Yelp (YELP)

We’re cautious of Yelp. Its sluggish sales growth shows demand is soft, a worrisome sign for investors in high-quality stocks.― StockStory Analyst Team

1. News

2. Summary

Why Yelp Is Not Exciting

Founded by PayPal alumni Jeremy Stoppelman and Russel Simmons, Yelp (NYSE:YELP) is an online platform that helps people discover local businesses through crowd-sourced reviews.

- Demand is forecasted to shrink as its estimated sales for the next 12 months are flat

- Lackluster 7.1% annual revenue growth over the last three years indicates the company is losing ground to competitors

- One positive is that its prominent and differentiated platform results in a best-in-class gross margin of 90.7%

Yelp’s quality isn’t up to par. We’d search for superior opportunities elsewhere.

Why There Are Better Opportunities Than Yelp

Yelp is trading at $23.83 per share, or 3.7x forward EV/EBITDA. This is a cheap valuation multiple, but for good reason. You get what you pay for.

Cheap stocks can look like a great deal at first glance, but they can be value traps. They often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. Yelp (YELP) Research Report: Q4 CY2025 Update

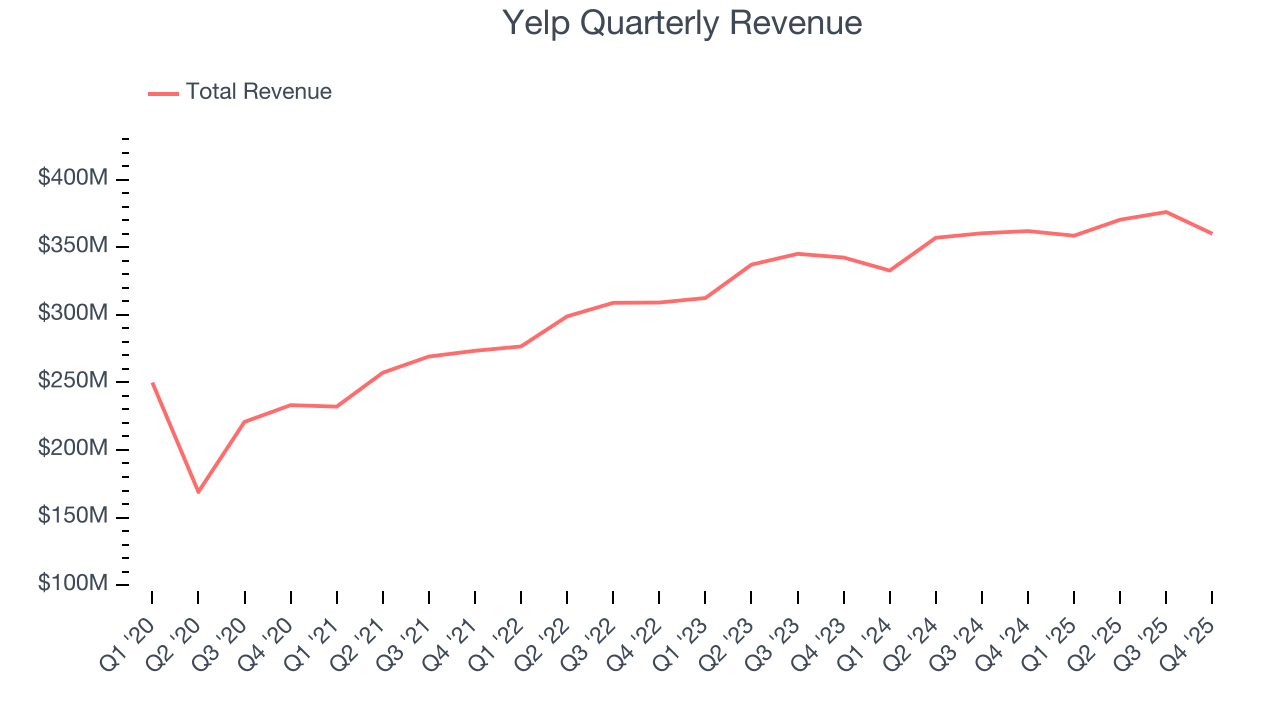

Local business platform Yelp (NYSE:YELP) met Wall Street’s revenue expectations in Q4 CY2025, but sales were flat year on year at $360 million. On the other hand, the company’s full-year revenue guidance of $1.47 billion at the midpoint came in 2.8% below analysts’ estimates. Its GAAP profit of $0.61 per share was 13.9% above analysts’ consensus estimates.

Yelp (YELP) Q4 CY2025 Highlights:

- Revenue: $360 million vs analyst estimates of $359.6 million (flat year on year, in line)

- EPS (GAAP): $0.61 vs analyst estimates of $0.54 (13.9% beat)

- Adjusted EBITDA: $85.69 million vs analyst estimates of $80.98 million (23.8% margin, 5.8% beat)

- EBITDA guidance for the upcoming financial year 2026 is $320 million at the midpoint, below analyst estimates of $357.5 million

- Operating Margin: 13.6%, down from 14.8% in the same quarter last year

- Free Cash Flow Margin: 20.1%, down from 31.6% in the previous quarter

- Market Capitalization: $1.43 billion

Company Overview

Founded by PayPal alumni Jeremy Stoppelman and Russel Simmons, Yelp (NYSE:YELP) is an online platform that helps people discover local businesses through crowd-sourced reviews.

Yelp is an online platform that provides consumer ratings, reviews, and photos of millions of local businesses. Consumers benefit from a network effect as the more users of the platform the more reviews get generated over time, improving the overall quality of Yelp’s platform.

For businesses, Yelp offers both free and paid products to engage with potential customers. Any business can register for a free account by claiming their businesses’ listing page and providing basic information. They can also respond to reviews (especially negative ones).

Yelp also offers paid advertising for businesses to promote themselves through premium services such as targeted search advertising and add-ons to their listing pages. Some examples include the ability to order food, make reservations at restaurants, and submit a “Request-A-Quote” for home and local services. Yelp also provides businesses with analytics regarding store-level visits through integrations with third-party data providers.

4. Social Networking

Businesses must meet their customers where they are, which over the past decade has come to mean on social networks. In 2020, users spent over 2.5 hours a day on social networks, a figure that has increased every year since measurement began. As a result, businesses continue to shift their advertising and marketing dollars online.

Yelp competes with online advertising platforms Google (NASDAQ:GOOGL) and Meta Platforms (NASDAQ:META), along with home services lead generation players like ANGI (NASDAQ:ANGI), and Porch Group (NASDAQ:PRCH).

5. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last three years, Yelp grew its sales at a tepid 7.1% compounded annual growth rate. This was below our standard for the consumer internet sector and is a tough starting point for our analysis.

This quarter, Yelp’s $360 million of revenue was flat year on year and in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 2.8% over the next 12 months, a deceleration versus the last three years. This projection doesn't excite us and implies its products and services will see some demand headwinds.

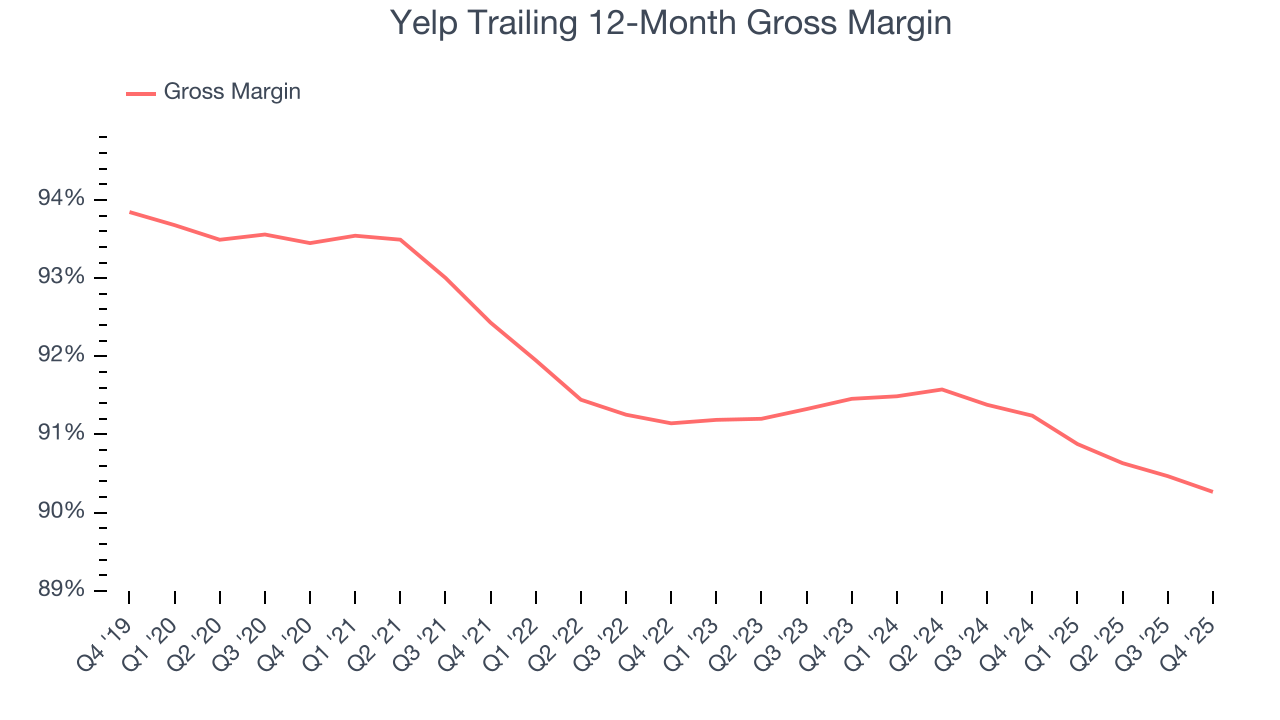

6. Gross Margin & Pricing Power

For social network businesses like Yelp, gross profit tells us how much money the company gets to keep after covering the base cost of its products and services, which typically include customer service, data center, and other infrastructure expenses.

Yelp’s gross margin is one of the highest in the consumer internet sector, an output of its asset-lite business model and strong pricing power. It also enables the company to fund large investments in product and marketing during periods of rapid growth to achieve higher profits in the future. As you can see below, it averaged an elite 90.7% gross margin over the last two years. That means Yelp only paid its providers $9.26 for every $100 in revenue.

Yelp produced a 90% gross profit margin in Q4, in line with the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs have been stable and it isn’t under pressure to lower prices.

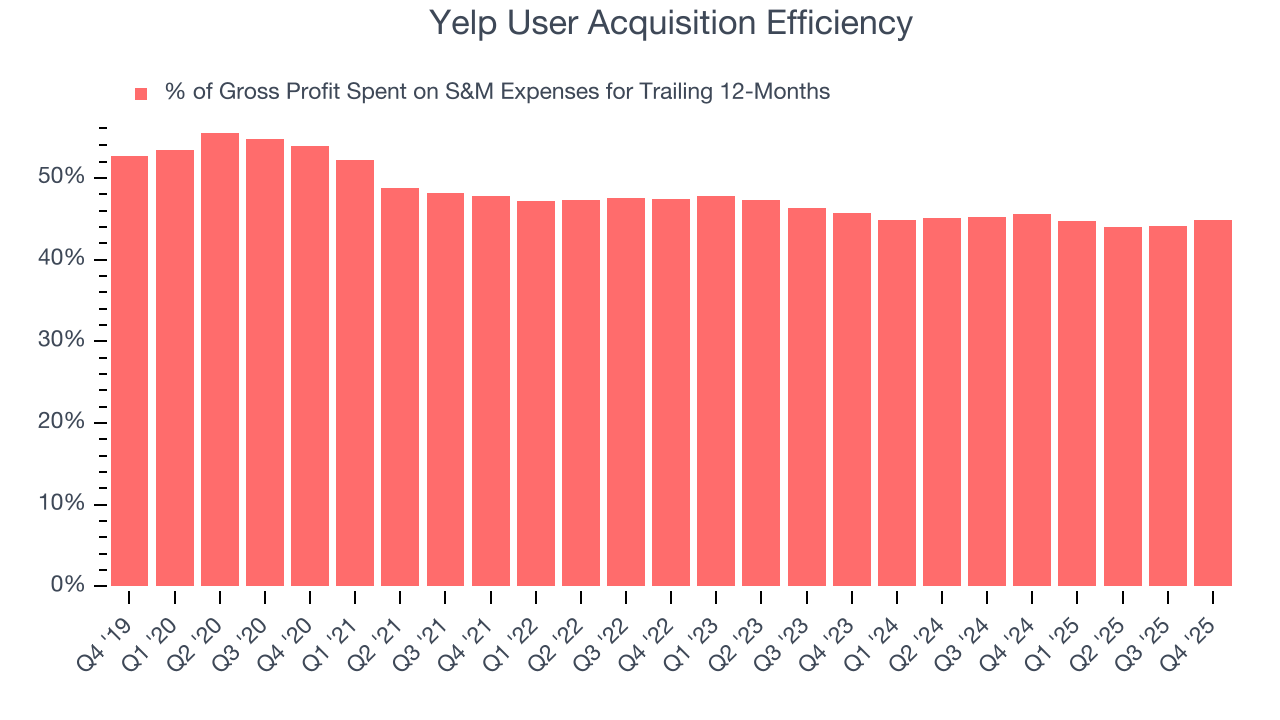

7. User Acquisition Efficiency

Consumer internet businesses like Yelp grow from a combination of product virality, paid advertisement, and incentives (unlike enterprise software products, which are often sold by dedicated sales teams).

Yelp does a decent job acquiring new users, spending 44.8% of its gross profit on sales and marketing expenses over the last year. This decent efficiency indicates relatively solid competitive positioning, giving Yelp the freedom to invest its resources into new growth initiatives.

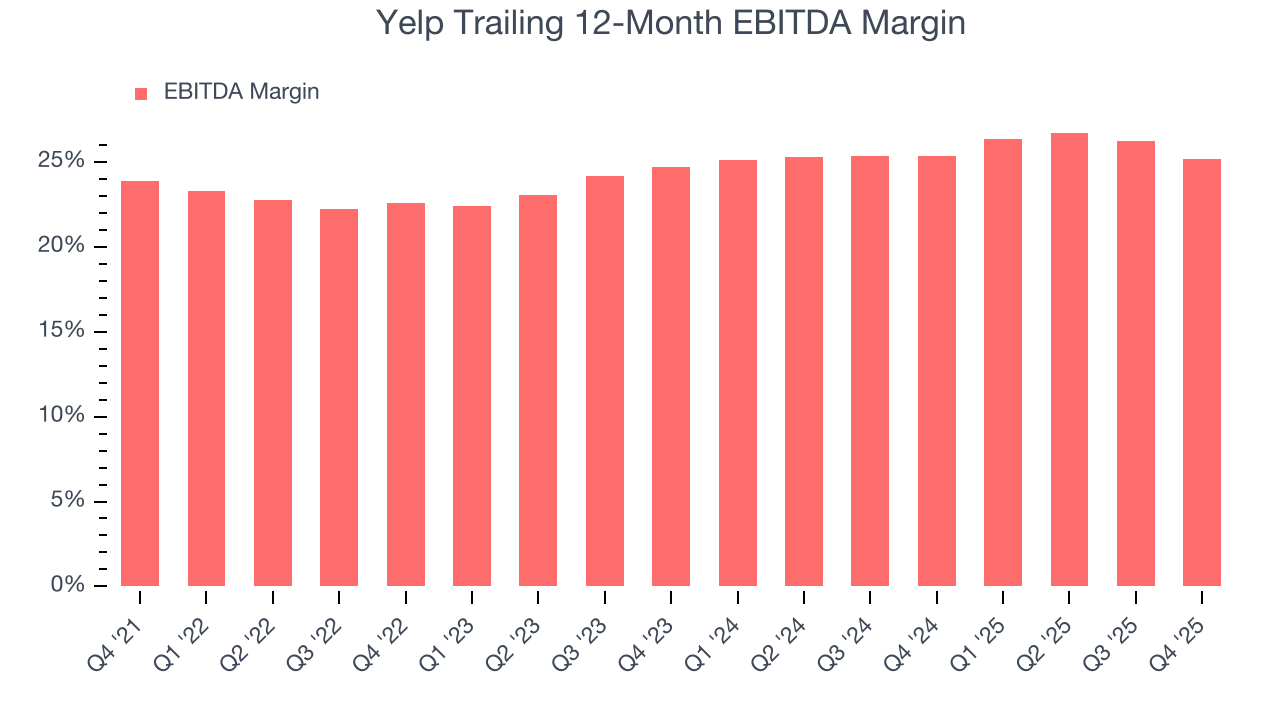

8. EBITDA

Investors frequently analyze operating income to understand a business’s core profitability. Similar to operating income, EBITDA is a common profitability metric for consumer internet companies because it removes various one-time or non-cash expenses, offering a more normalized view of profit potential.

Yelp has been a well-oiled machine over the last two years. It demonstrated elite profitability for a consumer internet business, boasting an average EBITDA margin of 25.3%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Yelp’s EBITDA margin rose by 2.6 percentage points over the last few years, as its sales growth gave it operating leverage.

This quarter, Yelp generated an EBITDA margin profit margin of 23.8%, down 4.1 percentage points year on year. Since Yelp’s EBITDA margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

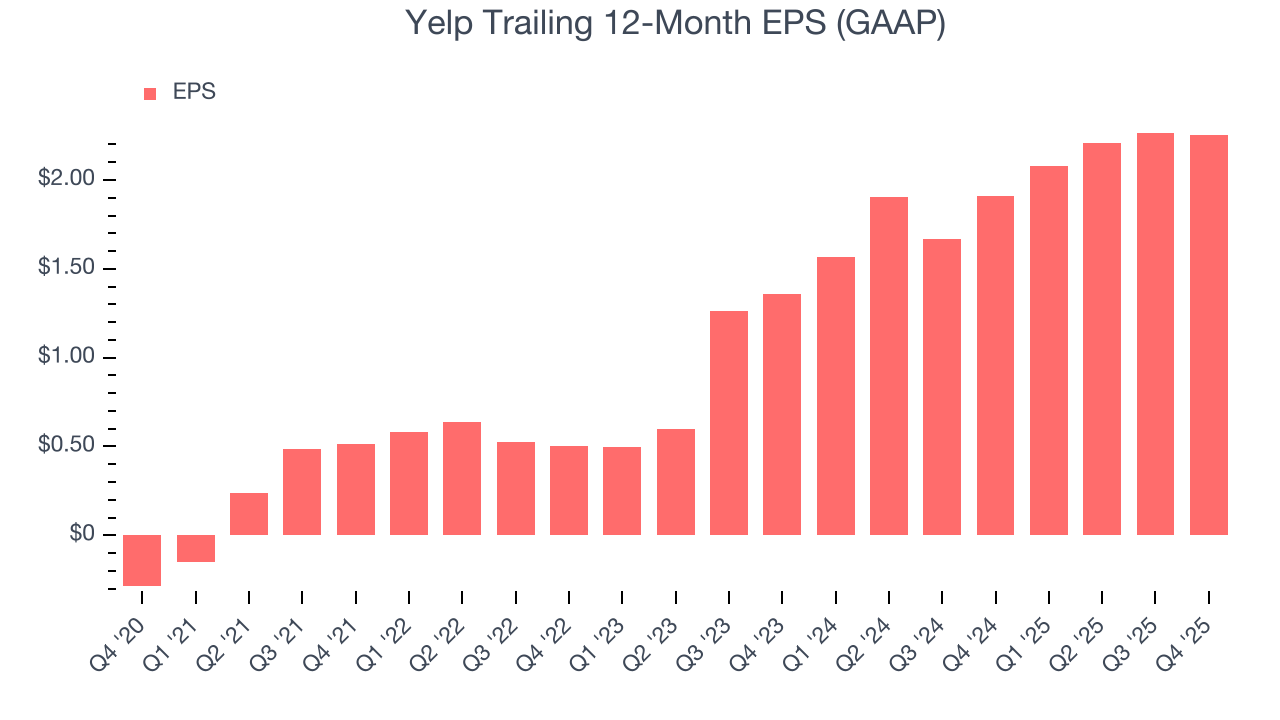

9. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Yelp’s EPS grew at an astounding 64.8% compounded annual growth rate over the last three years, higher than its 7.1% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

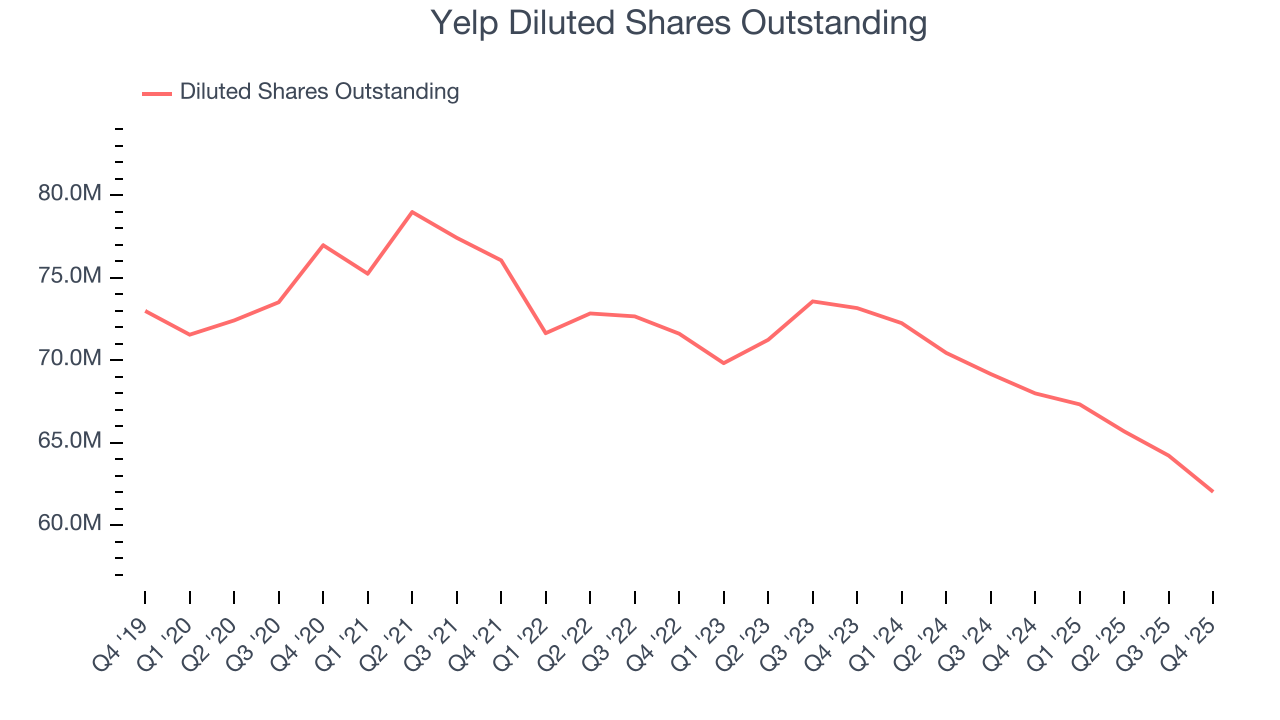

We can take a deeper look into Yelp’s earnings quality to better understand the drivers of its performance. As we mentioned earlier, Yelp’s EBITDA margin declined this quarter but expanded by 2.6 percentage points over the last three years. Its share count also shrank by 13.4%, and these factors together are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

In Q4, Yelp reported EPS of $0.61, down from $0.62 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Yelp’s full-year EPS of $2.26 to grow 19.2%.

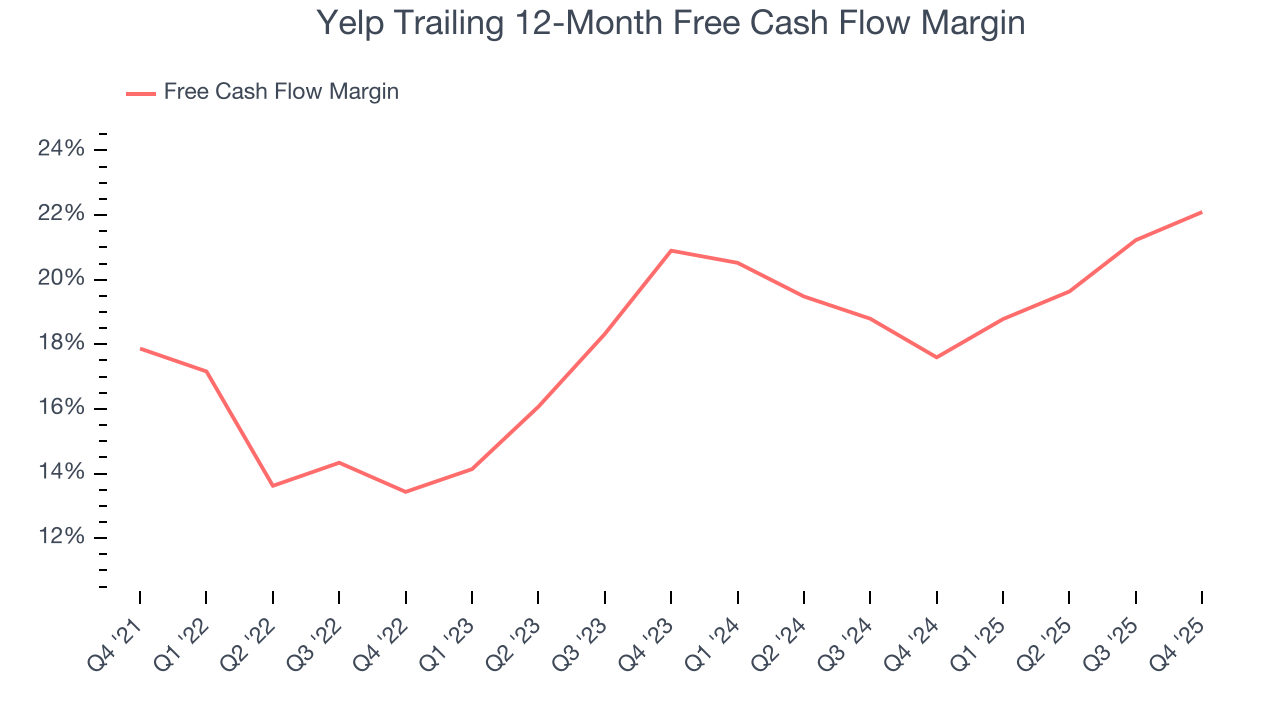

10. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Yelp has shown robust cash profitability, driven by its attractive business model that enables it to reinvest or return capital to investors while maintaining a cash cushion. The company’s free cash flow margin averaged 19.9% over the last two years, quite impressive for a consumer internet business.

Taking a step back, we can see that Yelp’s margin expanded by 8.7 percentage points over the last few years. This shows the company is heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

Yelp’s free cash flow clocked in at $72.27 million in Q4, equivalent to a 20.1% margin. This result was good as its margin was 3.5 percentage points higher than in the same quarter last year, building on its favorable historical trend.

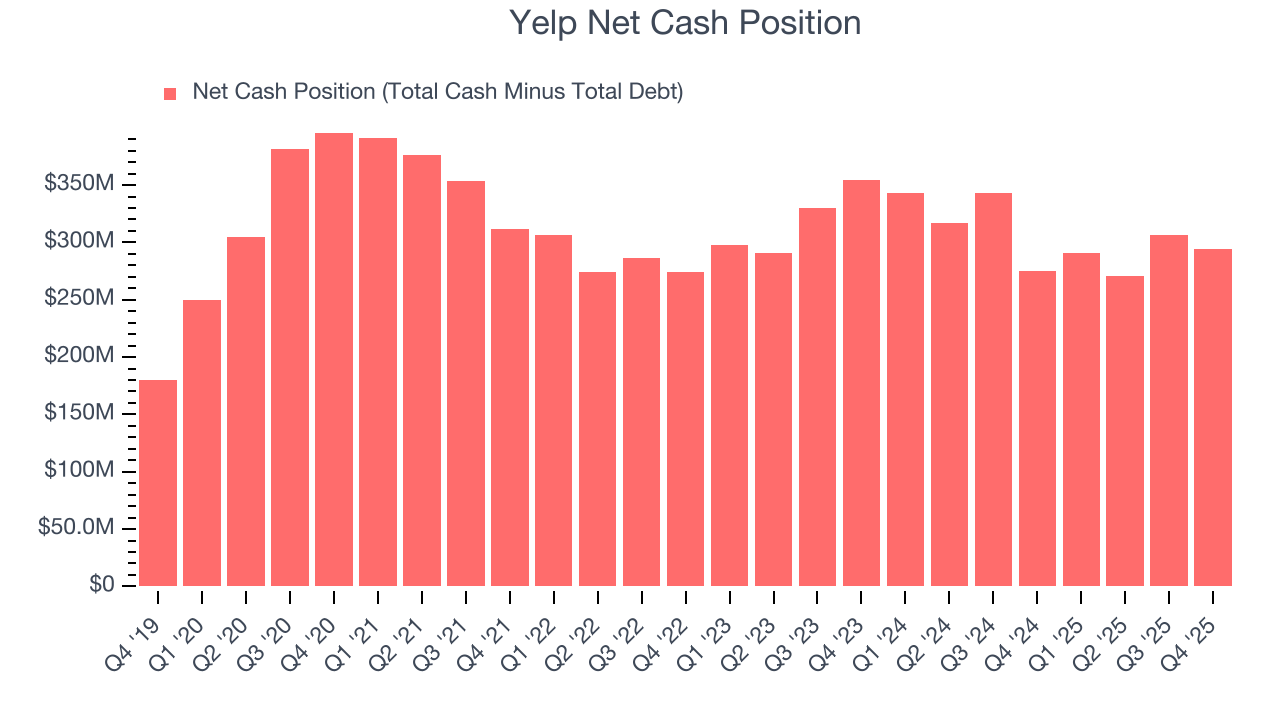

11. Balance Sheet Assessment

Companies with more cash than debt have lower bankruptcy risk.

Yelp is a profitable, well-capitalized company with $319.4 million of cash and $24.88 million of debt on its balance sheet. This $294.5 million net cash position is 20.6% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from Yelp’s Q4 Results

We enjoyed seeing Yelp beat analysts’ EBITDA expectations this quarter. On the other hand, its full-year revenue guidance missed and its full-year EBITDA guidance fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 6.2% to $21.40 immediately after reporting.

13. Is Now The Time To Buy Yelp?

Updated: March 14, 2026 at 10:18 PM EDT

Before making an investment decision, investors should account for Yelp’s business fundamentals and valuation in addition to what happened in the latest quarter.

Yelp isn’t a terrible business, but it doesn’t pass our bar. To kick things off, its revenue growth was uninspiring over the last three years, and analysts expect its demand to deteriorate over the next 12 months. And while Yelp’s admirable gross margins are a wonderful starting point for the overall profitability of the business, its projected EPS for the next year is lacking.

Yelp’s EV/EBITDA ratio based on the next 12 months is 3.7x. This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're fairly confident there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $25.50 on the company (compared to the current share price of $23.83).