CLEAR Secure (YOU)

We like CLEAR Secure. Its rare ability to win market share while pumping out profits is a feature many competitors envy.― StockStory Analyst Team

1. News

2. Summary

Why We Like CLEAR Secure

Recognized by its signature blue lanes and biometric pods at airport checkpoints across America, CLEAR Secure (NYSE:YOU) provides biometric identity verification technology that allows subscribers to bypass regular security lines at airports and access secure experiences at various venues.

- Fast payback periods on sales and marketing expenses allow the company to invest heavily and onboard many customers concurrently

- Excellent operating margin highlights the strength of its business model, and its rise over the last year was fueled by some leverage on its fixed costs

- Robust free cash flow profile gives it the flexibility to invest in growth initiatives or return capital to shareholders

CLEAR Secure is a market leader. The valuation seems fair when considering its quality, so this could be a good time to buy some shares.

Why Is Now The Time To Buy CLEAR Secure?

CLEAR Secure is trading at $33.75 per share, or 3.3x forward price-to-sales. This multiple is cheap, and we think the stock is a bargain considering its quality characteristics.

A powerful double-play is a business that can both grow earnings and achieve a loftier multiple over time. Elite companies trading at meaningful discounts are good ways to set up this play.

3. CLEAR Secure (YOU) Research Report: Q4 CY2025 Update

Identity verification company CLEAR Secure (NYSE:YOU) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 16.7% year on year to $240.8 million. Its GAAP profit of $0.31 per share was in line with analysts’ consensus estimates.

CLEAR Secure (YOU) Q4 CY2025 Highlights:

- Revenue: $240.8 million vs analyst estimates of $235.7 million (16.7% year-on-year growth, 2.1% beat)

- EPS (GAAP): $0.31 vs analyst estimates of $0.31 (in line)

- Adjusted EBITDA: $79.87 million vs analyst estimates of $68.28 million (33.2% margin, 17% beat)

- Operating Margin: 22.4%, up from 16.5% in the same quarter last year

- Free Cash Flow was $187.4 million, up from -$53.47 million in the previous quarter

- Market Capitalization: $3.27 billion

Company Overview

Recognized by its signature blue lanes and biometric pods at airport checkpoints across America, CLEAR Secure (NYSE:YOU) provides biometric identity verification technology that allows subscribers to bypass regular security lines at airports and access secure experiences at various venues.

The company's flagship service is CLEAR Plus, a subscription-based offering that lets members use dedicated security lanes at airports nationwide. When using CLEAR Plus, members verify their identity through biometric technology (facial recognition or fingerprints) at specialized kiosks rather than showing physical IDs to security personnel. After verification, CLEAR Ambassadors escort members to the front of security screening lines, significantly reducing wait times.

Beyond airports, CLEAR has expanded its platform through its CLEAR1 B2B offering, allowing businesses to integrate CLEAR's identity verification technology into their own customer experiences. This service operates on a "verify once, use everywhere" model, enabling frictionless transactions across various sectors including healthcare, financial services, and hospitality.

The company generates revenue primarily through its CLEAR Plus annual subscriptions (priced at $199 per year), with discounts available for airline frequent fliers and American Express cardholders. Additional revenue comes from TSA PreCheck enrollment services and transaction fees from business partners using the CLEAR1 platform.

CLEAR's network effect strengthens as it adds both members and partner locations—greater membership makes the platform more attractive to potential business partners, while more usage locations increase the value proposition for consumers. The company's physical presence in airports also serves as its most effective customer acquisition channel, with in-person enrollments accounting for the majority of new memberships.

4. Data Analytics

Organizations generate a lot of data that is stored in silos, often in incompatible formats, making it slow and costly to extract actionable insights, which in turn drives demand for modern cloud-based data analysis platforms that can efficiently analyze the siloed data.

CLEAR Secure's competitors include government-operated trusted traveler programs like TSA PreCheck and Global Entry, as well as emerging biometric identity verification companies such as IDEMIA and Telos ID that operate in similar spaces.

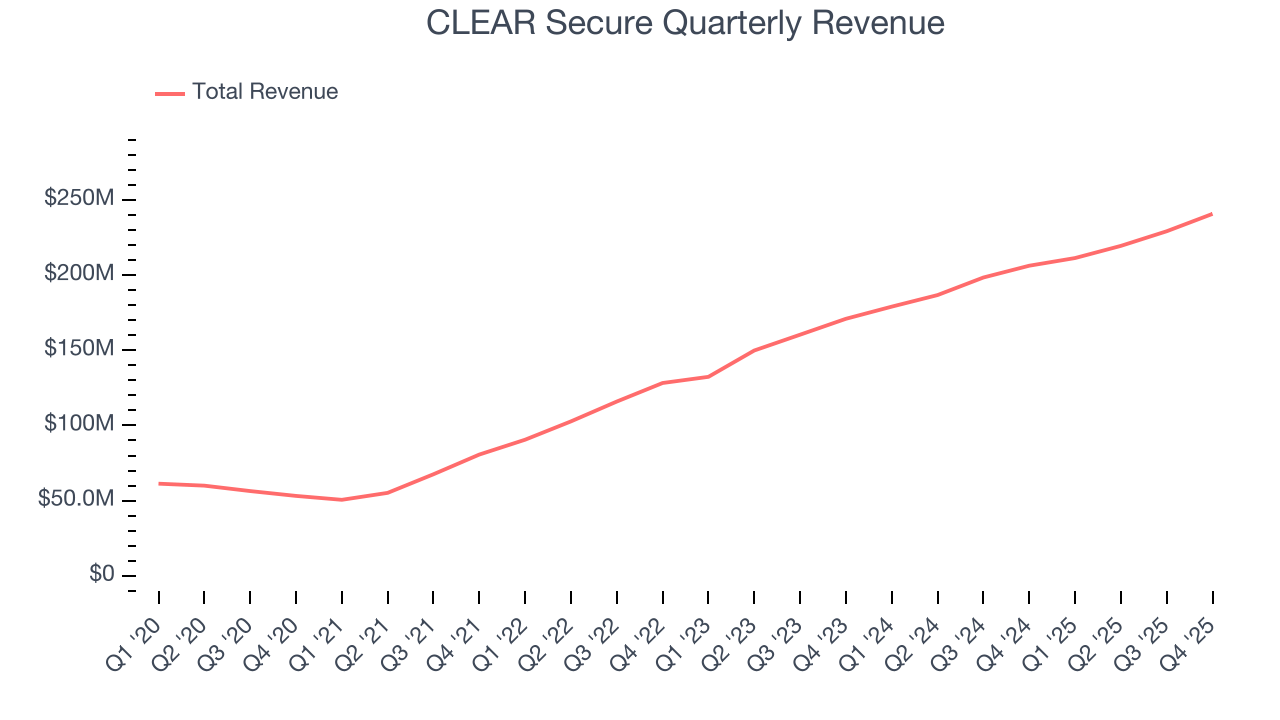

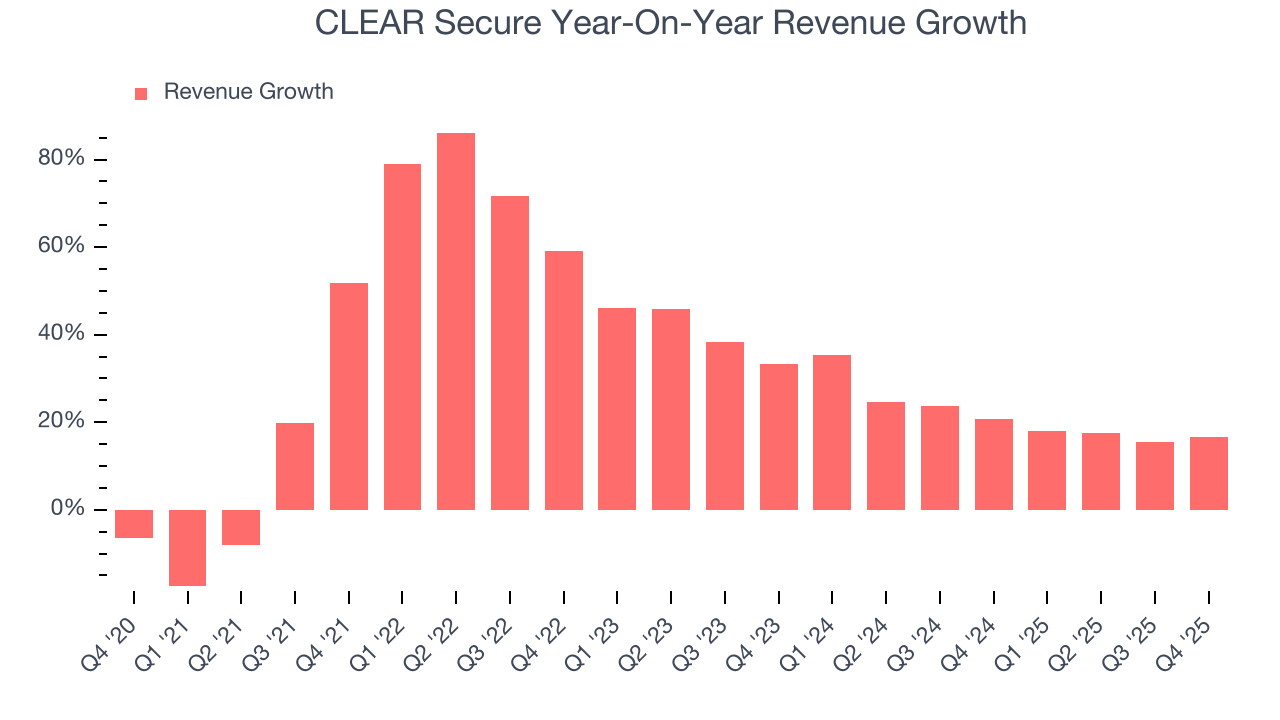

5. Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, CLEAR Secure grew its sales at an excellent 31.3% compounded annual growth rate. Its growth surpassed the average software company and shows its offerings resonate with customers, a great starting point for our analysis.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. CLEAR Secure’s annualized revenue growth of 21.2% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, CLEAR Secure reported year-on-year revenue growth of 16.7%, and its $240.8 million of revenue exceeded Wall Street’s estimates by 2.1%.

Looking ahead, sell-side analysts expect revenue to grow 11.7% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and indicates its products and services will see some demand headwinds. At least the company is tracking well in other measures of financial health.

6. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

CLEAR Secure is extremely efficient at acquiring new customers, and its CAC payback period checked in at 8.2 months this quarter. The company’s rapid recovery of its customer acquisition costs indicates it has a highly differentiated product offering and a strong brand reputation. These dynamics give CLEAR Secure more resources to pursue new product initiatives while maintaining the flexibility to increase its sales and marketing investments.

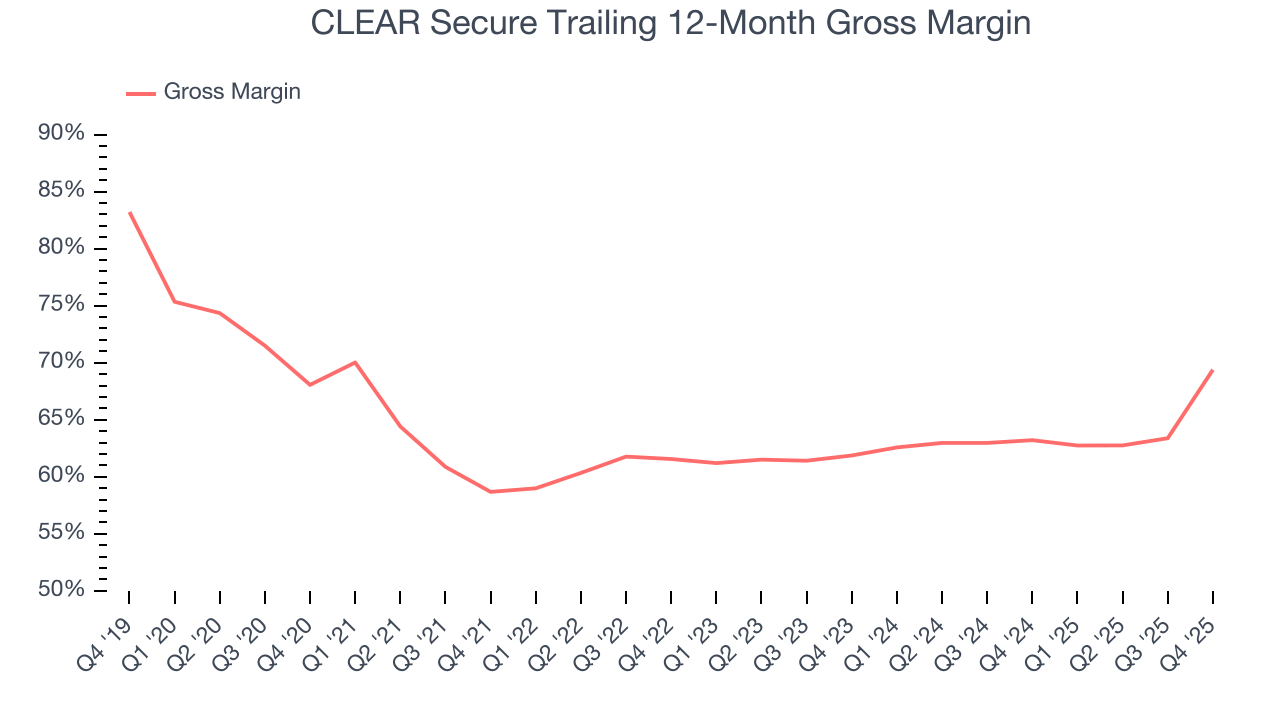

7. Gross Margin & Pricing Power

For software companies like CLEAR Secure, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

CLEAR Secure’s gross margin is worse than the software industry average, giving it less room than its competitors to hire new talent that can expand its products and services. As you can see below, it averaged a 69.4% gross margin over the last year. That means CLEAR Secure paid its providers a lot of money ($30.62 for every $100 in revenue) to run its business.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. CLEAR Secure has seen gross margins improve by 7.5 percentage points over the last 2 year, which is elite in the software space.

CLEAR Secure produced a 85.3% gross profit margin in Q4 , marking a 22.5 percentage point increase from 62.8% in the same quarter last year. CLEAR Secure’s full-year margin has also been trending up over the past 12 months, increasing by 6.2 percentage points. If this move continues, it could suggest a less competitive environment where the company has better pricing power and leverage from its growing sales on the fixed portion of its cost of goods sold (such as servers).

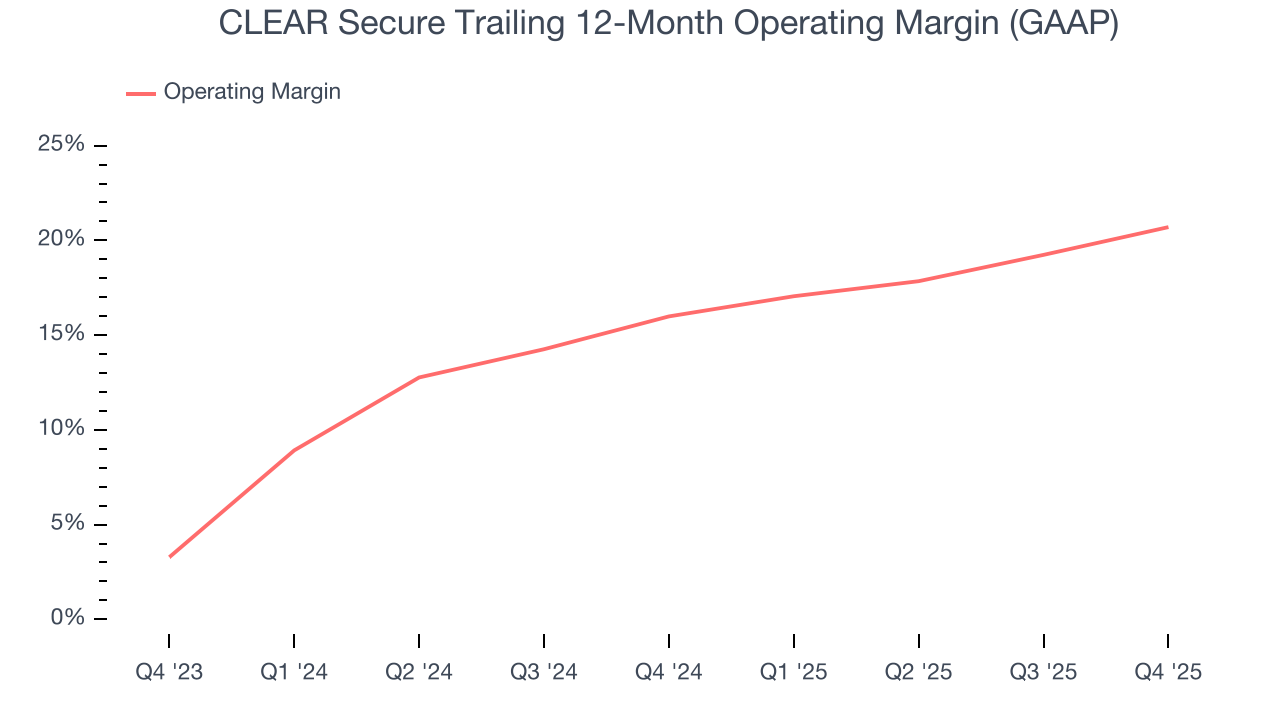

8. Operating Margin

Many software businesses adjust their profits for stock-based compensation (SBC), but we prioritize GAAP operating margin because SBC is a real expense used to attract and retain engineering and sales talent. This is one of the best measures of profitability because it shows how much money a company takes home after developing, marketing, and selling its products.

CLEAR Secure has been a well-oiled machine over the last year. It demonstrated elite profitability for a software business, boasting an average operating margin of 20.7%. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Analyzing the trend in its profitability, CLEAR Secure’s operating margin rose by 4.7 percentage points over the last two years, as its sales growth gave it operating leverage.

In Q4, CLEAR Secure generated an operating margin profit margin of 22.4%, up 5.9 percentage points year on year. The increase was driven by stronger leverage on its cost of sales (not higher efficiency with its operating expenses), as indicated by its larger rise in gross margin.

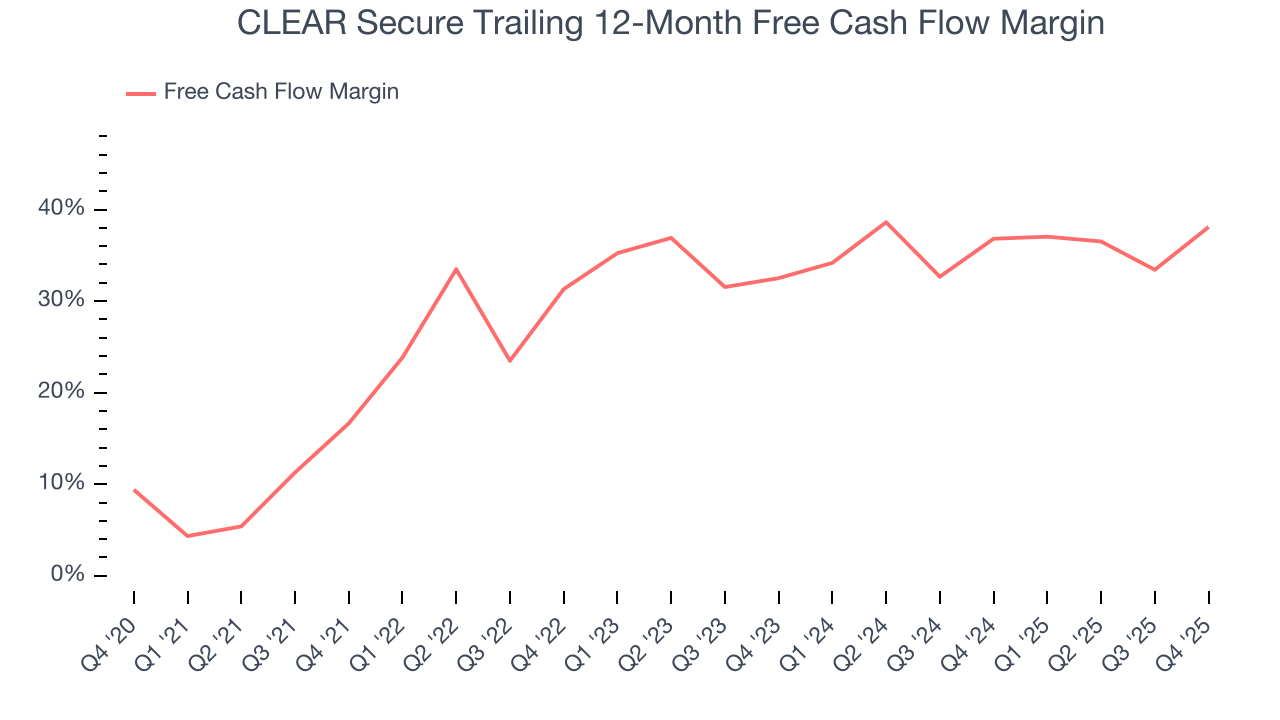

9. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

CLEAR Secure has shown terrific cash profitability, driven by its cost-effective customer acquisition strategy that enables it to stay ahead of the competition through investments in new products rather than sales and marketing. The company’s free cash flow margin was among the best in the software sector, averaging an eye-popping 38.1% over the last year.

CLEAR Secure’s free cash flow clocked in at $187.4 million in Q4, equivalent to a 77.8% margin. This result was good as its margin was 12.9 percentage points higher than in the same quarter last year. Its cash profitability was also above its one-year level, and we hope the company can build on this trend.

Over the next year, analysts predict CLEAR Secure’s cash conversion will slightly fall. Their consensus estimates imply its free cash flow margin of 38.1% for the last 12 months will decrease to 40%.

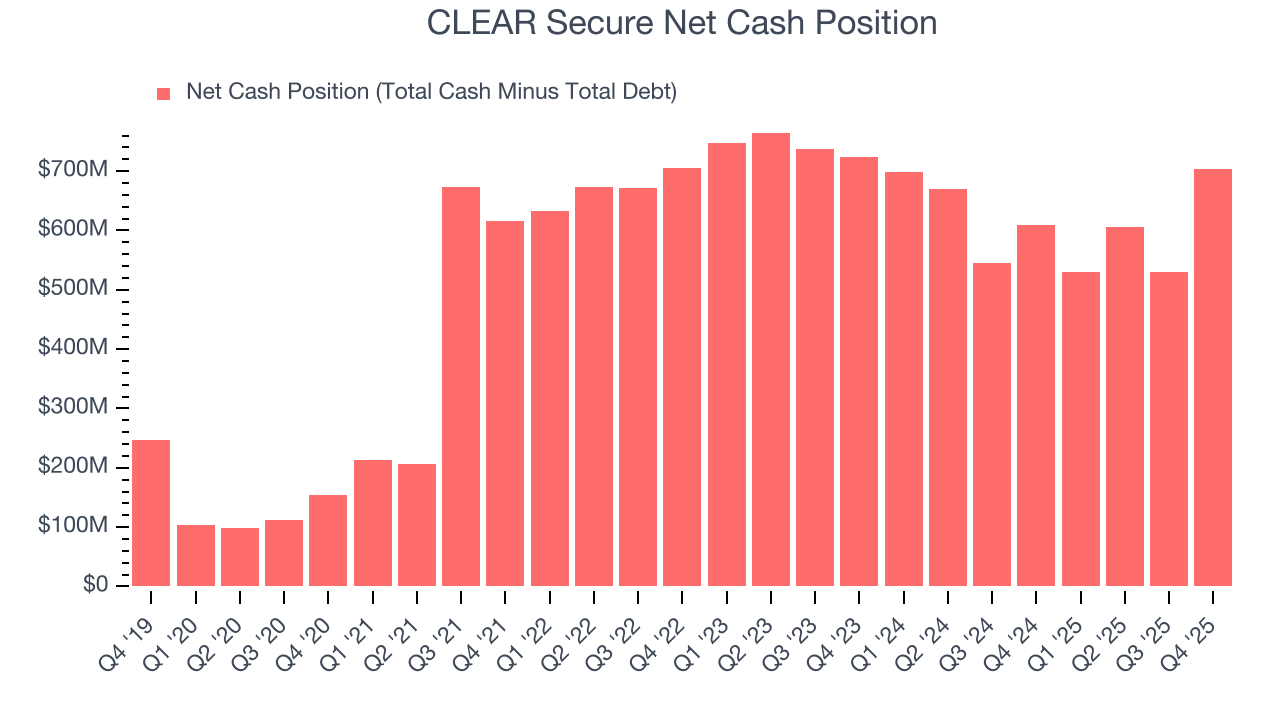

10. Balance Sheet Assessment

One of the best ways to mitigate bankruptcy risk is to hold more cash than debt.

CLEAR Secure is a profitable, well-capitalized company with $702.9 million of cash and no debt. This position is 21.5% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

11. Key Takeaways from CLEAR Secure’s Q4 Results

We were impressed by how significantly CLEAR Secure blew past analysts’ EBITDA expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. Zooming out, we think this was a solid print. The stock traded up 6.1% to $35.51 immediately after reporting.

12. Is Now The Time To Buy CLEAR Secure?

Before investing in or passing on CLEAR Secure, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

CLEAR Secure is a rock-solid business worth owning. For starters, its revenue growth was strong over the last five years. And while its expanding operating margin shows it’s becoming more efficient at building and selling its software, its bountiful generation of free cash flow empowers it to invest in growth initiatives. On top of that, CLEAR Secure’s efficient sales strategy allows it to target and onboard new users at scale.

CLEAR Secure’s price-to-sales ratio based on the next 12 months is 3.3x. Analyzing the software landscape today, CLEAR Secure’s positive attributes shine bright. We like the stock at this price.

Wall Street analysts have a consensus one-year price target of $40.25 on the company (compared to the current share price of $35.51), implying they see 13.3% upside in buying CLEAR Secure in the short term.