Tenable (NASDAQ:TENB) Q2: Beats On Revenue, Stock Soars

Anthony Lee /

July 25, 2023

Cybersecurity software maker Tenable (NASDAQ:TENB) reported Q2 FY2023 results exceeding Wall Street analysts' expectations, with revenue up 18.7% year on year to $195 million. Guidance for next quarter's revenue was also $198 million at the midpoint, 1.82% above Consensus. Tenable made a GAAP loss of $16 million, improving from its loss of $27.5 million in the same quarter last year.

Is now the time to buy Tenable? Find out by accessing our full research report free of charge.

Tenable (TENB) Q2 FY2023 Highlights:

- Revenue: $195 million vs analyst estimates of $188.5 million (3.47% beat)

- EPS (non-GAAP): $0.22 vs analyst estimates of $0.12 ($0.10 beat)

- Revenue guidance for Q3 2023 is $198 million at the midpoint, above analyst estimates of $194.5 million

- The company reconfirmed revenue guidance for the full year of $787 million at the midpoint

- Free cash flow of $27.7 million, down 25.8% from the previous quarter

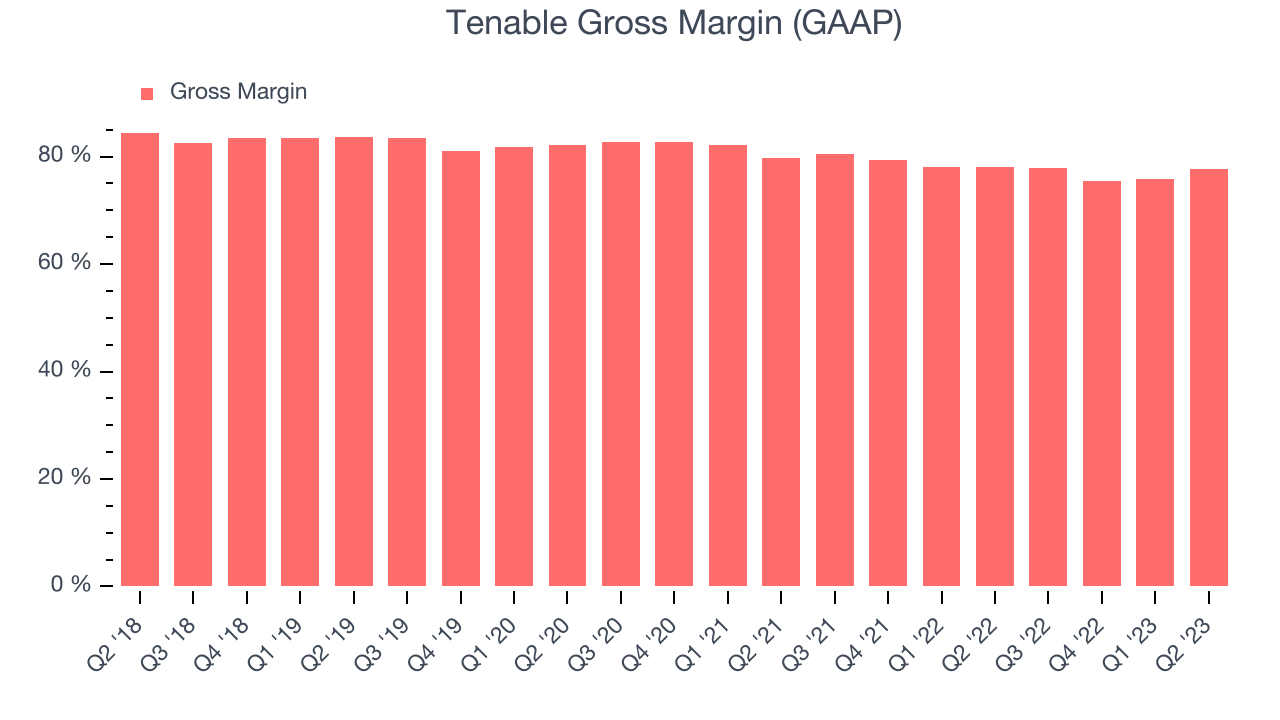

- Gross Margin (GAAP): 77.7%, in line with the same quarter last year

"We are very pleased with our Q2 results, which included better than expected top-line growth and a sizable beat in earnings," said Amit Yoran, Chairman and CEO of Tenable.

Founded in 2002 by three cybersecurity veterans, Tenable (NASDAQ:TENB) provides software as a service that helps companies understand where they are exposed to cyber security risk and how to reduce it.

The demand for cybersecurity is growing as more and more businesses are moving their data and processes into the cloud, which along with a major increase in employees working remotely, has increased their exposure to attacks and malware. Additionally, the growing array of corporate IT systems, applications and internet connected devices has increased the complexity of network security, all of which has substantially increased the demand for software meant to protect data breaches.

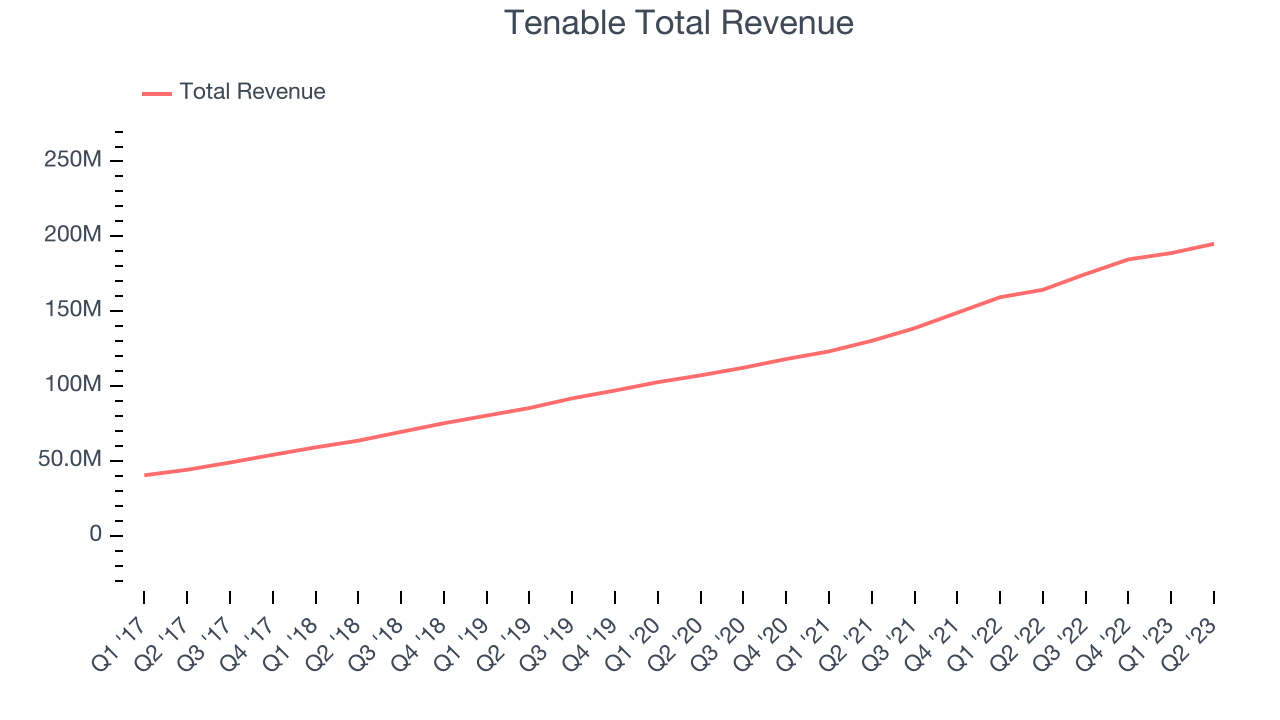

Sales Growth

As you can see below, Tenable's revenue growth has been over the last two years, growing from $130.3 million in Q2 FY2021 to $195 million this quarter.

This quarter, Tenable's quarterly revenue was once again up 18.7% year on year. We can see that Tenable's revenue increased by $6.2 million quarter on quarter, which is a solid improvement from the $4.21 million increase in Q1 2023. Shareholders should applaud the acceleration of growth.

Next quarter's guidance suggests that Tenable is expecting revenue to grow 13.2% year on year to $198 million, slowing down from the 26.1% year-on-year increase it recorded in the same quarter last year. Ahead of the earnings results announcement, the analysts covering the company were expecting sales to grow 11.8% over the next 12 months.

In volatile times like these, we look for robust businesses with strong pricing power. Overlooked by most investors, this company is one of the highest-quality software companies in the world, and its software products have been the gold standard in critical industries for decades. The result is an impressive business that's up an incredible 18,000%+ since its IPO. You can find it on our platform for free.

Profitability

What makes the software as a service business so attractive is that once the software is developed, it typically shouldn't cost much to provide it as an ongoing service to customers. Tenable's gross profit margin, an important metric measuring how much money there's left after paying for servers, licenses, technical support, and other necessary running expenses, was 77.7% in Q2.

That means that for every $1 in revenue the company had $0.78 left to spend on developing new products, sales and marketing, and general administrative overhead. Significantly up from the last quarter, Tenable's impressive gross margin allows it to fund large investments in product and sales during periods of rapid growth and achieve profitability when reaching maturity.

Key Takeaways from Tenable's Q2 Results

Sporting a market capitalization of $4.98 billion, Tenable is among smaller companies, but its more than $645.5 million in cash on hand and positive free cash flow over the last 12 months puts it in an attractive position to invest in growth.

It was great to see Tenable improve its gross margin this quarter. We were also glad that its revenue growth and EPS outperformed Wall Street's expectations. Additionally, both revenue and non-GAAP operating profit guidance for next quarter and for the full year exceeded expectations. Overall, this quarter's results seemed quite positive and shareholders should feel optimistic. The stock is up 10.5% after reporting and currently trades at $48.39 per share.

So should you invest in Tenable right now? When making that decision, it's important to consider its valuation, business qualities, and what's happened in the latest quarter. We cover this and more in our full company report, and it's free.

Looking for more investment opportunities? One way to find them is to watch for paradigm shifts, just like how every company in the world is slowly becoming a technology company and facing increasing cybersecurity risks. This company is leading the charge in cyber defense with its cloud-native cybersecurity solutions while generating best-in-class revenue growth and SaaS performance metrics. It should definitely be on your radar.

The author has no position in any of the stocks mentioned in this report.