Dropbox's (NASDAQ:DBX) Q1 Earnings Results: Revenue In Line With Expectations

Adam Hejl /

May 5, 2022

Cloud storage and e-signature company Dropbox (Nasdaq: DBX) reported results in line with analyst expectations in Q1 FY2022 quarter, with revenue up 9.92% year on year to $562.4 million. Dropbox made a GAAP profit of $79.7 million, improving on its profit of $47.6 million, in the same quarter last year.

Is now the time to buy Dropbox? Access our full analysis of the earnings results here, it's free.

Dropbox (DBX) Q1 FY2022 Highlights:

- Revenue: $562.4 million vs analyst estimates of $559 million (small beat)

- EPS (non-GAAP): $0.38 vs analyst estimates of $0.38 (small beat)

- Free cash flow of $130.7 million, down 19% from previous quarter

- Customers: 17,090,000, up from 16,790,000 in previous quarter

- Gross Margin (GAAP): 79.9%, up from 78.6% same quarter last year

“2022 is off to a strong start as we launched new functionality and features across Backup, Shop and document workflows with HelloSign, DocSend and PDF editing; all designed to help customers organize, secure, and do more with their digital content,” said Dropbox Co-Founder and Chief Executive Officer Drew Houston.

Founded by the long-serving CEO Drew Houston and Arash Ferdowsi in 2007, Dropbox (NASDAQ:DBX) provides a file hosting cloud platform that helps organizations collaborate and share documents.

The catch phrase 'digital transformation' orginally referred to the digitization of documents within enterprises. The growth of digital documents has spurred an explosion of collaboration within and between businesses, which in turn is driving the demand for e-signature and content management platforms.

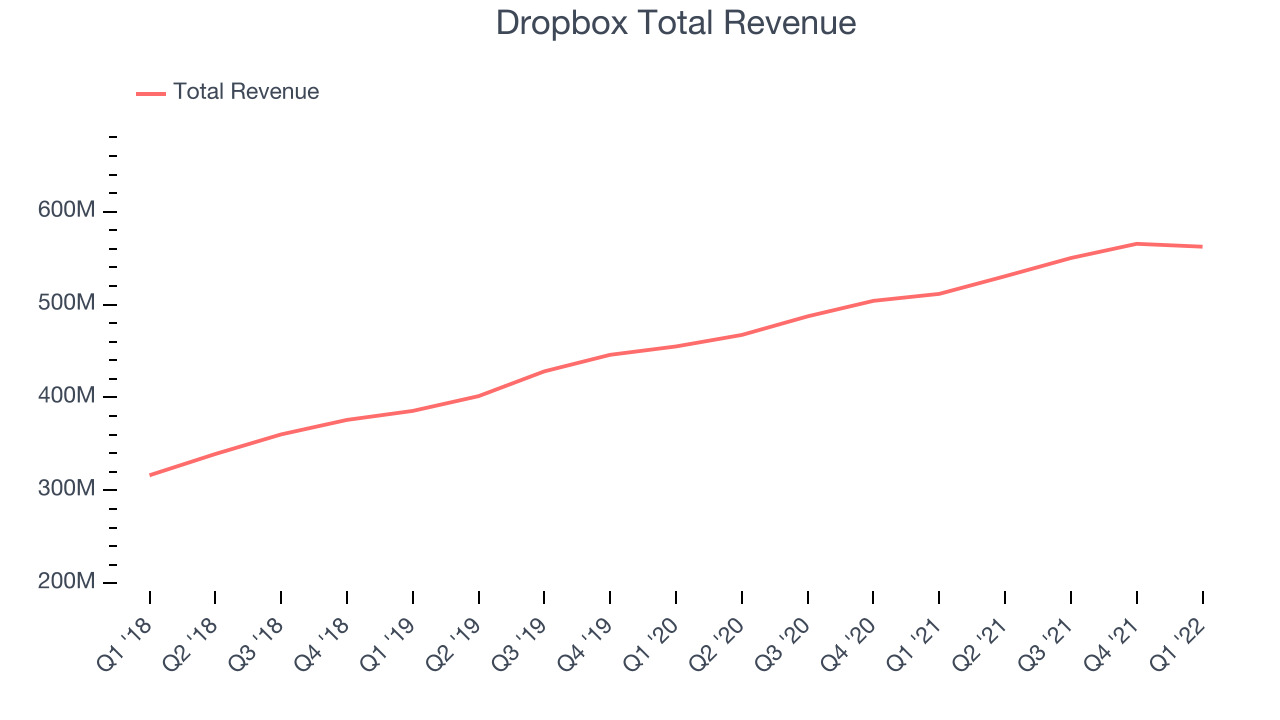

Sales Growth

As you can see below, Dropbox's revenue growth has been slower over the last year, growing from quarterly revenue of $511.6 million, to $562.4 million.

Dropbox's quarterly revenue was only up 9.92% year on year, which would likely disappoint many shareholders. But the revenue actually decreased by $3.1 million in Q1, compared to $15.3 million increase in Q4 2021.

Ahead of the earnings results the analysts covering the company were estimating sales to grow 7.49% over the next twelve months.

There are others doing even better than Dropbox. Founded by ex-Google engineers, a small company making software for banks has been growing revenue 90% year on year and is already up more than 150% since the IPO last December. You can find it on our platform for free.

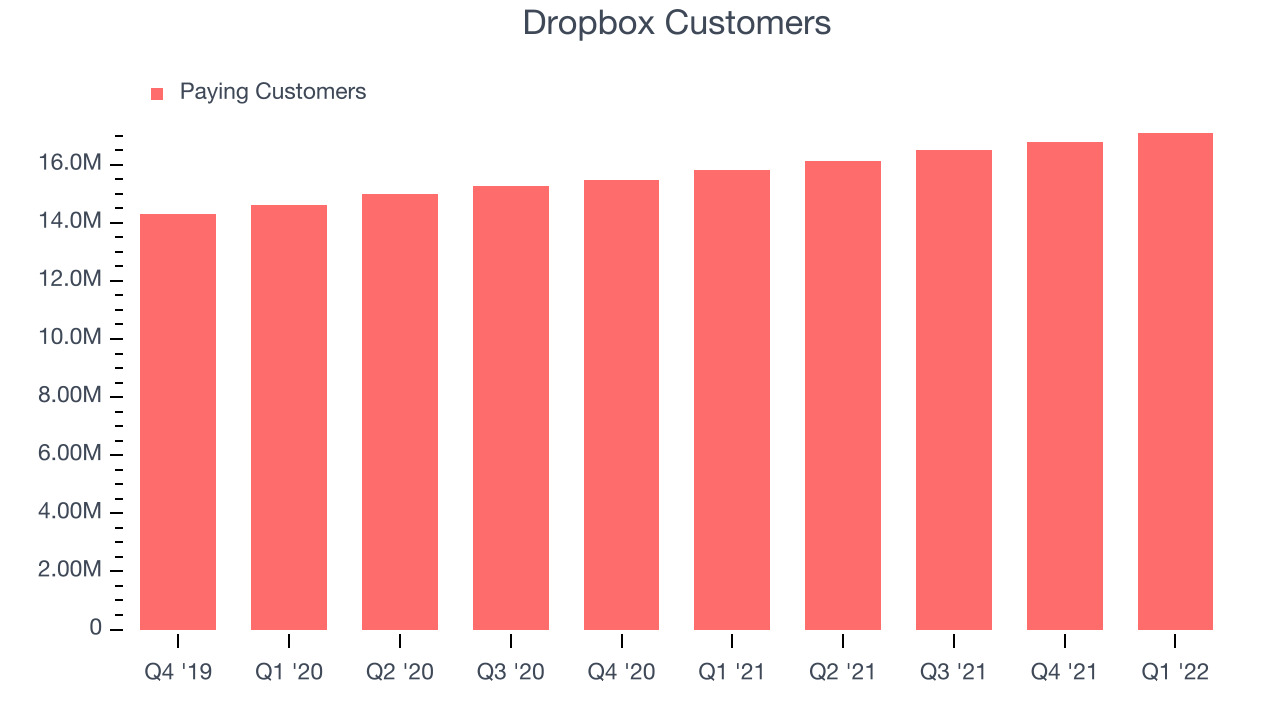

Customer Growth

You can see below that Dropbox reported 17,090,000 customers at the end of the quarter, an increase of 300,000 on last quarter. That's in line with the customer growth we have seen over the last couple of quarters, suggesting that the company can maintain its current sales momentum.

Key Takeaways from Dropbox's Q1 Results

With a market capitalization of $8.46 billion Dropbox is among smaller companies, but its more than $1.49 billion in cash and positive free cash flow over the last twelve months give us confidence that Dropbox has the resources it needs to pursue a high growth business strategy.

Dropbox reported results in line with estimates, with robust free cash flow. On the other hand, revenue growth is slower these days. The company is up 1.96% on the results and currently trades at $21.75 per share.

Should you invest in Dropbox right now? It is important that you take into account its valuation and business qualities, as well as what happened in the latest quarter. We look at that in our actionable report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 70% year on year and best-in-class SaaS metrics it should definitely be on your radar.

The author has no position in any of the stocks mentioned.