UnitedHealth (UNH)

We see potential in UnitedHealth. Its scale gives it meaningful leverage when negotiating reimbursement rates.― StockStory Analyst Team

1. News

2. Summary

Why UnitedHealth Is Interesting

With over 100 million people served across its various businesses and a workforce of more than 400,000, UnitedHealth Group (NYSE:UNH) operates a health insurance business and Optum, a healthcare services division that provides everything from pharmacy benefits to primary care.

- Massive revenue base of $447.6 billion gives it meaningful leverage when negotiating reimbursement rates

- ROIC punches in at 19.6%, illustrating management’s expertise in identifying profitable investments

- A drawback is its incremental sales over the last five years were less profitable as its earnings per share were flat while its revenue grew

UnitedHealth almost passes our quality test. If you like the stock, the valuation seems reasonable.

Why Is Now The Time To Buy UnitedHealth?

UnitedHealth is trading at $269.85 per share, or 15.4x forward P/E. Many healthcare companies feature higher valuation multiples than UnitedHealth. Regardless, we think UnitedHealth’s current price is appropriate given the quality you get.

Now could be a good time to invest if you believe in the story.

3. UnitedHealth (UNH) Research Report: Q4 CY2025 Update

Health insurance company UnitedHealth (NYSE:UNH) met Wall Streets revenue expectations in Q4 CY2025, with sales up 12.3% year on year to $113.2 billion. On the other hand, the company’s full-year revenue guidance of $439 billion at the midpoint came in 3.7% below analysts’ estimates. Its non-GAAP profit of $2.11 per share was in line with analysts’ consensus estimates.

UnitedHealth (UNH) Q4 CY2025 Highlights:

- Revenue: $113.2 billion vs analyst estimates of $113.6 billion (12.3% year-on-year growth, in line)

- Adjusted EPS: $2.11 vs analyst estimates of $2.11 (in line)

- Adjusted EPS guidance for the upcoming financial year 2026 is $17.75 at the midpoint, in line with analyst estimates

- Operating Margin: 0.3%, down from 7.7% in the same quarter last year

- Free Cash Flow Margin: 0.1%, down from 1.4% in the same quarter last year

- Market Capitalization: $318.5 billion

Company Overview

With over 100 million people served across its various businesses and a workforce of more than 400,000, UnitedHealth Group (NYSE:UNH) operates a health insurance business and Optum, a healthcare services division that provides everything from pharmacy benefits to primary care.

UnitedHealth Group's business is divided into two main segments: UnitedHealthcare, which provides health insurance, and Optum, which offers healthcare services. The UnitedHealthcare segment serves various populations through employer-sponsored plans, Medicare Advantage and supplement plans, Medicaid programs, and individual marketplace plans. For example, a mid-sized manufacturing company might contract with UnitedHealthcare to provide health benefits for its employees, while a senior citizen might enroll in one of UnitedHealthcare's Medicare Advantage plans to receive comprehensive coverage beyond traditional Medicare.

Optum consists of three businesses: Optum Health, which delivers care through clinics, virtual visits, and home-based services; Optum Insight, which provides data analytics and technology solutions to healthcare organizations; and Optum Rx, which manages pharmacy benefits and operates specialty pharmacies. A hospital system might use Optum Insight's software to improve its billing efficiency, while an employer might partner with Optum Rx to manage prescription costs for its workforce.

The company generates revenue primarily through insurance premiums, service fees, and direct payments for healthcare services. UnitedHealth Group has significant government relationships, with approximately 40% of its revenue coming from the Centers for Medicare & Medicaid Services.

UnitedHealth Group has expanded its care delivery capabilities substantially, now employing or contracting with thousands of physicians and operating numerous clinics and surgery centers. This vertical integration strategy allows the company to both pay for and provide healthcare services, giving it unique visibility into healthcare costs and utilization patterns.

The company operates globally, with a presence in Brazil, Chile, Colombia, Peru, and over 150 other countries, though the vast majority of its business remains in the United States.

4. Health Insurance Providers

Upfront premiums collected by health insurers lead to reliable revenue, but profitability ultimately depends on accurate risk assessments and the ability to control medical costs. Health insurers are also highly sensitive to regulatory changes and economic conditions such as unemployment. Going forward, the industry faces tailwinds from an aging population, increasing demand for personalized healthcare services, and advancements in data analytics to improve cost management. However, continued regulatory scrutiny on pricing practices, the potential for government-led reforms such as expanded public healthcare options, and inflation in medical costs could add volatility to margins. One big debate among investors is the long-term impact of AI and whether it will help underwriting, fraud detection, and claims processing or whether it may wade into ethical grey areas like reinforcing biases and widening disparities in medical care.

UnitedHealth Group's main competitors include other major health insurers such as Cigna (NYSE:CI), Humana (NYSE:HUM), CVS Health's Aetna (NYSE:CVS), Elevance Health (NYSE:ELV), and Centene (NYSE:CNC). In its Optum businesses, the company competes with a range of healthcare service providers including CVS Health, Walgreens Boots Alliance (NASDAQ:WBA), and numerous specialized healthcare technology and service companies.

5. Economies of Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With $447.6 billion in revenue over the past 12 months, UnitedHealth is one of the most scaled enterprises in healthcare. This is particularly important because health insurance providers companies are volume-driven businesses due to their low margins.

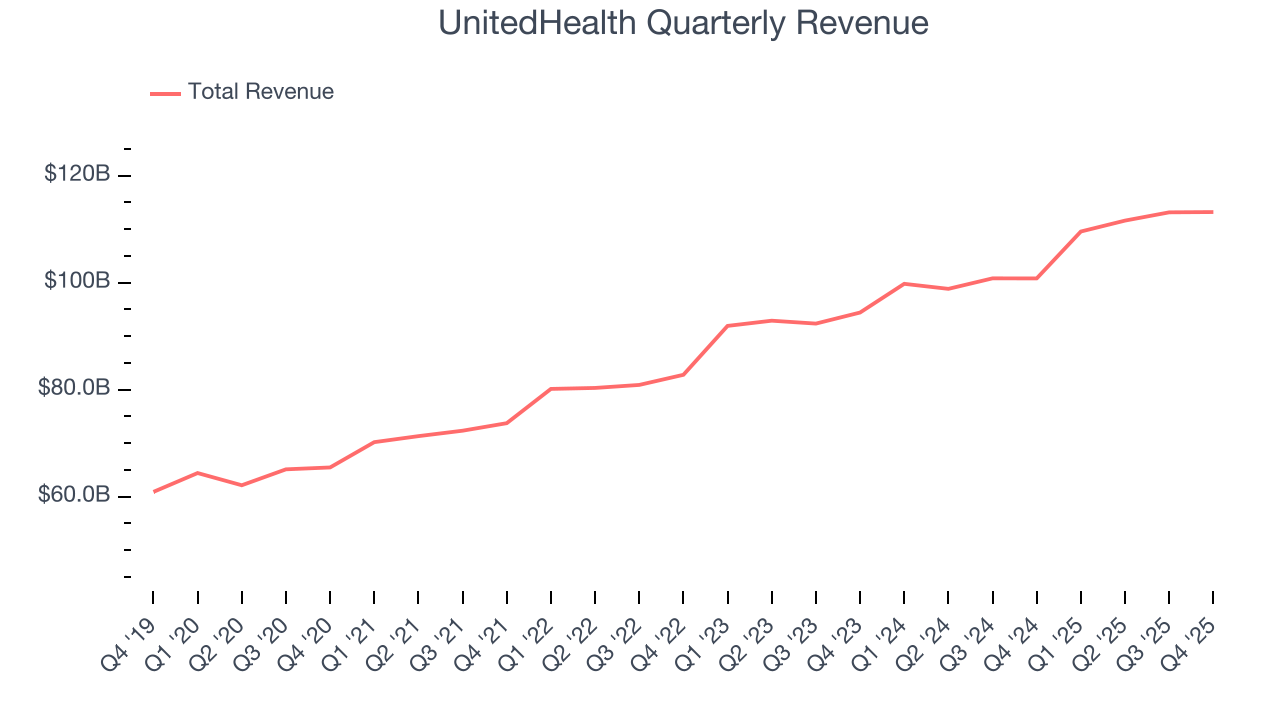

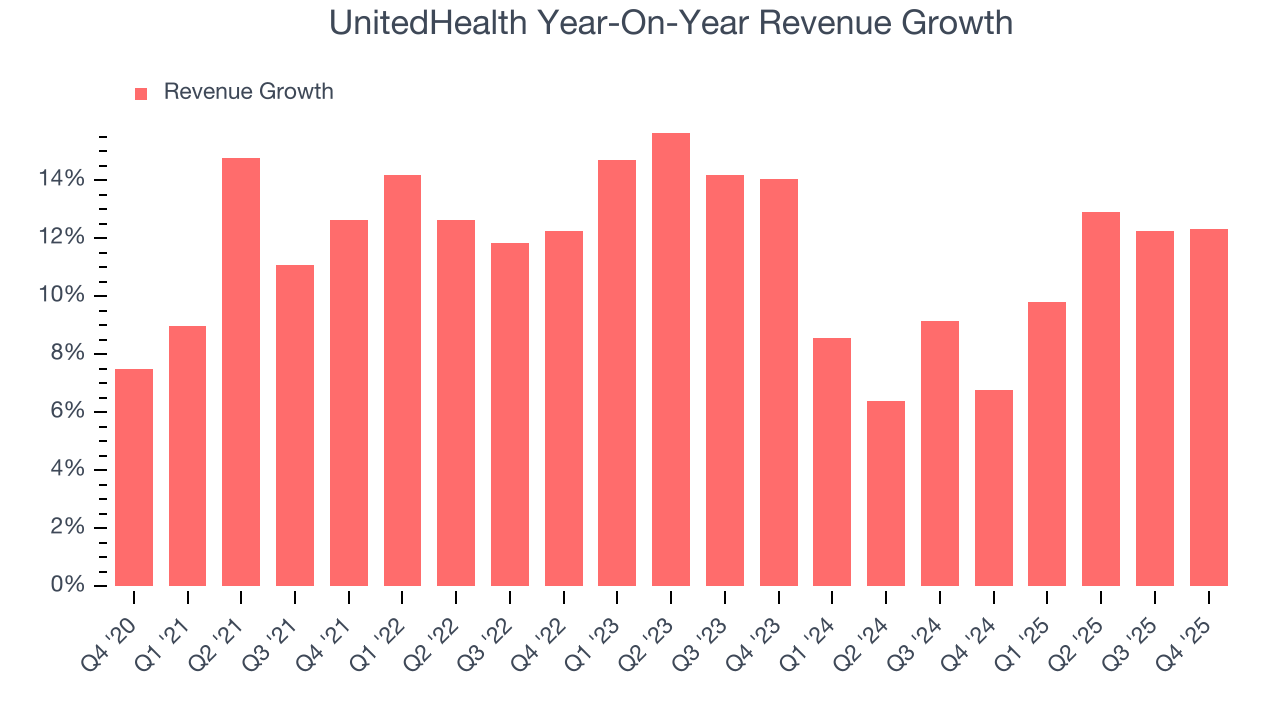

6. Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Luckily, UnitedHealth’s sales grew at a decent 11.7% compounded annual growth rate over the last five years. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. UnitedHealth’s annualized revenue growth of 9.7% over the last two years is below its five-year trend, but we still think the results were respectable.

This quarter, UnitedHealth’s year-on-year revenue growth was 12.3%, and its $113.2 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 1.8% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

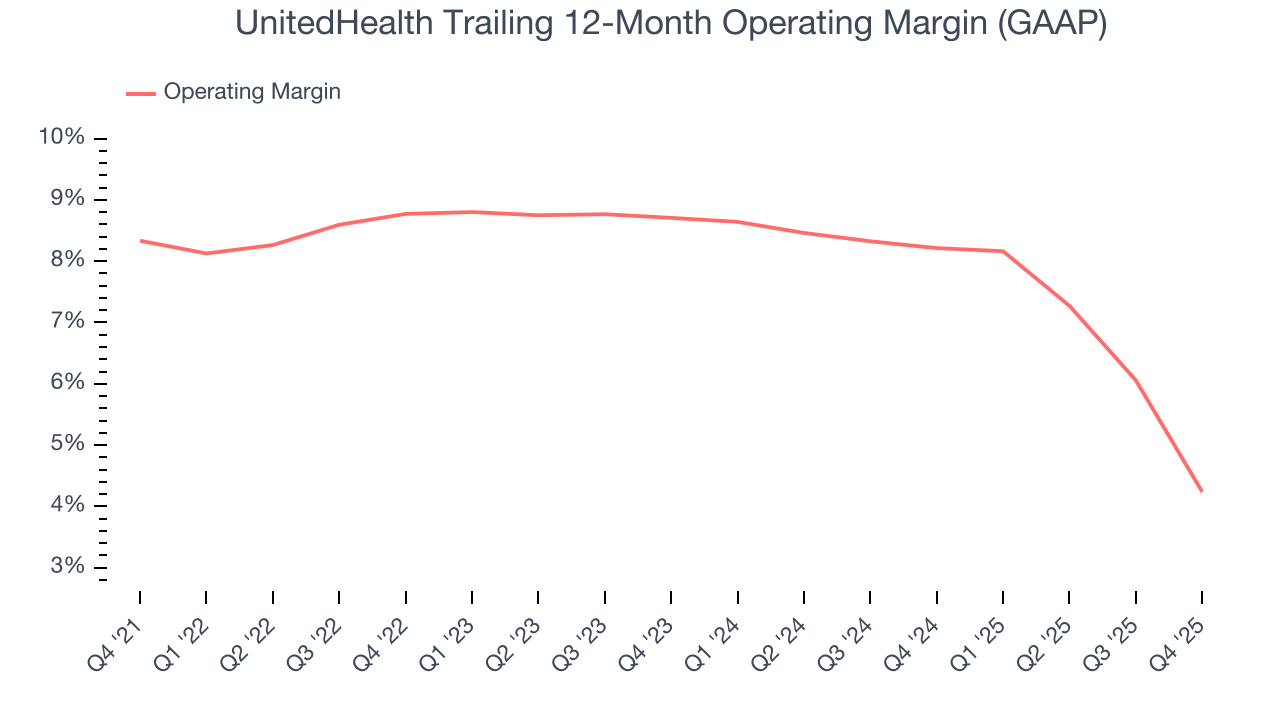

7. Operating Margin

UnitedHealth was profitable over the last five years but held back by its large cost base. Its average operating margin of 7.5% was weak for a healthcare business.

Looking at the trend in its profitability, UnitedHealth’s operating margin decreased by 4.1 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 4.5 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

In Q4, UnitedHealth’s breakeven margin was down 7.4 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

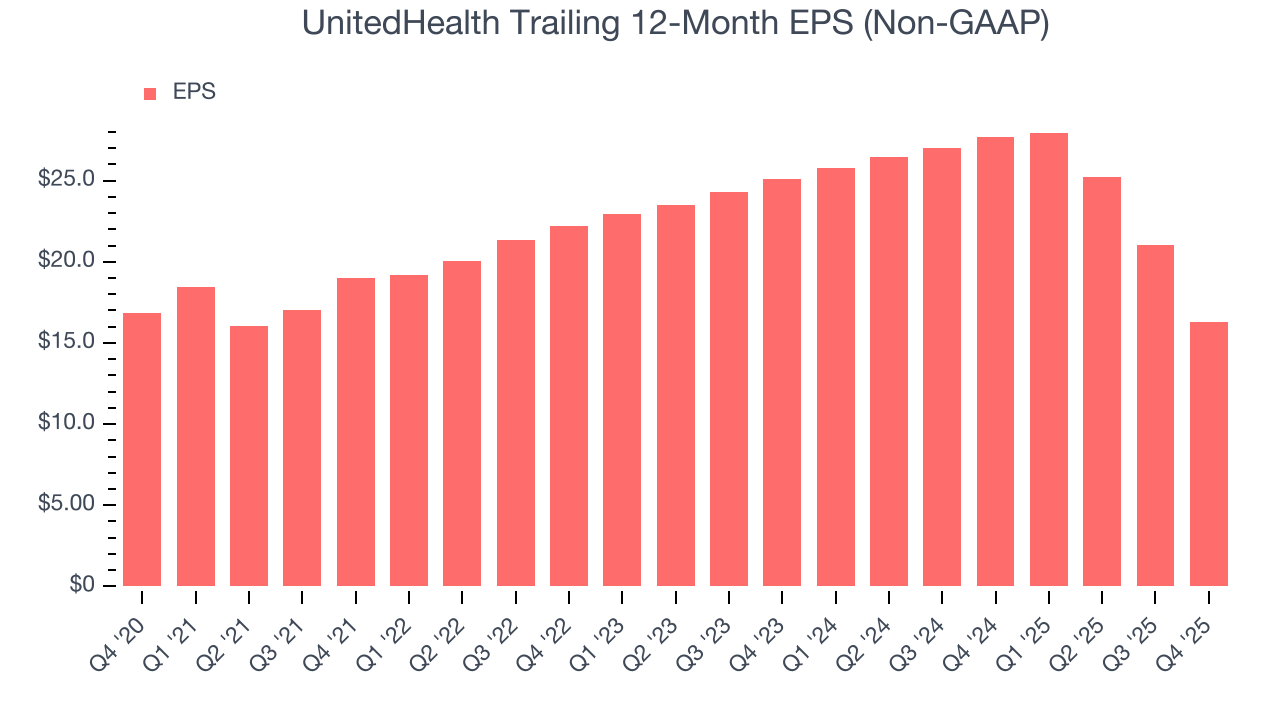

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

UnitedHealth’s flat EPS over the last five years was below its 11.7% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded due to non-fundamental factors such as interest expenses and taxes.

Diving into the nuances of UnitedHealth’s earnings can give us a better understanding of its performance. As we mentioned earlier, UnitedHealth’s operating margin declined by 4.1 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, UnitedHealth reported adjusted EPS of $2.11, down from $6.81 in the same quarter last year. This print was close to analysts’ estimates. Over the next 12 months, Wall Street expects UnitedHealth’s full-year EPS of $16.31 to grow 8.8%.

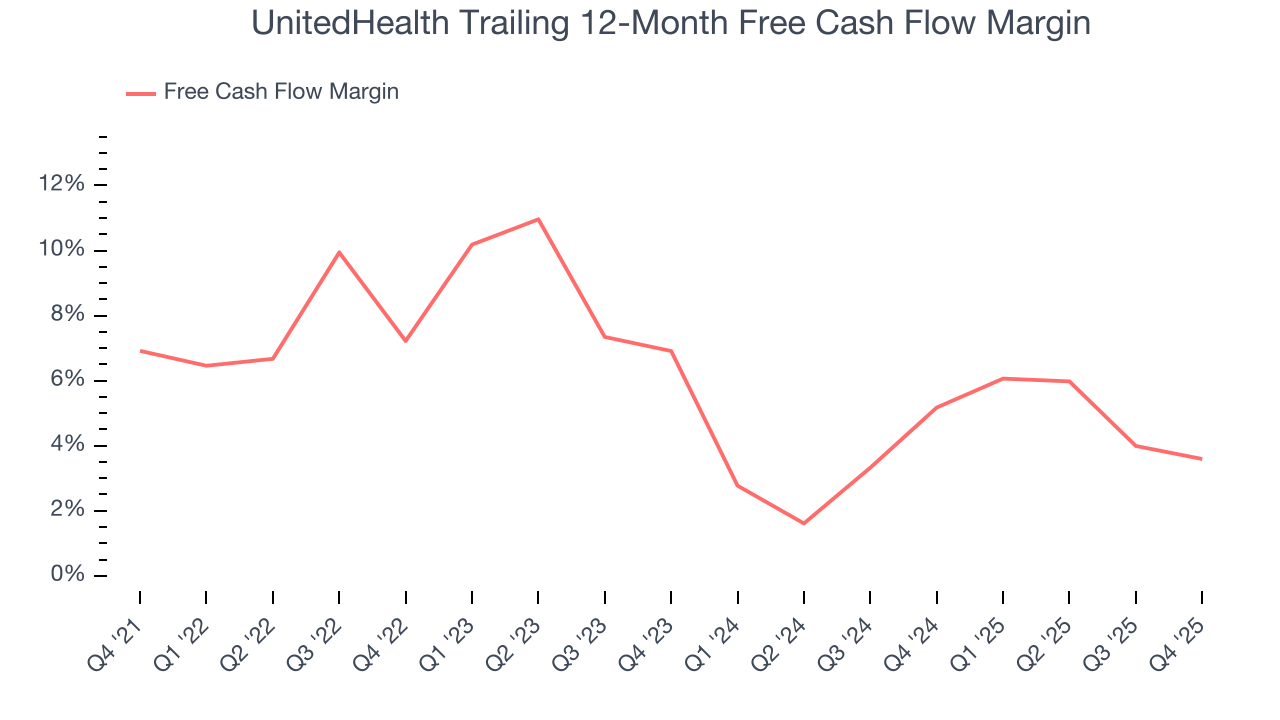

9. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

UnitedHealth has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 5.8% over the last five years, slightly better than the broader healthcare sector.

Taking a step back, we can see that UnitedHealth’s margin dropped by 3.3 percentage points during that time. We’re willing to live with its performance for now but hope its cash conversion can rise soon. Continued declines could signal it is in the middle of an investment cycle.

UnitedHealth broke even from a free cash flow perspective in Q4. The company’s cash profitability regressed as it was 1.3 percentage points lower than in the same quarter last year, which isn’t ideal considering its longer-term trend.

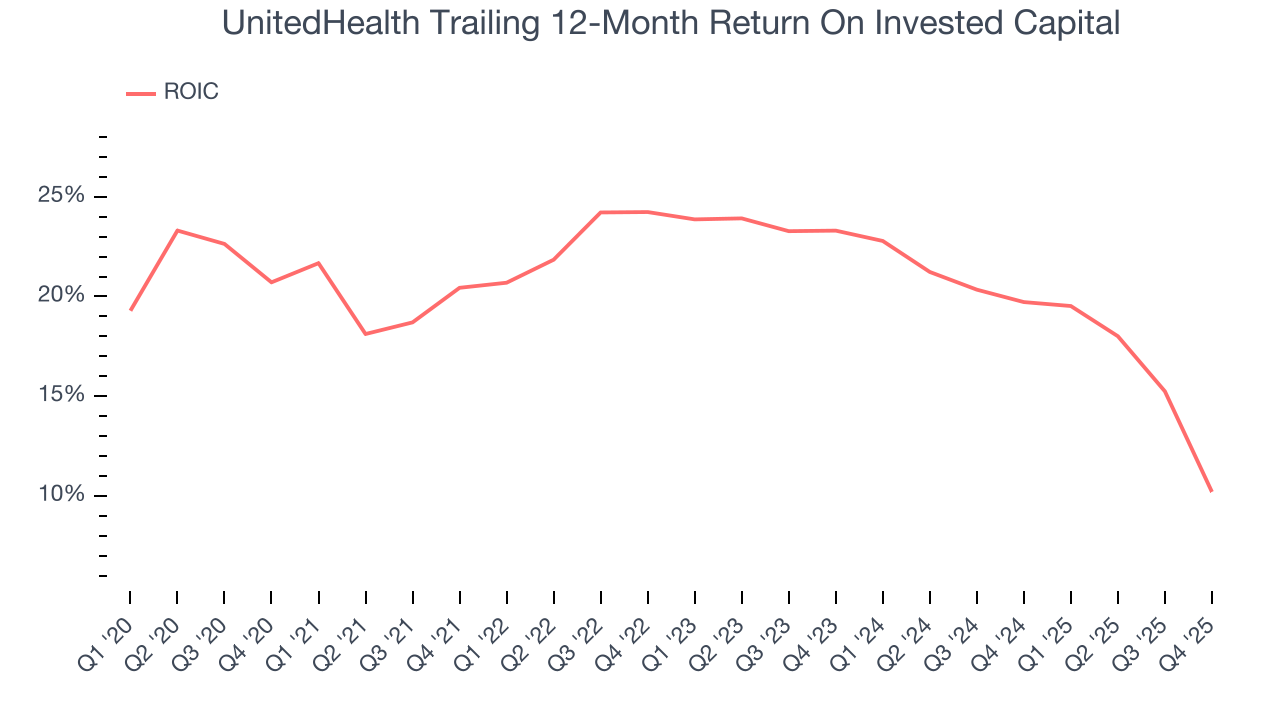

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

UnitedHealth’s five-year average ROIC was 19.6%, beating other healthcare companies by a wide margin. This illustrates its management team’s ability to invest in attractive growth opportunities and produce tangible results for shareholders.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, UnitedHealth’s ROIC has decreased over the last few years. Only time will tell if its new bets can bear fruit and potentially reverse the trend.

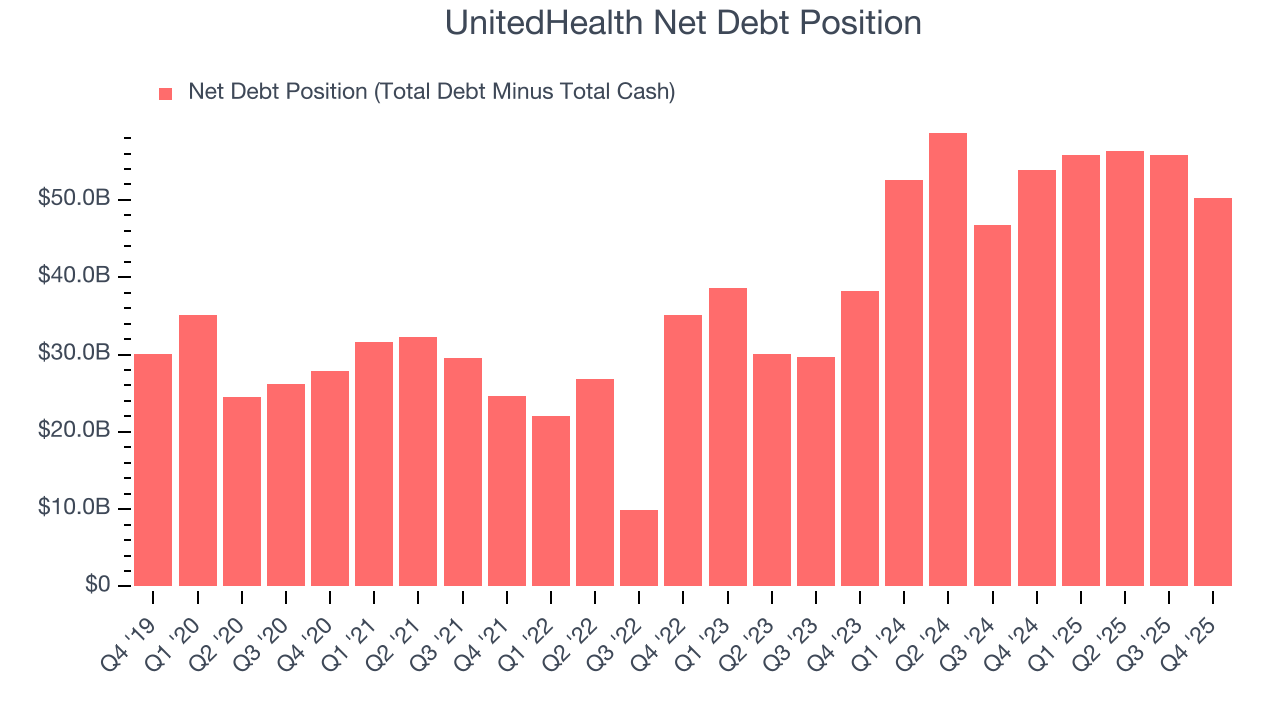

11. Balance Sheet Assessment

UnitedHealth reported $28.12 billion of cash and $78.39 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $23.5 billion of EBITDA over the last 12 months, we view UnitedHealth’s 2.1× net-debt-to-EBITDA ratio as safe. We also see its $2.05 billion of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from UnitedHealth’s Q4 Results

We struggled to find many positives in these results. Its full-year revenue guidance missed and its revenue was in line with Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 12.3% to $308.54 immediately following the results.

13. Is Now The Time To Buy UnitedHealth?

Updated: March 24, 2026 at 12:01 AM EDT

Before investing in or passing on UnitedHealth, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

There are things to like about UnitedHealth. First off, its revenue growth was good over the last five years. And while its weak EPS growth over the last five years shows it’s failed to produce meaningful profits for shareholders, its scale gives it meaningful leverage when negotiating reimbursement rates. On top of that, its market-beating ROIC suggests it has been a well-managed company historically.

UnitedHealth’s P/E ratio based on the next 12 months is 15.4x. Looking at the healthcare space right now, UnitedHealth trades at a compelling valuation. For those confident in the business and its management team, this is a good time to invest.

Wall Street analysts have a consensus one-year price target of $361.21 on the company (compared to the current share price of $269.85), implying they see 33.9% upside in buying UnitedHealth in the short term.