Yum China (YUMC)

We’re not sold on Yum China. Its poor sales growth and falling returns on capital suggest its growth opportunities are shrinking.― StockStory Analyst Team

1. News

2. Summary

Why Yum China Is Not Exciting

One of China’s largest restaurant companies, Yum China (NYSE:YUMC) is an independent entity spun off from Yum! Brands in 2016.

- Weak same-store sales trends over the past two years suggest there may be few opportunities in its core markets to open new restaurants

- Gross margin of 20.1% reflects the bad unit economics inherent in most restaurant businesses

- A consolation is that its market-beating returns on capital illustrate that management has a knack for investing in profitable ventures

Yum China lacks the business quality we seek. There are superior stocks for sale in the market.

Why There Are Better Opportunities Than Yum China

Yum China’s stock price of $48.60 implies a valuation ratio of 17.5x forward P/E. This multiple is lower than most restaurant companies, but for good reason.

Cheap stocks can look like great bargains at first glance, but you often get what you pay for. These mediocre businesses often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. Yum China (YUMC) Research Report: Q3 CY2025 Update

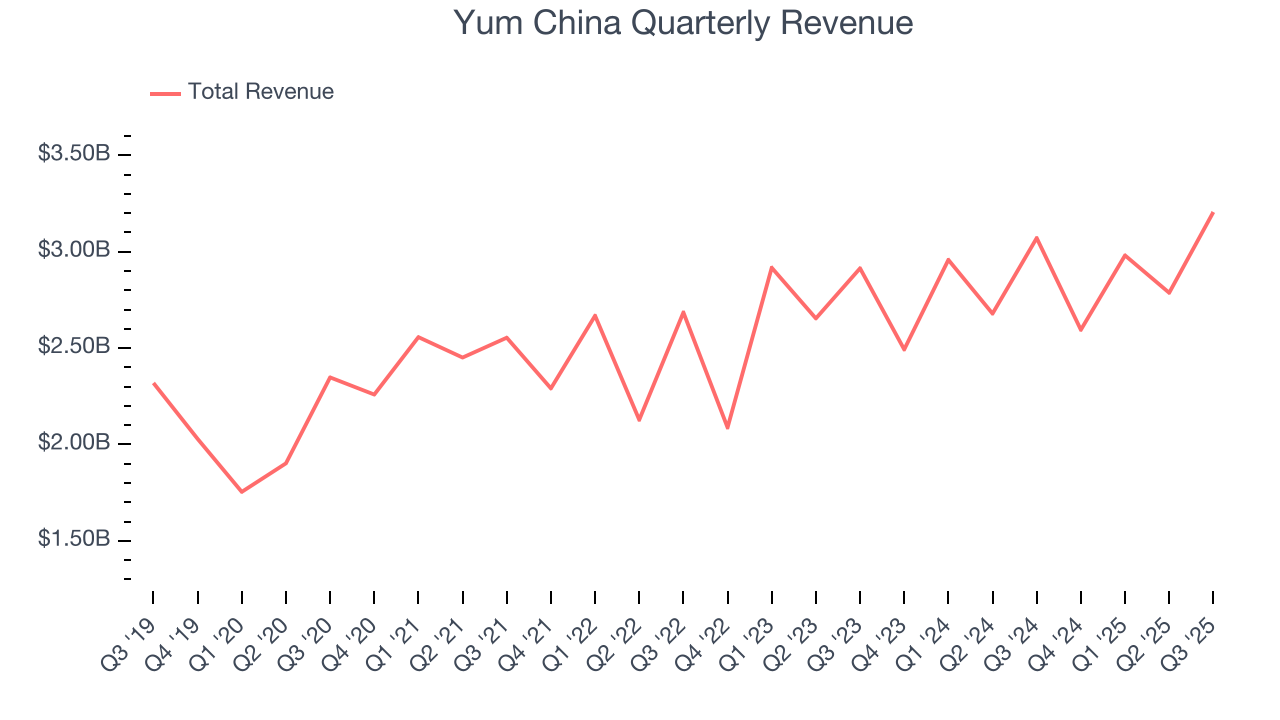

Fast-food company Yum China (NYSE:YUMC) met Wall Streets revenue expectations in Q3 CY2025, with sales up 4.4% year on year to $3.21 billion. Its non-GAAP profit of $0.76 per share was in line with analysts’ consensus estimates.

Yum China (YUMC) Q3 CY2025 Highlights:

- Revenue: $3.21 billion vs analyst estimates of $3.20 billion (4.4% year-on-year growth, in line)

- Adjusted EPS: $0.76 vs analyst estimates of $0.76 (in line)

- Operating Margin: 12.5%, in line with the same quarter last year

- Free Cash Flow Margin: 10.9%, up from 7.9% in the same quarter last year

- Locations: 17,514 at quarter end, up from 15,861 in the same quarter last year

- Same-Store Sales rose 1% year on year (-3% in the same quarter last year)

- Market Capitalization: $15.86 billion

Company Overview

One of China’s largest restaurant companies, Yum China (NYSE:YUMC) is an independent entity spun off from Yum! Brands in 2016.

It was strategically separated from its parent company to focus on the Chinese restaurant market, which has vast potential and different dynamics than the United States. Today, the company mainly operates KFC (fried chicken), Pizza Hut (pizza), and Taco Bell (Mexican) fast-food chains in China.

Yum China has carved itself a niche in the country as the predominant destination for traditional American flavors with an Asian twist. Its success can be attributed to localization, and through its deep understanding of Chinese consumers, has revamped its menu items to include innovative dishes such as KFC’s fried chicken meal, which comes with rice, soup, and mushroom salad, Pizza Hut’s jumbo bacon-wrapped shrimp basil pesto pizza and escargot, and Taco Bell’s beef bulgogi and kimchi burrito.

Additionally, unlike its United States counterparts, Yum China’s fast-food locations are perceived as premium dining options due to their cleanliness, price point, and inclusion of technology like self-service digital kiosks. Generally, its stores’ layouts are similar to those in the United States with a counter where customers can place orders and seating areas with a mix of booths and tables. Some of its locations, however, also offer table service, which is unheard of in typical fast-food joints.

4. Traditional Fast Food

Traditional fast-food restaurants are renowned for their speed and convenience, boasting menus filled with familiar and budget-friendly items. Their reputations for on-the-go consumption make them favored destinations for individuals and families needing a quick meal. This class of restaurants, however, is fighting the perception that their meals are unhealthy and made with inferior ingredients, a battle that's especially relevant today given the consumers increasing focus on health and wellness.

American competitors include Burger King (owned by Restaurant Brands, NYSE:QSR), McDonald’s (NYSE:MCD), and Starbucks (NASDAQ:SBUX) while Chinese competitors comprise of Dicos, Home Original Chicken, and Real Kungfu.

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $11.57 billion in revenue over the past 12 months, Yum China is one of the most widely recognized restaurant chains and benefits from customer loyalty, a luxury many don’t have. Its scale also gives it negotiating leverage with suppliers, enabling it to source its ingredients at a lower cost. However, its scale is a double-edged sword because it’s harder to find incremental growth when your existing restaurant banners have penetrated most of the market. For Yum China to boost its sales, it likely needs to adjust its prices, launch new chains, or lean into foreign markets.

As you can see below, Yum China grew its sales at a sluggish 4.9% compounded annual growth rate over the last six years (we compare to 2019 to normalize for COVID-19 impacts).

This quarter, Yum China grew its revenue by 4.4% year on year, and its $3.21 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 5.4% over the next 12 months, similar to its six-year rate. This projection is underwhelming and suggests its newer menu offerings will not accelerate its top-line performance yet.

6. Restaurant Performance

Number of Restaurants

A restaurant chain’s total number of dining locations influences how much it can sell and how quickly revenue can grow.

Yum China operated 17,514 locations in the latest quarter. It has opened new restaurants at a rapid clip over the last two years, averaging 12% annual growth, much faster than the broader restaurant sector.

When a chain opens new restaurants, it usually means it’s investing for growth because there’s healthy demand for its meals and there are markets where its concepts have few or no locations.

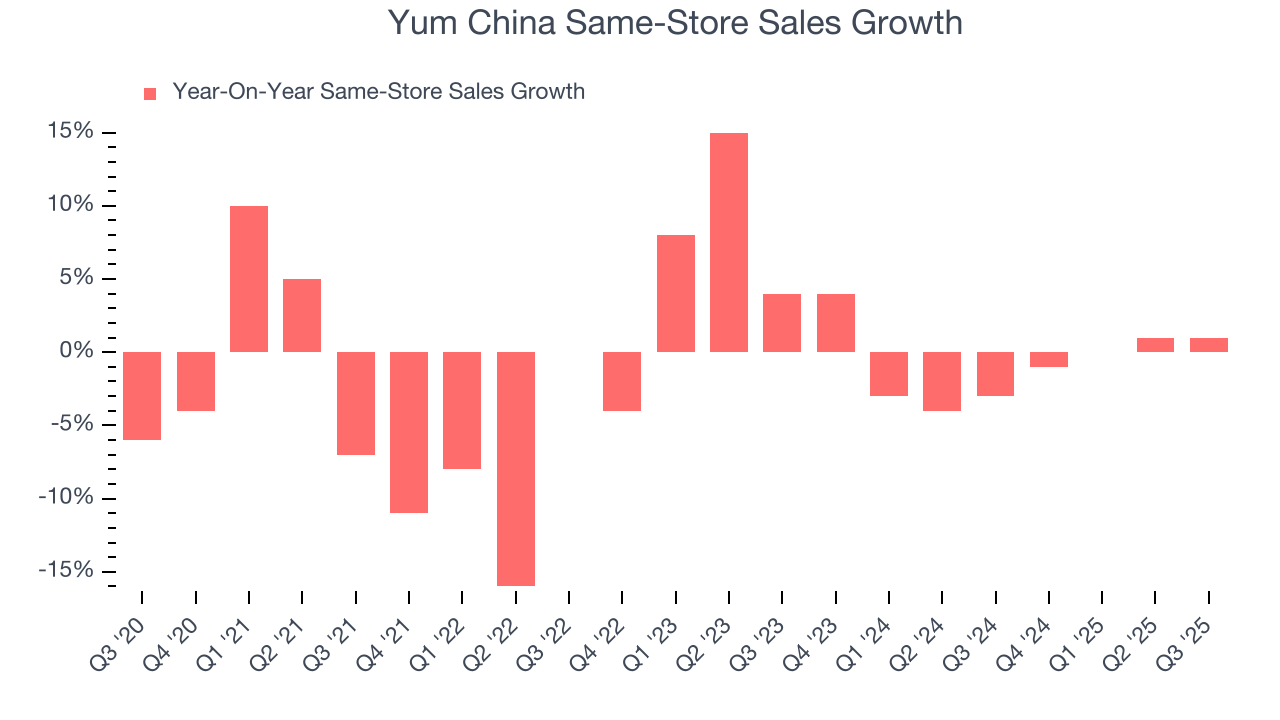

Same-Store Sales

The change in a company's restaurant base only tells one side of the story. The other is the performance of its existing locations, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales gives us insight into this topic because it measures organic growth at restaurants open for at least a year.

Yum China’s demand within its existing dining locations has barely increased over the last two years as its same-store sales were flat. Yum China should consider improving its foot traffic and efficiency before expanding its restaurant base.

In the latest quarter, Yum China’s same-store sales rose 1% year on year. This growth was a well-appreciated turnaround from its historical levels, showing the business is regaining momentum.

7. Gross Margin & Pricing Power

Yum China has bad unit economics for a restaurant company, giving it less room to reinvest and grow its presence. As you can see below, it averaged a 20.7% gross margin over the last two years. Said differently, Yum China had to pay a chunky $79.29 to its suppliers for every $100 in revenue.

Yum China produced a 22.3% gross profit margin in Q3, marking a 4.4 percentage point increase from 17.9% in the same quarter last year. Yum China’s full-year margin has also been trending up over the past 12 months, increasing by 1.7 percentage points. If this move continues, it could suggest better unit economics due to more leverage from its growing sales on the fixed portion of its cost of goods sold

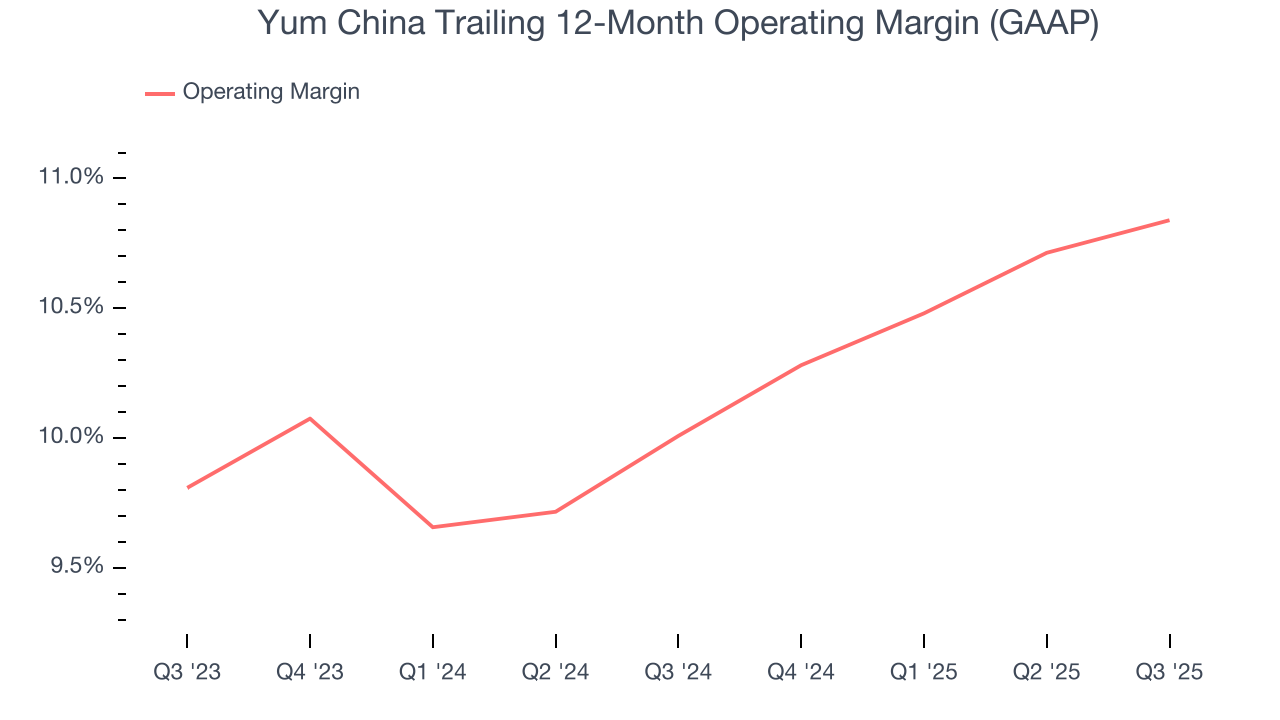

8. Operating Margin

Operating margin is a key profitability metric because it accounts for all expenses keeping the business in motion, including food costs, wages, rent, advertising, and other administrative costs.

Yum China’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 10.4% over the last two years. This profitability was higher than the broader restaurant sector, showing it did a decent job managing its expenses.

Looking at the trend in its profitability, Yum China’s operating margin might fluctuated slightly but has generally stayed the same over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Yum China generated an operating margin profit margin of 12.5%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

9. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Yum China’s unimpressive 5.5% annual EPS growth over the last six years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

In Q3, Yum China reported adjusted EPS of $0.76, down from $0.77 in the same quarter last year. This print was close to analysts’ estimates. Over the next 12 months, Wall Street expects Yum China’s full-year EPS of $2.41 to grow 18.6%.

10. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Yum China has shown impressive cash profitability, giving it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 7% over the last two years, better than the broader restaurant sector.

Taking a step back, we can see that Yum China’s margin expanded by 2.3 percentage points over the last year. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability was flat.

Yum China’s free cash flow clocked in at $351 million in Q3, equivalent to a 10.9% margin. This result was good as its margin was 3 percentage points higher than in the same quarter last year, building on its favorable historical trend.

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Although Yum China hasn’t been the highest-quality company lately because of its poor top-line performance, it found a few growth initiatives in the past that worked out wonderfully. Its five-year average ROIC was 27.3%, splendid for a restaurant business.

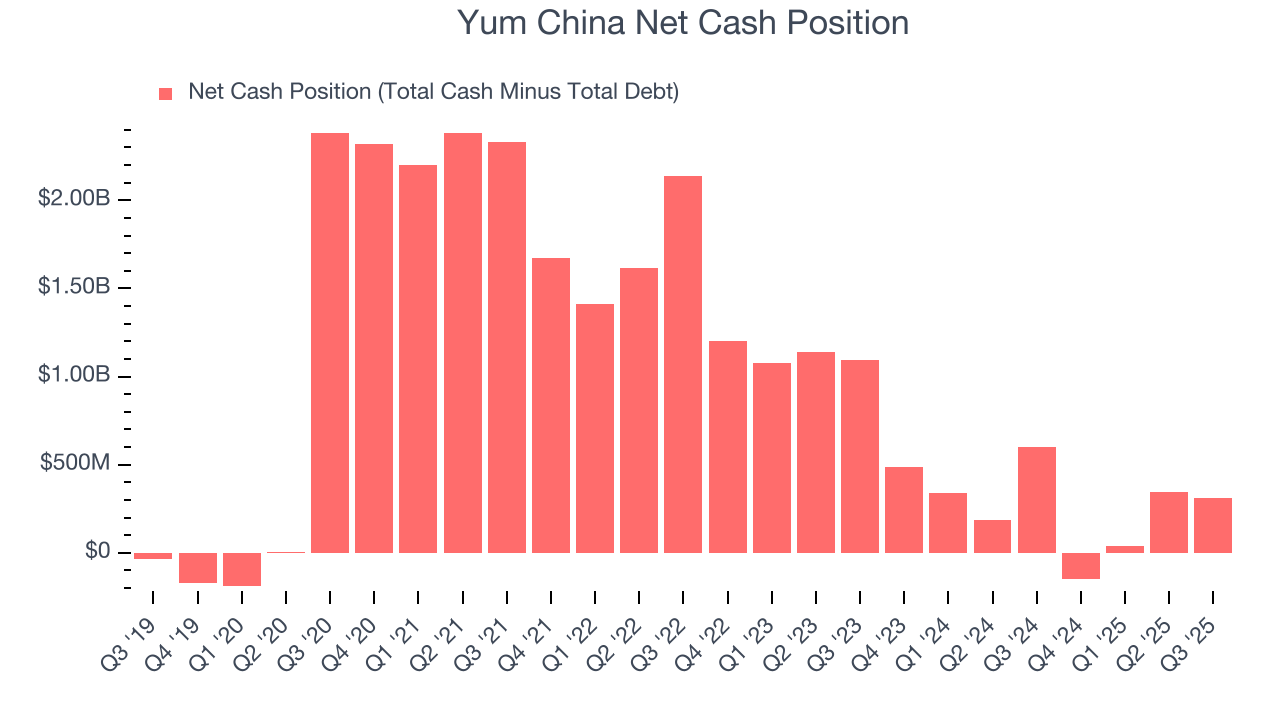

12. Balance Sheet Assessment

One of the best ways to mitigate bankruptcy risk is to hold more cash than debt.

Yum China is a profitable, well-capitalized company with $2.15 billion of cash and $1.84 billion of debt on its balance sheet. This $309 million net cash position gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

13. Key Takeaways from Yum China’s Q3 Results

Both revenue and EPS were in line with analysts’ expectations this quarter. This was a quarter without many surprises, good or bad. The market seemed to be hoping for more, and the stock traded down 1.1% to $43.50 immediately after reporting.

14. Is Now The Time To Buy Yum China?

Updated: January 24, 2026 at 9:51 PM EST

Before deciding whether to buy Yum China or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

Yum China isn’t a bad business, but we’re not clamoring to buy it here and now. Although its revenue growth was a little slower over the last six years, its growth over the next 12 months is expected to be higher. And while Yum China’s poor same-store sales performance has been a headwind, its new restaurant openings have increased its brand equity.

Yum China’s P/E ratio based on the next 12 months is 17.5x. This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're pretty confident there are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $58.13 on the company (compared to the current share price of $48.60).