Veeva Systems (VEEV)

Veeva Systems piques our interest. Although its sales growth has been weak, its profitability gives it the flexibility to ride out cycles.― StockStory Analyst Team

1. News

2. Summary

Why Veeva Systems Is Interesting

Originally named "Verticals onDemand" before rebranding in 2009, Veeva Systems (NYSE:VEEV) provides cloud software, data solutions, and consulting services that help life sciences companies develop and bring products to market more efficiently.

- Successful business model is illustrated by its impressive operating margin, and its operating leverage amplified its profits over the last year

- Robust free cash flow profile gives it the flexibility to invest in growth initiatives or return capital to shareholders

- One risk is its operating profits and efficiency rose over the last year as it benefited from some fixed cost leverage

Veeva Systems shows some promise. If you’ve been itching to buy the stock, the valuation looks fair.

Why Is Now The Time To Buy Veeva Systems?

Veeva Systems’s stock price of $186.50 implies a valuation ratio of 8.7x forward price-to-sales. While this multiple is higher than most software companies, we think the valuation is fair for the quality you get.

This could be a good time to invest if you think there are underappreciated aspects of the business.

3. Veeva Systems (VEEV) Research Report: Q4 CY2025 Update

Life sciences cloud software provider Veeva Systems (NYSE:VEEV) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 16% year on year to $836 million. Guidance for next quarter’s revenue was better than expected at $856.5 million at the midpoint, 1% above analysts’ estimates. Its non-GAAP profit of $2.06 per share was 6.5% above analysts’ consensus estimates.

Veeva Systems (VEEV) Q4 CY2025 Highlights:

- Revenue: $836 million vs analyst estimates of $810.7 million (16% year-on-year growth, 3.1% beat)

- Adjusted EPS: $2.06 vs analyst estimates of $1.94 (6.5% beat)

- Adjusted Operating Income: $366.5 million vs analyst estimates of $352 million (43.8% margin, 4.1% beat)

- Revenue Guidance for Q1 CY2026 is $856.5 million at the midpoint, above analyst estimates of $847.9 million

- Adjusted EPS guidance for the upcoming financial year 2027 is $8.85 at the midpoint, beating analyst estimates by 3%

- Operating Margin: 29.4%, up from 26.1% in the same quarter last year

- Free Cash Flow Margin: 12.8%, down from 22.5% in the previous quarter

- Market Capitalization: $30.56 billion

Company Overview

Originally named "Verticals onDemand" before rebranding in 2009, Veeva Systems (NYSE:VEEV) provides cloud software, data solutions, and consulting services that help life sciences companies develop and bring products to market more efficiently.

Veeva's solutions are organized into three main categories. Veeva Development Cloud supports the entire R&D process with applications for clinical trials, regulatory submissions, quality management, and safety monitoring. Veeva Commercial Cloud helps pharmaceutical sales and marketing teams engage with healthcare professionals through customer relationship management tools, content management, and analytics. Veeva Data Cloud provides reference data and insights on healthcare providers, organizations, and patients.

The company's technology addresses the unique regulatory and compliance requirements of the pharmaceutical, biotechnology, and medical device industries. For instance, a pharmaceutical company might use Veeva's clinical trial management system to track study progress across multiple research sites while maintaining regulatory compliance, then leverage Veeva CRM to efficiently coordinate communication between its sales representatives and physicians after product approval.

Veeva generates revenue through software subscriptions and professional services. Its professional services teams offer implementation support, training, and strategic consulting to help customers transform their business processes. While primarily focused on life sciences, Veeva has expanded some of its quality and regulatory solutions to serve consumer products companies as well. The company maintains data centers globally to support customers across North America, Europe, Asia, and other regions.

4. Healthcare And Life Sciences Software

The coronavirus pandemic has underscored the importance of high-quality health infrastructure in times of crisis. Coupled with intense competition between drugmakers and the growing volume of data in the health care sector, demand for data management solutions in the healthcare space is expected to remain strong in the years ahead.

Veeva's primary competitor is IQVIA Holdings Inc., which offers competing CRM applications, data products, and analytics services. Other competitors include Dassault Systèmes, OpenText Corporation, Oracle Corporation, and Honeywell International Inc. in various segments of the life sciences software market.

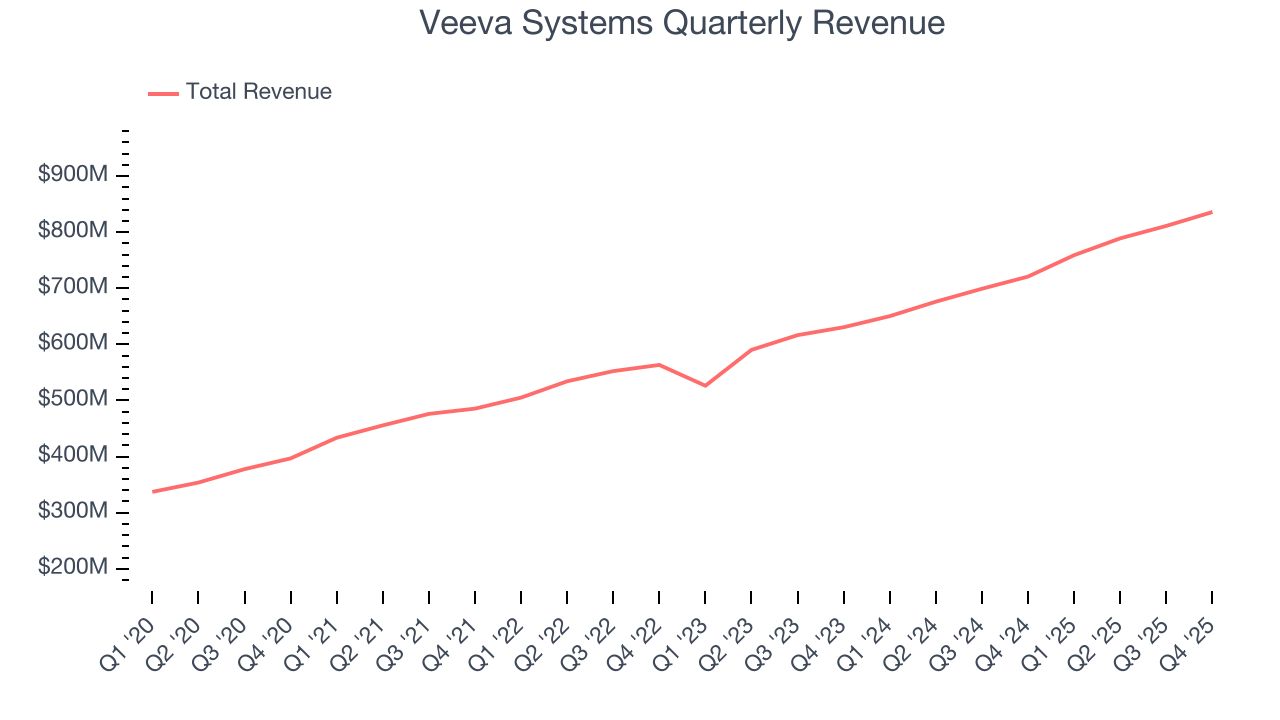

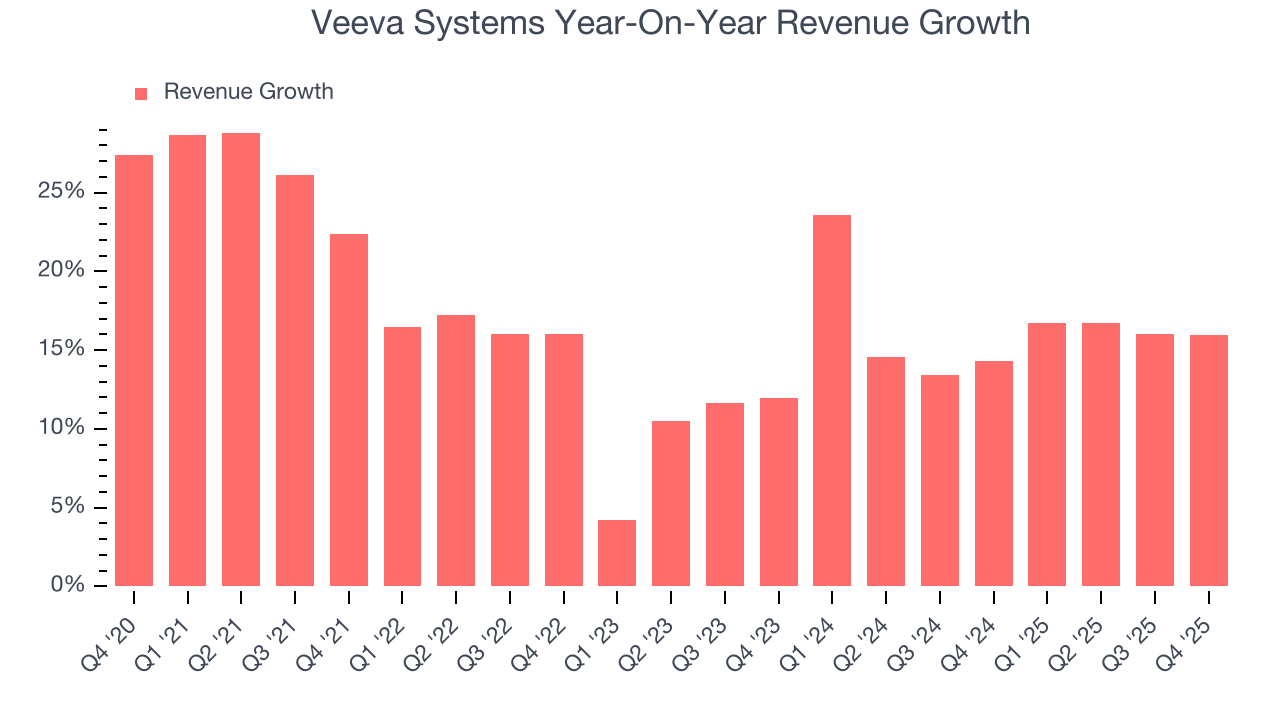

5. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Veeva Systems grew its sales at a 16.9% compounded annual growth rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the software sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded. Luckily, there are other things to like about Veeva Systems.

We at StockStory place the most emphasis on long-term growth, but within software, a half-decade historical view may miss recent innovations or disruptive industry trends. Veeva Systems’s annualized revenue growth of 16.3% over the last two years aligns with its five-year trend, suggesting its demand was stable.

This quarter, Veeva Systems reported year-on-year revenue growth of 16%, and its $836 million of revenue exceeded Wall Street’s estimates by 3.1%. Company management is currently guiding for a 12.8% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 11.4% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and suggests its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

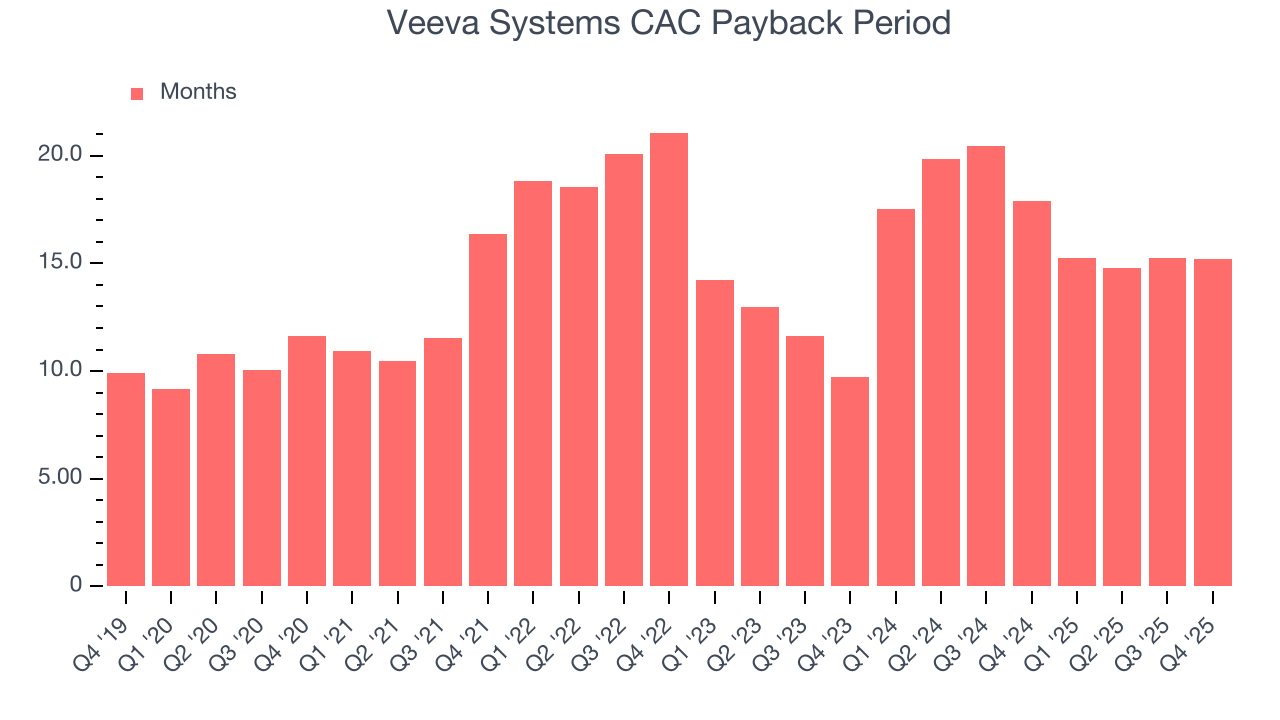

6. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

Veeva Systems is extremely efficient at acquiring new customers, and its CAC payback period checked in at 15.2 months this quarter. The company’s rapid recovery of its customer acquisition costs indicates it has a highly differentiated product offering and a strong brand reputation. These dynamics give Veeva Systems more resources to pursue new product initiatives while maintaining the flexibility to increase its sales and marketing investments.

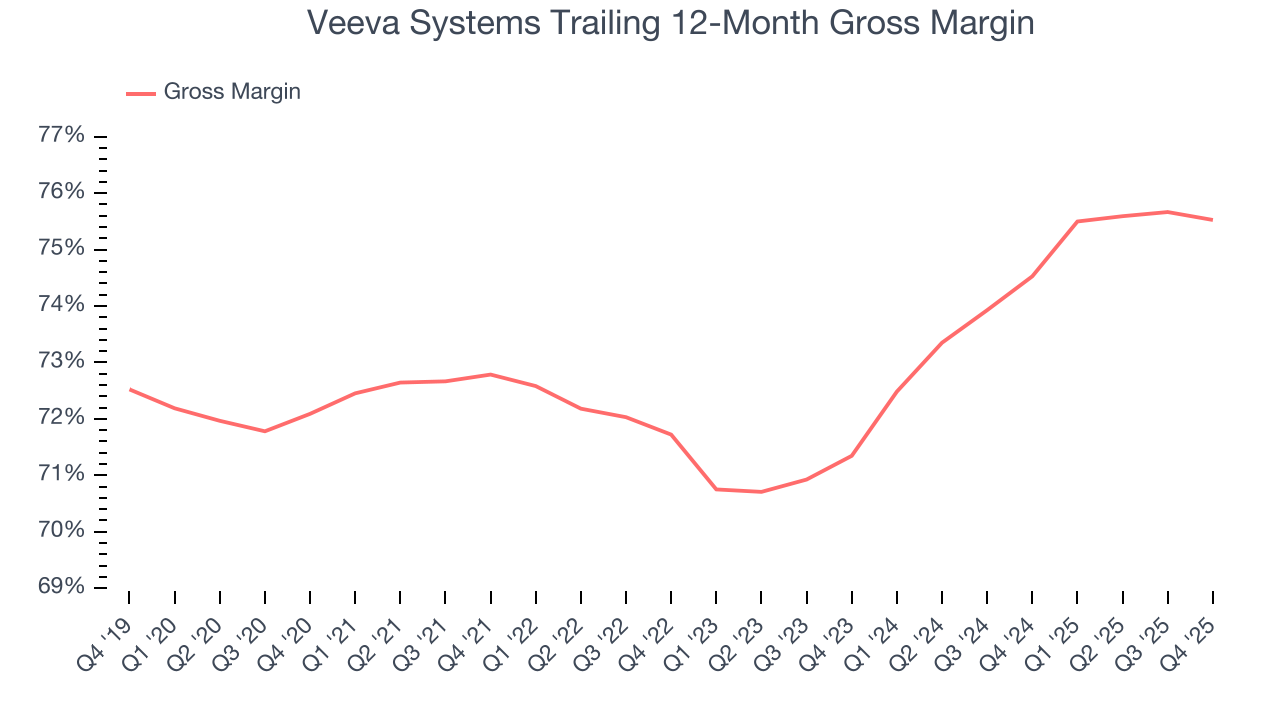

7. Gross Margin & Pricing Power

What makes the software-as-a-service model so attractive is that once the software is developed, it usually doesn’t cost much to provide it as an ongoing service. These minimal costs can include servers, licenses, and certain personnel.

Veeva Systems’s gross margin is good for a software business and points to its solid unit economics, competitive products and services, and lack of meaningful pricing pressure. As you can see below, it averaged an impressive 75.5% gross margin over the last year. Said differently, Veeva Systems paid its providers $24.47 for every $100 in revenue.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. Veeva Systems has seen gross margins improve by 4.2 percentage points over the last 2 year, which is very good in the software space.

This quarter, Veeva Systems’s gross profit margin was 74.5%, in line with the same quarter last year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting its input costs have been stable and it isn’t under pressure to lower prices.

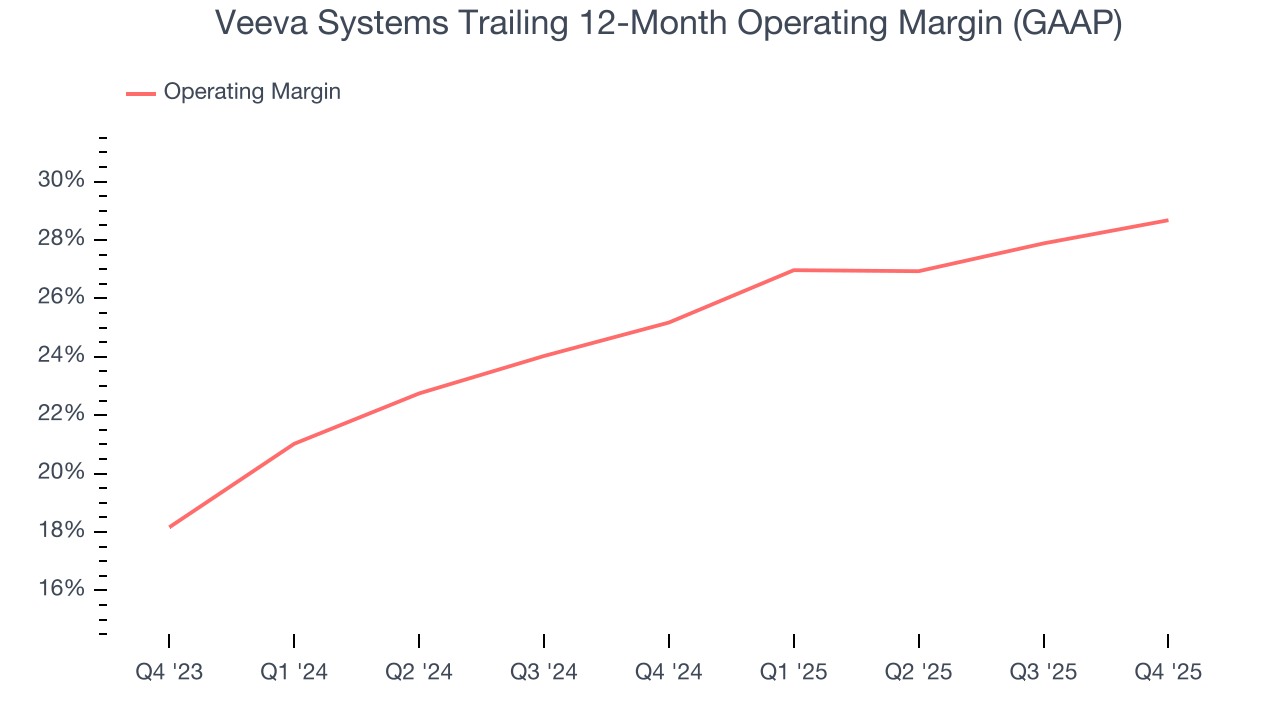

8. Operating Margin

Veeva Systems has been a well-oiled machine over the last year. It demonstrated elite profitability for a software business, boasting an average operating margin of 28.7%. This result isn’t too surprising as its gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Veeva Systems’s operating margin rose by 3.5 percentage points over the last two years, as its sales growth gave it operating leverage.

In Q4, Veeva Systems generated an operating margin profit margin of 29.4%, up 3.3 percentage points year on year. The increase was encouraging, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

9. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

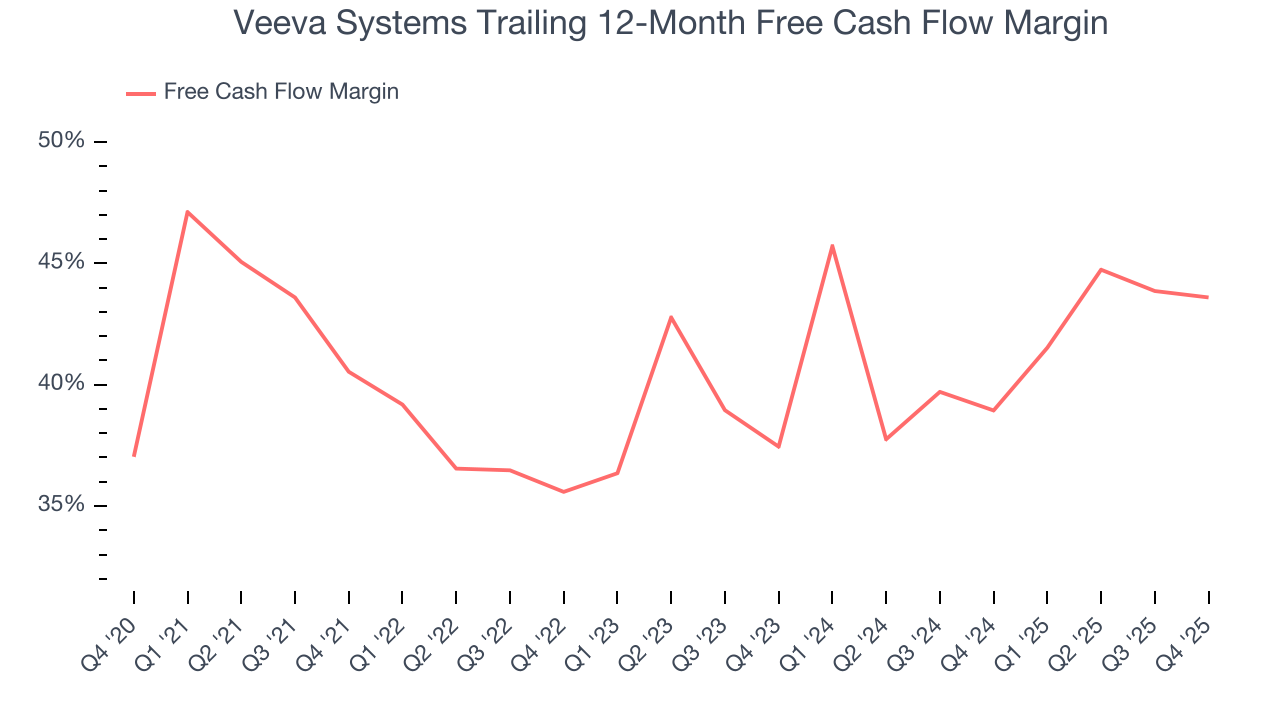

Veeva Systems has shown terrific cash profitability, driven by its lucrative business model and cost-effective customer acquisition strategy that enable it to stay ahead of the competition through investments in new products rather than sales and marketing. The company’s free cash flow margin was among the best in the software sector, averaging an eye-popping 43.6% over the last year. Veeva Systems has shown terrific cash profitability relative to peers over the last year, giving the company fewer opportunities to return capital to shareholders.

Veeva Systems’s free cash flow clocked in at $106.8 million in Q4, equivalent to a 12.8% margin. This result was good as its margin was 3.8 percentage points higher than in the same quarter last year, but we note it was lower than its one-year cash profitability. Nevertheless, we wouldn’t read too much into a single quarter because investment needs can be seasonal, leading to short-term swings. Long-term trends are more important.

Over the next year, analysts’ consensus estimates show they’re expecting Veeva Systems’s free cash flow margin of 43.6% for the last 12 months to remain the same.

10. Balance Sheet Assessment

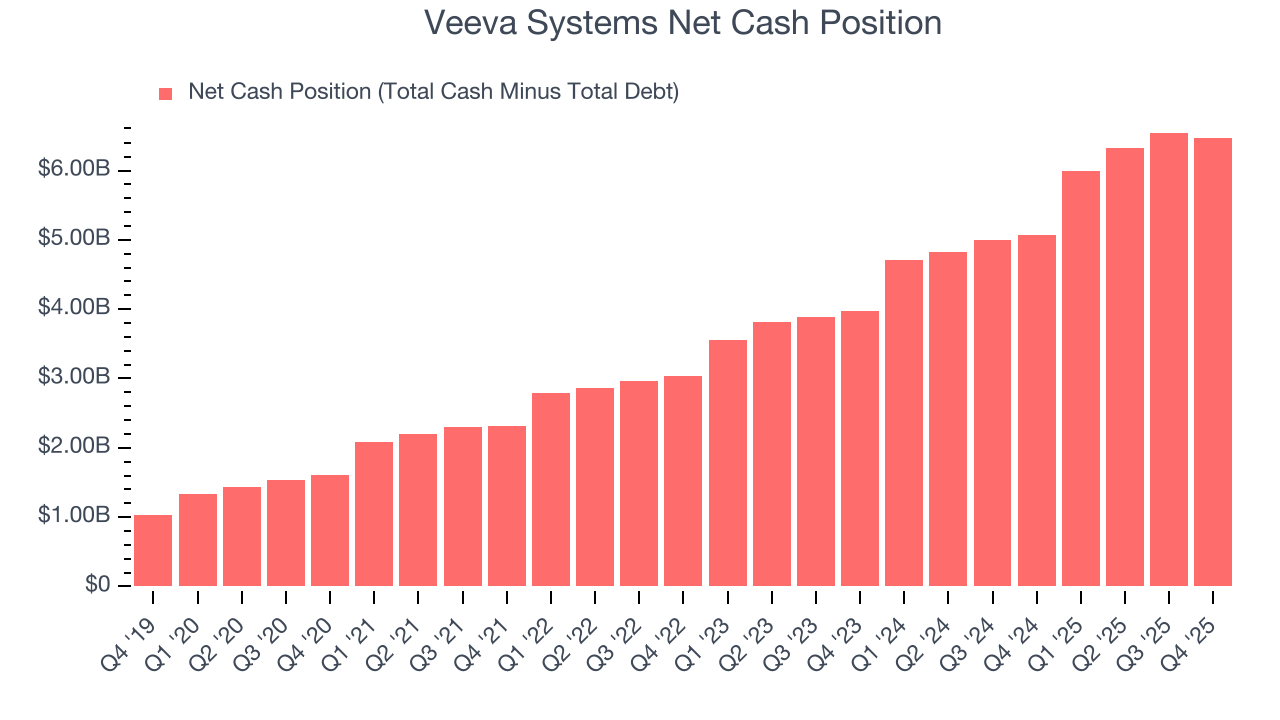

Businesses that maintain a cash surplus face reduced bankruptcy risk.

Veeva Systems is a profitable, well-capitalized company with $6.56 billion of cash and $95.86 million of debt on its balance sheet. This $6.46 billion net cash position is 20.1% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

11. Key Takeaways from Veeva Systems’s Q4 Results

It was great to see Veeva Systems’s full-year EPS guidance top analysts’ expectations. We were also glad its EPS guidance for next quarter exceeded Wall Street’s estimates. On the other hand, its revenue guidance for next year suggests growth will decelerate. Overall, we think this was a solid quarter with some key areas of upside. The stock traded up 8.9% to $205.04 immediately after reporting.

12. Is Now The Time To Buy Veeva Systems?

Updated: March 17, 2026 at 10:12 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Veeva Systems.

In our opinion, Veeva Systems is a solid company. Although its revenue growth was mediocre over the last five years and analysts expect growth to slow over the next 12 months, its bountiful generation of free cash flow empowers it to invest in growth initiatives. And while its expanding operating margin shows it’s becoming more efficient at building and selling its software, its impressive operating margins show it has a highly efficient business model.

Veeva Systems’s price-to-sales ratio based on the next 12 months is 8.7x. Looking at the software landscape right now, Veeva Systems trades at a pretty interesting price. For those confident in the business and its management team, this is a good time to invest.

Wall Street analysts have a consensus one-year price target of $270.93 on the company (compared to the current share price of $186.50), implying they see 45.3% upside in buying Veeva Systems in the short term.