Walmart (WMT)

Walmart doesn’t excite us. Its underwhelming revenue growth and failure to generate meaningful free cash flow is a concerning trend.― StockStory Analyst Team

1. News

2. Summary

Why Walmart Is Not Exciting

Known for its large-format Supercenters, Walmart (NYSE:WMT) is a retail pioneer that serves a budget-conscious consumer who is looking for a wide range of products under one roof.

- Commoditized inventory, bad unit economics, and high competition are reflected in its low gross margin of 24.8%

- Subpar operating margin constrains its ability to invest in process improvements or effectively respond to new competitive threats

- On the plus side, its unparalleled revenue scale of $703.1 billion offsets its poor gross margin and gives it advantageous pricing and terms with suppliers

Walmart doesn’t measure up to our expectations. You should search for better opportunities.

Why There Are Better Opportunities Than Walmart

Walmart is trading at $114.62 per share, or 39.3x forward P/E. This multiple is quite expensive for the quality you get.

Paying up for elite businesses with strong earnings potential is better than investing in lower-quality companies with shaky fundamentals. That’s how you avoid big downside over the long term.

3. Walmart (WMT) Research Report: Q3 CY2025 Update

Retail behemoth Walmart (NYSE:WMT) announced better-than-expected revenue in Q3 CY2025, with sales up 5.8% year on year to $179.5 billion. Its non-GAAP profit of $0.62 per share was 3.2% above analysts’ consensus estimates.

Walmart (WMT) Q3 CY2025 Highlights:

- Revenue: $179.5 billion vs analyst estimates of $177.5 billion (5.8% year-on-year growth, 1.1% beat)

- Adjusted EPS: $0.62 vs analyst estimates of $0.60 (3.2% beat)

- Management raised its full-year Adjusted EPS guidance to $2.61 at the midpoint, a 1.4% increase

- Operating Margin: 3.7%, in line with the same quarter last year

- Free Cash Flow Margin: 1%, similar to the same quarter last year

- Same-Store Sales rose 4.5% year on year (5.5% in the same quarter last year)

- Market Capitalization: $802.1 billion

Company Overview

Known for its large-format Supercenters, Walmart (NYSE:WMT) is a retail pioneer that serves a budget-conscious consumer who is looking for a wide range of products under one roof.

Founded in 1962 by Sam Walton in Bentonville, Arkansas, Walmart is currently one of the world's largest retailers. The company is known for its "Everyday Low Prices" strategy, which is achieved through bulk purchasing, cost efficiency, and optimizing supply chain management.

Walmart serves the value-focused household in suburban and rural areas by offering low prices and convenience. Convenience from the core Supercenter concept stems from offering everything from groceries to clothing to toys to home décor to consumer electronics under one roof. Recent initiatives to add convenience to the Walmart shopping experience include launching the ecommerce site in 2000, online grocery order and physical pickup in 2014, and grocery delivery in 2018.

While the Walmart Supercenter—which can be 200,000 square feet per store—is the most famous format, the company also has smaller formats and other banners such as the Sam’s Club membership warehouse concept. For example, the company launched Walmart Neighborhood Markets in 1998. These stores were meant for more dense urban areas where a large format store would not be feasible, and the limited space was dedicated primarily to groceries and pharmacy services.

4. Large-format Grocery & General Merchandise Retailer

Big-box retailers operate large stores that sell groceries and general merchandise at highly competitive prices. Because of their scale and resulting purchasing power, these big-box retailers–with annual sales in the tens to hundreds of billions of dollars–are able to get attractive volume discounts and sell at often the lowest prices. While e-commerce is a threat, these retailers have been able to weather the storm by either providing a unique in-store shopping experience or by reinvesting their hefty profits into omnichannel investments.

Scaled competitors that sell general merchandise and/or groceries to US consumers include Amazon.com (NASDAQ:AMZN), Costco (NYSE:COST), and Dollar General (NYSE:DG).

5. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

With $703.1 billion in revenue over the past 12 months, Walmart is a behemoth in the consumer retail sector and benefits from economies of scale, giving it an edge in distribution. This also enables it to gain more leverage on its fixed costs than smaller competitors and the flexibility to offer lower prices. However, its scale is a double-edged sword because it’s harder to find incremental growth when you’ve penetrated most of the market. To expand meaningfully, Walmart likely needs to tweak its prices or enter new markets.

As you can see below, Walmart’s 5.1% annualized revenue growth over the last six years (we compare to 2019 to normalize for COVID-19 impacts) was tepid, but to its credit, it opened new stores and increased sales at existing, established locations.

This quarter, Walmart reported year-on-year revenue growth of 5.8%, and its $179.5 billion of revenue exceeded Wall Street’s estimates by 1.1%.

Looking ahead, sell-side analysts expect revenue to grow 4.6% over the next 12 months, similar to its six-year rate. This projection is particularly noteworthy for a company of its scale and implies the market sees success for its products.

6. Store Performance

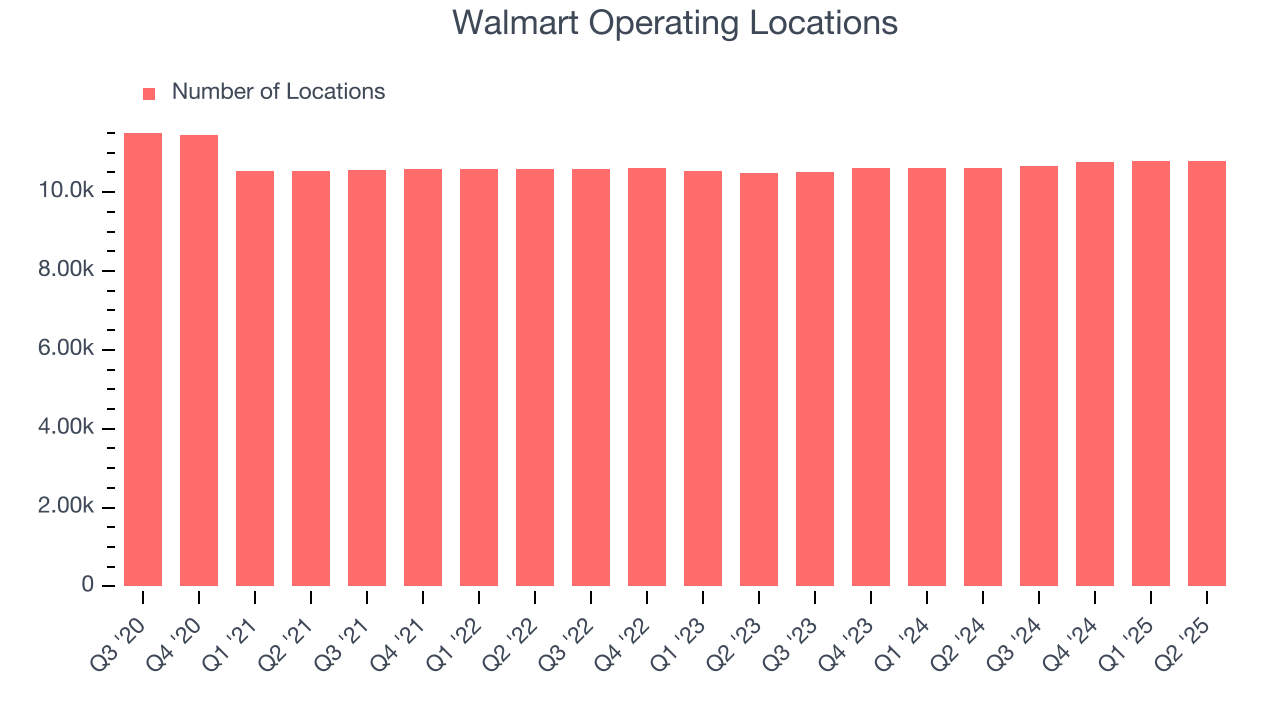

Number of Stores

A retailer’s store count influences how much it can sell and how quickly revenue can grow.

Over the last two years, Walmart has generally opened new stores, averaging 1.2% annual growth. This was faster than the broader consumer retail sector.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

Note that Walmart reports its store count intermittently, so some data points are missing in the chart below.

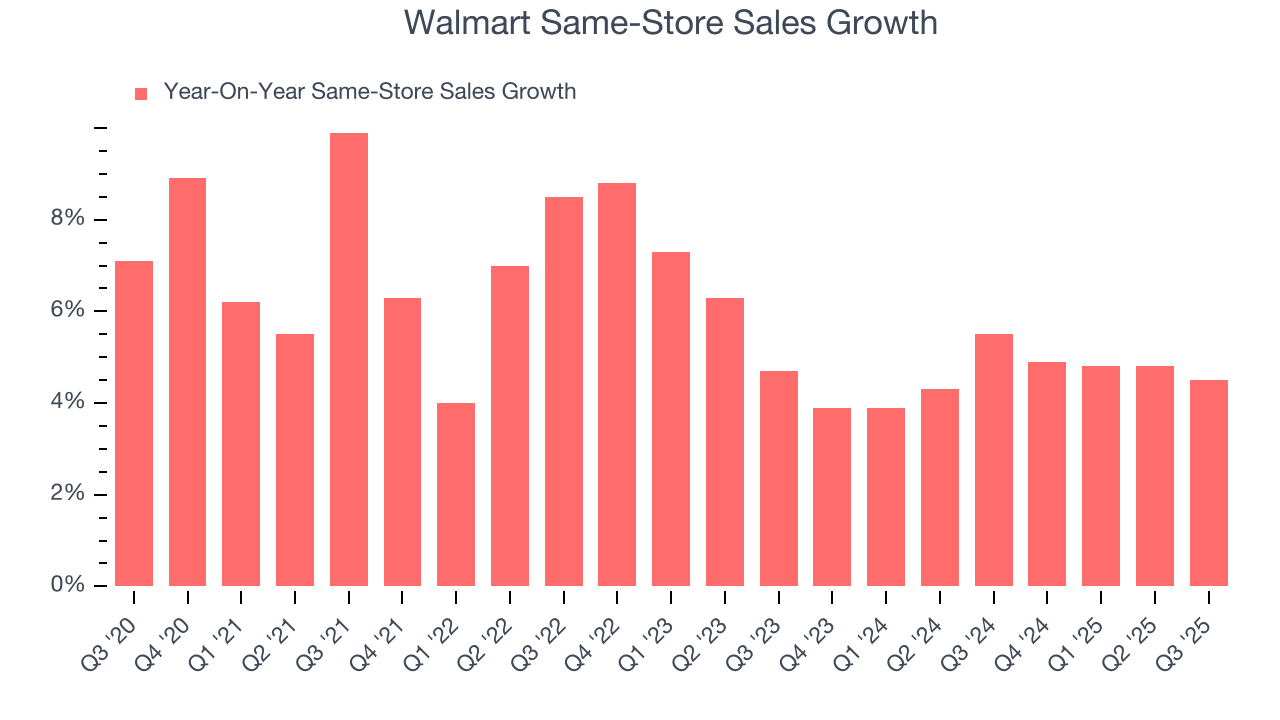

Same-Store Sales

A company's store base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales provides a deeper understanding of this issue because it measures organic growth at brick-and-mortar shops for at least a year.

Walmart has been one of the most successful retailers over the last two years thanks to skyrocketing demand within its existing locations. On average, the company has posted exceptional year-on-year same-store sales growth of 4.6%. This performance suggests its measured rollout of new stores is beneficial for shareholders. We like this backdrop because it gives Walmart multiple ways to win: revenue growth can come from new stores, e-commerce, or increased foot traffic and higher sales per customer at existing locations.

In the latest quarter, Walmart’s same-store sales rose 4.5% year on year. This performance was more or less in line with its historical levels.

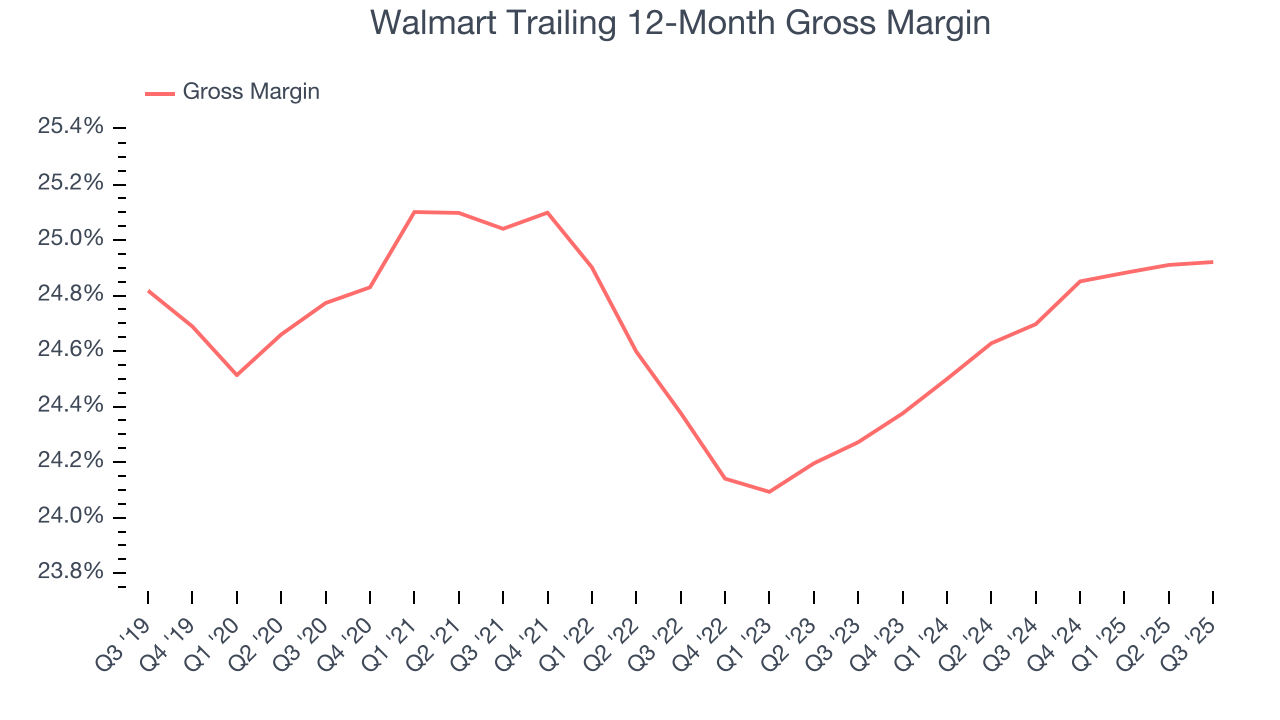

7. Gross Margin & Pricing Power

At StockStory, we prefer high gross margin businesses because they indicate pricing power or differentiated products, giving the company a chance to generate higher operating profits.

Walmart has bad unit economics for a retailer, signaling it operates in a competitive market and lacks pricing power because its inventory is sold in many places. As you can see below, it averaged a 24.8% gross margin over the last two years.

Non-discretionary retailers, however, must be viewed through a different lens because they compete on the lowest price, sell products easily found elsewhere, and have high transportation costs to move goods. These dynamics lead to structurally lower gross margins, so the best metrics to assess them are free cash flow margin, operating leverage, and profit volatility, which account for their scale advantages and non-cyclical demand.

Walmart produced a 25% gross profit margin in Q3, in line with the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting it strives to keep prices low for customers and has stable input costs (such as labor and freight expenses to transport goods).

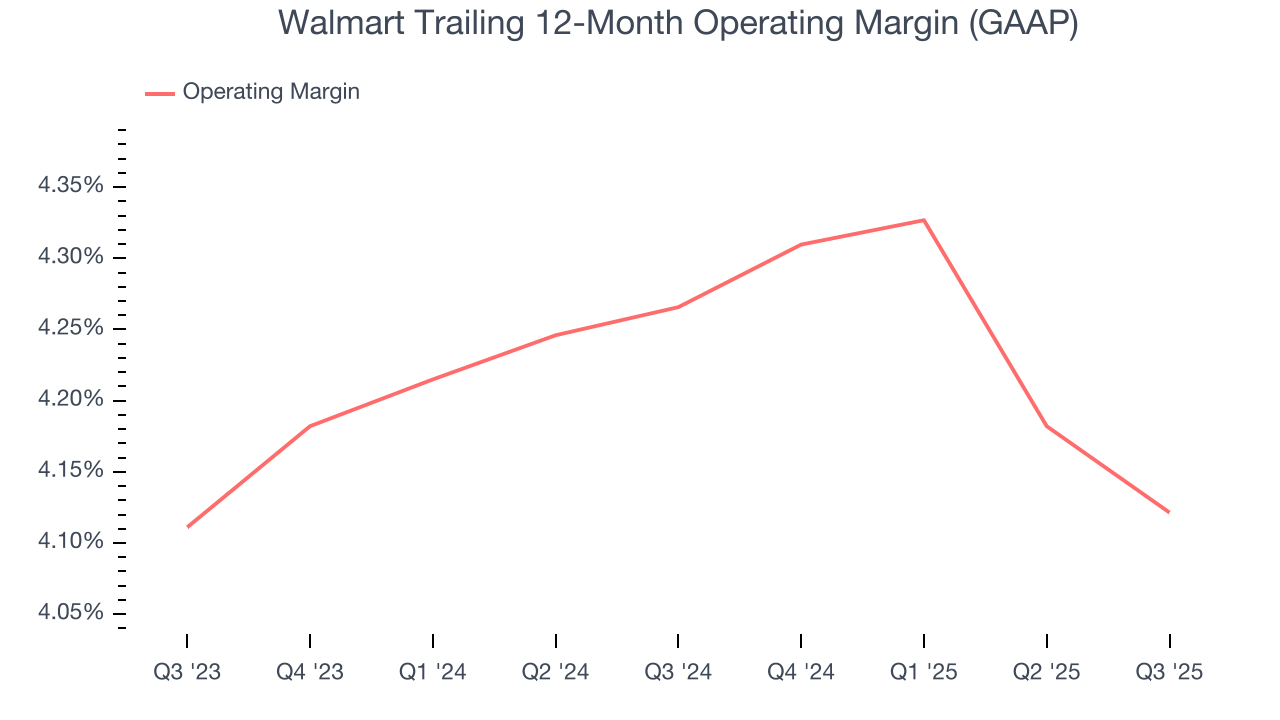

8. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Walmart’s operating margin might fluctuated slightly over the last 12 months but has generally stayed the same, averaging 4.2% over the last two years. This profitability was lousy for a consumer retail business and caused by its suboptimal cost structureand low gross margin.

Looking at the trend in its profitability, Walmart’s operating margin might fluctuated slightly but has generally stayed the same over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q3, Walmart generated an operating margin profit margin of 3.7%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

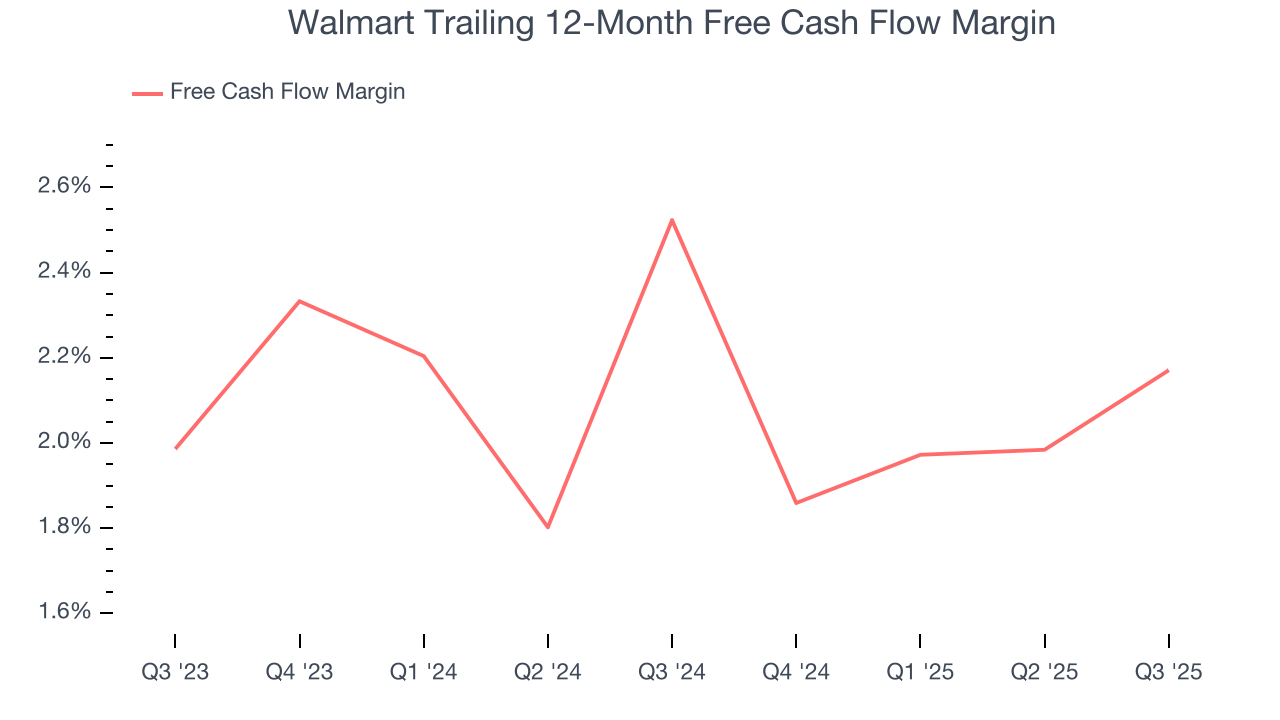

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Walmart has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 2.3% over the last two years, slightly better than the broader consumer retail sector.

Walmart’s free cash flow clocked in at $1.88 billion in Q3, equivalent to a 1% margin. This cash profitability was in line with the comparable period last year but below its two-year average. We wouldn’t put too much weight on it because investment needs can be seasonal, causing short-term swings. Long-term trends trump temporary fluctuations.

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Walmart’s management team makes decent investment decisions and generates value for shareholders. Its five-year average ROIC was 16.4%, slightly better than typical consumer retail business.

11. Balance Sheet Assessment

Walmart reported $10.58 billion of cash and $68.42 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $43.3 billion of EBITDA over the last 12 months, we view Walmart’s 1.3× net-debt-to-EBITDA ratio as safe. We also see its $1.23 billion of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Walmart’s Q3 Results

It was encouraging to see Walmart beat analysts’ revenue expectations this quarter on healthy same-store sales growth. We were also happy its gross margin outperformed Wall Street’s estimates. The last positive was that the company lifted full-year guidance. The company saw some weakness when Supplemental Nutrition Assistance Program (SNAP) benefits were paused during the government shutdown. Overall, this was a decent quarter. The market seemed to be expecting more though, and the stock traded down 2.2% to $98.45 immediately following the results.

13. Is Now The Time To Buy Walmart?

Updated: December 4, 2025 at 9:40 PM EST

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

Walmart has some positive attributes, but it isn’t one of our picks. Although its revenue growth was a little slower over the last three years, its coveted brand awareness makes it a household name consumers consistently turn to. Tread carefully with this one, however, as its gross margins make it more challenging to reach positive operating profits compared to other consumer retail businesses.

Walmart’s P/E ratio based on the next 12 months is 40x. This multiple tells us a lot of good news is priced in - we think there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $118.79 on the company (compared to the current share price of $114.88).