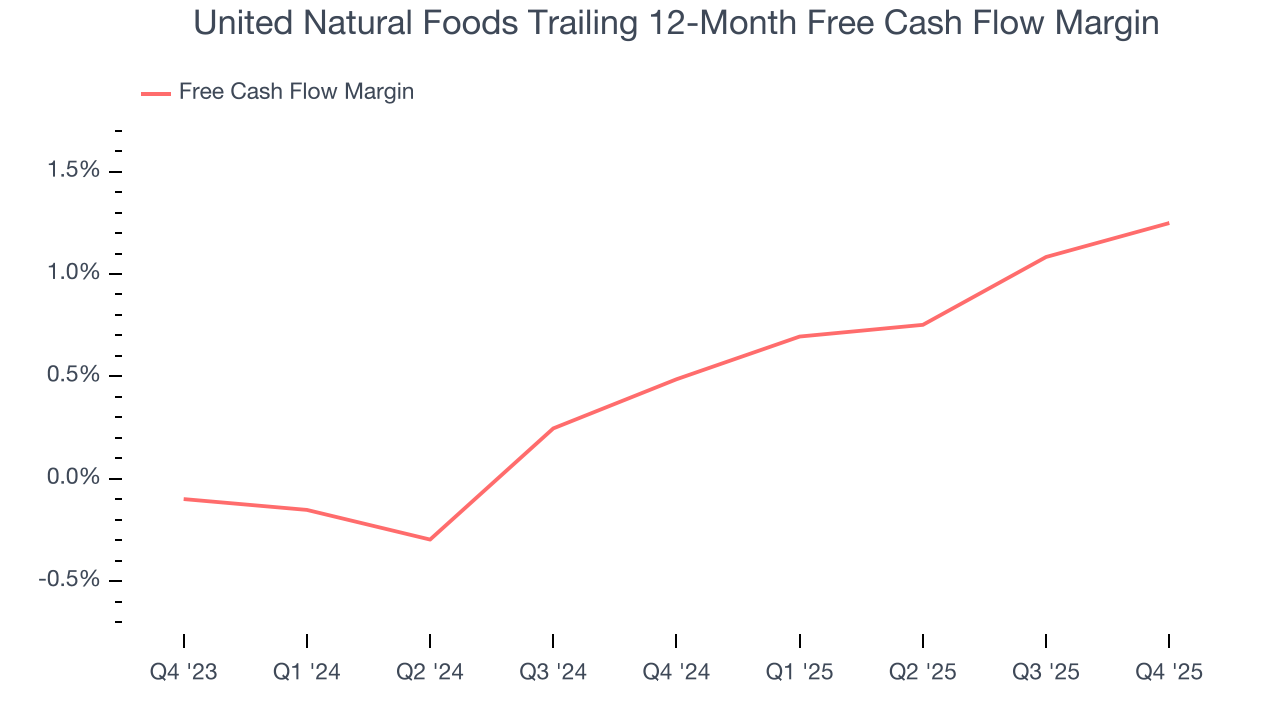

9. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

United Natural Foods broke even from a free cash flow perspective over the last two years, giving the company limited opportunities to return capital to shareholders.

United Natural Foods’s free cash flow clocked in at $243 million in Q4, equivalent to a 3.1% margin. This cash profitability was in line with the comparable period last year and above its two-year average.

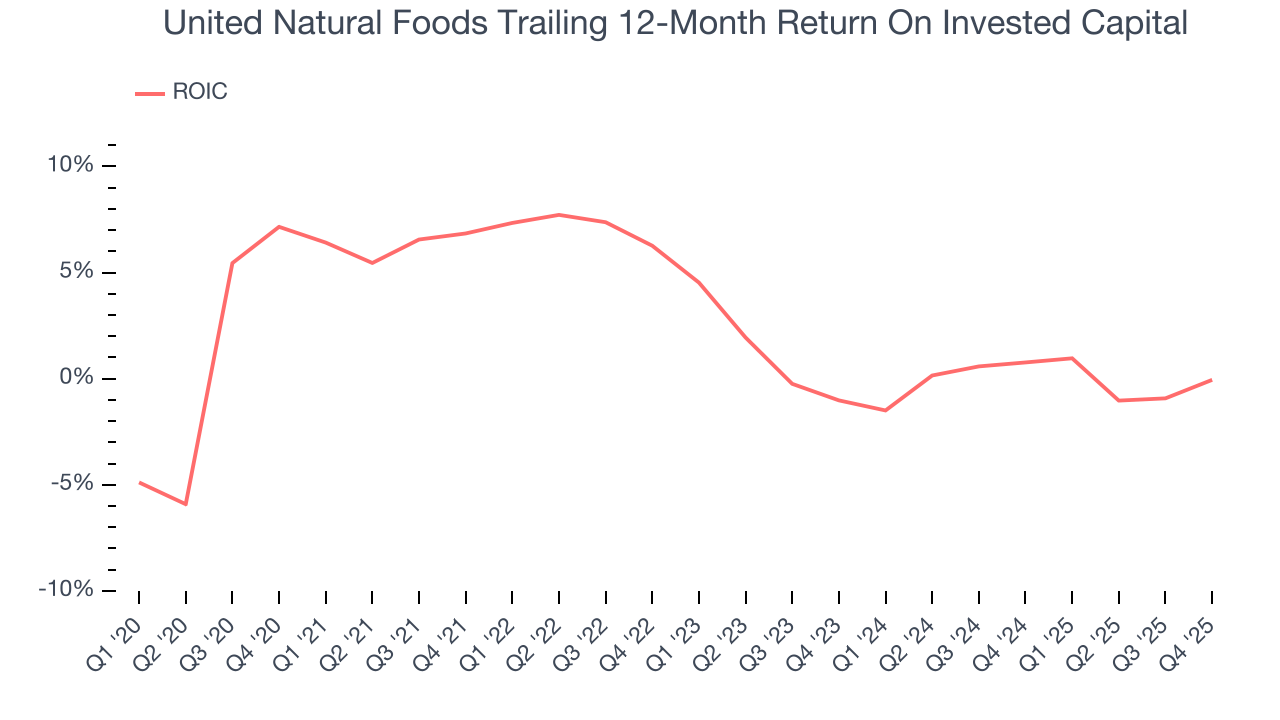

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

United Natural Foods historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 2.6%, lower than the typical cost of capital (how much it costs to raise money) for consumer staples companies.

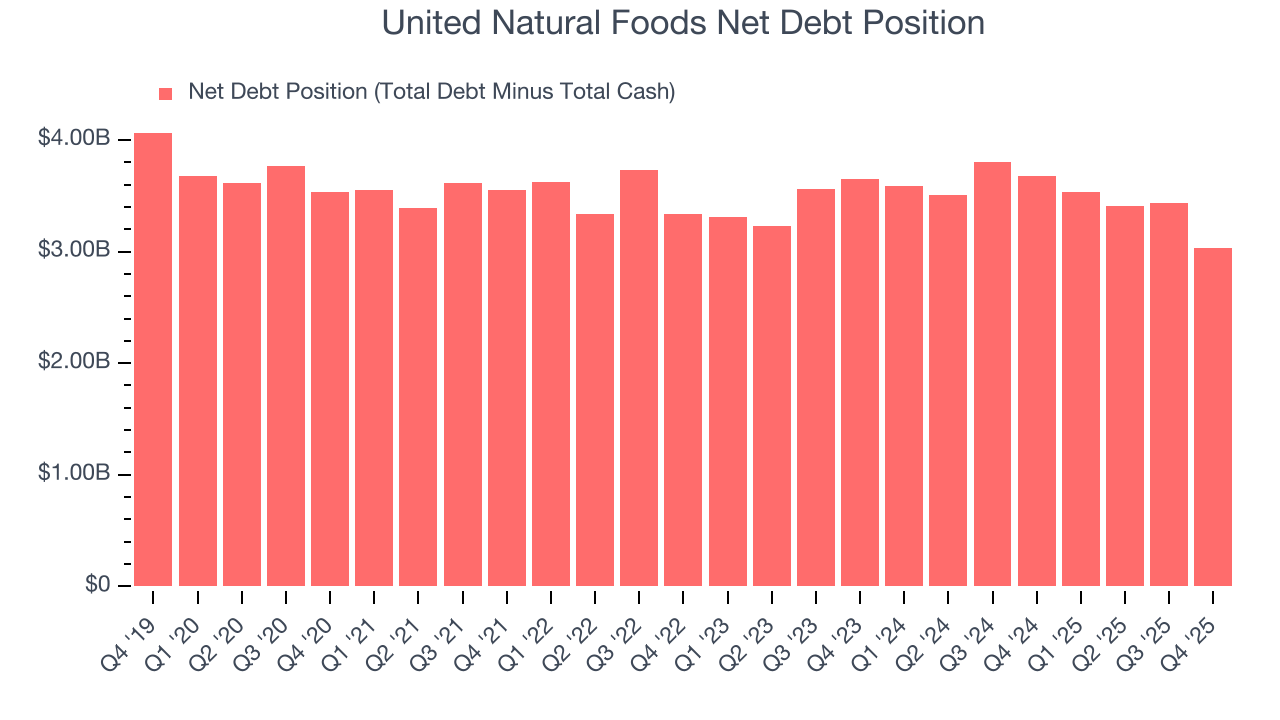

11. Balance Sheet Assessment

United Natural Foods reported $52 million of cash and $3.09 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $619 million of EBITDA over the last 12 months, we view United Natural Foods’s 4.9× net-debt-to-EBITDA ratio as safe. We also see its $70 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from United Natural Foods’s Q4 Results

We enjoyed seeing United Natural Foods beat analysts’ EBITDA and EPS expectations this quarter. On the other hand, its full-year revenue guidance missed and its revenue fell short of Wall Street’s estimates. Overall, this print could have been better. Investors were likely hoping for more, and shares traded down 1.5% to $38.49 immediately following the results.

13. Is Now The Time To Buy United Natural Foods?

Updated: March 12, 2026 at 12:42 AM EDT

Before deciding whether to buy United Natural Foods or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

We see the value of companies helping consumers, but in the case of United Natural Foods, we’re out. First off, its revenue growth was uninspiring over the last three years, and analysts expect its demand to deteriorate over the next 12 months. While its projected EPS for the next year implies the company’s fundamentals will improve, the downside is its declining EPS over the last three years makes it a less attractive asset to the public markets. On top of that, its gross margins make it more challenging to reach positive operating profits compared to other consumer staples businesses.

United Natural Foods’s P/E ratio based on the next 12 months is 13.2x. This valuation is reasonable, but the company’s shaky fundamentals present too much downside risk. There are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $44.25 on the company (compared to the current share price of $40.50).