Yum! Brands (YUM)

Yum! Brands is intriguing. It generates heaps of cash that are reinvested into the business, creating a virtuous cycle of returns.― StockStory Analyst Team

1. News

2. Summary

Why Yum! Brands Is Interesting

Spun off as an independent company from PepsiCo, Yum! Brands (NYSE:YUM) is a multinational corporation that owns KFC, Pizza Hut, Taco Bell, and The Habit Burger Grill.

- Excellent operating margin highlights the strength of its business model

- Impressive free cash flow profitability enables the company to fund new investments or reward investors with share buybacks/dividends

- One risk is its poor same-store sales performance over the past two years indicates it’s having trouble bringing new diners into its restaurants

Yum! Brands almost passes our quality test. If you like the stock, the price seems reasonable.

Why Is Now The Time To Buy Yum! Brands?

Yum! Brands is trading at $159.15 per share, or 24.2x forward P/E. Many restaurant companies feature higher valuation multiples than Yum! Brands. Regardless, we think Yum! Brands’s current price is appropriate given the quality you get.

This could be a good time to invest if you think there are underappreciated aspects of the business.

3. Yum! Brands (YUM) Research Report: Q4 CY2025 Update

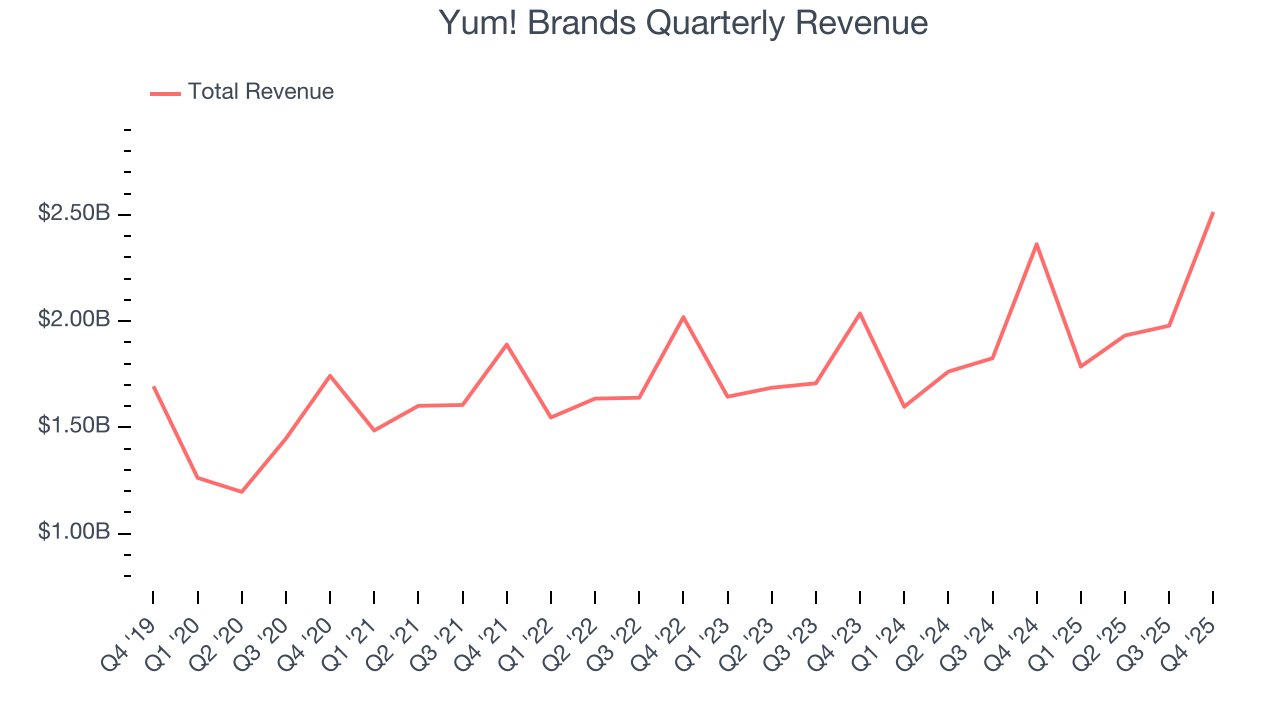

Fast-food company Yum! Brands (NYSE:YUM) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 6.4% year on year to $2.51 billion. Its non-GAAP profit of $1.73 per share was 1.5% below analysts’ consensus estimates.

Yum! Brands (YUM) Q4 CY2025 Highlights:

- Revenue: $2.51 billion vs analyst estimates of $2.45 billion (6.4% year-on-year growth, 2.5% beat)

- Adjusted EPS: $1.73 vs analyst expectations of $1.76 (1.5% miss)

- Operating Margin: 29.4%, up from 27.8% in the same quarter last year

- Free Cash Flow Margin: 33.9%, up from 17.2% in the same quarter last year

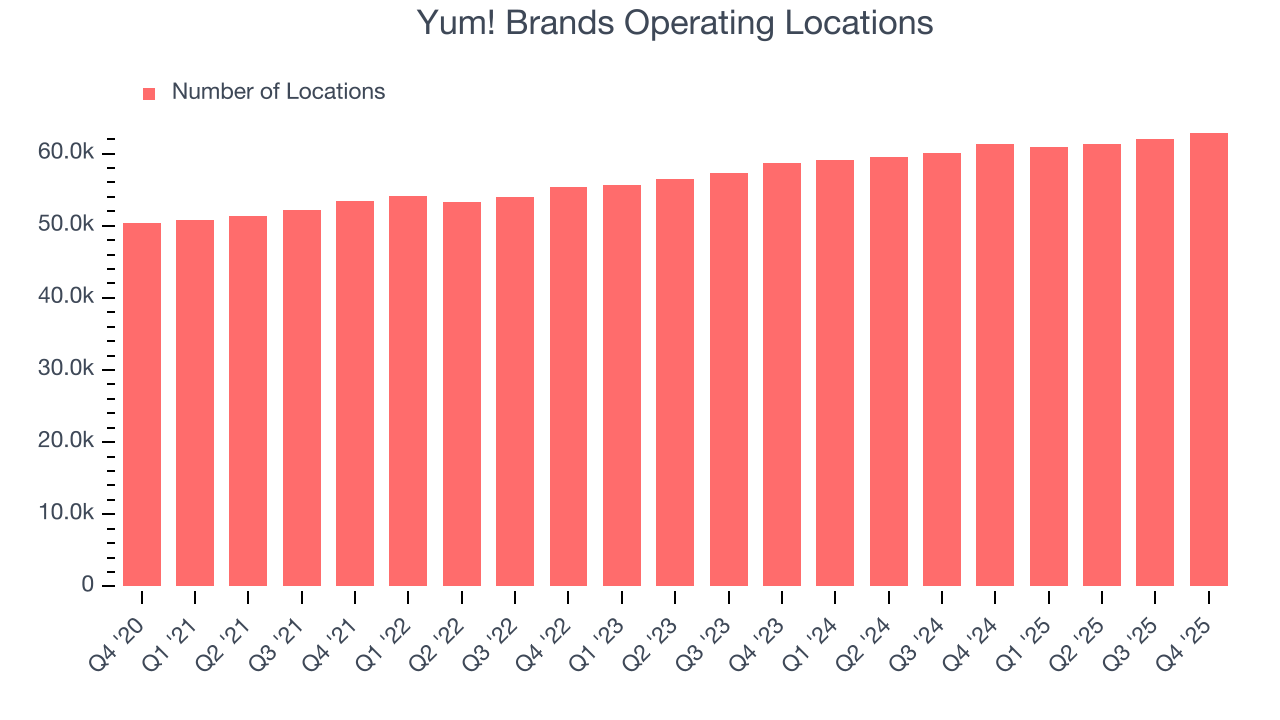

- Locations: 62,901 at quarter end, up from 61,346 in the same quarter last year

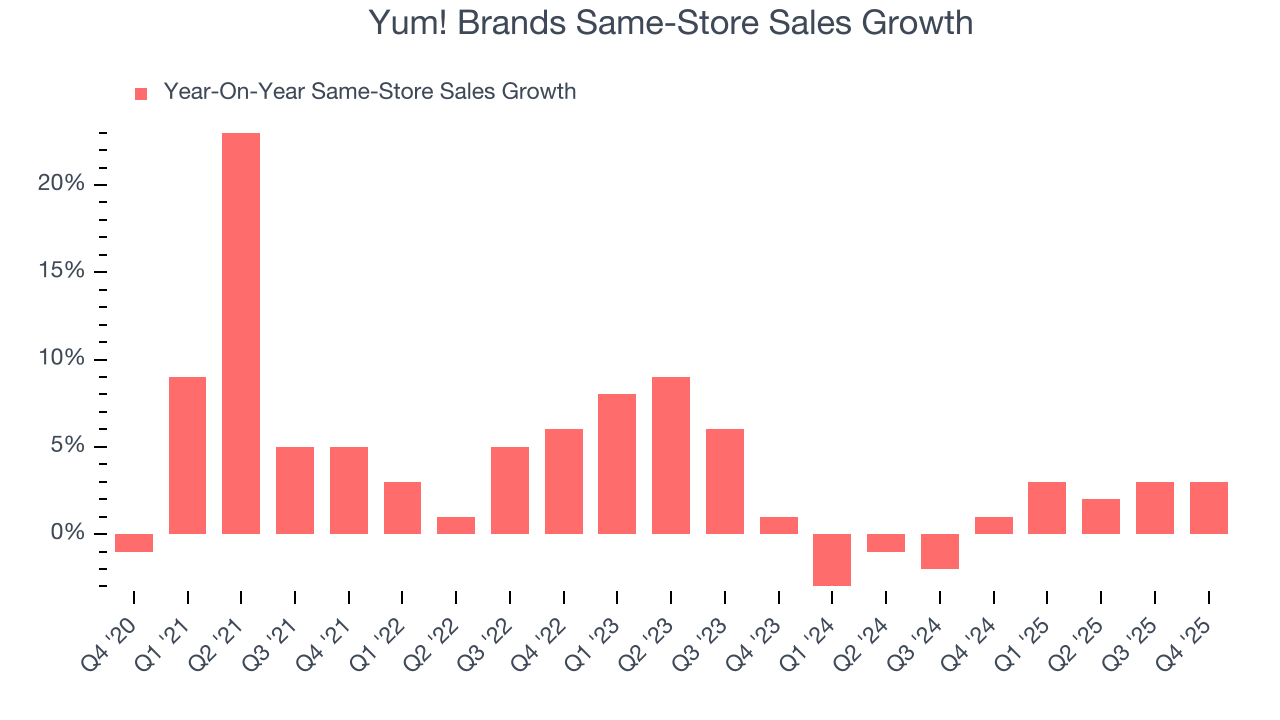

- Same-Store Sales rose 3% year on year (1% in the same quarter last year)

- Market Capitalization: $44.07 billion

Company Overview

Spun off as an independent company from PepsiCo, Yum! Brands (NYSE:YUM) is a multinational corporation that owns KFC, Pizza Hut, Taco Bell, and The Habit Burger Grill.

Specifically, the company’s 1997 strategic separation from PepsiCo was meant to increase focus on the fast-food opportunity.

Each banner within Yum! Brands brings its own unique history and culinary offerings. KFC, famous for its “finger-lickin' good” fried chicken, traces its roots back to Colonel Harland Sanders and his secret blend of herbs and spices. Pizza Hut revolutionized the pizza industry with its dine-in experience and unique creations like the “Original Stuffed Crust” pizza. Taco Bell introduced Mexican-inspired flavors to a wider audience, offering innovative and affordable menu choices. And most recently, The Habit Burger Grill caters to the fast-casual market through its never-frozen, always-fresh burgers.

Yum! Brands has successfully grown its presence internationally by adapting menus and experiences to local tastes and preferences. One example is Pizza Hut’s “Mizza” in Taiwan, which is a pizza using rice instead of traditional dough. Another contributing factor is its focus on customer convenience, evident in the creation of mobile apps that enable online ordering, customization, and rewards programs. Additionally, the company has forged partnerships with popular delivery platforms, ensuring that customers can savor their favorite meals in the comfort of their own homes.

4. Traditional Fast Food

Traditional fast-food restaurants are renowned for their speed and convenience, boasting menus filled with familiar and budget-friendly items. Their reputations for on-the-go consumption make them favored destinations for individuals and families needing a quick meal. This class of restaurants, however, is fighting the perception that their meals are unhealthy and made with inferior ingredients, a battle that's especially relevant today given the consumers increasing focus on health and wellness.

Yum! Brands’ competitors include include Burger King and Popeyes (owned by Restaurant Brands, NYSE:QSR), Domino’s (NYSE:DPZ), McDonald’s (NYSE:MCD), and Wendy’s (NASDAQ:WEN).

5. Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $8.21 billion in revenue over the past 12 months, Yum! Brands is one of the most widely recognized restaurant chains and benefits from customer loyalty, a luxury many don’t have. Its scale also gives it negotiating leverage with suppliers, enabling it to source its ingredients at a lower cost. However, its scale is a double-edged sword because there is only so much real estate to build restaurants, placing a ceiling on its growth. To expand meaningfully, Yum! Brands likely needs to tweak its prices, start new chains, or enter new markets.

As you can see below, Yum! Brands’s sales grew at a mediocre 6.6% compounded annual growth rate over the last six years.

This quarter, Yum! Brands reported year-on-year revenue growth of 6.4%, and its $2.51 billion of revenue exceeded Wall Street’s estimates by 2.5%.

Looking ahead, sell-side analysts expect revenue to grow 8.7% over the next 12 months, an acceleration versus the last six years. This projection is above average for the sector and indicates its newer menu offerings will catalyze better top-line performance.

6. Restaurant Performance

Number of Restaurants

A restaurant chain’s total number of dining locations influences how much it can sell and how quickly revenue can grow.

Yum! Brands sported 62,901 locations in the latest quarter. Over the last two years, it has opened new restaurants at a rapid clip by averaging 4.1% annual growth, among the fastest in the restaurant sector. Additionally, one dynamic making expansion more seamless is the company’s franchise model, where franchisees are primarily responsible for opening new restaurants while Yum! Brands provides support.

When a chain opens new restaurants, it usually means it’s investing for growth because there’s healthy demand for its meals and there are markets where its concepts have few or no locations.

Same-Store Sales

The change in a company's restaurant base only tells one side of the story. The other is the performance of its existing locations, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales provides a deeper understanding of this issue because it measures organic growth at restaurants open for at least a year.

Yum! Brands’s demand within its existing dining locations has barely increased over the last two years as its same-store sales were flat. Yum! Brands should consider improving its foot traffic and efficiency before expanding its restaurant base.

In the latest quarter, Yum! Brands’s same-store sales rose 3% year on year. This growth was an acceleration from its historical levels, which is always an encouraging sign.

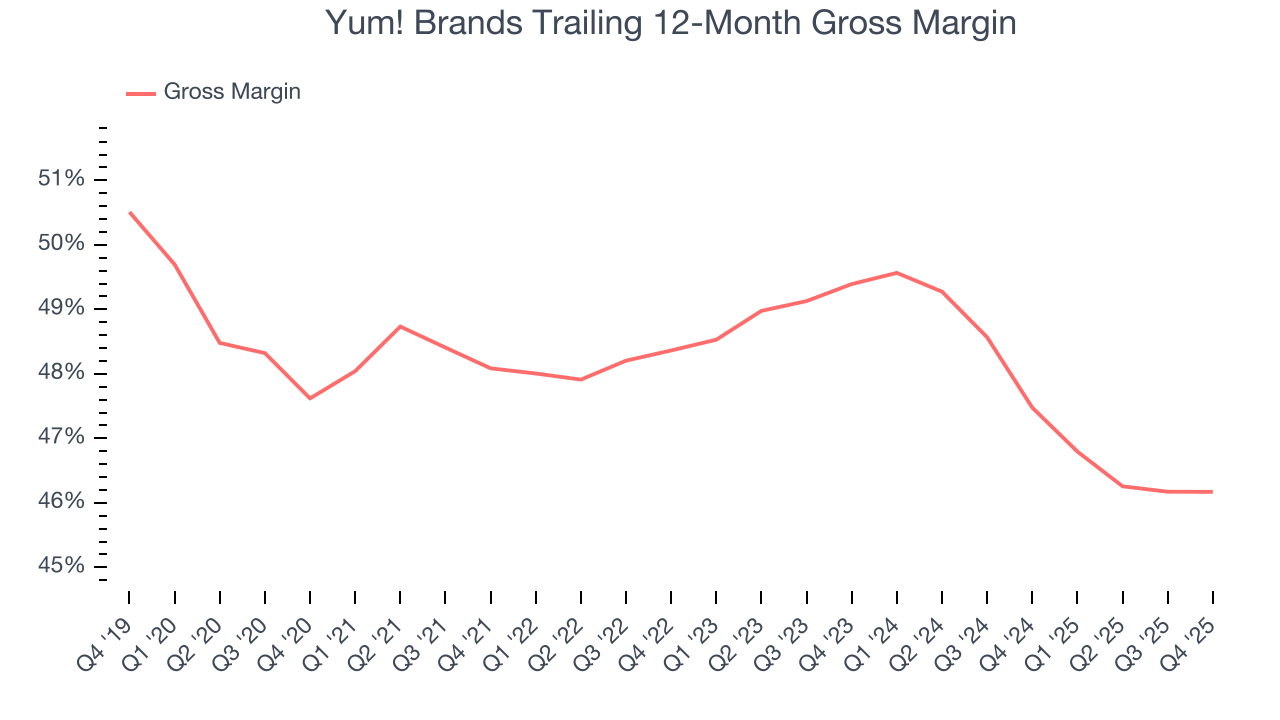

7. Gross Margin & Pricing Power

We prefer higher gross margins because they not only make it easier to generate more operating profits but also indicate pricing power and differentiation, whether it be the dining experience or quality and taste of food.

Yum! Brands has best-in-class unit economics for a restaurant company, enabling it to invest in areas such as marketing and talent to grow its brand. As you can see below, it averaged an elite 46.8% gross margin over the last two years. Said differently, roughly $46.80 was left to spend on selling, marketing, and general administrative overhead for every $100 in revenue.

This quarter, Yum! Brands’s gross profit margin was 44.5%, in line with the same quarter last year. Zooming out, Yum! Brands’s full-year margin has been trending down over the past 12 months, decreasing by 1.3 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to lower prices and higher input costs (such as ingredients and transportation expenses).

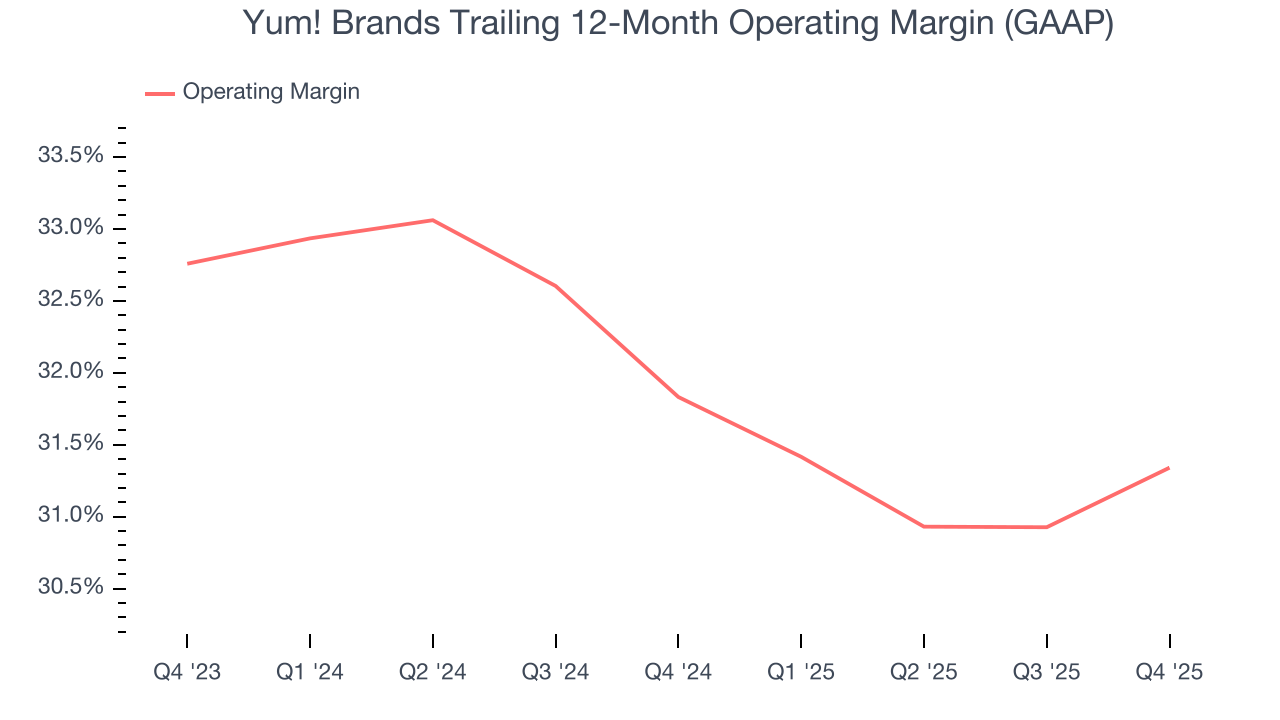

8. Operating Margin

Yum! Brands’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 31.6% over the last two years. This profitability was elite for a restaurant business thanks to its efficient cost structure and economies of scale. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Yum! Brands’s operating margin might fluctuated slightly but has generally stayed the same over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Yum! Brands generated an operating margin profit margin of 29.4%, up 1.5 percentage points year on year. The increase was encouraging, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, and administrative overhead.

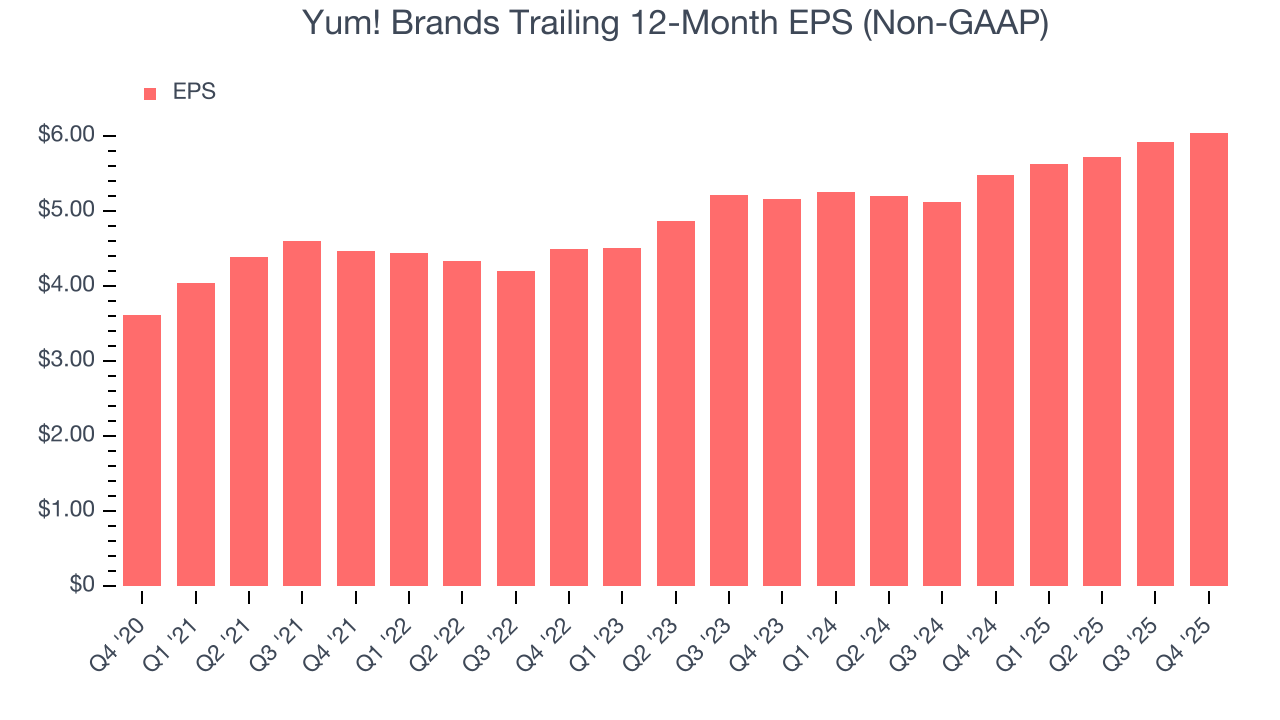

9. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Yum! Brands’s EPS grew at an unimpressive 9.3% compounded annual growth rate over the last six years. This performance was better than its flat revenue but doesn’t tell us much about its business quality because its operating margin didn’t improve.

In Q4, Yum! Brands reported adjusted EPS of $1.73, up from $1.61 in the same quarter last year. Despite growing year on year, this print slightly missed analysts’ estimates. Over the next 12 months, Wall Street expects Yum! Brands’s full-year EPS of $6.05 to grow 10.4%.

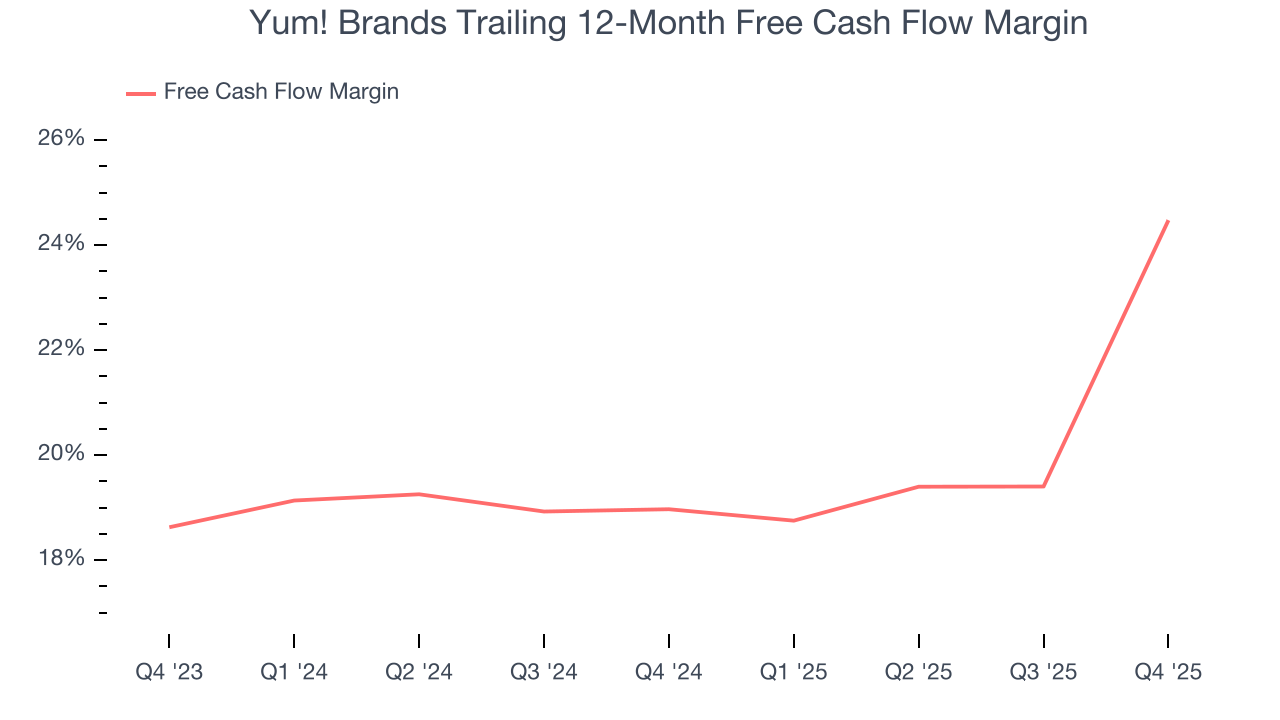

10. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Yum! Brands has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition. The company’s free cash flow margin was among the best in the restaurant sector, averaging 21.8% over the last two years.

Taking a step back, we can see that Yum! Brands’s margin expanded by 5.5 percentage points over the last year. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability was flat.

Yum! Brands’s free cash flow clocked in at $853 million in Q4, equivalent to a 33.9% margin. This result was good as its margin was 16.7 percentage points higher than in the same quarter last year, building on its favorable historical trend.

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Yum! Brands’s five-year average ROIC was 71.8%, placing it among the best restaurant companies. This illustrates its management team’s ability to invest in highly profitable ventures and produce tangible results for shareholders.

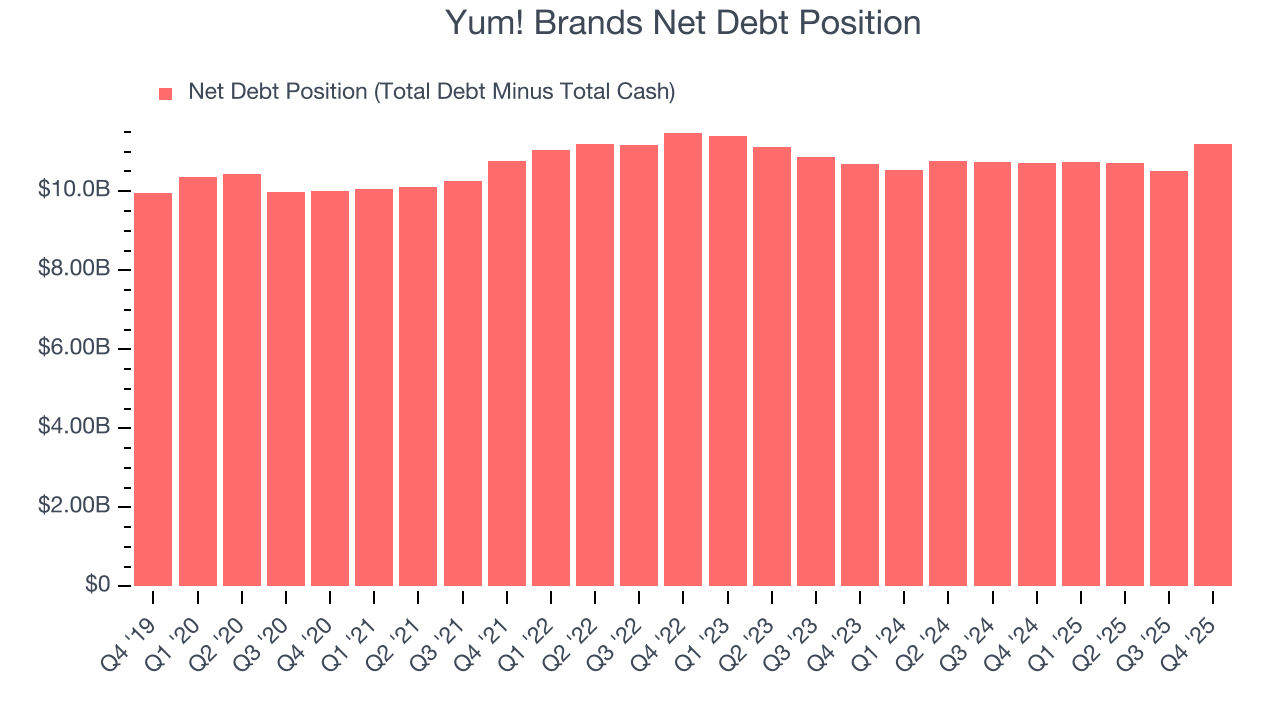

12. Balance Sheet Assessment

Yum! Brands reported $709 million of cash and $11.91 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $2.87 billion of EBITDA over the last 12 months, we view Yum! Brands’s 3.9× net-debt-to-EBITDA ratio as safe. We also see its $233 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

13. Key Takeaways from Yum! Brands’s Q4 Results

We enjoyed seeing Yum! Brands beat analysts’ revenue expectations this quarter. We were also glad its same-store sales outperformed Wall Street’s estimates. On the other hand, its EPS slightly missed. Overall, we think this was still a solid quarter with some key areas of upside. The stock traded up 1.1% to $160.50 immediately following the results.

14. Is Now The Time To Buy Yum! Brands?

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own Yum! Brands, you should also grasp the company’s longer-term business quality and valuation.

There are definitely a lot of things to like about Yum! Brands. Although its revenue growth was mediocre over the last six years, its growth over the next 12 months is expected to be higher. And while Yum! Brands’s projected EPS for the next year is lacking, its new restaurant openings have increased its brand equity. On top of that, its impressive operating margins show it has a highly efficient business model.

Yum! Brands’s P/E ratio based on the next 12 months is 23.8x. Looking at the restaurant landscape right now, Yum! Brands trades at a pretty interesting price. For those confident in the business and its management team, this is a good time to invest.

Wall Street analysts have a consensus one-year price target of $167.54 on the company (compared to the current share price of $160.50), implying they see 4.4% upside in buying Yum! Brands in the short term.