Five9 (NASDAQ:FIVN) Beats Q4 Sales Targets But Stock Drops

Adam Hejl /

February 22, 2023

Call center software provider Five9 (NASDAQ: FIVN) reported Q4 FY2022 results topping analyst expectations, with revenue up 20% year on year to $208.3 million. The company expects that next quarter's revenue would be around $207.5 million, which is the midpoint of the guidance range. That was in roughly line with analyst expectations. Five9 made a GAAP loss of $13.7 million, down on its loss of $3.6 million, in the same quarter last year.

Is now the time to buy Five9? Access our full analysis of the earnings results here, it's free.

Five9 (FIVN) Q4 FY2022 Highlights:

- Revenue: $208.3 million vs analyst estimates of $204.4 million (1.92% beat)

- EPS (non-GAAP): $0.54 vs analyst estimates of $0.41 (30.5% beat)

- Revenue guidance for Q1 2023 is $207.5 million at the midpoint, slightly below analyst estimates of $209 million

- Management's revenue guidance for upcoming financial year 2023 is $901.5 million at the midpoint, in line with analyst expectations and predicting 15.7% growth (vs 28.2% in FY2022)

- Free cash flow of $25 million, up 32% from previous quarter

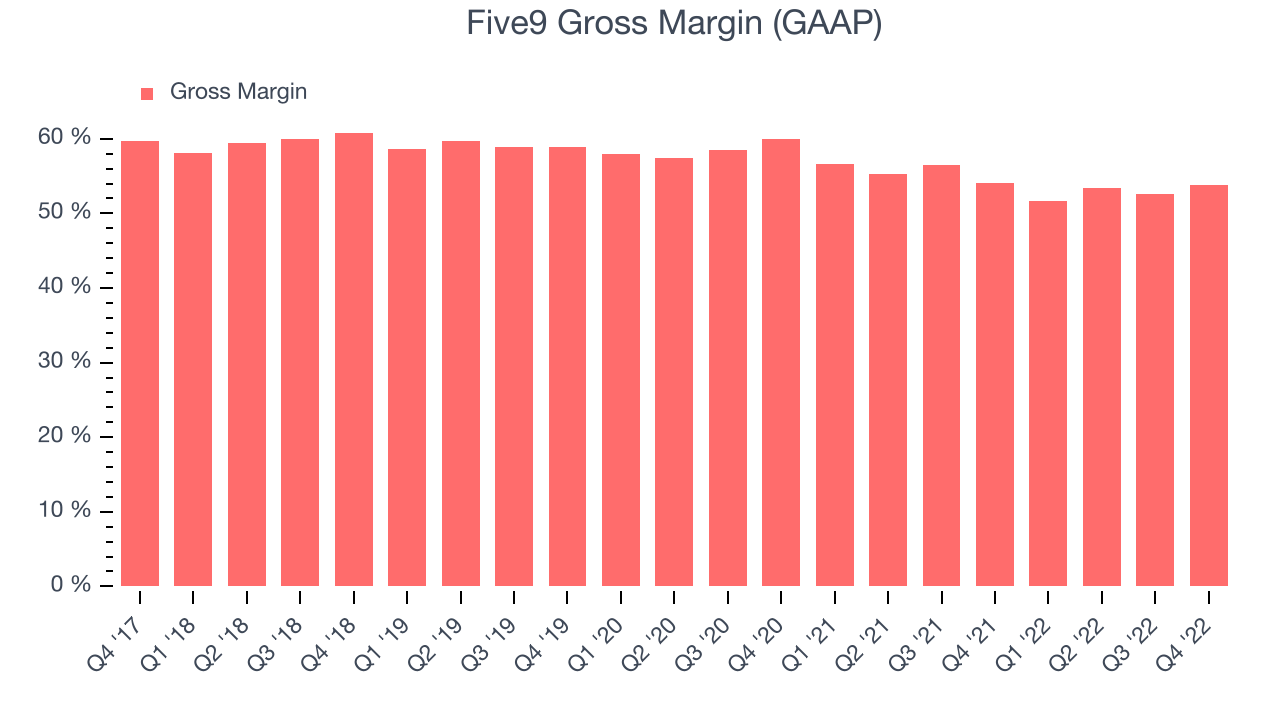

- Gross Margin (GAAP): 53.8%, in line with same quarter last year

“We are pleased to report strong fourth quarter results with revenue growing 20% year-over-year to a record $208.3 million. This growth was driven by the continued strength of our Enterprise business where LTM subscription revenue grew 32% year-over-year. Our investments in international expansion are also paying off as our 2022 international revenue grew 44%. In the fourth quarter, we achieved another record for operating cash flow, driven by adjusted EBITDA margin reaching 22%. As we execute against a massive and underpenetrated opportunity, we continue to march up-market, expand internationally and deliver innovation. Speaking of which, we are excited to announce two new product offerings that leverage GPT-3 from OpenAI, namely AI Insights and AI Summaries. .”

Started in 2001, Five9 (NASDAQ: FIVN) offers software as a service that makes it easier for companies to set up and efficiently run call centers, and offer more tailored customer support.

Work is becoming more distributed, both across geographies and devices. In order for businesses to keep functioning efficiently, they need to be able to communicate as well as they did when the teams were co-located, which drives the demand for integrated communication platforms.

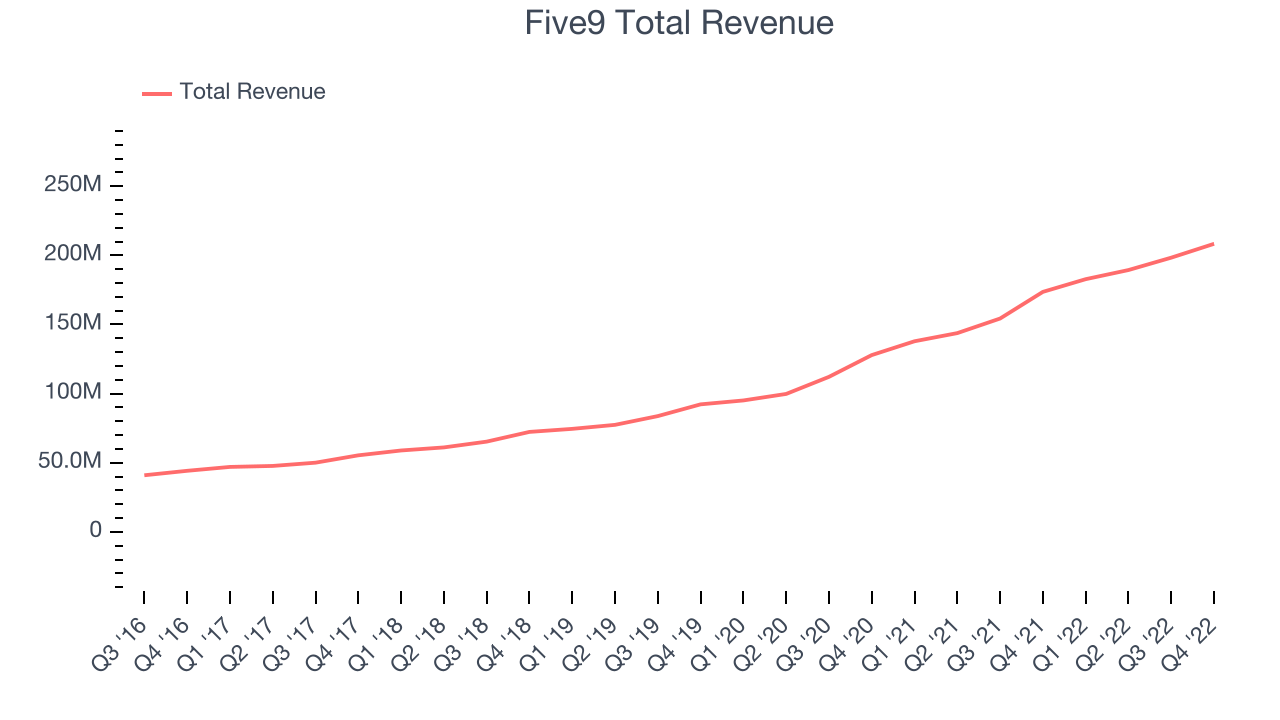

Sales Growth

As you can see below, Five9's revenue growth has been very strong over the last two years, growing from quarterly revenue of $127.9 million in Q4 FY2020, to $208.3 million.

This quarter, Five9's quarterly revenue was once again up a very solid 20% year on year. On top of that, revenue increased $10 million quarter on quarter, a solid improvement on the $8.96 million increase in Q3 2022. Happily, that's a slight re-acceleration of growth.

Guidance for the next quarter indicates Five9 is expecting revenue to grow 13.5% year on year to $207.5 million, slowing down from the 32.6% year-over-year increase in revenue the company had recorded in the same quarter last year. For the upcoming financial year management expects revenue to be $901.5 million at the midpoint, growing 15.7% compared to 27.8% increase in FY2022.

In volatile times like these we look for robust businesses with strong pricing power. Unknown to most investors, this company is one of the highest-quality software companies in the world, and their software products have been the default standard in critical industries for decades. The result is an impressive business that is up an incredible 18,152% since the IPO. You can find it on our platform for free.

Profitability

What makes the software as a service business so attractive is that once the software is developed, it typically shouldn't cost much to provide it as an ongoing service to customers. Five9's gross profit margin, an important metric measuring how much money there is left after paying for servers, licenses, technical support and other necessary running expenses was at 53.8% in Q4.

That means that for every $1 in revenue the company had $0.54 left to spend on developing new products, marketing & sales and the general administrative overhead. While it improved significantly from the previous quarter this would still be considered a low gross margin for a SaaS company and we would like to see the improvements continue.

Key Takeaways from Five9's Q4 Results

With a market capitalization of $5.55 billion Five9 is among smaller companies, but its more than $614.3 million in cash and positive free cash flow over the last twelve months give us confidence that Five9 has the resources it needs to pursue a high growth business strategy.

It was good to see Five9 improve their gross margin this quarter. And we were also happy to see it topped analysts’ revenue expectations, even if just narrowly. On the other hand, the in-line revenue guidance for next year indicates a significant slowdown. Overall, it seems to us that this was a mixed quarter for Five9. The company is flat on the results and currently trades at $81.5 per share.

Five9 may have had a tough quarter, but does that actually create an opportunity to invest right now? It is important that you take into account its valuation and business qualities, as well as what happened in the latest quarter. We look at that in our actionable report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 70% year on year and best-in-class SaaS metrics it should definitely be on your radar.

The author has no position in any of the stocks mentioned.