Universal Technical Institute (UTI)

Universal Technical Institute keeps us up at night. Its sales have underperformed and its low returns on capital show it has few growth opportunities.― StockStory Analyst Team

1. News

2. Summary

Why We Think Universal Technical Institute Will Underperform

Founded in 1965, Universal Technical Institute (NYSE: UTI) is a leading provider of technical training programs, specializing in automotive, diesel, collision repair, motorcycle, and marine technicians.

- 17.3% annual revenue growth over the last two years was slower than its consumer discretionary peers

- Poor expense management has led to an operating margin that is below the industry average

- Ability to fund investments or reward shareholders with increased buybacks or dividends is restricted by its weak free cash flow margin of 7.5% for the last two years

Universal Technical Institute doesn’t fulfill our quality requirements. There are more appealing investments to be made.

Why There Are Better Opportunities Than Universal Technical Institute

Universal Technical Institute’s stock price of $28.24 implies a valuation ratio of 15.2x forward EV-to-EBITDA. This multiple is quite expensive for the quality you get.

It’s better to invest in high-quality businesses with strong long-term earnings potential rather than to buy lower-quality companies with open questions and big downside risks.

3. Universal Technical Institute (UTI) Research Report: Q4 CY2025 Update

Vocational education Universal Technical Institute (NYSE:UTI) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, with sales up 9.6% year on year to $220.8 million. The company expects the full year’s revenue to be around $910 million, close to analysts’ estimates. Its GAAP profit of $0.23 per share was 66.3% above analysts’ consensus estimates.

Universal Technical Institute (UTI) Q4 CY2025 Highlights:

- Revenue: $220.8 million vs analyst estimates of $217.5 million (9.6% year-on-year growth, 1.6% beat)

- EPS (GAAP): $0.23 vs analyst estimates of $0.14 (66.3% beat)

- Adjusted EBITDA: $27.15 million vs analyst estimates of $23.94 million (12.3% margin, 13.4% beat)

- The company reconfirmed its revenue guidance for the full year of $910 million at the midpoint

- EBITDA guidance for the full year is $116.5 million at the midpoint, in line with analyst expectations

- Operating Margin: 7.1%, down from 13.6% in the same quarter last year

- Free Cash Flow was -$19.16 million, down from $19.62 million in the same quarter last year

- New Students: 5,449, up 136 year on year

- Market Capitalization: $1.57 billion

Company Overview

Founded in 1965, Universal Technical Institute (NYSE: UTI) is a leading provider of technical training programs, specializing in automotive, diesel, collision repair, motorcycle, and marine technicians.

UTI offers industry-aligned curricula and a hands-on training approach. The institute collaborates with some of the biggest names in the automotive and manufacturing sectors, such as Ford, BMW, and Harley-Davidson, to ensure that the training and education provided are aligned with industry needs and technological advancements.

The programs offered at UTI cover a range of transportation-related fields, and students pay tuition to enroll in its courses. In automotive, students are trained in vehicle repair and maintenance, including engine diagnostics, drivability, and electronic systems. The diesel technician training involves learning about large vehicles and engines, focusing on fuel systems, hydraulics, and power generators. Additionally, UTI offers specialized programs in collision repair, welding, CNC machining, and marine technology.

In addition to its core programs, UTI has expanded its offerings to include Manufacturer-Specific Advanced Training (MSAT) programs. These specialized courses are designed to provide advanced training in specific brands and technologies to give students an edge in the highly competitive job market.

One of UTI’s focuses is on career readiness. Its Career Services department actively assists students and graduates in finding employment opportunities, utilizing UTI's extensive network of industry contacts. This includes job placement assistance, resume building, and interview preparation.

4. Education Services

A whole industry has emerged to address the problem of rising education costs, offering consumers alternatives to traditional education paths such as four-year colleges. These alternative paths, which may include online courses or flexible schedules, make education more accessible to those with work or child-rearing obligations. However, some have run into issues around the value of the degrees and certifications they provide and whether customers are getting a good deal. Those who don’t prove their value could struggle to retain students, or even worse, invite the heavy hand of regulation.

Universal Technical Institute’s primary competitors include Lincoln Educational Services (NASDAQ:LINC), Adtalem Global Education (NYSE:ATGE), Strategic Education (NASDAQ:STRA), Chegg (NYSE:CHGG), and private companies WyoTech and Ohio Technical College.

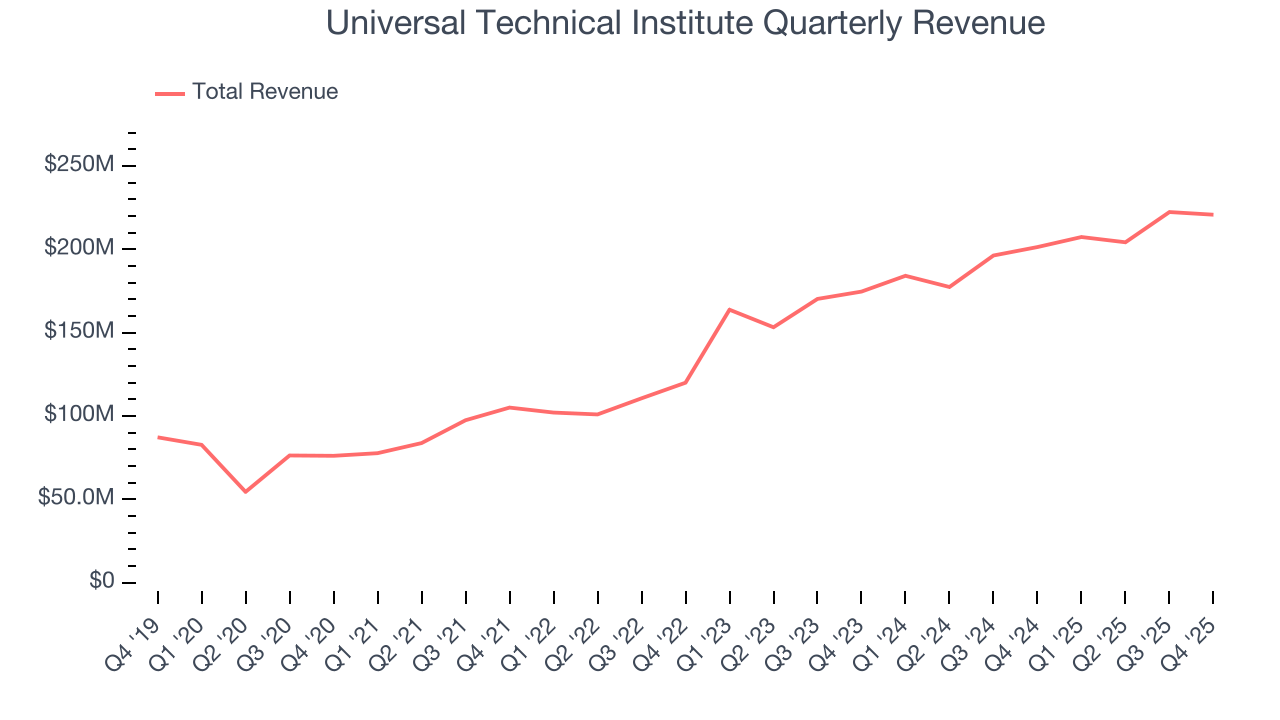

5. Revenue Growth

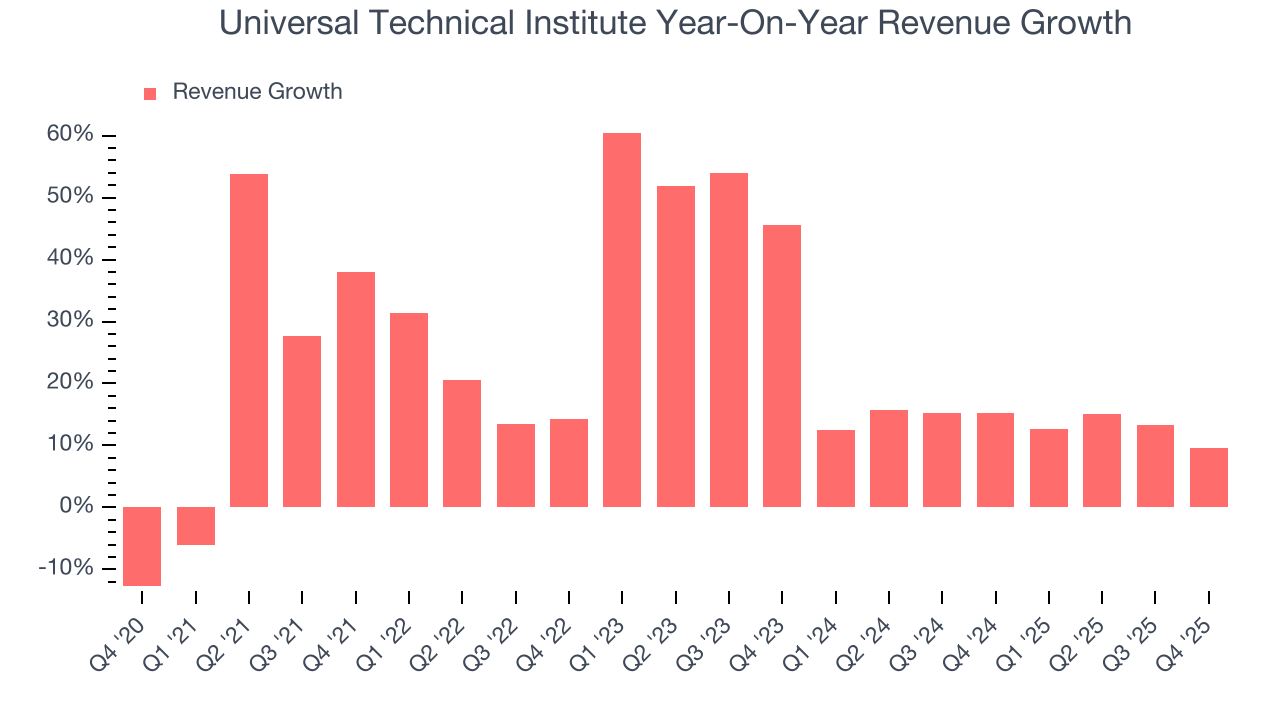

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Universal Technical Institute grew its sales at a 24.2% compounded annual growth rate. Although this growth is acceptable on an absolute basis, it fell slightly short of our standards for the consumer discretionary sector, which enjoys a number of secular tailwinds.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Universal Technical Institute’s recent performance shows its demand has slowed as its annualized revenue growth of 13.6% over the last two years was below its five-year trend.

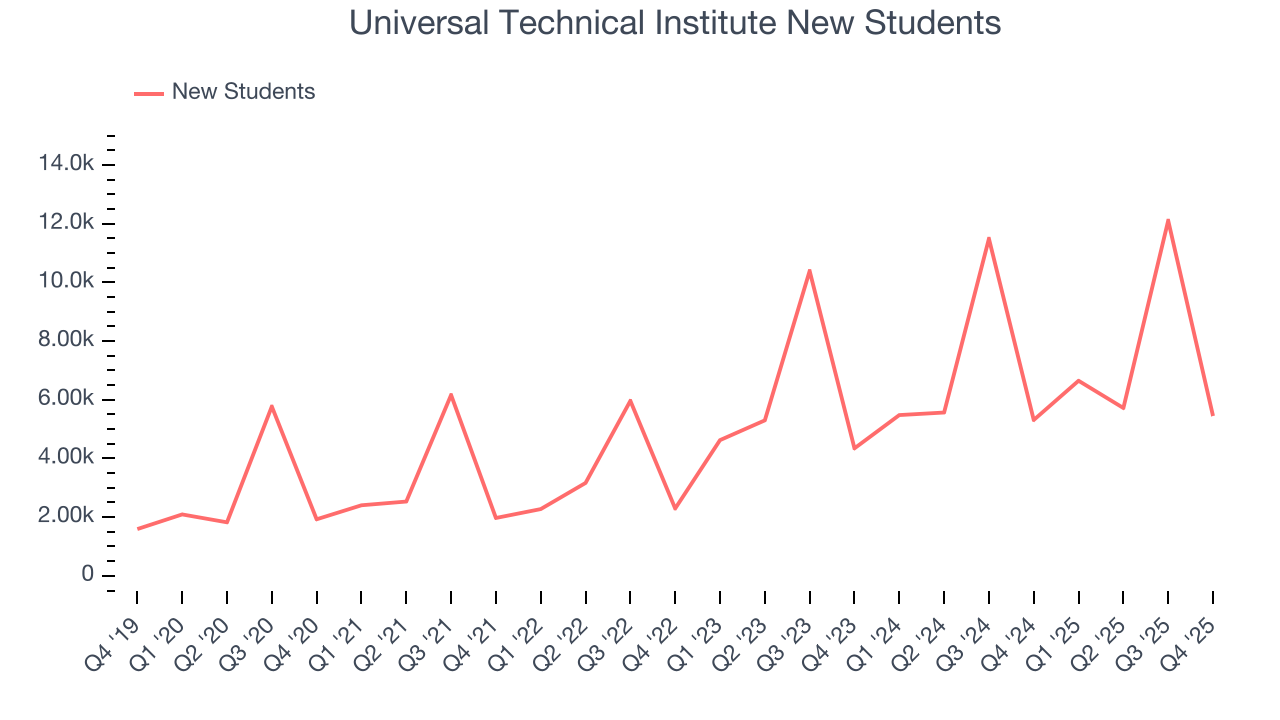

Universal Technical Institute also discloses its number of new students, which reached 5,449 in the latest quarter. Over the last two years, Universal Technical Institute’s new students averaged 11% year-on-year growth. Because this number is lower than its revenue growth during the same period, we can see the company’s monetization has risen.

This quarter, Universal Technical Institute reported year-on-year revenue growth of 9.6%, and its $220.8 million of revenue exceeded Wall Street’s estimates by 1.6%.

Looking ahead, sell-side analysts expect revenue to grow 8.8% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and implies its products and services will face some demand challenges.

6. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

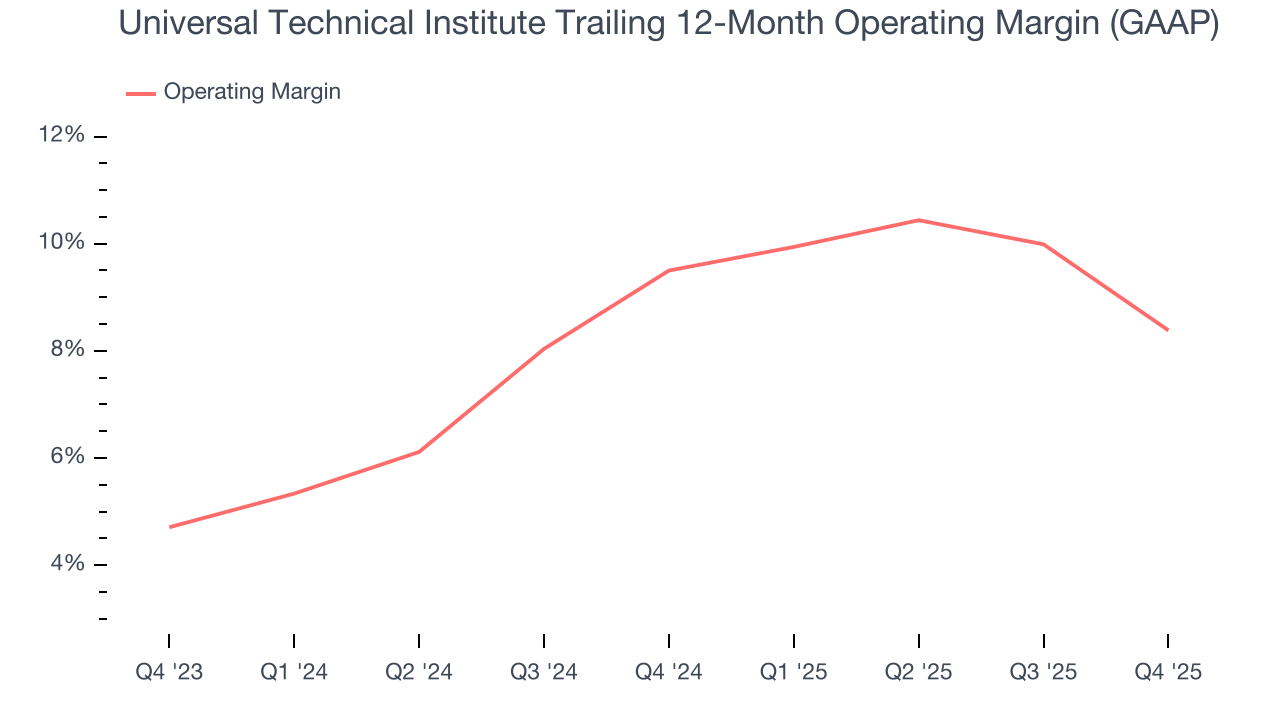

Universal Technical Institute’s operating margin has been trending down over the last 12 months and averaged 8.9% over the last two years. The company’s profitability was mediocre for a consumer discretionary business and shows it couldn’t pass its higher operating expenses onto its customers.

This quarter, Universal Technical Institute generated an operating margin profit margin of 7.1%, down 6.5 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

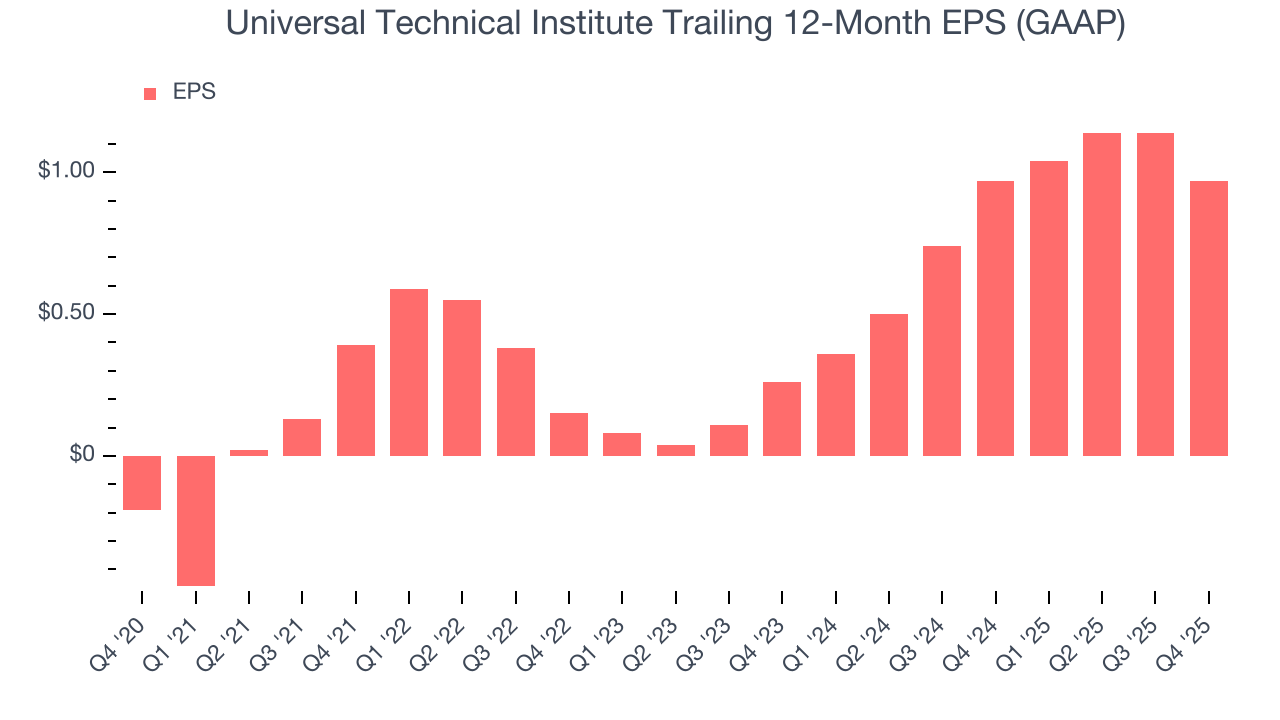

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Universal Technical Institute’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

In Q4, Universal Technical Institute reported EPS of $0.23, down from $0.40 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Universal Technical Institute’s full-year EPS of $0.97 to shrink by 16.7%.

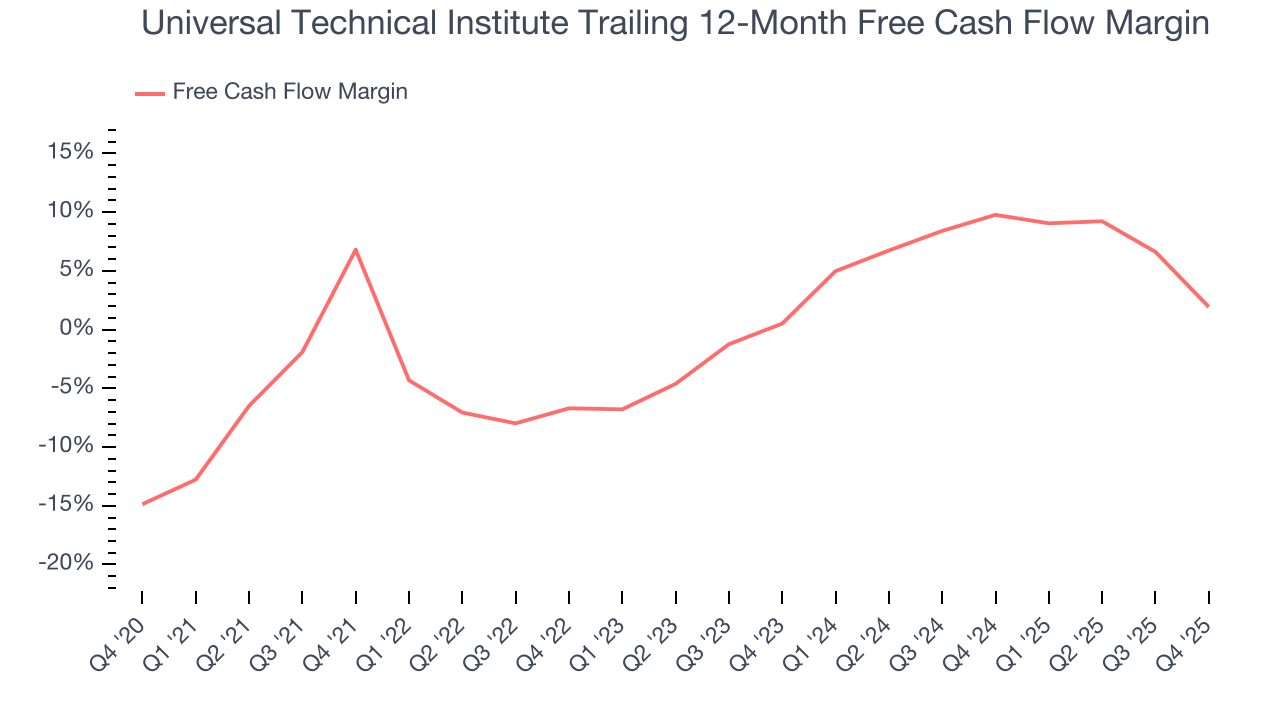

8. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Universal Technical Institute has shown poor cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 5.6%, lousy for a consumer discretionary business.

Universal Technical Institute burned through $19.16 million of cash in Q4, equivalent to a negative 8.7% margin. The company’s cash flow turned negative after being positive in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

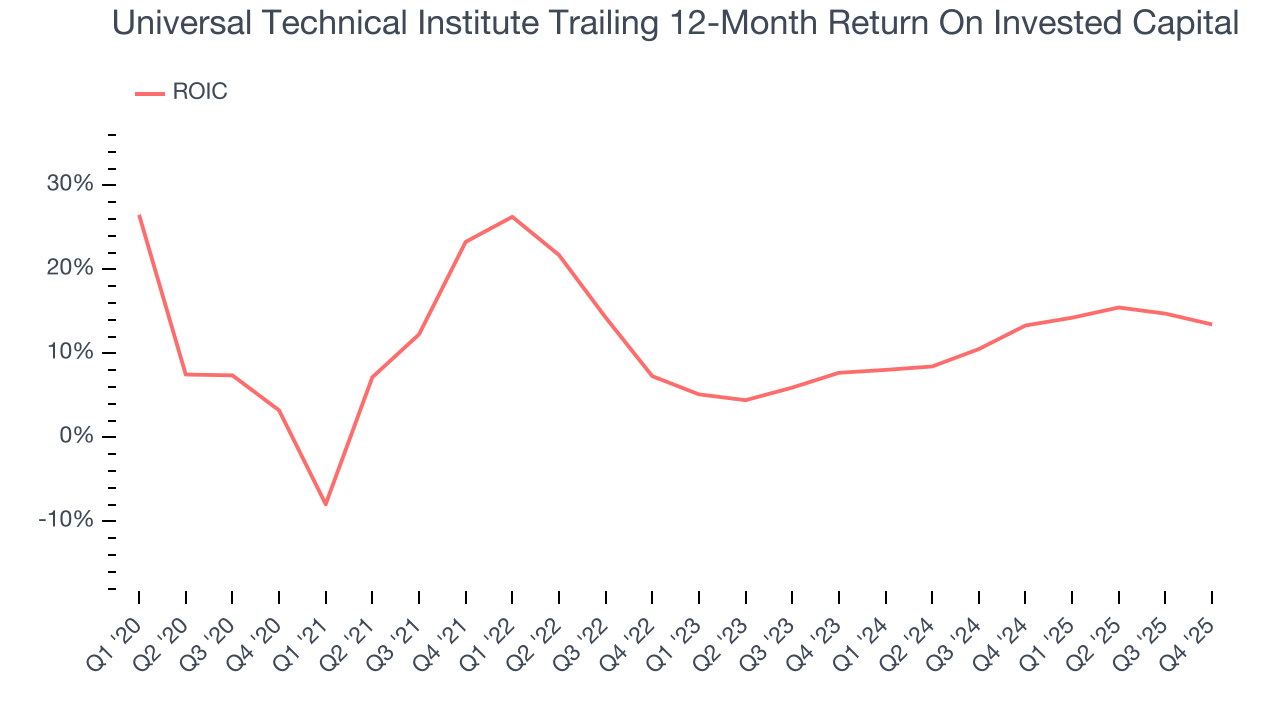

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Universal Technical Institute historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 13%, somewhat low compared to the best consumer discretionary companies that consistently pump out 25%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Universal Technical Institute’s ROIC averaged 1.9 percentage point decreases each year over the last few years. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

10. Balance Sheet Assessment

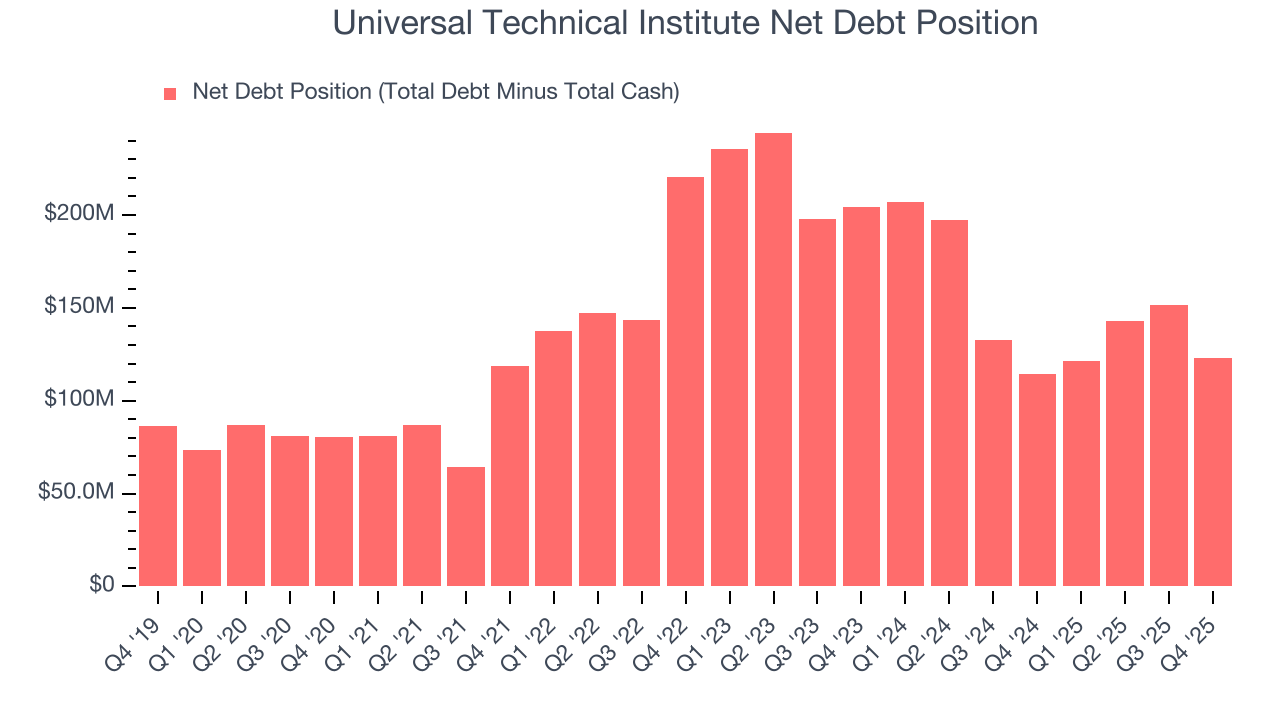

Universal Technical Institute reported $166.7 million of cash and $289.6 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $118.1 million of EBITDA over the last 12 months, we view Universal Technical Institute’s 1.0× net-debt-to-EBITDA ratio as safe. We also see its $121,000 of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from Universal Technical Institute’s Q4 Results

It was good to see Universal Technical Institute beat analysts’ EPS expectations this quarter. We were also glad its EBITDA outperformed Wall Street’s estimates. On the other hand, its number of new students missed. Overall, this print had some key positives. The stock remained flat at $27.89 immediately following the results.

12. Is Now The Time To Buy Universal Technical Institute?

Updated: February 4, 2026 at 4:16 PM EST

Are you wondering whether to buy Universal Technical Institute or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

We see the value of companies helping consumers, but in the case of Universal Technical Institute, we’re out. First off, its revenue growth was weak over the last five years, and analysts expect its demand to deteriorate over the next 12 months. And while its remarkable EPS growth over the last five years shows its profits are trickling down to shareholders, the downside is its number of new students has disappointed. On top of that, its projected EPS for the next year is lacking.

Universal Technical Institute’s EV-to-EBITDA ratio based on the next 12 months is 14x. This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $37.33 on the company (compared to the current share price of $27.89).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.