Zurn Elkay (ZWS)

We’re cautious of Zurn Elkay. Its low returns on capital and plummeting sales suggest it struggles to generate demand and profits, a red flag.― StockStory Analyst Team

1. News

2. Summary

Why We Think Zurn Elkay Will Underperform

Claiming to have saved more than 30 billion gallons of water, Zurn Elkay (NYSE:ZWS) provides water management solutions to various industries.

- Falling earnings per share over the last five years has some investors worried as stock prices ultimately follow EPS over the long term

- Flat sales over the last five years suggest it must find different ways to grow during this cycle

- A positive is that its powerful free cash flow generation enables it to reinvest its profits or return capital to investors consistently

Zurn Elkay’s quality isn’t up to par. There are superior stocks for sale in the market.

Why There Are Better Opportunities Than Zurn Elkay

At $48.03 per share, Zurn Elkay trades at 28.4x forward P/E. Not only does Zurn Elkay trade at a premium to companies in the industrials space, but this multiple is also high for its top-line growth.

We prefer to invest in similarly-priced but higher-quality companies with superior earnings growth.

3. Zurn Elkay (ZWS) Research Report: Q4 CY2025 Update

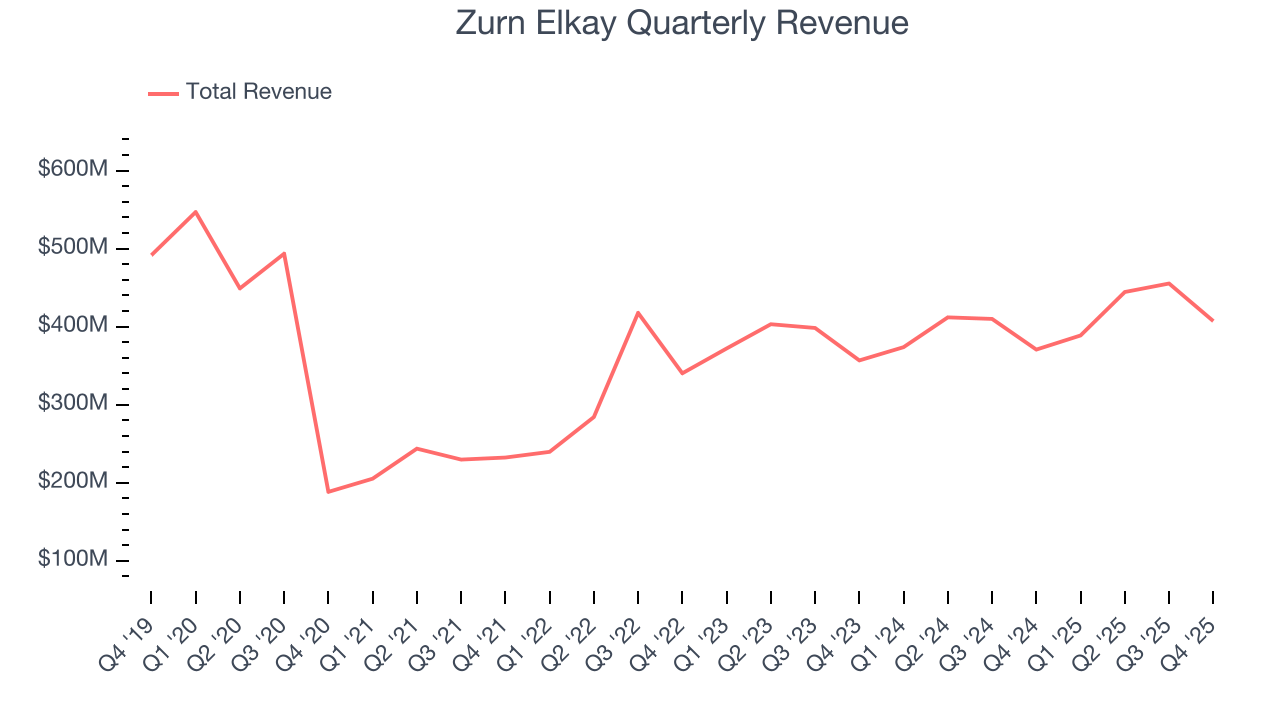

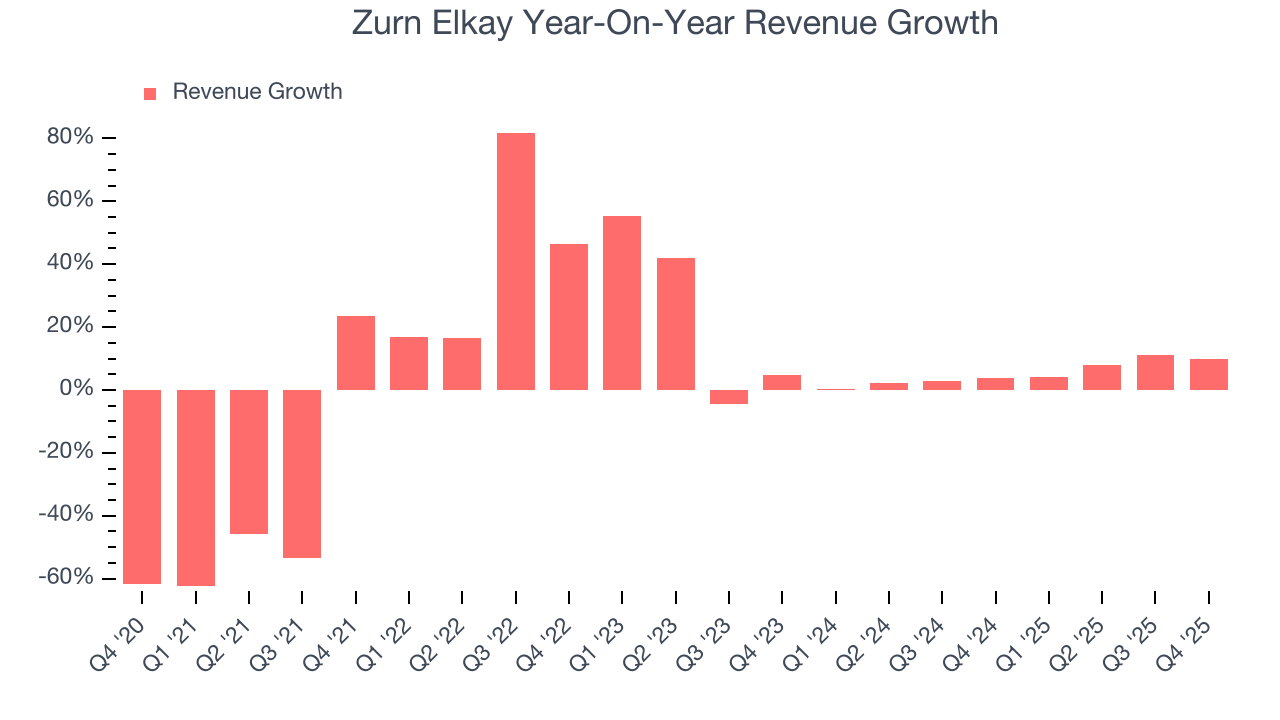

Water management solutions company Zurn Elkay (NYSE:ZWS) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 9.8% year on year to $407.2 million. Its non-GAAP profit of $0.36 per share was 5.9% above analysts’ consensus estimates.

Zurn Elkay (ZWS) Q4 CY2025 Highlights:

- Revenue: $407.2 million vs analyst estimates of $401.5 million (9.8% year-on-year growth, 1.4% beat)

- Adjusted EPS: $0.36 vs analyst estimates of $0.34 (5.9% beat)

- Adjusted EBITDA: $104.1 million vs analyst estimates of $101.1 million (25.6% margin, 2.9% beat)

- Operating Margin: 14.8%, up from 13.3% in the same quarter last year

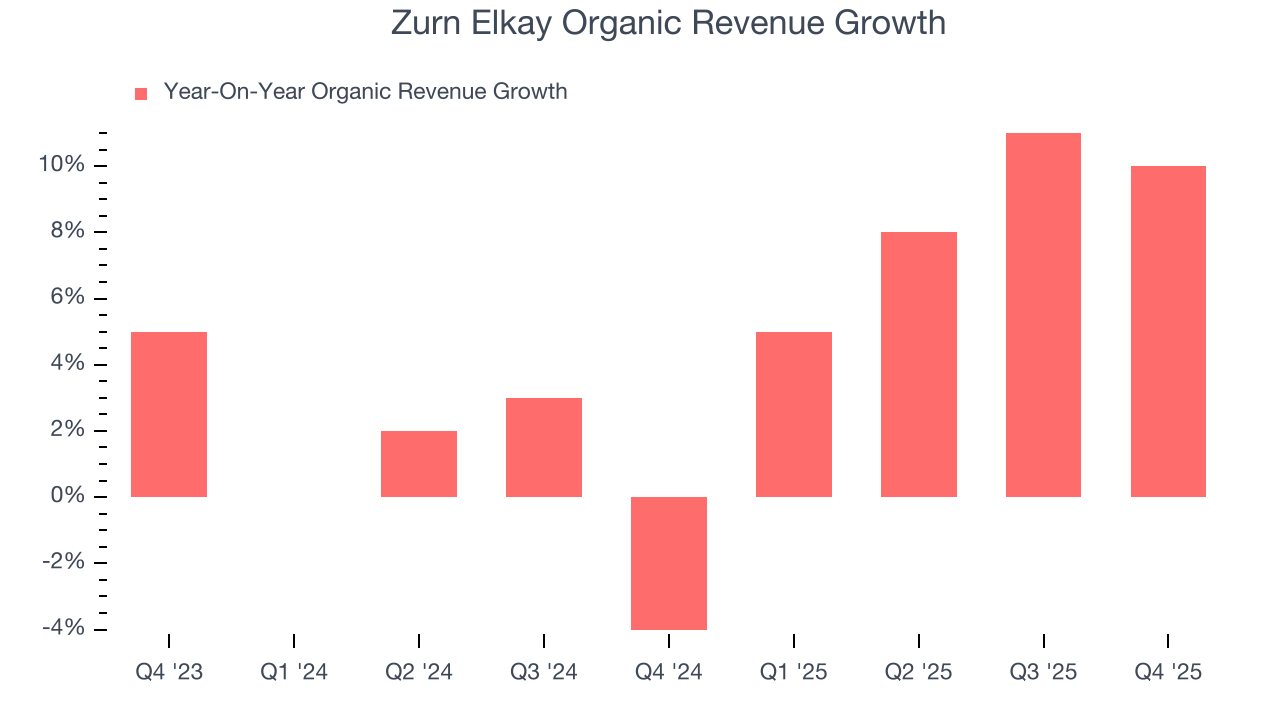

- Organic Revenue rose 10% year on year

- Market Capitalization: $7.85 billion

Company Overview

Claiming to have saved more than 30 billion gallons of water, Zurn Elkay (NYSE:ZWS) provides water management solutions to various industries.

Specifically, the company's systems seek to conserve water and improve hygiene in public, commercial, and residential settings. Its solutions include professional-grade water safety and control products, flow system products, hygienic and environmental products, and filtered drinking water products for public and private use.

Zurn Elkay generates revenue through the sale of its water management products to a wide array of clientele, including construction firms, municipalities, commercial entities, and private residents. Sales are driven by both direct and distributor channels, with a significant portion of income potentially recurring due to the essential nature of water infrastructure maintenance and upgrades.

4. HVAC and Water Systems

Many HVAC and water systems companies sell essential, non-discretionary infrastructure for buildings. Since the useful lives of these water heaters and vents are fairly standard, these companies have a portion of predictable replacement revenue. In the last decade, trends in energy efficiency and clean water are driving innovation that is leading to incremental demand. On the other hand, new installations for these companies are at the whim of residential and commercial construction volumes, which tend to be cyclical and can be impacted heavily by economic factors such as interest rates.

Other companies in the water management solution industry include Watts Water (NYSE:WTS), Pentair (NYSE:PNR), and private company Sloan Valve.

5. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Unfortunately, Zurn Elkay struggled to consistently increase demand as its $1.70 billion of sales for the trailing 12 months was close to its revenue five years ago. This was below our standards and is a sign of lacking business quality.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Zurn Elkay’s annualized revenue growth of 5.3% over the last two years is above its five-year trend, but we were still disappointed by the results.

We can better understand the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Zurn Elkay’s organic revenue averaged 4.4% year-on-year growth. Because this number aligns with its two-year revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, Zurn Elkay reported year-on-year revenue growth of 9.8%, and its $407.2 million of revenue exceeded Wall Street’s estimates by 1.4%.

Looking ahead, sell-side analysts expect revenue to grow 5.2% over the next 12 months, similar to its two-year rate. This projection is underwhelming and indicates its newer products and services will not catalyze better top-line performance yet.

6. Gross Margin & Pricing Power

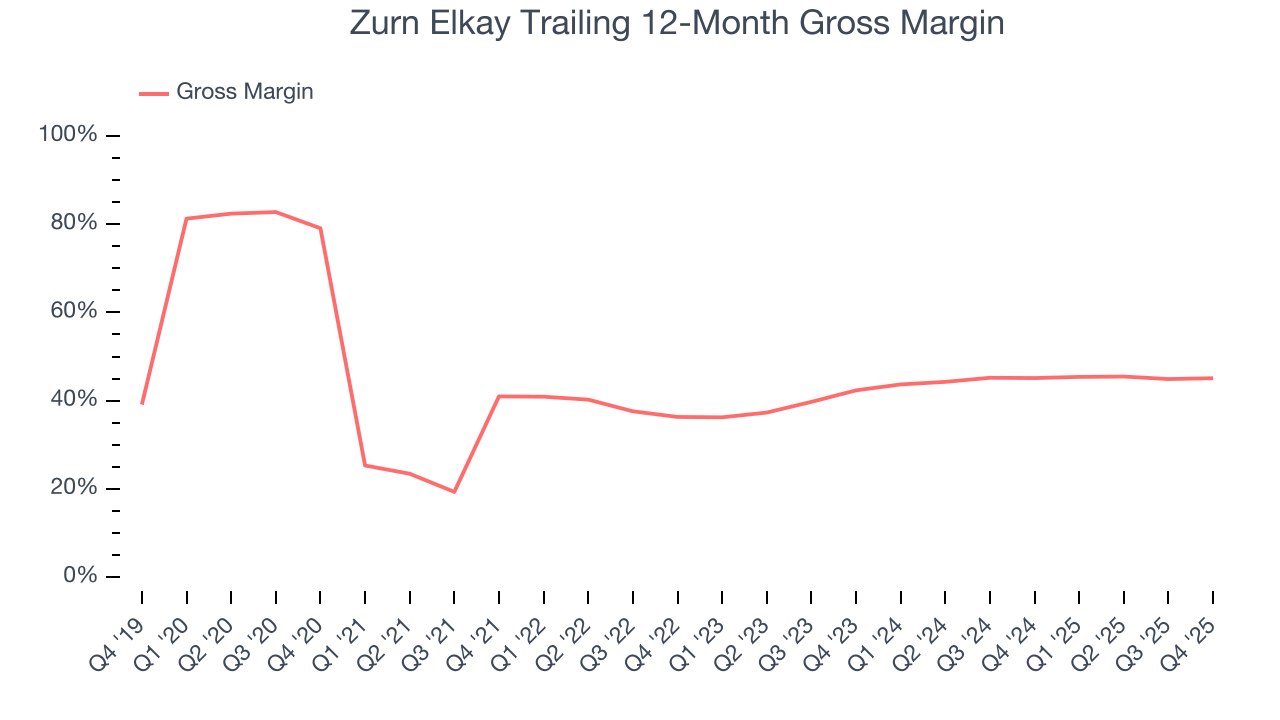

Zurn Elkay has best-in-class unit economics for an industrials company, enabling it to invest in areas such as research and development. Its margin also signals it sells differentiated products, not commodities. As you can see below, it averaged an elite 42.4% gross margin over the last five years. That means Zurn Elkay only paid its suppliers $57.65 for every $100 in revenue.

Zurn Elkay produced a 44.4% gross profit margin in Q4, in line with the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

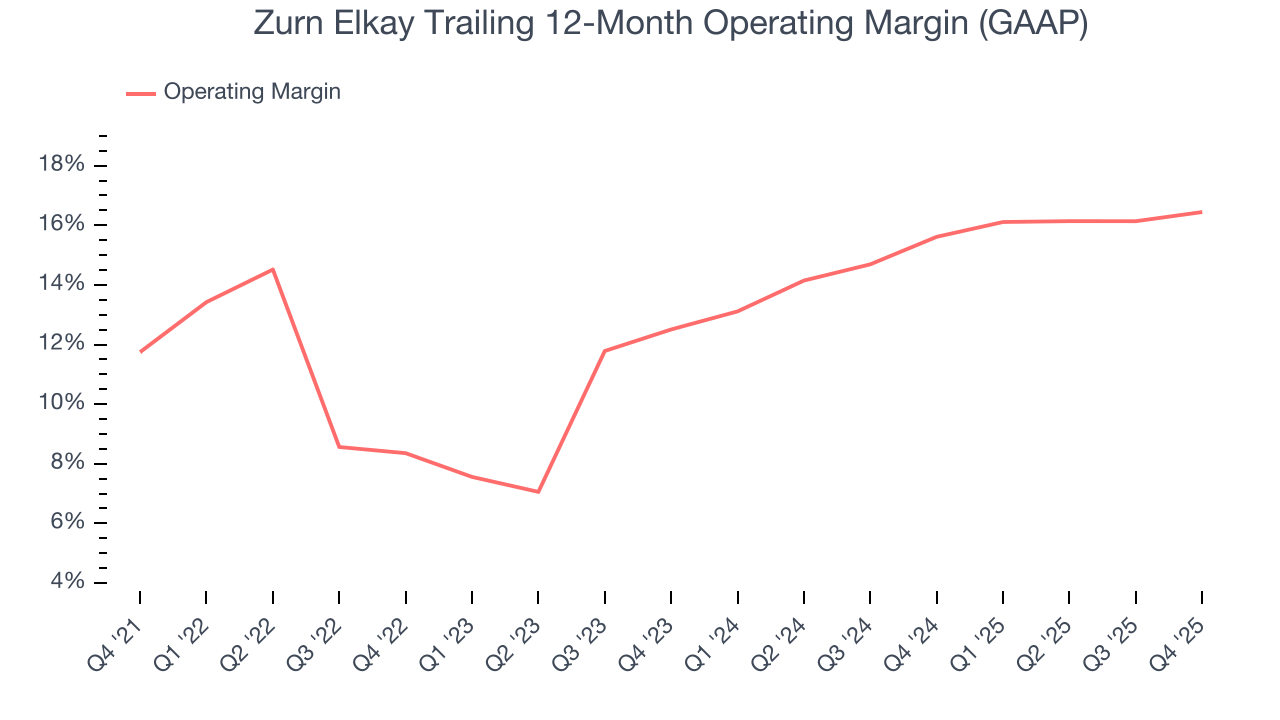

7. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Zurn Elkay has been an efficient company over the last five years. It was one of the more profitable businesses in the industrials sector, boasting an average operating margin of 13.3%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Looking at the trend in its profitability, Zurn Elkay’s operating margin rose by 4.7 percentage points over the last five years, showing its efficiency has improved.

In Q4, Zurn Elkay generated an operating margin profit margin of 14.8%, up 1.5 percentage points year on year. The increase was encouraging, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

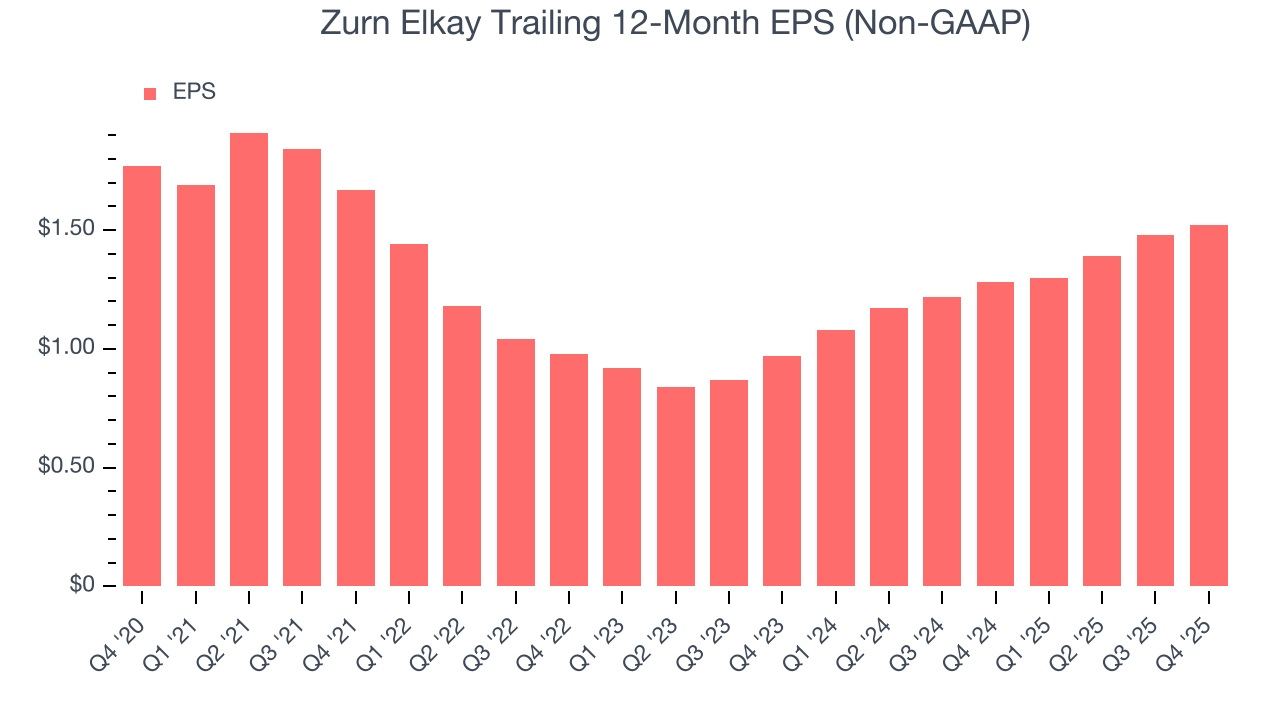

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Zurn Elkay, its EPS declined by 3% annually over the last five years while its revenue was flat. However, its operating margin actually improved during this time, telling us that non-fundamental factors such as interest expenses and taxes affected its ultimate earnings.

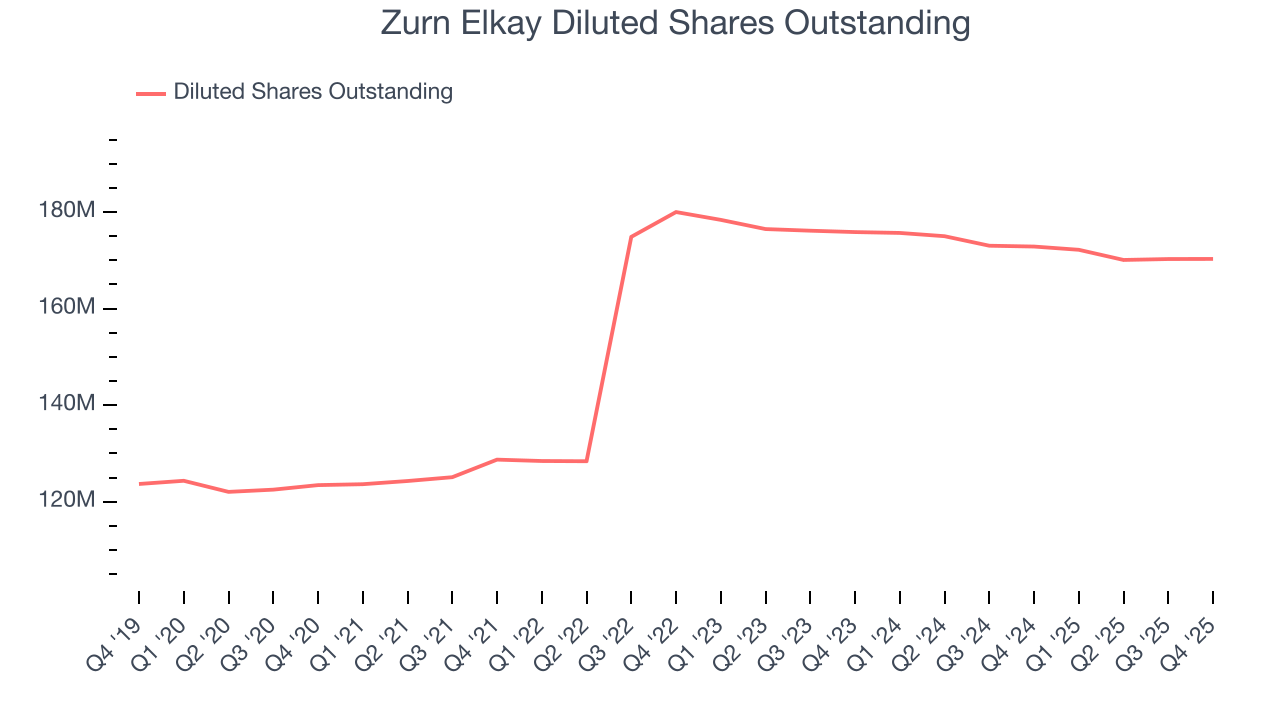

We can take a deeper look into Zurn Elkay’s earnings to better understand the drivers of its performance. A five-year view shows Zurn Elkay has diluted its shareholders, growing its share count by 38%. This dilution overshadowed its increased operational efficiency and has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Zurn Elkay, its two-year annual EPS growth of 25.2% was higher than its five-year trend. This acceleration made it one of the faster-growing industrials companies in recent history.

In Q4, Zurn Elkay reported adjusted EPS of $0.36, up from $0.32 in the same quarter last year. This print beat analysts’ estimates by 5.9%. Over the next 12 months, Wall Street expects Zurn Elkay’s full-year EPS of $1.52 to grow 8.5%.

9. Cash Is King

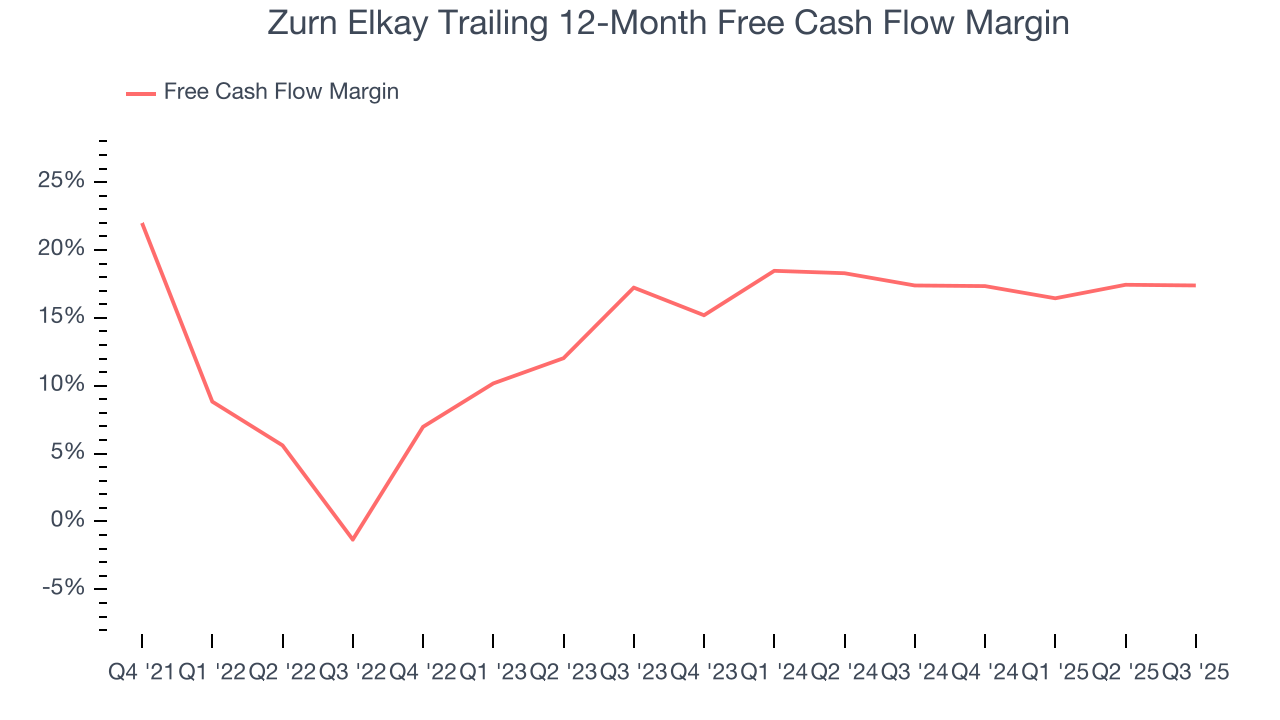

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Zurn Elkay has shown terrific cash profitability, putting it in an advantageous position to invest in new products, return capital to investors, and consolidate the market during industry downturns. The company’s free cash flow margin was among the best in the industrials sector, averaging 15.6% over the last five years.

Taking a step back, we can see that Zurn Elkay’s margin dropped by 14.9 percentage points during that time. If its declines continue, it could signal increasing investment needs and capital intensity.

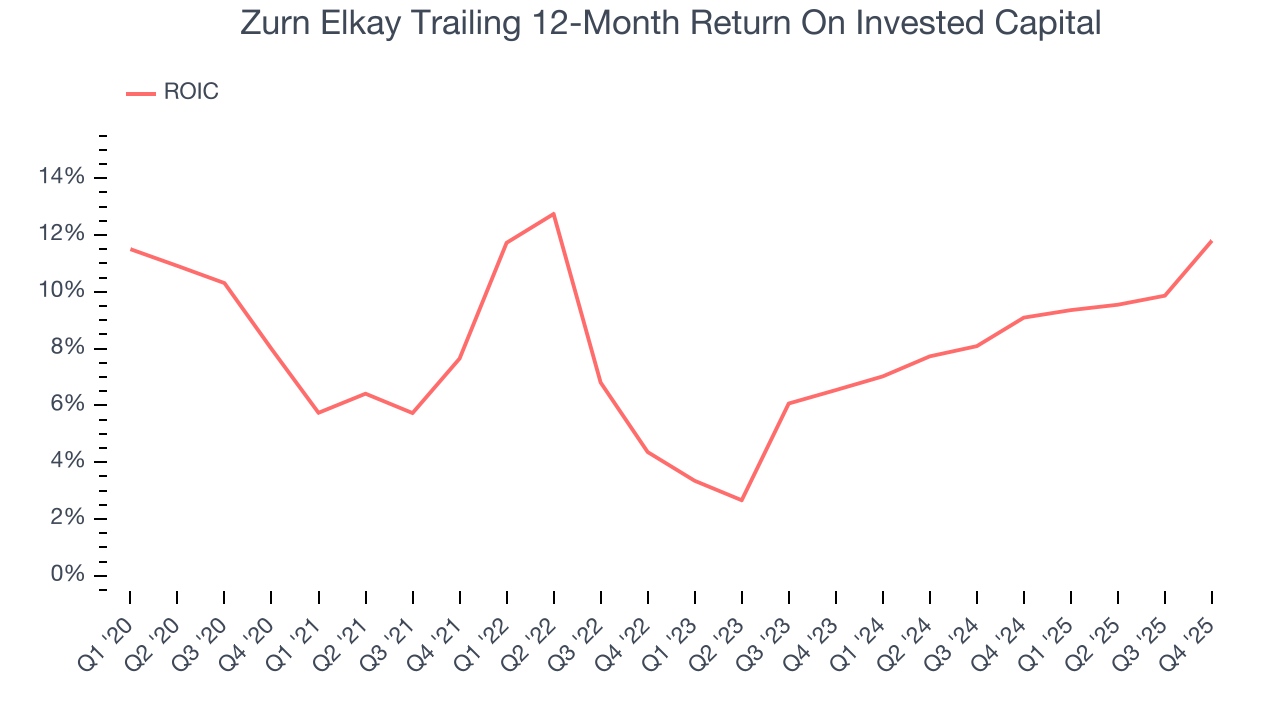

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Zurn Elkay historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 7.9%, somewhat low compared to the best industrials companies that consistently pump out 20%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Zurn Elkay’s ROIC averaged 4.4 percentage point increases each year. This is a good sign, and we hope the company can continue improving.

11. Balance Sheet Assessment

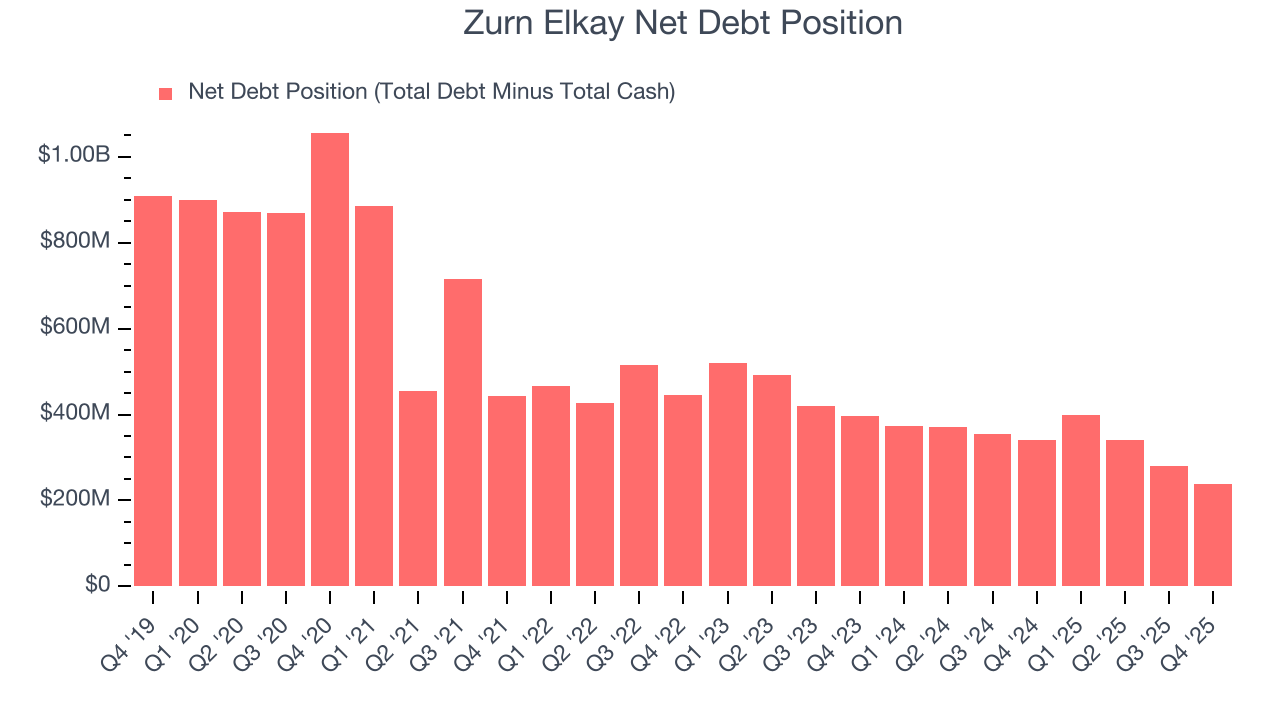

Zurn Elkay reported $300.5 million of cash and $538.5 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $442.2 million of EBITDA over the last 12 months, we view Zurn Elkay’s 0.5× net-debt-to-EBITDA ratio as safe. We also see its $28.6 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Zurn Elkay’s Q4 Results

It was good to see Zurn Elkay narrowly top analysts’ revenue expectations this quarter. We were also happy its EBITDA outperformed Wall Street’s estimates. Overall, we think this was a solid quarter with some key areas of upside. The stock remained flat at $47 immediately after reporting.

13. Is Now The Time To Buy Zurn Elkay?

Updated: February 3, 2026 at 10:16 PM EST

Before deciding whether to buy Zurn Elkay or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

Zurn Elkay isn’t a terrible business, but it isn’t one of our picks. For starters, its revenue growth was weak over the last five years. And while its powerful free cash flow generation enables it to stay ahead of the competition through consistent reinvestment of profits, the downside is its declining EPS over the last five years makes it a less attractive asset to the public markets. On top of that, its cash profitability fell over the last five years.

Zurn Elkay’s P/E ratio based on the next 12 months is 28.4x. Investors with a higher risk tolerance might like the company, but we think the potential downside is too great. We're fairly confident there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $51.22 on the company (compared to the current share price of $48.03).